Table of Contents

Overview

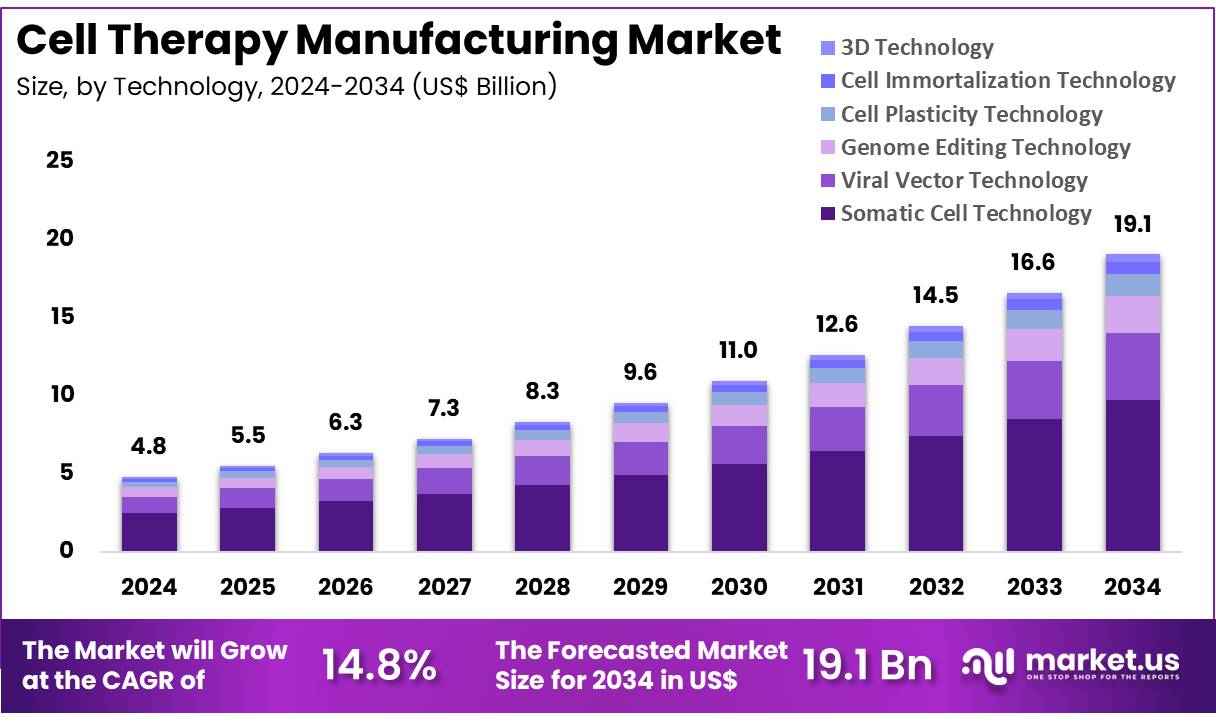

New York, NY – Nov 27, 2025 – Global Cell Therapy Manufacturing Market size is expected to be worth around US$ 19.1 billion by 2034 from US$ 4.8 billion in 2024, growing at a CAGR of 14.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 42.8% share with a revenue of US$ 2.1 Billion.

The Cell Therapy Manufacturing market is experiencing steady expansion as advancements in regenerative medicine, biotechnology, and personalized treatments continue to accelerate. Increasing demand for advanced therapeutic modalities, including stem cell therapies, CAR-T cell therapies, and allogeneic cell-based products, has strengthened the need for scalable, compliant, and cost-efficient manufacturing solutions. Growth of the market is being driven by rising investment in cell-based research, increasing clinical pipeline activity, and the commercialization of novel therapies across oncology, immunology, and rare diseases.

Significant progress in automation, closed-system processing, and single-use technologies has improved manufacturing efficiency. Adoption of Good Manufacturing Practices (GMP) facilities and standardized workflows has enhanced product consistency and reduced operational risk. The expansion of contract development and manufacturing organizations (CDMOs) is supporting companies with limited in-house infrastructure, further contributing to market growth.

The market was valued at several billion dollars in recent years, and sustained growth is expected as regulatory approvals for cell-based therapies continue to increase. North America currently leads the global landscape due to strong research funding and early technology adoption, while Asia-Pacific is emerging rapidly due to cost-effective manufacturing capabilities and expanding clinical activities.

Overall, the Cell Therapy Manufacturing sector is positioned for long-term growth. The rising prevalence of chronic diseases, continued scientific innovation, and supportive regulatory frameworks are expected to reinforce market expansion and strengthen the availability of advanced therapeutic options globally.

Key Takeaways

- The cell therapy manufacturing market generated US$ 4.8 billion in revenue in 2024, and a CAGR of 14.8% has been projected, with the market expected to reach US$ 19.1 billion by 2033.

- The therapy type segment is categorized into allogenic cell therapy and autologous cell therapy, with autologous cell therapy leading in 2024 by accounting for 58.3% of the market share.

- Based on technology, the market includes somatic cell technology, viral vector technology, genome editing technology, cell plasticity technology, cell immortalization technology, and 3D technology. Somatic cell technology dominated in 2024 with a 51.2% share.

- In terms of application, the market is segmented into musculoskeletal, oncology, neurological, gastrointestinal, cardiovascular, and others, with the oncology segment holding the largest revenue share of 53.8%.

- The source segment comprises induced pluripotent stem cells, umbilical cord, neural stem, bone marrow, and adipose tissues, with induced pluripotent stem cells leading at 54.7% of the total revenue.

- North America remained the leading regional market in 2024, capturing a 42.8% market share.

Regional Analysis

North America Leading the Cell Therapy Manufacturing Market

North America accounted for the largest revenue share of 42.8% in the cell therapy manufacturing market, supported by its advanced research ecosystem, a well-established biopharmaceutical sector, and substantial venture capital inflows. More than US$ 20 billion was invested in cell and gene therapy companies in the region between 2021 and 2023, strengthening innovation and commercialization activities. In fiscal year 2024, the U.S. National Institutes of Health (NIH) allocated over US$ 6 billion to cell and gene therapy research, which has contributed to the development of new therapies requiring sophisticated manufacturing capabilities.

The U.S. FDA has approved more than 20 cell and gene therapies since 2017, with a notable increase in approvals after 2021. This regulatory momentum has accelerated demand for scalable and compliant manufacturing solutions. The concentration of leading academic institutions, research centers, and biotechnology companies actively driving cell therapy development reinforces North America’s dominant position in the global market.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to witness the highest CAGR over the forecast period due to rising healthcare investments, expanding regenerative medicine programs, and an increase in cell therapy research initiatives. China has demonstrated annual R&D spending growth of over 15% in the biopharmaceutical sector from 2021 to 2024, while Japan continues to enhance its regenerative medicine capabilities through significant government support, including over US$ 1 billion allocated by AMED in 2023.

Clinical trial activity in the region has increased by more than 40% since 2021, supported by a large patient population and growing adoption of advanced therapies, driving the need for expanded cell therapy manufacturing infrastructure.

Emerging Trends

- Advanced and Distributed Manufacturing: Cell therapy production is shifting toward flexible, distributed manufacturing models. These approaches enable smaller regional facilities to generate therapies closer to patients, reducing logistical risks and improving accessibility. Collaborative initiatives, such as the FDA–VHA MOU, are promoting trusted networks for both emergency and routine cell therapy production.

- Closed, Automated Bioreactor Systems: Closed-system bioreactors are increasingly being adopted to automate critical manufacturing steps under aseptic conditions. These platforms maintain strict control of expansion parameters, including fluid dynamics and mechanical cues, thereby lowering contamination risks and enhancing overall product consistency.

- Expanded Regulatory Guidance and Lifecycle Focus: Regulatory agencies have issued new guidance documents to address evolving cell therapy manufacturing challenges. Draft guidances on comparability studies and genome editing (2023–2025) reinforce a lifecycle-based framework, requiring manufacturers to manage process changes while ensuring sustained product quality.

- Integration of Artificial Intelligence and Data Science: AI and machine learning tools are gaining validation for real-time monitoring and optimization of manufacturing processes. Since 2016, more than 70 IND submissions have incorporated AI/ML for anomaly detection and process control, demonstrating increasing regulatory acceptance of data-driven analytics.

Use Cases

- Autologous CAR-T Cell Therapies: Autologous CAR-T manufacturing is used to treat hematologic malignancies by engineering a patient’s T cells. Six FDA-approved CAR-T products including Kymriah, Yescarta, and Carvykti utilize leukapheresis, genetic modification, and ex vivo expansion, achieving complete response rates of up to 67% in lymphoma.

- Regenerative Medicine Advanced Therapies (RMAT): Six therapies have received RMAT designation as of March 31, 2025, covering indications such as metastatic melanoma and congenital athymia. Recent approvals, including Amtagvi (2024) and Lyfgenia (2023), depend on scalable vector production and precision cell culture to deliver batches containing up to 5×10¹² vector genomes or 1×10 viable cells.

Frequently Asked Questions on Cell Therapy Manufacturing

- How are cells sourced for manufacturing?

Cells are commonly obtained from autologous or allogeneic sources. Autologous cells are collected directly from the patient, while allogeneic cells originate from healthy donors. Both pathways require strict screening, traceability, and regulatory compliance to ensure product safety. - What steps are involved in the manufacturing workflow?

The manufacturing workflow includes cell isolation, activation, genetic modification when required, expansion, harvesting, formulation, and cryopreservation. Each stage is performed under Good Manufacturing Practice standards to ensure product consistency, purity, and viability. - Why is quality control important in cell therapy production?

Quality control ensures that every batch meets safety, identity, potency, and sterility requirements. Rigorous testing reduces risks associated with contamination, variable cell performance, and batch failure, thereby supporting regulatory approval and patient safety outcomes. - What are the major challenges in cell therapy manufacturing?

Key challenges include process scalability, high production costs, complex supply chains, and variability in biological materials. Regulatory constraints, workforce shortages, and technological limitations also contribute to manufacturing inefficiencies and delayed commercialization timelines. - Which segments dominate the market?

Autologous and allogeneic manufacturing segments dominate the market. Autologous therapies lead early commercialization, while allogeneic platforms gain traction due to scalability advantages. Service-based manufacturing and advanced technology platforms also contribute significantly to overall market performance. - Which regions hold the largest market share?

North America holds a significant share due to strong research infrastructure, funding availability, and supportive regulatory pathways. Europe follows closely with robust manufacturing capacity, while Asia-Pacific is experiencing rapid growth driven by expanding biotechnology ecosystems. - What is the market outlook for the next decade?

The market is projected to grow steadily as clinical successes increase and advanced manufacturing technologies mature. Investments from pharmaceutical firms and continued regulatory support are expected to accelerate commercialization, expanding global access to cell-based therapeutic solutions.

Conclusion

The cell therapy manufacturing market is positioned for sustained, long-term expansion as advancements in regenerative medicine, personalized therapies, and biotechnology continue to accelerate global adoption. Rising investment, expanding clinical pipelines, and increasing regulatory approvals are strengthening demand for scalable and compliant manufacturing systems.

Progress in automation, closed-system processing, and AI-driven optimization is enhancing product quality and operational efficiency. North America maintains market leadership, while Asia Pacific is emerging rapidly with robust R&D and manufacturing growth. Overall, the sector is expected to advance steadily as scientific innovation, supportive policies, and increasing therapeutic needs reinforce global market momentum.