Table of Contents

Overview

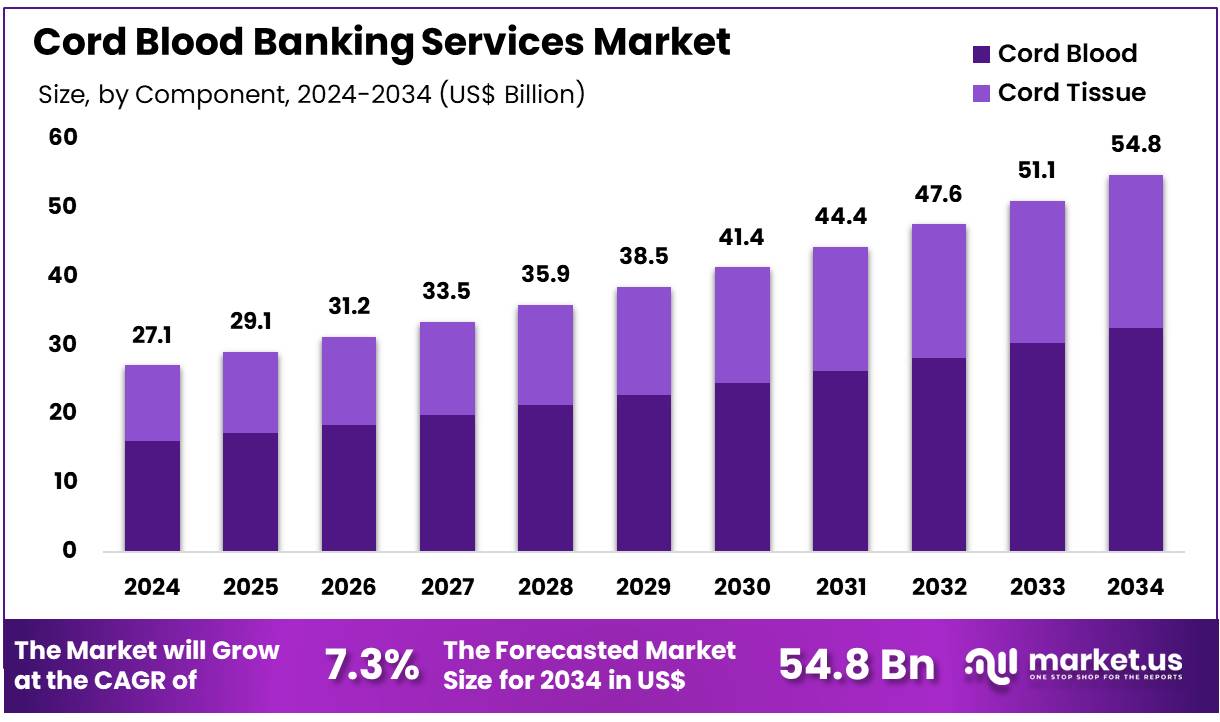

New York, NY – Nov 13, 2025 – Global Cord Blood Banking Services Market size is expected to be worth around US$ 54.8 Billion by 2034 from US$ 27.1 Billion in 2024, growing at a CAGR of 7.3% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 39.6% share with a revenue of US$ 10.7 Billion.

The global demand for cord blood banking services has been expanding steadily, driven by rising awareness of stem cell therapies and the growing prevalence of chronic and genetic disorders. The market has been supported by the increasing adoption of advanced preservation technologies, which has improved the viability and long-term storage of cord blood stem cells. Regulatory support in several countries has contributed to wider acceptance of stem cell banking as a preventive healthcare measure.

Growth in the sector has been attributed to the rising number of births in developing economies and the increasing willingness of parents to invest in biological insurance for future medical needs. Public and private banking models have continued to evolve, with private banks demonstrating significant uptake due to high consumer preference for personalized storage services. Public banks have played an essential role in supporting clinical research and allogeneic transplant requirements.

Technological advancements in cryopreservation, automated processing systems, and genetic testing have strengthened service offerings across the industry. The market has been further influenced by expanding research into regenerative medicine, where cord blood stem cells are being evaluated for potential applications in neurological, metabolic, and immune-related conditions.

Strategic collaborations among biotechnology firms, healthcare providers, and research institutions have accelerated innovation within the sector. The overall outlook for cord blood banking services remains positive, supported by continuous investment, increasing healthcare expenditure, and a growing emphasis on preventive medicine. The market is expected to maintain stable growth as scientific progress reinforces the therapeutic value of stem cell preservation.

Key Takeaways

- In 2024, the Cord Blood Banking Services market generated revenue of US$ 27.1 billion, supported by a 7.3% CAGR, and is projected to reach US$ 54.8 billion by 2033.

- The service segment includes collection & transportation, processing, analysis, and storage, with processing emerging as the leading category in 2023, accounting for 42.8% of the market.

- By component, the market is classified into cord tissue and cord blood, with cord blood representing 59.3% of the total share.

- Based on application, the market comprises diabetes, cancer, blood disorder, immune disorder, metabolic disorder, and others, where cancer dominated with a 36.4% revenue share.

- The end-user segment includes hospitals, pharmaceutical & biotechnology companies, and academic & research institutes, with hospitals leading at 51.7%.

- North America was the leading regional market, holding a 39.6% share in 2023.

Segmentation Analysis

- Service Analysis: In 2023, the processing segment accounted for 42.8% of the cord blood banking services market, supported by progress in cryopreservation, transportation, and analytical procedures. Rising demand for high-quality stem cell processing is driving steady growth. Increasing incidences of genetic disorders and stricter compliance requirements are encouraging providers to upgrade processing capabilities. Expansion in emerging economies and advances in long-term storage technologies are expected to reinforce this segment’s upward trajectory.

- Component Analysis: Cord blood represented 59.3% of the overall market share, driven by increasing awareness of its therapeutic value. Growing interest among parents in preserving stem cells for future medical use continues to support strong demand. Although cord blood remains dominant, research highlighting the regenerative potential of cord tissue is gaining momentum. Rising clinical trial activity, greater investment in stem cell innovation, and supportive public initiatives are expected to enhance uptake of both cord blood and cord tissue storage services.

- Application Analysis: The cancer segment held a 36.4% revenue share, supported by the extensive use of cord blood stem cells in treating hematologic cancers such as leukemia and lymphoma. Growth is being reinforced by advancements in immunotherapy and regenerative solutions. Increasing global cancer prevalence, expanding clinical development programs, and stronger collaboration between research institutions and healthcare providers are contributing to wider adoption. Improved therapeutic effectiveness is projected to sustain the segment’s leading position.

- End-user Analysis: Hospitals captured 51.7% of market revenue in 2023, driven by the growing integration of stem cell therapies into standard clinical pathways. Rising utilization of regenerative treatments for cancers and immune disorders supports this segment’s expansion. Partnerships between hospitals and cord blood banks are increasing, strengthened by active clinical research and improved therapeutic protocols. The hospital sector is expected to maintain dominance due to advanced infrastructure and broader access to stem cell-based interventions.

Regional Analysis

North America has been identified as the leading region in the Cord Blood Banking Services market. The region accounted for 39.6% of total revenue, supported by rising awareness of the therapeutic potential of stem cells and continued progress in regenerative medicine. Public and private funding directed toward stem cell research and regenerative therapies strengthened demand for cord blood banking services. Market expansion has also been supported by the growing number of expectant parents opting to preserve their newborns’ cord blood for potential future treatments.

In April 2022, Global Cord Blood Corporation announced plans to acquire Cellenkos, Inc., securing full rights to develop and commercialize its product pipeline. This move demonstrated ongoing strategic efforts by major companies to enhance their portfolios and broaden their market presence. The rising use of cord blood transplants, particularly for conditions such as leukemia and lymphoma, further stimulated market growth. In addition, advancements in healthcare infrastructure and regulatory support continued to drive the adoption of cord blood banking services across the region.

The Asia Pacific region is projected to record the fastest CAGR during the forecast period. Growth is expected to be driven by increased healthcare investments and rising awareness of stem cell–based therapies. Countries such as China, India, and Japan are anticipated to witness strong expansion as healthcare providers continue to broaden their regenerative medicine and stem cell service offerings.

A growing number of parents in the region are expected to choose cord blood storage as a preventive healthcare measure, supporting long-term market development. In October 2024, scientists at Cordlife Group Limited introduced a machine-learning model designed to predict CD34+ cell counts in cord blood samples. This innovation is expected to improve cord blood selection and enhance transplant success rates, contributing to overall market efficiency.

The integration of artificial intelligence and data-driven methodologies is forecast to improve service quality and operational effectiveness, increasing the attractiveness of cord blood banking services. As market conditions evolve, supportive healthcare regulations and collaborations with biotechnology companies are expected to further encourage industry growth across the Asia Pacific region.

Frequently Asked Questions on Cord Blood Banking Services

- How is cord blood collected?

Cord blood is collected immediately after childbirth through a simple, painless procedure. The remaining blood in the umbilical cord and placenta is drawn, sealed, and transported to a laboratory where it undergoes processing and cryogenic storage. - What conditions can be treated using cord blood?

Cord blood stem cells have demonstrated effectiveness in treating leukemia, lymphoma, immune deficiencies, metabolic disorders, and certain genetic diseases. Their regenerative properties support therapeutic applications across hematopoietic reconstruction, immune system repair, and emerging regenerative medicine interventions. - What is the difference between public and private cord blood banking?

Public banking donates cord blood for communal use, supporting patients in need of matched stem cell transplants. Private banking stores samples exclusively for the donor family, offering personalized biological insurance for potential future medical requirements. - How long can cord blood be stored?

Cord blood units can be preserved for several decades under controlled cryogenic conditions. Research indicates stability and viability of stem cells for long-term therapeutic use when stored at extremely low temperatures with validated preservation protocols. - Is cord blood banking safe for mother and baby?

Cord blood collection is considered safe, as it occurs after delivery without affecting the birthing process. The procedure is non-invasive, posing no risk to mother or child, and does not interfere with standard medical care. - How is the quality of stored cord blood maintained?

Quality is maintained through advanced processing technologies, sterility testing, controlled cryopreservation systems, and continuous monitoring. Accredited laboratories apply strict protocols to ensure long-term cell viability, safety, and compliance with global regulatory standards. - Which regions dominate the cord blood banking market?

North America and Europe currently dominate the market due to strong healthcare infrastructure, higher awareness, and established regulatory frameworks. Significant growth is also being observed across Asia-Pacific, supported by rising birth rates and expanding biotechnology investments. - What technological trends influence the market?

Technological progress in cryopreservation, automated processing, genetic screening, and stem cell expansion is influencing market development. These advancements enhance cell viability, improve safety, and support broader therapeutic applications of stored cord blood samples.

Conclusion

The global cord blood banking services market has been characterized by stable expansion, supported by increasing awareness of stem cell therapies, advancements in preservation technologies, and sustained regulatory encouragement. Growth has been reinforced by rising birth rates in developing regions, stronger clinical adoption, and expanding applications in cancer and immune-related disorders.

Technological innovations, collaborative research, and improved healthcare infrastructure have strengthened market capabilities. North America continues to lead, while Asia Pacific is poised for rapid growth. Overall, the sector is expected to maintain a positive trajectory as investment, scientific progress, and preventive healthcare trends continue to support long-term demand.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)