Table of Contents

Overview

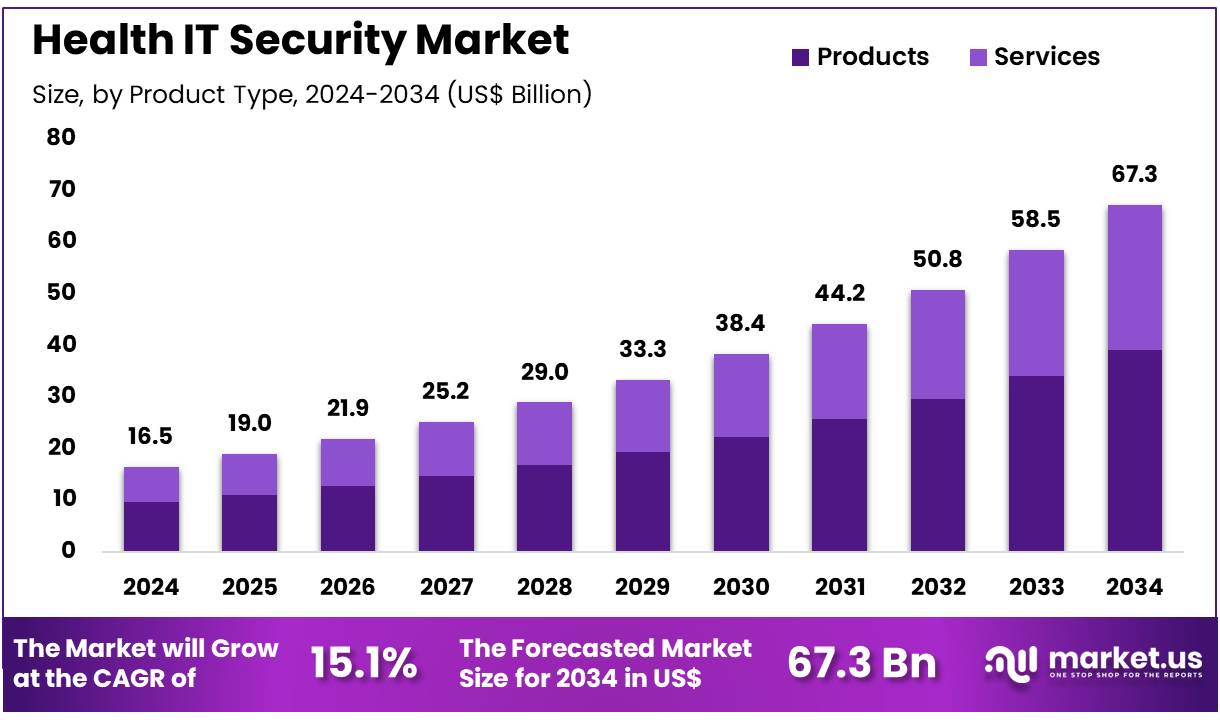

New York, NY – Nov 19, 2025 – Global Health IT Security Market size is expected to be worth around US$ 67.3 Billion by 2034 from US$ 16.5 Billion in 2024, growing at a CAGR of 15.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.9% share with a revenue of US$ 6.6 Billion.

The strengthening of Health IT security has been recognized as a critical priority for safeguarding clinical operations, patient confidentiality, and institutional integrity. A significant rise in digital adoption across hospitals, clinics, and health systems has resulted in increased exposure to cyber risks. The expansion of electronic health records, remote monitoring tools, and cloud-based data platforms has amplified the need for resilient security frameworks. As a result, the implementation of advanced cybersecurity protocols has become essential for maintaining trust and ensuring regulatory compliance.

The growing frequency of ransomware attacks and unauthorized data breaches has accelerated investment in health information protection. The adoption of multi-factor authentication, encryption standards, and continuous monitoring solutions has been widely encouraged to mitigate vulnerabilities. The integration of artificial intelligence and machine learning is enabling faster threat detection and automated response mechanisms, ensuring that sensitive health information remains protected at all times.

Regulatory bodies have emphasized stronger enforcement of data privacy requirements, leading healthcare organizations to upgrade infrastructure and strengthen workforce training. The shift toward interoperability and digital transformation has further highlighted the need for unified security practices across all health IT systems. Collaboration between healthcare providers, technology firms, and cybersecurity experts has been viewed as essential for creating a secure digital ecosystem.

The ongoing focus on Health IT security is expected to support safer data environments, improve response readiness, and enhance overall system resilience. The advancement of protective technologies is poised to play a crucial role in sustaining patient trust and supporting the secure modernization of healthcare delivery.

Key Takeaways

- The Health IT Security market generated US$ 16.5 billion in 2024, growing at a CAGR of 15.1%, and is projected to reach US$ 67.3 billion by 2033.

- By product type, the market is categorized into products and services, with products accounting for 58.2% of the total share in 2024.

- Based on deployment mode, the segmentation includes on-cloud and on-premises, where on-cloud held a dominant share of 62.5%.

- In terms of application, the market covers application security, network security, endpoint security, and content security, with network security leading at 44.5% revenue share.

- By end user, the market is divided into healthcare facility providers and healthcare payers, with healthcare facility providers representing 59.3% of the market.

- North America emerged as the leading regional market, holding a 39.9% share in 2024.

Regional Analysis

North America Leading the Health IT Security Market

North America accounted for the largest revenue share of 39.9%, driven by rising cyber threats, regulatory enforcement, and accelerated digitalization across healthcare systems. A 25% increase in healthcare data breaches between 2022 and 2024, as reported by the US Department of Health and Human Services, has reinforced the need for stronger security frameworks. Updated regulatory mandates, including the 2023 HIPAA revisions, have encouraged significant investments in cybersecurity infrastructure.

The adoption of electronic health records continued to expand, with a 15% rise in EHR usage among US hospitals, according to the Office of the National Coordinator for Health Information Technology. The growth of telehealth services also contributed to the demand for secure IT environments, reflected by a 30% increase in telehealth utilization in 2023 reported by the Centers for Medicare & Medicaid Services.

Collaborative initiatives between major healthcare providers and technology companies have further supported the development of advanced threat detection and encryption systems. Notably, a leading US health system allocated US$ 500 million to cybersecurity enhancements in 2023. These developments illustrate the sustained expansion of the Health IT Security market in North America.

Asia Pacific Expected to Record the Highest CAGR

Asia Pacific is anticipated to register the fastest CAGR due to rapid digital transformation and heightened exposure to cyber threats. Regulatory measures, such as India’s Digital Personal Data Protection Act of 2023, have strengthened requirements for healthcare data security. The World Health Organization documented a 20% rise in cyberattacks on healthcare systems in the region from 2022 to 2024, driving increased cybersecurity spending.

Digital health adoption continues to accelerate, with China’s National Health Commission reporting a 25% rise in digital health platform usage and Japan allocating US$ 300 million in 2023 to enhance cybersecurity in public healthcare facilities. Rising chronic disease prevalence and expanding smart healthcare initiatives in South Korea and Singapore are further increasing the need for secure data-sharing systems. Collectively, these factors are expected to support strong growth in the Asia Pacific Health IT Security market.

Emerging Trends

- Rising Frequency of Large-Scale Breaches: A significant escalation in large-scale health data breaches has been observed. In 2023, an average of 1.99 incidents involving 500 or more records occurred daily, resulting in approximately 364,571 health records being exposed each day across the healthcare sector.

- Accelerated Ransomware Activity: Ransomware attacks continue to intensify, with major healthcare-related incidents increasing by 93% between 2018 and 2023. This growth reflects the expanding threat landscape and the heightened targeting of hospitals and clinical networks by extortion-driven actors.

- Heightened Focus on Medical Device Cybersecurity: Cybersecurity expectations for medical devices have strengthened following the FDA’s final guidance issued in September 2023. Manufacturers are now required to embed comprehensive risk-management practices into device design and submit detailed cybersecurity plans in all premarket documentation.

- Mandated Minimum Cyber Hygiene Under HIPAA: The NCVHS has recommended the adoption of essential cybersecurity hygiene practices under the HIPAA Security Rule. These recommendations include multi-factor authentication, offline data backups, and predictive risk-modeling tools to establish a stronger baseline of compliance across covered entities.

Use Cases

- EHR System Protection: Electronic Health Record systems are being reinforced with end-to-end encryption and multi-factor authentication to restrict unauthorized access. In alignment with NCVHS recommendations, more than 75% of covered entities are expected to deploy predictive risk-analysis tools by 2025 for proactive vulnerability management.

- Telehealth Session Security: Telehealth platforms are being secured through encrypted communication channels and compliant video-conferencing protocols. As telemedicine usage among U.S. physicians rose from 15.4% in 2019 to 86.5% in 2021, these measures have become essential for safeguarding patient interactions under HIPAA.

- Medical Device Risk Management: Healthcare providers increasingly require device manufacturers to submit cybersecurity documentation with premarket applications. Following the FDA’s September 2023 guidance, all Class II and III device submissions now include structured vulnerability assessments and mitigation strategies to address potential cyber risks.

- Breach Response and Notification: Automated breach-detection systems are being deployed to accelerate incident reporting processes. In 2023, these tools supported an average notification time of 18 days after breach discovery, reducing patient exposure periods and improving adherence to OCR reporting requirements.

Frequently Asked Questions on Health IT Security

- Why is Health IT Security important?

Its importance is driven by rising cyberattacks, increased electronic health record adoption, and strict regulatory requirements. Strong security controls help reduce unauthorized access risks, safeguard sensitive patient data, and maintain trust in digital healthcare ecosystems. - What are the major threats in Health IT Security?

Major threats include ransomware, phishing, insider breaches, misconfigured cloud systems, and vulnerabilities in connected medical devices. These threats disrupt healthcare operations, compromise patient data, and create substantial financial and operational consequences for healthcare organizations globally. - How is patient data protected in Health IT systems?

Patient data is protected through encryption, access controls, identity management, continuous monitoring, and regular audits. These mechanisms ensure only authorized personnel access sensitive information while minimizing data manipulation or leakage across healthcare environments. - What is the Health IT Security Market?

The health IT security market encompasses solutions and services designed to protect digital healthcare infrastructure. Its growth is driven by rising cyberattacks, expanding digital health adoption, and increasing regulatory compliance needs across hospitals, clinics, and insurance organizations. - What factors are driving market growth?

Growth is driven by increasing ransomware incidents, rapid cloud migration, the rise of connected medical devices, and stronger compliance mandates. These elements collectively elevate investment in advanced security platforms within the global healthcare technology ecosystem. - Which segments dominate the Health IT Security Market?

Key segments include cybersecurity services, endpoint protection, identity management, and network security. Services currently dominate, as healthcare providers rely heavily on external expertise to manage complex security environments and address evolving cyber threats effectively. - Which regions lead the Health IT Security Market?

North America leads due to strict regulations, high digital adoption, and frequent targeted attacks. Europe follows with strong data protection frameworks, while Asia-Pacific shows rapid expansion driven by healthcare modernization and increasing investment in cyber resilience.

Conclusion

The continued expansion of digital health infrastructure has intensified the need for robust Health IT security systems. Rising cyber threats, stricter regulatory mandates, and accelerated adoption of cloud platforms and connected devices have reinforced investments in advanced protective technologies. Stronger emphasis on encryption, multi-factor authentication, and AI-driven threat detection is supporting safer data environments and improving organizational resilience.

Regional initiatives across North America and Asia Pacific demonstrate sustained commitment to strengthening cybersecurity readiness. Overall, the market’s growth is expected to be sustained by ongoing digital transformation, heightened risk exposure, and the increasing prioritization of secure healthcare delivery systems.