Table of Contents

Overview

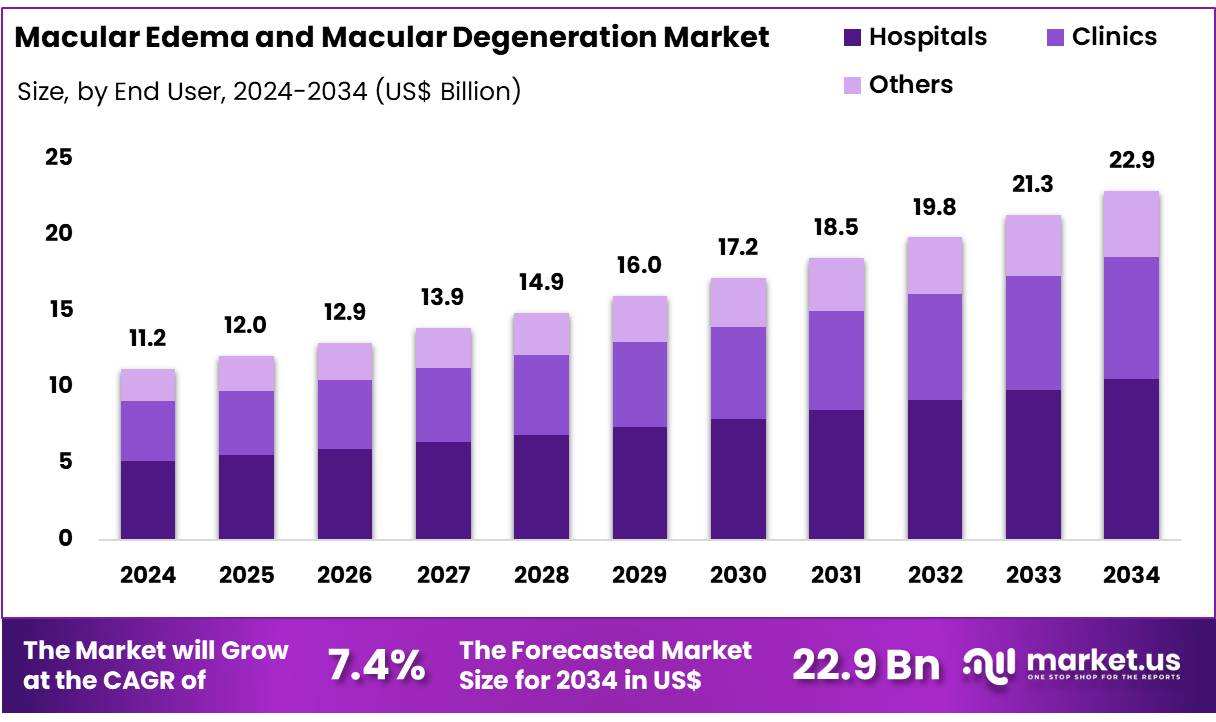

New York, NY – Nov 27, 2025 – Global Macular Edema and Macular Degeneration Market size is expected to be worth around US$ 22.9 Billion by 2034 from US$ 11.2 Billion in 2024, growing at a CAGR of 7.2% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 42.7% share with a revenue of US$ 4.7 Billion.

Macular disorders continue to receive significant attention as the prevalence of vision impairment increases worldwide. Macular edema and macular degeneration are recognized as two of the most common conditions affecting the central part of the retina, known as the macula. The macula is responsible for sharp, detailed, and central vision, and its deterioration can lead to considerable visual disability.

Macular edema occurs when fluid accumulates within the macula, causing swelling and distortion of vision. The development of this condition is most often linked to diabetic retinopathy, retinal vein occlusion, postoperative inflammation, and other underlying ocular diseases. The progression of macular edema can be slowed when early diagnosis and treatment are implemented. Therapeutic approaches generally include anti-VEGF injections, corticosteroids, and laser therapy. The demand for these treatments has been increasing as screening programs improve and awareness of retinal health strengthens.

Macular degeneration, particularly age-related macular degeneration (AMD), remains a major cause of vision loss among older adults. The growth of the aging population has been driving a steady rise in AMD cases. AMD is categorized into dry and wet forms, with the wet form accounting for the majority of severe vision loss. The advancement of imaging technologies and the introduction of innovative biologic therapies have supported early detection and improved management outcomes.

Greater emphasis on preventive eye care, routine retinal examinations, and timely intervention continues to play a central role in reducing the burden of macular diseases.

Key Takeaways

- The global macular edema and macular degeneration market is projected to reach US$ 22.9 billion by 2034, increasing from US$ 11.02 billion in 2024.

- The market is anticipated to expand at a CAGR of 7.2% between 2025 and 2034.

- Drug therapy accounted for the leading share of 63.4% in the treatment type segment in 2024.

- The macular edema application segment represented a dominant 29.3% share in 2024.

- The hospital end-use segment held the largest share at 46.2% in 2024.

- North America emerged as the leading regional market in 2024, contributing 42.7% share, equivalent to US$ 4.7 billion in revenue.

Regional Analysis

In 2024, North America maintained a leading position in the market, accounting for more than 72.7% of the total share and reaching a market value of US$ 4.7 billion. The dominance of the region is associated with the high prevalence of age-related macular degeneration (AMD). Estimates from the National Eye Institute indicate that AMD affects nearly one in ten individuals aged 50 years and above in the United States.

At the same time, diabetic macular edema (DME) continues to represent a significant clinical burden. Approximately 3.8% of U.S. adults aged 40 years and older with diabetes are affected, corresponding to about 746,000 people. Early detection is strongly supported by an advanced healthcare network, characterized by broad access to OCT imaging systems and specialized retina care centers. Favorable reimbursement structures under Medicare and private insurance plans have facilitated wider adoption of intravitreal treatment options.

Extensive research funding from organizations such as the NIH and NEI has contributed to strong innovation in pharmacologic and gene-based therapeutic pipelines. The expansion of teleophthalmology services has further improved access to retinal care, particularly in rural communities. Public health programs, including Healthy People 2030, continue to promote early screening and patient awareness. These combined factors strengthen North America’s market leadership and indicate sustained regional dominance in the coming years.

Emerging Trends

The prevalence of advanced age-related macular degeneration (AMD) has been rising as population aging continues. In the United States, the number of adults aged ≥40 years with vision-threatening AMD is projected to increase from approximately 1.8 million in 2020 to 2.9 million by 2030. Globally, a comparable escalation is anticipated as the “baby boomer” cohort advances in age, increasing pressure on retina care infrastructure.

Diabetic macular edema (DME) is becoming more common among adults living with diabetes. National estimates indicate that DME affects about 3.8 % of U.S. adults aged ≥40 years with diabetes, representing nearly 746,000 individuals. Between 2009 and 2018, the annual prevalence of any DME rose from 0.7 % to 2.6 %, reflecting an average annual percent change (AAPC) of 19.8 % (p < 0.001).

Adoption of anti-vascular endothelial growth factor (anti-VEGF) therapies as first-line treatment has accelerated. Among patients with DME, claims for anti-VEGF injections increased by 327 % from 2009 to 2018. This shift was accompanied by a 68 % decline in laser photocoagulation procedures for DME during the same period, demonstrating a major transition in preferred therapeutic modalities.

Advances in diagnostic technologies and telemedicine are improving early detection rates. Optical coherence tomography (OCT) has become the standard modality for cross-section retinal imaging and has transformed diagnostic practices for AMD and diabetic retinopathy since its FDA approval in 1991. Simultaneously, AI-enabled image analysis and teleophthalmology platforms are being evaluated to support remote screening, thereby expanding diagnostic access in rural and underserved regions.

Use Cases

- Anti-VEGF Injection Protocols: Patients diagnosed with neovascular (“wet”) AMD or DME are routinely managed with intravitreal anti-VEGF injections. Clinical utilization data show a 327 % rise in anti-VEGF claims for DME between 2009 and 2018, reflecting widespread integration of this targeted therapy. Treat-and-extend dosing strategies continue to be refined to optimize visual outcomes while reducing treatment burden.

- Nutritional Supplementation (AREDS Formulas): Findings from the AREDS and AREDS2 clinical trials, supported by the National Eye Institute, demonstrate that high-dose antioxidant vitamins and minerals can slow progression from intermediate to advanced AMD. Approximately 50 % of eligible patients report using AREDS-based supplements after diagnosis, contributing to reduced risk of vision loss within a two-year period.

- Teleophthalmology Screening Programs: Retinal imaging systems and telemedicine platforms are being implemented to screen high-risk groups including individuals with diabetes or those aged ≥60 years in community-based settings. Remote interpretation of fundus photographs and OCT scans has facilitated earlier referral, with pilot programs reporting diagnostic concordance exceeding 90 % when compared with in-person evaluations.

- Clinical Trials in Gene and Cell-Based Therapies: Early-stage clinical trials employing patient-derived induced pluripotent stem cells (hIPSCs) for dry AMD have commenced under National Eye Institute funding. These studies aim to restore retinal pigment epithelium function and are planned to enroll additional participants over the next 12 months. Parallel research is assessing viral-vector gene therapy platforms designed to deliver anti-angiogenic factors directly to retinal tissue.

Frequently Asked Questions on Macular Edema and Macular Degeneration

- What is macular degeneration?

Macular degeneration is defined as a progressive retinal disorder affecting central vision due to deterioration of the macula. It is primarily age-related and is influenced by genetic, environmental, and lifestyle factors. Early detection supports timely intervention and slows disease progression significantly. - What are the main types of macular degeneration?

Macular degeneration exists as dry and wet forms. The dry type progresses gradually with drusen accumulation, whereas the wet type advances rapidly due to abnormal vessel growth. Treatment responses differ, making accurate classification essential for optimal patient management and clinical outcomes. - What symptoms are commonly associated with macular edema and degeneration?

Patients frequently report blurred central vision, reduced contrast sensitivity, dark spots, or difficulty reading. Progressive distortion of straight lines often suggests advancing retinal involvement. Timely evaluation by eye-care professionals ensures proper diagnosis and prevents irreversible vision impairment through timely intervention. - How are macular edema and macular degeneration diagnosed?

Diagnosis relies on optical coherence tomography, fluorescein angiography, and comprehensive retinal examination. These diagnostic technologies allow visualization of structural changes, fluid buildup, and vascular abnormalities. Accurate imaging guides treatment decisions and enables monitoring of therapeutic responses over time. - What treatment options are available?

Treatment includes anti-VEGF injections, corticosteroid implants, laser therapy, and nutritional supplementation depending on disease type. Anti-VEGF therapy has shown strong efficacy in wet degeneration and edema. Tailored treatment regimens improve long-term outcomes and reduce vision loss risk substantially. - What risk factors contribute to these conditions?

Age, smoking, hypertension, diabetes, and genetic variations significantly elevate risk. Chronic inflammatory processes and oxidative stress also influence disease progression. Regular monitoring and lifestyle modification reduce the likelihood of advanced macular pathology and support better long-term visual stability.

Conclusion

The global burden of macular edema and macular degeneration is expected to rise as aging demographics and diabetes prevalence increase. Strong demand for early diagnosis, anti-VEGF therapies, and advanced imaging technologies continues to support market expansion. North America’s leadership is reinforced by robust healthcare infrastructure, widespread screening, and sustained research funding.

The shift toward biologics, teleophthalmology, and gene-based innovations reflects an evolving therapeutic landscape. Preventive care, timely intervention, and improved access to retina services are anticipated to reduce long-term visual impairment. Overall, steady market growth is projected through 2034, driven by increasing awareness and continuous technological progress.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)