Table of Contents

Overview

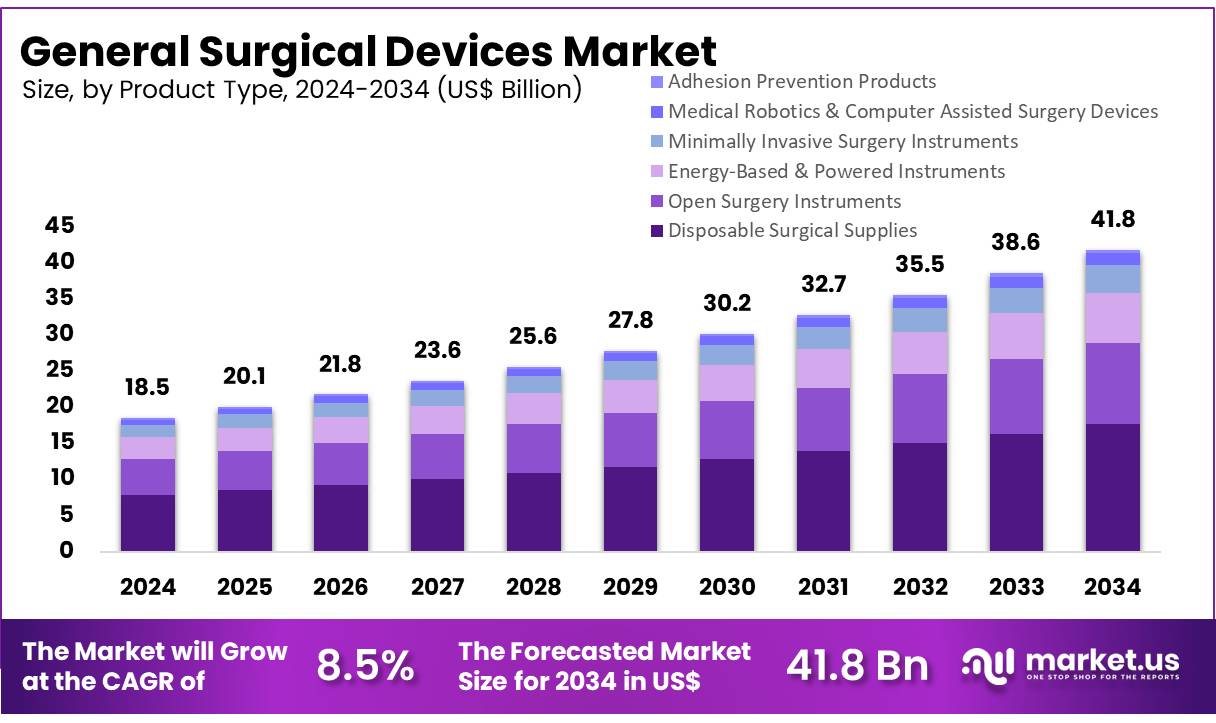

New York, NY – Nov 13, 2025 – Global General Surgical Devices Market size is expected to be worth around US$ 41.8 billion by 2034 from US$ 18.5 billion in 2024, growing at a CAGR of 8.5% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 38.1% share with a revenue of US$ 7.0 Million.

The general surgical devices market has been expanding steadily as demand for advanced surgical interventions continues to rise. Growth has been supported by increasing surgical volumes, the adoption of minimally invasive procedures, and continuous technological innovation. The market has been driven by the development of precision instruments, enhanced safety features, and improved ergonomics that facilitate better surgical outcomes.

Significant investments in healthcare infrastructure and the growing prevalence of chronic diseases have contributed to wider device utilization across hospitals, clinics, and ambulatory surgical centers. The introduction of smart surgical tools, robotics-assisted systems, and disposable instruments has further strengthened market penetration by reducing infection risks and improving procedural efficiency.

Market expansion has also been supported by favorable regulatory approvals and the availability of high-quality products from established manufacturers. The integration of digital technologies in operating rooms, including imaging-guided devices and sensor-based tools, has been recognized as a key advancement that enhances accuracy during complex procedures.

North America and Europe continue to represent major revenue-generating regions due to strong healthcare systems and early technology adoption. Meanwhile, rapid improvements in medical facilities across Asia-Pacific have been creating new opportunities for device manufacturers.

Overall, the market outlook remains positive as healthcare providers increasingly prioritize efficiency, safety, and precision. Continued innovation and a shift toward value-based care are expected to support sustained growth in the general surgical devices sector over the coming years.

Key Takeaways

- In 2023, the general surgical devices market generated revenue amounting to US$ 18.5 billion, supported by a CAGR of 8.5%, and the market size is projected to reach US$ 41.8 billion by 2033.

- The product landscape is categorized into disposable surgical supplies, open surgery instruments, energy-based and powered instruments, minimally invasive surgery instruments, medical robotics and computer-assisted surgery devices, and adhesion prevention products. Among these categories, disposable surgical supplies accounted for the largest share at 42.4% in 2023.

- Based on application, the market is segmented into orthopedic surgery, cardiology, wound care, ophthalmology, audiology, and other procedures. Orthopedic surgery emerged as the dominant application area, capturing 40.7% of the market.

- In terms of end users, the segmentation includes hospitals and clinics, ambulatory surgical centers, and specialty clinics. The hospitals and clinics segment held the leading position with 54.5% of the total revenue share in 2023.

- From a regional perspective, North America represented the largest share of the global market, accounting for 38.1% in 2023.

Regional Analysis

North America accounted for the largest revenue share of 38.1%, supported by rising demand for minimally invasive procedures and the growing incidence of chronic conditions that require surgical treatment. Advances in surgical technologies, including robotics and precision-based tools, have improved clinical outcomes and reduced recovery periods. The expansion of healthcare infrastructure and increasing healthcare expenditure further strengthened the region’s market position.

The expansion of outpatient surgical centers and the wider use of same-day discharge procedures also contributed to the demand for efficient and cost-effective surgical devices. In August 2024, Johnson & Johnson launched an advanced chest fixation system aimed at enhancing stability following major thoracic and cardiac surgeries. The system’s improved locking strength and faster fixation reflect a broader industry shift toward innovation that enhances surgical outcomes. Rising awareness and better access to healthcare services have additionally supported device adoption across the region.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to witness the fastest CAGR during the forecast period, driven by demographic shifts, improved healthcare accessibility, and a notable increase in surgical procedures. According to the National Bureau of Statistics of China, individuals aged 60 and above are expected to represent 21.1% of the total population in 2024. The growing elderly population is anticipated to elevate the need for surgical interventions, particularly in cardiovascular and orthopedic domains.

The rising burden of chronic diseases and ongoing healthcare infrastructure development in China, India, and Japan are expected to support further expansion. Increased government healthcare spending and investments in advanced medical technologies are likely to enhance the availability and performance of surgical devices.

Additionally, the region’s expanding medical tourism industry is expected to bolster demand for high-quality surgical procedures, supporting market growth. With the introduction of favorable healthcare policies and improved reimbursement frameworks, the general surgical devices market in Asia Pacific is anticipated to record strong and sustained growth in the years ahead.

Emerging Trends

- Expansion of Robotic-Assisted Surgery: The regulatory environment has experienced a measurable rise in approvals for robotic-assisted surgical platforms. In early 2024, the FDA verified the safety and performance of the da Vinci Surgical System Model IS5000 for multiple procedures, supported by equivalence studies with earlier models. The MIRA Surgical System, a compact table-mounted electromechanical platform, was also classified as Class II through the De Novo pathway, indicating growing interest in smaller robotic systems designed for minimally invasive colectomies.

- Shift to Single-Use Devices for Infection Control: Healthcare-associated infections continue to present a significant clinical challenge. An estimated 110,800 surgical site infections were reported among inpatient surgeries in the U.S. in 2015, and the standardized infection ratio rose by about 2% by 2023. These trends have accelerated the shift toward sterile, single-use instruments such as trocar sleeves, drapes, and electrosurgical pencils to reduce cross-contamination and enhance adherence to strict sterilization protocols.

- Integration of Artificial Intelligence and Machine Learning: The FDA’s catalog of AI- and ML-enabled medical devices now includes an expanding range of authorized systems designed to improve surgical precision and intraoperative support. These technologies include navigation tools that refine real-time tissue differentiation and predictive platforms guiding surgical margins. The consistent addition of new systems reflects increasing adoption of data-driven, adaptive technologies within surgical environments.

- Adoption of Three-Dimensional Printing for Customization: Growing use of 3D printing in surgical care is supported by recent literature reviews identifying 110 publications describing 140 distinct 3D-printed devices applied directly in patient treatment, with notable acceleration in the past three years. Surgeons are increasingly relying on patient-specific models and customized guides created from CT or MRI data to improve preoperative planning, reduce operative times, and support improved surgical outcomes.

Frequently Asked Questions on Surgical Devices

- What are the main categories of general surgical devices?

The devices are categorized into handheld instruments, electrosurgical devices, minimally invasive instruments, and suturing or stapling systems. These categories support surgeons across different procedural steps, ensuring effective tissue handling, reduced trauma, and improved procedural control during operations. - Why are general surgical devices important in healthcare?

These devices are essential for maintaining surgical accuracy, minimizing procedural risks, and supporting successful patient recovery. Their use enhances surgical workflow efficiency, ensures consistent performance, and contributes to improved clinical outcomes in both routine and advanced procedures. - What materials are commonly used in general surgical devices?

Surgical instruments are typically made from stainless steel, titanium, polymers, and advanced alloys. These materials ensure durability, corrosion resistance, and biocompatibility, enabling repeated sterilization and sustained performance during diverse surgical applications across medical specialties. - What are minimally invasive surgical devices?

Minimally invasive surgical devices enable procedures through small incisions using laparoscopic or endoscopic tools. Their adoption reduces trauma, shortens recovery time, and enhances surgical precision, contributing to improved patient satisfaction and lower overall healthcare burdens. - How is quality ensured in general surgical devices?

Quality is ensured through strict manufacturing standards, material testing, regulatory certifications, and performance validation. These processes confirm durability, sterility, and mechanical precision, guaranteeing consistent functionality required for high-quality surgical interventions across healthcare institutions. - Which regions dominate the general surgical devices market?

North America and Europe dominate due to developed healthcare systems, high surgical procedure volumes, and strong technological adoption. Asia-Pacific is experiencing rapid growth, supported by improving healthcare access, rising investments, and expanding medical tourism across emerging economies. - Which product segments show the highest growth?

Electrosurgical devices and minimally invasive instruments show the fastest growth due to improved precision, reduced patient trauma, and shorter recovery periods. These products support efficient workflow and align with the increasing shift toward advanced surgical intervention techniques. - Who are the major end users of general surgical devices?

Primary end users include hospitals, surgical centers, and ambulatory care facilities. These institutions rely on advanced devices to ensure procedural safety, operational efficiency, and improved patient outcomes across general, specialized, and minimally invasive surgical procedures.

Conclusion

The general surgical devices market is expected to maintain steady expansion as surgical volumes rise and technological innovation strengthens procedural efficiency and safety. Growth has been supported by increased adoption of minimally invasive techniques, advancements in robotics and digital integration, and wider availability of high-quality disposable and precision-based instruments.

Strong demand in North America and Europe, coupled with rapid healthcare development in Asia-Pacific, continues to enhance global market performance. Favorable regulations, improved healthcare infrastructure, and rising chronic disease prevalence further reinforce long-term market prospects, indicating sustained progress driven by innovation and value-based care priorities.