Table of Contents

Overview

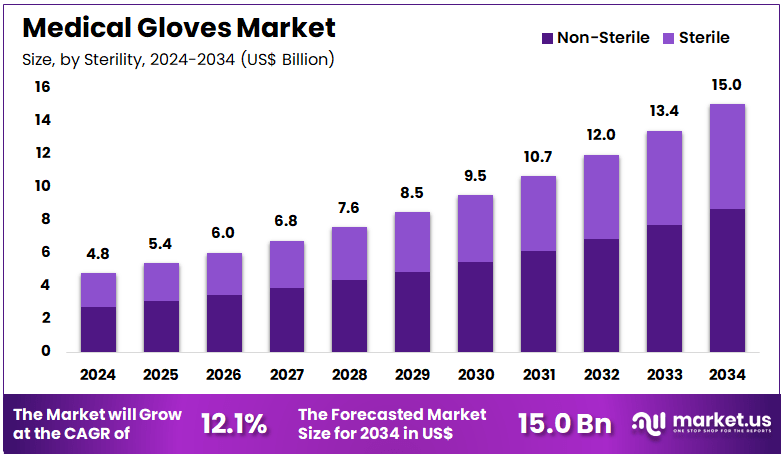

New York, NY – Nov 20, 2025 – The Global Medical Gloves Market size is expected to be worth around US$ 15.0 Billion by 2034 from US$ 4.8 Billion in 2024, growing at a CAGR of 12.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.7% share with a revenue of US$ 2.0 Billion.

The medical gloves market has been positioned for steady expansion as demand for protective equipment continues to rise across healthcare settings. Growth has been supported by the increasing incidence of infectious diseases, where a heightened emphasis on hygiene has strengthened the adoption of disposable examination and surgical gloves. The use of these products has been reinforced by stringent regulations designed to ensure patient and provider safety, which has contributed to sustained consumption in hospitals, clinics, and ambulatory care centers.

The market has been influenced by the widespread preference for nitrile gloves due to their strong puncture resistance and favorable chemical protection profile. Latex gloves have remained present in several applications, although concerns regarding allergic reactions have encouraged gradual product substitution. Vinyl gloves continue to serve as cost-effective options in non-critical procedures, allowing flexibility across diverse medical environments.

The expansion of healthcare infrastructure in emerging economies has generated additional demand. Investments in public health systems and the growth of private sector facilities have supported higher utilization rates, particularly in high-volume examination settings. Production capacity has been strengthened globally, as manufacturers have focused on automation and improved material technologies to ensure consistent quality and supply stability.

The market outlook remains cautiously optimistic. The growth of the sector can be attributed to continuous infection-control initiatives, rising surgical volumes, and increasing awareness of worker protection standards. Continued product innovation and supply chain improvements are expected to enhance reliability and support long-term market development.

Key Takeaways

- The medical gloves market recorded revenue of US$ 4.8 billion in 2024, progressing at a CAGR of 12.1%, and is projected to attain US$ 15.0 billion by 2033.

- By product type, the market is categorized into latex, vinyl, nitrile, neoprene, and others, with nitrile gloves accounting for 49.5% of the share in 2024.

- Based on form, the market is divided into powder-free and powdered gloves, where powder-free variants represented 61.7% of the total share.

- In terms of sterility, the segmentation includes sterile and non-sterile gloves, with the non-sterile segment dominating at 57.5%.

- The distribution channel segment comprises offline and online platforms, and the offline channel held 63.2% of the revenue share.

- By end-user, the market is segmented into hospitals, clinics, ambulatory surgical centers, diagnostic centers, and others, with hospitals capturing 54.3% of the market share.

- Regionally, North America led the global market, contributing 42.7% of the share in 2024.

Regional Analysis

North America Remains the Leading Regional Market

North America maintained its position as the leading market for medical gloves, holding a substantial revenue share of 42.7%. This dominance has been supported by increased utilization of healthcare services and stronger adherence to infection control practices. A notable rise in hospital admissions was documented by the US Centers for Disease Control and Prevention (CDC), indicating a 50% increase in December 2023, which contributed to higher consumption of personal protective equipment, including medical gloves.

Further momentum was generated by regulatory activity, as the US Food and Drug Administration (FDA) approved a record number of new medical devices in 2023, many of which required strict infection control protocols. In addition, the US Department of Health and Human Services (HHS) allocated US$500 million in 2023 to strengthen national stockpiles of essential medical supplies, including gloves. These factors collectively reinforced the demand for medical gloves in the region.

Asia Pacific Expected to Record the Fastest Growth

The Asia Pacific region is anticipated to exhibit the highest CAGR during the forecast period due to rapid expansion of healthcare infrastructure and increasing emphasis on infection prevention. In India, the Ministry of Health and Family Welfare (MoHFW) raised funding for digital health initiatives by 20% in 2023, strengthening hospital capabilities, including infection control tools.

In China, the National Health Commission (NHC) reported higher procurement of medical consumables in 2022, especially within rural healthcare systems, highlighting rising glove usage. Japan’s Ministry of Health, Labour, and Welfare (MHLW) allocated US$45 million in 2023 to upgrade laboratory capabilities, emphasizing improved infection control. Additionally, the Australian Department of Health invested US$100 million in 2022 to expand telehealth services, indirectly supporting increased glove utilization. These initiatives are expected to drive robust market growth throughout Asia Pacific.

What trends have been observed in medical glove usage per patient encounter in major healthcare systems?

Across major healthcare systems, glove use per patient encounter has increased markedly over the past two decades, driven by universal precautions, rising procedure volumes, and infection-prevention standards. Consensus guidelines emphasising routine gloving for direct patient contact have contributed to this structural rise.

In intensive care units, observational data indicate extremely high utilisation, with more than 100 disposable gloves used per patient per day in some critical care settings. On general wards, quality-improvement work has reported average consumption of about 33–34 gloves per occupied bed-day, with unit-level ranges from roughly 27 to 41 gloves, illustrating wide variation in practice patterns between services and over time.

The COVID-19 pandemic produced a transient surge in glove use per encounter, although some hospital procurement analyses suggest that glove volumes stabilised more quickly than other PPE categories. Recent evidence and policy statements now highlight that over-gloving does not necessarily reduce infection risk and may worsen hand-hygiene compliance, increase healthcare-associated infections, and add substantially to plastic waste and cost.

Consequently, current trends in leading systems include targeted de-implementation of unnecessary gloving, reinforcement of “gloves are not a substitute for hand hygiene,” and monitoring glove use per patient-day as a stewardship and sustainability metric.

Emerging Trends

- Integration of Hand Hygiene With Glove Use: The coordination of glove use with hand hygiene protocols has been strengthened. It has been recognized that gloves can become contaminated at the same rate as bare hands. Updated WHO guidelines emphasize that gloves must be removed after each patient interaction, followed immediately by proper hand hygiene, supporting adherence to the “5 Moments for Hand Hygiene” framework.

- Shift Toward Nitrile and Other Non-Latex, Non-Powdered Gloves: The transition toward nitrile and other non-latex materials has been driven by concerns related to latex sensitivity and environmental impact. Reports indicate that up to 12% of healthcare workers experience latex-related skin reactions. Non-powdered gloves are being favored to avoid powder-associated complications.

- Increasing Focus on Sustainability and Waste Reduction: The rise in glove consumption has contributed substantially to healthcare waste volumes. A 2021 WHO assessment indicated that only 54% of facilities possessed basic waste management services. Current initiatives aim to optimize glove utilization, ensuring gloves are used strictly when required, thereby reducing waste generation and mitigating environmental burden.

- Advancement in Chemically Resistant Glove Materials: Research activity has intensified to address existing gaps in protection against hazardous substances, including chemotherapy agents and high-potency opioids. Material innovation is progressing toward gloves engineered with enhanced barrier properties capable of resisting permeation by antineoplastic drugs and emerging chemical threats.

Frequently Asked Questions on Medical Gloves

- What are medical gloves?

Medical gloves are protective hand coverings used in healthcare environments to prevent contamination between patients and providers. Their utilization supports infection control procedures and ensures safe handling of biological materials, thereby reducing the risk of cross-transmission during medical interventions. - What materials are used to manufacture medical gloves?

Medical gloves are typically produced from latex, nitrile, vinyl, and neoprene. The choice of material depends on required durability, tactile sensitivity, and allergy considerations. Nitrile and vinyl alternatives have gained widespread adoption due to improved puncture resistance and minimized allergy risks. - Why are medical gloves important in healthcare settings?

Medical gloves are essential because they minimize exposure to infectious agents while supporting sterile procedures. Their consistent usage enhances patient safety, reduces contamination incidents, and maintains clinical hygiene standards across hospitals, laboratories, and diagnostic environments dealing with routine or invasive activities. - What types of medical gloves are commonly used?

Common categories include examination gloves, surgical gloves, sterile gloves, and chemotherapy-rated gloves. Each type is designed to meet specific performance requirements related to tactile precision, sterility, durability, and chemical resistance, depending on the clinical procedure being undertaken. - What is driving growth in the medical gloves market?

Market growth is driven by rising healthcare expenditure, expanding infection prevention protocols, and increased surgical volume. The demand has been accelerated by heightened awareness of hygiene practices and regulatory emphasis on safety standards across global healthcare institutions and laboratories. - Which regions are leading the medical gloves market?

North America and Europe dominate due to strong healthcare infrastructure and strict safety regulations. However, rapid expansion in Asia-Pacific is observed, supported by rising hospital capacity, improved manufacturing capabilities, and increased public health awareness in developing economies. - Who are the major players in the medical gloves market?

Leading companies include Top Glove Corporation, Ansell Limited, Hartalega Holdings, and Medline Industries. Their market presence is strengthened through large production capacities, technological advancements, and strategic expansions across regions with rising demand for protective healthcare products.

Conclusion

The medical gloves market is expected to maintain steady expansion as infection-control measures, rising surgical volumes, and heightened hygiene awareness continue to drive sustained demand across healthcare settings. The preference for nitrile materials, the predominance of powder-free formats, and the strong uptake within hospitals underscore structural shifts in product usage.

Growth in emerging economies, supported by healthcare infrastructure development and public health investments, is projected to reinforce long-term consumption. With North America leading and Asia Pacific advancing rapidly, the sector’s outlook remains positive, supported by regulatory initiatives, technological improvements, and ongoing emphasis on safety and worker protection standards.Is this conversation helpful so far?

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)