Table of Contents

Overview

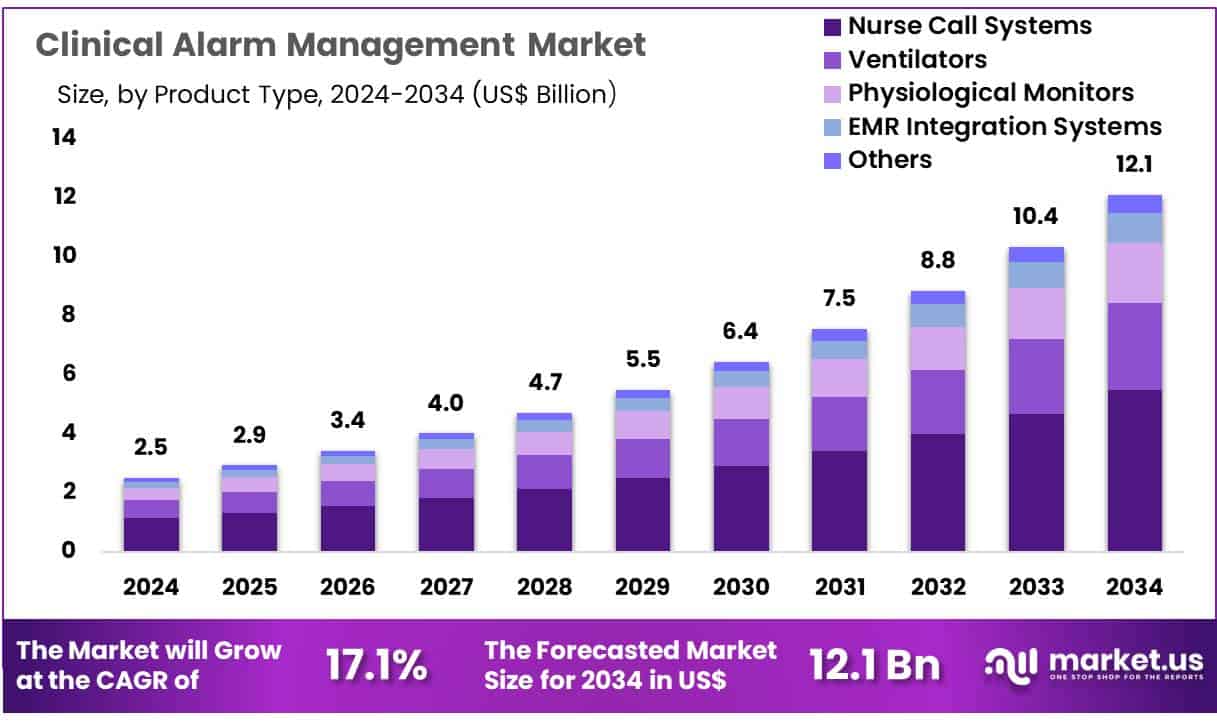

New York, NY – June 13, 2025 – Global Clinical Alarm Management Market size is expected to be worth around US$ 12.1 billion by 2034 from US$ 2.5 billion in 2024, growing at a CAGR of 17.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 13.8% share with a revenue of US$ 1.1 billion.

The global clinical alarm management market is witnessing steady growth, driven by the increasing need to improve patient safety, reduce alarm fatigue among healthcare providers, and streamline clinical workflows. Clinical alarm management refers to systems and protocols used to prioritize, filter, and respond to medical alarms in healthcare environments. These systems are essential in reducing false or non-actionable alerts and ensuring timely intervention in critical care scenarios.

The growing burden of chronic diseases, rising hospital admissions, and the widespread use of connected medical devices are contributing to the expansion of this market. Technological advancements in alarm integration platforms, mobile alert systems, and intelligent alarm analytics are further accelerating adoption across hospitals and healthcare facilities.

Regulatory guidelines from agencies such as The Joint Commission and the U.S. Food and Drug Administration (FDA) have placed increased emphasis on alarm safety, prompting healthcare providers to adopt comprehensive alarm management solutions. North America currently leads the market due to high technology adoption and strict regulatory compliance, while Asia-Pacific is expected to register the fastest growth due to expanding healthcare infrastructure. With continued emphasis on real-time data monitoring and clinical decision support, the clinical alarm management market is poised for sustained growth in the years ahead.

Key Takeaways

- In 2023, the Clinical Alarm Management Market generated a revenue of US$ 2.5 billion and is projected to reach US$ 12.1 billion by 2033, growing at a CAGR of 17.1% over the forecast period.

- By product type, the market is segmented into nurse call systems, ventilators, physiological monitors, EMR integration systems, and others. Among these, nurse call systems led the segment in 2023, accounting for 45.3% of the total market share.

- Based on component, the market is categorized into solutions and services, with solutions dominating the segment by holding a 58.3% market share in 2023.

- In terms of end users, the market includes hospitals & clinics, specialty centers, long-term care facilities, home care settings, and ambulatory care centers. Hospitals & clinics emerged as the leading end-user, capturing 52.3% of the total revenue.

- Regionally, North America dominated the global market, securing a 43.8% share in 2023, driven by technological advancements, high awareness of patient safety, and strict compliance regulations in healthcare facilities.

Segmentation Analysis

- Product Type Analysis: In 2023, the nurse call systems segment led the clinical alarm management market, holding a 45.3% share. This growth is driven by the adoption of advanced communication tools that enhance staff responsiveness and patient care. Integration with physiological monitors and EMR systems is improving real-time alerting capabilities. Additionally, voice-activated and wireless technologies are streamlining workflow in clinical environments. These innovations are expected to increase the adoption of nurse call systems across hospitals and healthcare facilities.

- Component Analysis: The solutions segment dominated the market in 2023, accounting for 58.3% of the total share. Healthcare providers are increasingly opting for integrated platforms that manage alarm fatigue and support better clinical decisions. Solutions offering real-time alerts, advanced analytics, and seamless integration with hospital systems are seeing rising demand. As patient safety and communication efficiency gain importance, these technologies are becoming essential for optimizing alarm response. The need to minimize false alarms is further boosting segment growth.

- End-User Analysis: Hospitals and clinics held the largest share of 52.3% in 2023, driven by their high patient volume and need for continuous monitoring. These facilities rely on clinical alarm management systems to reduce alarm fatigue and ensure timely responses to critical alerts. Integrated platforms linking monitoring devices, nurse call systems, and EMRs are widely adopted to streamline operations. With a strong focus on safety and efficiency, hospitals and clinics are expected to remain the primary end users in this market.

Market Segments

Product Type

- Nurse Call Systems

- Ventilators

- Physiological Monitors

- EMR Integration Systems

- Others

Component

- Solutions

- Services

End-user

- Hospitals & Clinics

- Specialty Centers

- Long-Term Care Facilities

- Home Care Settings

- Ambulatory Care Centers

Regional Analysis

In 2023, North America held the largest share of the global clinical alarm management market, accounting for 43.8% of total revenue. This dominance is attributed to the widespread adoption of advanced healthcare technologies, regulatory mandates, and growing concerns over alarm fatigue.

According to the FDA, adverse events linked to alarm fatigue rose by 30% between 2022 and 2023, prompting hospitals to invest in smarter alarm systems. The Joint Commission’s safety goals led to a 25% rise in compliance spending, while over 85% of U.S. hospitals upgraded their systems. Institutions like Mayo Clinic and Cleveland Clinic have adopted AI-based solutions, reducing non-actionable alarms by 40%.

Asia Pacific is projected to register the highest CAGR during the forecast period, fueled by healthcare digitization and infrastructure investments. The WHO reported a 22% rise in technology adoption across the region. India and China made significant investments in modernizing hospitals, while Japan and Australia emphasized AI and safety improvements. Southeast Asian nations are also expanding digital health initiatives. Rising demand for patient monitoring, coupled with public-sector efforts to improve care quality, is expected to drive rapid growth in the Asia Pacific clinical alarm management market.

Emerging Trends

- Regulatory Mandates for Alarm Safety: A new National Patient Safety Goal (NPSG.06.01.01) took effect in January 2024, requiring accredited hospitals to improve clinical alarm systems and reduce patient harm. This mandate has driven hospitals to evaluate and redesign their alarm protocols.

- Rise of Evidence-Based Alarm Reduction Programs: Quality improvement methods such as Plan-Do-Study-Act (PDSA) cycles have been adopted more widely. In one multi-hospital initiative, alarm counts were reduced by 74% to 95% over two years and sustained for at least 12 months.

- Personalization of Alarm Parameters: Alarm settings are increasingly being tailored to specific patient populations and clinical contexts. Custom limits and delays are now recommended to filter out non-actionable alerts, thereby improving the signal-to-noise ratio in critical care.

- Recognition of Alarm Fatigue as a Patient Safety Hazard: Analysis of sentinel event data showed 98 alarm-related adverse events between January 2009 and June 2012, of which approximately 80 were linked to alarm fatigue. This recognition has underscored the need for system-level interventions.

Use Cases

- High Alert Volumes in Intensive Care: In a 66-bed academic ICU, more than 2 million physiologic monitor alerts were generated in one month. This equated to roughly 187 warnings per patient per day and triggered a system redesign to curb excessive alarms.

- Alarm Reduction via PDSA Strategy: A hospital network applied a PDSA model over two years to target nuisance alarms. Alarm counts dropped by between 74% and 95% across three hospitals, with the improvements maintained for at least 12 months.

- Vendor Monitor Software Alerts: After a software upgrade on Philips central and bedside monitors, more than 47 000 “no data” monitor alarms were generated in 30 days. This highlighted the need for vendor-software customization and alarm prioritization.

- Alert Fatigue in Decision-Support Software: The FDA received an adverse event report linked to clinical decision-support software alerts, noting that perceptual desensitization to frequent notifications can lead to missed critical alerts.

Conclusion

The global clinical alarm management market is experiencing robust growth, driven by rising awareness of patient safety, alarm fatigue mitigation, and technological advancements in hospital systems. With strong regulatory support and increasing adoption of AI-powered, integrated alarm solutions, hospitals are streamlining clinical workflows and improving response times.

North America remains the market leader due to high compliance and infrastructure, while Asia Pacific shows the fastest growth backed by healthcare digitization. Emerging trends like alarm personalization and evidence-based reduction strategies are reshaping the market landscape. These developments position clinical alarm management as a critical component of modern, patient-centric healthcare systems worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)