Table of Contents

Overview

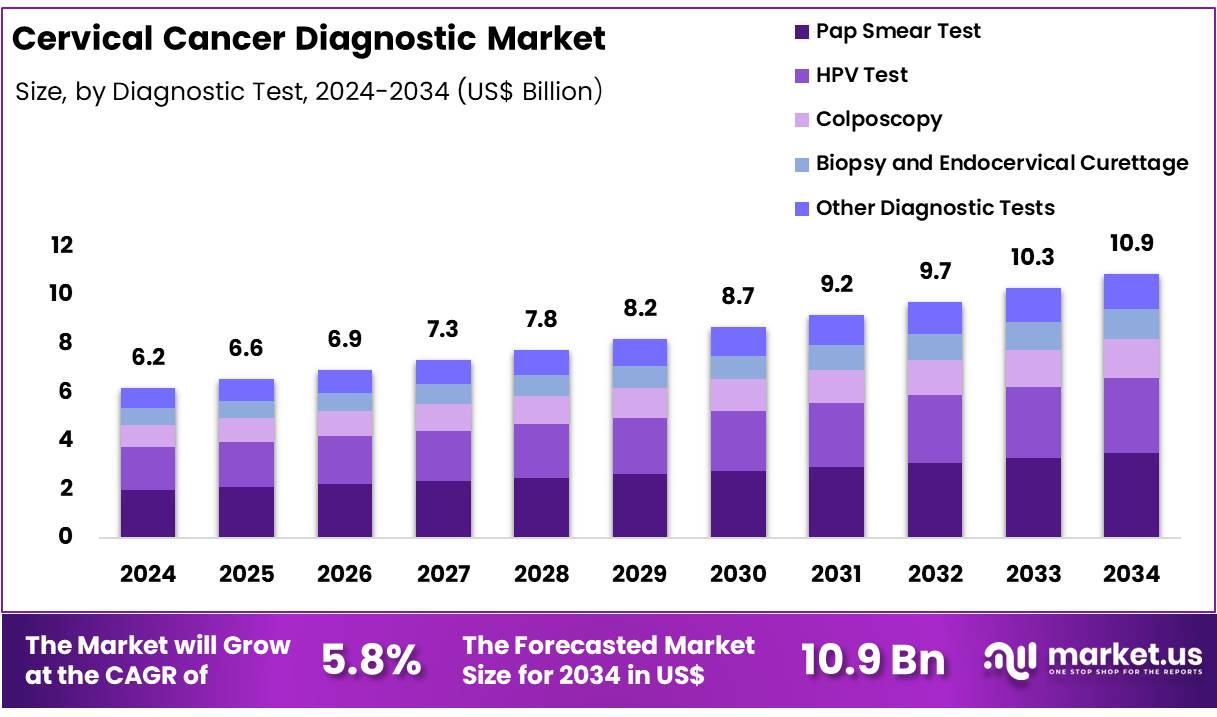

New York, NY – Nov 24, 2025 – Global Cervical Cancer Diagnostic Market size is expected to be worth around US$ 10.9 Billion by 2034 from US$ 6.2 Billion in 2024, growing at a CAGR of 5.8% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 45.6% share with a revenue of US$ 2.8 Billion.

The global cervical cancer diagnostics market has been experiencing steady growth as early detection has been recognized as a critical factor in reducing morbidity and mortality associated with the disease. The market value has been increasing due to the rising adoption of screening programs, improved diagnostic technologies, and growing awareness regarding preventive healthcare. The burden of human papillomavirus (HPV) infection, which is responsible for the majority of cervical cancer cases, has been a primary driver for the deployment of advanced diagnostic solutions.

The market expansion has been supported by the widespread use of Pap tests, HPV DNA testing, colposcopy, and biopsy procedures. The development of molecular diagnostic tools has contributed to enhanced accuracy, faster turnaround times, and improved patient outcomes. The increased preference for non-invasive and cost-effective screening methods has further strengthened market penetration across both developed and developing regions.

Government-led initiatives, national screening guidelines, and public health campaigns have played an essential role in promoting routine screening. The adoption of HPV vaccination programs has also complemented diagnostic demand by broadening preventive strategies. However, the market has been constrained by limited access to screening services in low-resource settings, insufficient healthcare infrastructure, and a lack of skilled medical professionals in certain regions.

The growth of the market is expected to be sustained as investments in research, diagnostic modernization, and digital pathology continue to increase. The emphasis on early detection, combined with rising healthcare expenditure and technological advancements, is anticipated to support the expansion of cervical cancer diagnostic solutions worldwide.

Key Takeaways

- The global cervical cancer diagnostic market is projected to reach US$ 10.9 billion by 2034, increasing from US$ 6.2 billion in 2024.

- The market is anticipated to expand at a CAGR of 5.8% from 2025 to 2034.

- The Pap smear test segment accounted for the largest share in 2024, representing 32.1% of the market.

- The hospital segment remained the leading end user in 2024, holding a 42.5% share.

- North America dominated regional demand in 2024 with a 45.6% market share, valued at US$ 2.8 billion.

Regional Analysis

In 2024, North America maintained a dominant position in the cervical cancer diagnostic market, accounting for over 45.6% of global revenue and reaching a market value of US$ 2.8 billion. This leadership is supported by high awareness levels, extensive early screening programs, and a well-established healthcare infrastructure. The region has benefited from the broad implementation of advanced diagnostic technologies, including HPV testing and Pap smear screening.

The United States represents the largest contributor within the region. Strong government-supported prevention programs, such as the CDC’s National Breast and Cervical Cancer Early Detection Program (NBCCEDP), have played a significant role in improving screening access for underserved groups and strengthening overall diagnostic uptake.

Canada also provides substantial support to regional growth. Preventive screenings are included under public healthcare coverage, enabling high participation rates among women aged 25 to 69, the demographic most at risk for cervical cancer.

North America’s leading position is further strengthened by its high healthcare expenditure. As reported by the World Bank, the United States allocates more than 16% of its GDP to healthcare, facilitating the rapid integration of advanced diagnostic solutions.

Overall, North America’s dominance in the cervical cancer diagnostic market is driven by comprehensive early detection strategies, public health initiatives, and strong medical infrastructure. These factors continue to support consistent market expansion and promote early diagnosis, contributing to improved survival outcomes across the region.

Use Cases

- Population-Based HPV DNA Testing: High-performance HPV DNA assays are being adopted as primary screening tools to detect high-risk HPV types before malignant transformation. Under the WHO elimination framework, 70% of women should undergo HPV testing by ages 35 and 45, a measure expected to reduce mortality by up to 80%.

- Pap Test (Cytology) Programs: Pap cytology continues to serve as a foundational screening method. In the United States, routine Pap and HPV tests identify nearly 200,000 cervical pre-cancer cases each year. Approximately 10,800 invasive cervical cancer diagnoses occur annually, and screening initiatives aim to significantly lower this incidence.

- Self-Sampling for HPV Screening: Self-collection HPV screening programs have expanded access among underscreened populations. A U.S. trial involving 9,960 recipients demonstrated a 50% increase in screening uptake, though only 26% completed testing. When validated assays are used, self-sampling offers convenience and diagnostic sensitivity comparable to clinician-collected samples.

- Single-Visit “Screen-and-Treat” Models: Integrated “screen-and-treat” models are being deployed in several sub-Saharan African countries. Zambia has implemented this approach across 345 facilities, enabling women to undergo HPV testing and receive immediate precancer treatment during the same visit, thereby improving adherence and reducing loss to follow-up.

- National Screening Targets and Outcomes: Some nations have established large-scale screening commitments. Ethiopia aims to screen one million eligible women annually and treat 90% of detected precancer cases. These initiatives support WHO’s 2030 “90–70–90” goals, which target high vaccination, screening, and treatment coverage.

Frequently Asked Questions on Cervical Cancer Diagnostic

- Why is cervical cancer screening important?

Screening is essential because early-stage cervical cancer often presents no symptoms. Timely screening enables identification of precancerous lesions, allowing treatment before they develop into invasive cancer. This significantly lowers health burdens, improves survival rates, and enhances long-term patient outcomes globally. - What are the main diagnostic methods used?

Diagnostic methods include Pap tests, HPV DNA testing, liquid-based cytology, colposcopy examinations, and targeted biopsies. These techniques enable detection of cellular abnormalities, viral infections, and disease progression stages, ensuring accurate clinical decision-making for early, effective management. - What factors increase the risk of cervical cancer?

Persistent HPV infection is the primary risk factor. Additional contributors include early sexual activity, multiple partners, smoking, weakened immunity, and limited screening participation. Understanding these risks supports early prevention measures and enhances the effectiveness of diagnostic and screening strategies. - How accurate are current cervical cancer diagnostic tests?

Modern diagnostics exhibit high accuracy, particularly HPV DNA testing, which provides strong sensitivity for identifying high-risk viral strains. Liquid-based cytology and colposcopy also enhance precision, supporting comprehensive diagnostic workflows that improve early detection rates and clinical outcomes. - Which diagnostic technologies are contributing most to market expansion?

Molecular diagnostics, including HPV DNA testing, liquid-based cytology platforms, and automated screening systems, are contributing significantly. These technologies offer improved sensitivity and workflow efficiency, supporting broader adoption and strengthening market penetration across clinical laboratories worldwide. - Which regions hold the largest share of the cervical cancer diagnostic market?

North America and Europe hold dominant market shares due to robust healthcare systems, high awareness levels, and widespread screening programs. Asia-Pacific is experiencing rapid growth, driven by expanding infrastructure, rising disease burden, and greater government focus on screening initiatives. - How is technological innovation influencing the market?

Technological progress is improving test accuracy, automation, and workflow efficiency. Innovations such as AI-enhanced screening, point-of-care HPV tests, and integrated molecular platforms are enabling earlier detection, streamlined processing, and wider accessibility, strengthening market competitiveness.

Conclusion

The global cervical cancer diagnostics market is expected to sustain steady growth, supported by rising screening adoption, technological advancement, and strong public health initiatives. Increased utilization of HPV DNA testing, Pap cytology, and molecular diagnostics has enhanced early detection capabilities, contributing to improved clinical outcomes.

Although disparities in access persist, expanding national programs, digital pathology, and self-sampling innovations are strengthening coverage, particularly in underserved regions. With healthcare investments rising and preventive strategies advancing, the market is projected to experience continued expansion, reinforcing early diagnosis as a critical component in reducing global cervical cancer incidence and mortality.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)