Table of Contents

Overview

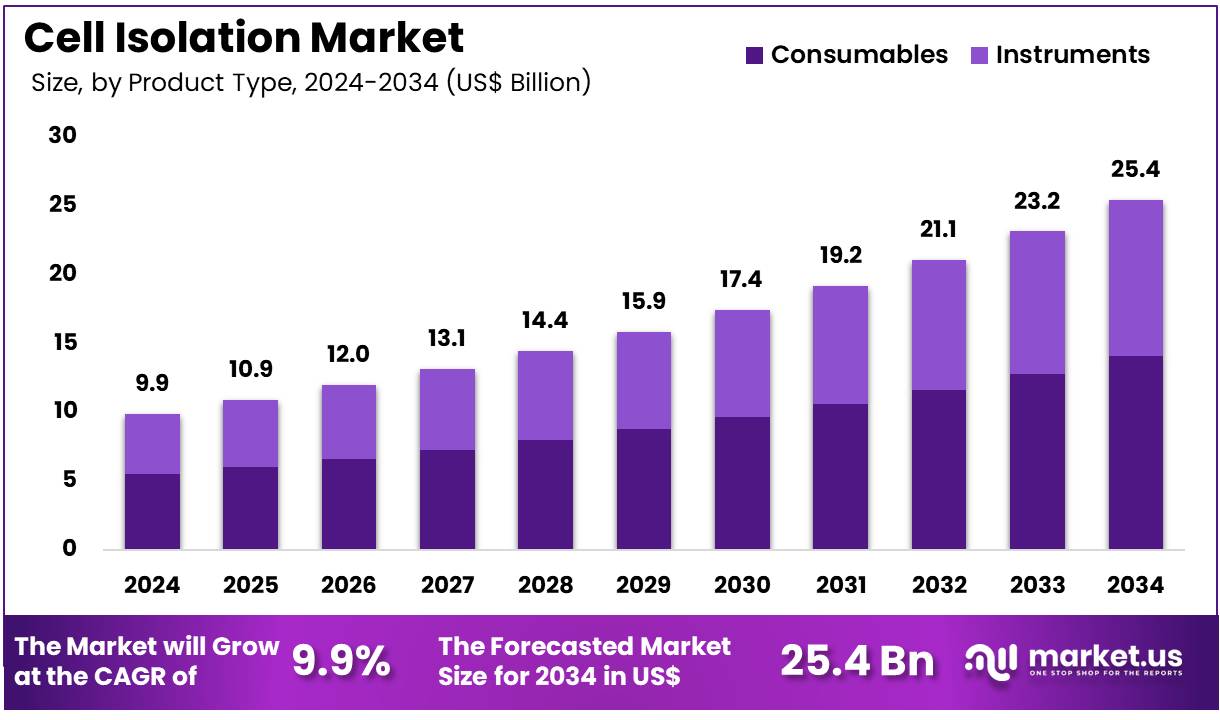

New York, NY – Nov 18, 2025 – Global Cell Isolation Market size is expected to be worth around US$ 25.4 Billion by 2034 from US$ 9.9 Billion in 2024, growing at a CAGR of 9.9% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 40.8% share with a revenue of US$ 4.0 Billion.

The global cell isolation market has been experiencing sustained expansion, supported by rising investments in biotechnology, regenerative medicine, and advanced cell-based research. Cell isolation, defined as the extraction of specific cell populations from heterogeneous biological samples, has become a critical process within diagnostics, therapeutics development, and translational research. The demand for high-purity cells has increased due to the growing adoption of cell-based assays, stem-cell studies, and personalized medicine programs.

The growth of the market can be attributed to the increasing prevalence of chronic diseases and the heightened emphasis on early-stage drug discovery. Continuous improvements in magnetic-activated and fluorescence-activated cell sorting technologies have enhanced accuracy, throughput, and reproducibility, thereby strengthening adoption across research institutions and biopharmaceutical companies. Expanded usage in immunology, oncology, and neurology research has further accelerated the requirement for efficient isolation platforms.

The market is also being supported by the rising availability of automated systems that reduce manual error and improve workflow consistency. Additionally, government-funded research programs and strategic industry collaborations have contributed to the broadening application landscape.

While high equipment costs and technical complexities continue to pose challenges, steady innovation and the development of user-friendly solutions are expected to mitigate these constraints. Overall, the cell isolation market is positioned for continued growth as scientific and clinical communities increase reliance on precise cellular analysis for therapeutic development and disease understanding.

Key Takeaways

- In 2024, the Cell Isolation market generated revenue of US$ 9.9 Billion, recorded a CAGR of 9.9%, and is projected to reach US$ 25.4 Billion by 2033.

- The product type segment is categorized into consumables and instruments, with consumables leading the market in 2024 with a 55.3% share.

- Based on technology, the market is segmented into centrifugation, surface marker, and filtration, with centrifugation accounting for a significant 49.5% share.

- In terms of application, the market comprises biomolecule isolation, cancer research, tissue regeneration, therapeutics, stem cell research, and in vitro diagnostics. Biomolecule isolation dominated this segment with a 31.7% revenue share.

- The cell type segment is divided into human cells and animal cells, with animal cells leading at 63.5% market share.

- By end-user, the market includes research laboratories and institutes, hospitals & diagnostic laboratories, cell banks, and biotechnology & biopharmaceutical companies, the latter holding a notable 41.3% share.

- North America emerged as the leading regional market, capturing a 40.8% share in 2024.

Regional Analysis

North America Leading the Cell Isolation Market

North America dominated the cell isolation market by capturing a revenue share of 40.8%, supported by strong advancements in biotechnology, growing demand for personalized medicine, and increased investments in regenerative medicine research. Funding for cell-based studies by the National Institutes of Health (NIH) increased by 18% in 2023, with a notable allocation directed toward isolation technologies. The U.S. Food and Drug Administration (FDA) approved more than 20 cell-based therapies during the same period, many of which required precise isolation methods.

Major industry players, including Thermo Fisher Scientific and BD Biosciences, introduced advanced magnetic bead-based isolation systems that achieved broad adoption. The Centers for Disease Control and Prevention (CDC) reported a 15% rise in clinical trials using isolated stem cells in 2023, while the Canadian Institutes of Health Research (CIHR) recorded a 12% increase in grants for cancer research utilizing isolation techniques.

Rising cancer and autoimmune disease incidence, supported by a 10% increase in U.S. cancer diagnoses between 2022 and 2024, further strengthened market demand. These factors, combined with expanding biobanking initiatives and greater use of single-cell analysis, have reinforced North America’s leadership position.

Asia Pacific Expected to Record the Highest CAGR

Asia Pacific is projected to register the fastest growth rate due to increasing healthcare investments, a rising chronic disease burden, and expanding biotechnology research capabilities. The World Health Organization (WHO) highlighted a 20% rise in government funding for life sciences research between 2022 and 2024. China recorded a 25% increase in stem-cell research funding in 2023, while the Indian Council of Medical Research (ICMR) reported a 15% rise in the adoption of cell-based therapies in public hospitals.

Cancer incidence continues to rise, with the International Agency for Research on Cancer (IARC) estimating a 12% increase in cases across the region from 2022 to 2024. Collaborations between global companies such as Merck and regional biotechnology firms have facilitated the availability of cost-effective isolation technologies suited to local needs.

Japan also reported a 10% increase in the use of isolation tools in regenerative medicine projects. These developments, supported by expanding biomanufacturing capacity and growing interest in precision medicine, are expected to drive strong market growth in Asia Pacific.

Emerging Trends

The adoption of affinity-based cell separation has increased because it provides high yield and purity while remaining scalable for both research and clinical use. Techniques such as magnetic bead-based separation and antibody-mediated capture have become central to isolation workflows, as they consistently achieve recovery rates above 90% for target cells obtained from complex biological samples.

Microfluidic and label-free isolation methods are also gaining attention. Advances in spectral flow cytometry and cytomics now allow multi-parameter analysis and high-speed sorting exceeding 10,000 cells per second, reducing sample volume requirements and operator involvement. Newer microfluidic platforms use hydrodynamic, acoustic, or dielectrophoretic forces to isolate cells without labeling, ensuring that cell viability and function are preserved for downstream applications.

Substantial public-sector funding is accelerating progress in single-cell isolation technologies. In 2024, the National Cancer Institute awarded a USD 14.4 million grant to support the development of traceless, aptamer-based isolation systems designed for cell therapy manufacturing. This investment is encouraging innovations that aim to isolate millions of cells per experiment with minimal disruption, thereby strengthening both fundamental research and therapeutic production.

Use Cases

- CAR-T Cell Therapy Manufacturing: Autologous CAR-T cell production relies on isolating patient-derived T cells from peripheral blood mononuclear cells through magnetic bead-based enrichment. Review of ClinicalTrials.gov data indicates that 679 CAR-T trials have been completed, with 195 studies (28.7%) publishing results, highlighting the essential function of high-quality cell isolation in therapy development and performance evaluation.

- Single-Cell and Spatial Omics: The NIH Common Fund’s HuBMAP program intends to map tissues at single-cell resolution by isolating between 10 million and 100 million cells per experiment for transcriptomic and proteomic analyses. This capability is enabling the creation of advanced 3D cellular atlases that support deeper understanding of cell-type distribution in normal and diseased states.

- High-Throughput Clinical Diagnostics: Modern flow cytometers and microfluidic sorting platforms support immunophenotyping and rare-cell detection, including circulating tumor cells, by processing more than 20,000 events per second. These capabilities allow clinical laboratories to deliver rapid diagnostic outputs for hematological malignancies and infectious disease monitoring.

Frequently Asked Questions on Cell Isolation

- Why is cell isolation important in research?

Cell isolation is essential because it provides purified cell populations required for reliable experimentation. The process supports accurate characterization, controlled testing conditions, and the development of targeted therapies. Research outcomes are strengthened through improved reproducibility enabled by consistently isolated and defined cell subsets. - What methods are used for cell isolation?

Cell isolation methods include centrifugation, magnetic-activated cell sorting, fluorescence-activated cell sorting, and microfluidic techniques. Each method is chosen based on required purity levels, sample type, and desired throughput, enabling optimized workflows for various biological research and clinical applications. - What factors influence the selection of a cell isolation technique?

Technique selection is influenced by sample complexity, required purity, target cell abundance, viability needs, and downstream applications. Cost, processing time, and instrument availability also play significant roles in determining the most suitable isolation strategy for laboratory workflows. - What is driving growth in the cell isolation market?

Market growth is supported by rising investments in cell-based research, increasing prevalence of chronic diseases, and expanding applications in regenerative medicine. Strong demand for precision therapeutics and high-purity cell products also contributes to sustained industry expansion globally. - Which technologies dominate the cell isolation market?

Magnetic-activated cell sorting and fluorescence-activated cell sorting dominate due to high specificity, scalability, and compatibility with advanced research workflows. These technologies offer improved accuracy, rapid processing capabilities, and suitability for complex analytical applications across biotechnology and clinical laboratories. - Which end-use sectors contribute most to market demand?

Biotechnology companies, academic institutes, and research laboratories contribute significantly to demand. Clinical diagnostic centers and pharmaceutical firms also demonstrate strong adoption as cell-based assays, immunotherapy research, and personalized medicine initiatives continue to grow across key global regions. - What regions are experiencing the fastest market growth?

North America leads in market share due to strong research infrastructure, while Asia-Pacific exhibits the fastest growth driven by expanding biotechnology investments. Europe maintains stable demand supported by advanced academic research and rising adoption of high-precision cell isolation tools.

Conclusion

The global cell isolation market continues to demonstrate strong, sustained growth driven by advancements in biotechnology, expanding clinical applications, and rising investment in cell-based research. Increasing dependence on high-purity cells for diagnostics, therapeutics, and regenerative medicine has reinforced the importance of advanced isolation technologies.

North America maintains a leading position, while Asia Pacific is projected to grow rapidly due to expanding research capabilities and healthcare investment. Although high equipment costs and technical complexities persist, continuous innovation, automation, and broader adoption across research and clinical settings are expected to support steady market expansion throughout the forecast period.