Table of Contents

Overview

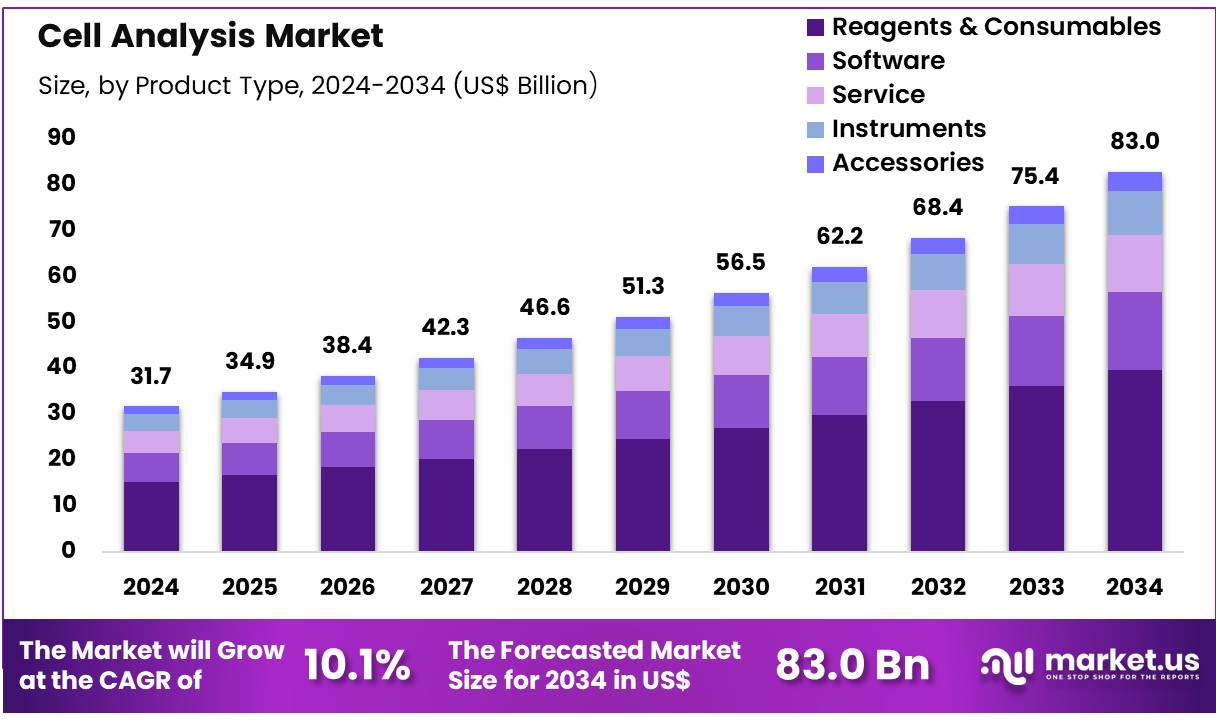

New York, NY – Dec 01, 2025 – Global Cell Analysis Market size is expected to be worth around US$ 83.0 Billion by 2034 from US$ 31.7 Billion in 2024, growing at a CAGR of 10.1% during the forecast period 2025 to 2034.

The global cell analysis market has been observed to expand at a steady pace as demand for advanced research methodologies continues to rise across biotechnology, pharmaceutical, and academic environments. Significant growth has been supported by the increasing adoption of single-cell technologies, high-content screening systems, and automated platforms that enable precise cell characterization and functional evaluation. The market has also been influenced by the surge in chronic diseases, which has increased reliance on cell-based assays for drug discovery and diagnostics.

According to recent industry assessments, strong investment flows into life science research infrastructure have strengthened the global adoption of innovative analytical instruments. The expansion of stem cell research, immuno-oncology studies, and regenerative medicine has further accelerated the integration of specialized cell analysis systems. The growth of the market can be attributed to continuous technological upgrades that improve speed, sensitivity, and throughput in laboratory workflows.

North America has maintained a dominant share due to advanced research facilities and significant funding activities, while Asia-Pacific has been recognized as a high-growth region supported by expanding biotechnology sectors and government initiatives promoting scientific development. The cell analysis market is expected to witness sustained growth as organizations prioritize accuracy, reproducibility, and automation in experimental processes.

Key Takeaways

- In 2024, the cell analysis market generated revenue of US$ 31.7 billion, supported by a 10.1% CAGR, and is projected to reach US$ 83.0 billion by 2033.

- By product type, the market is categorized into reagents & consumables, software, services, instruments, and accessories, with reagents & consumables leading at 47.9% of the total share in 2024.

- Based on technology, the segmentation includes flow cytometry, PCR, microscopy, cell microarrays, and others; flow cytometry accounted for the largest share at 49.6%.

- In the application category, the market is segmented into cell interaction, cell viability, cell signaling pathways, cell proliferation, cell identification, and others, with cell interaction emerging as the leading application at 42.5%.

- The end-user segmentation comprises pharmaceutical & biotechnology companies, academic & research institutes, hospitals & clinical testing laboratories, and others. Pharmaceutical & biotechnology companies dominated the segment with a 60.4% revenue share.

- Regionally, North America held the highest share of the cell analysis market in 2024, accounting for 40.5%.

Market Segmentation Analysis

- Product Type Analysis: The reagents and consumables segment held 47.9% of the market in 2023, supported by rising laboratory research needs and expanding biopharmaceutical activities. Continuous innovation to deliver cost-effective, high-performance materials and increasing genomics and immunology research are expected to sustain segment growth.

- Technology Analysis: Flow cytometry accounted for 49.6% of the market due to its rapid, multiparametric cellular analysis capabilities. Its expanding use in oncology, infectious diseases, and immunology, coupled with technological improvements such as automation, enhanced resolution, and AI integration, continues to strengthen adoption across research and clinical diagnostics.

- Application Analysis: Cell interaction dominated with a 42.5% share, driven by rising demand to examine cellular communication in complex systems. Growing use of live-cell imaging and advanced assays supports precision research. Increasing emphasis on cellular drug-response evaluation is expected to maintain steady growth of this application segment.

- End-user Analysis: Pharmaceutical and biotechnology companies represented 60.4% of revenue, reflecting strong dependence on cell analysis for drug development, biomarker discovery, and safety assessment. Increasing adoption of biologics, gene therapies, and personalized treatments is reinforcing the need for advanced cell analysis tools within R&D pipelines.

Regional Analysis

North America Leading the Cell Analysis Market

North America has been identified as the leading region in the cell analysis market, accounting for a revenue share of 40.5%. The growth of the region has been supported by the increasing integration of advanced analytical tools in drug discovery and development processes. Significant contributions from the National Institutes of Health (NIH) have strengthened regional research activities. In fiscal year 2023, the NIH allocated a major portion of its US$ 47.7 billion budget to extramural research, which included projects focused on understanding disease mechanisms. These initiatives rely extensively on advanced cell analysis techniques, thereby driving market demand.

Further momentum has been generated by the U.S. Food and Drug Administration (FDA), which emphasizes the use of in vitro studies and cell-based models for evaluating drug safety and efficacy. Guidance documents issued between 2022 and 2024 have reinforced the importance of cell-based assays in regulatory submissions, enhancing their adoption across the pharmaceutical landscape in North America.

Asia Pacific Expected to Record the Highest CAGR

The Asia Pacific region is projected to register the fastest CAGR during the forecast period due to rising investments in pharmaceutical and biotechnology industries. Expanding research capabilities in countries such as China and India are expected to accelerate the adoption of advanced cell analysis technologies.

Government initiatives in China to bolster its biopharmaceutical sector are anticipated to increase demand for these tools in drug screening applications. According to the National Bureau of Statistics, China’s R&D expenditure reached 2.54% of GDP in 2022. In addition, the increasing burden of chronic diseases across the region is expected to promote research activities that rely heavily on advanced analytical methodologies.

Use Cases

- Leukemia Diagnostics: The addition of flow cytometry to standard cytomorphology in pediatric B-cell acute lymphoblastic leukemia increased central nervous system involvement detection from 4% to 17% of cerebrospinal fluid samples. Earlier clinical intervention was enabled in 33 of 165 evaluated cases.

- Point-of-Care Infectious Disease Testing: The FDA authorized the Reveal® G4 Rapid HIV-1/2 Antibody Test in 2023 as a single-use immunoassay suitable for whole blood, serum, or plasma. Its approval supports same-visit HIV screening in clinics operating without centralized laboratory infrastructure.

- Cancer Companion Diagnostics: Companion diagnostic technologies have expanded, with FDA listings indicating more than 50 cleared in vitro and imaging-based tools for matching oncology patients to targeted therapies. These devices are strengthening precision medicine adoption across cancer treatment centers.

- Cell Therapy Quality Control: Flow cytometry panels with 8-color and 13-parameter configurations are routinely applied to characterize therapeutic cell products. This approach ensures compliance with purity thresholds exceeding 95% prior to infusion in regenerative medicine clinical trials.

- Vaccine Immune Profiling: Single-cell RNA sequencing has been used in COVID-19 vaccine research to analyze more than 100,000 immune cells per study. The method enables quantification of rare T-cell subsets associated with protective antibody responses in phase II clinical cohorts.

Frequently Asked Questions on Cell Analysis

Why is cell analysis important in research?

Cell analysis is important because it provides insights into cellular mechanisms that drive disease progression, therapeutic responses, and biological interactions. These insights support the development of targeted treatments and improve understanding of complex biological systems.

What technologies are commonly used in cell analysis?

Common technologies include flow cytometry, microscopy, PCR, cell microarrays, and high-content screening platforms. These technologies support high-precision cellular characterization, enabling accurate measurement of cell viability, proliferation, signaling pathways, and functional responses.

Which segment holds the largest share in the cell analysis market?

Reagents and consumables currently hold the largest market share due to frequent usage in experimental workflows. This segment benefits from continuous demand in laboratories, supporting routine analysis, assay development, and large-scale research activities.

Which technology dominates the cell analysis market?

Flow cytometry dominates the market because it offers rapid, accurate, and multiparametric cell evaluation. Its ability to analyze large cell populations in real time makes it essential for immunology, oncology, and drug development studies.

Which region leads the global cell analysis market?

North America leads the market due to strong research infrastructure, significant funding for life sciences, and high adoption of advanced analytical tools. Government support and active biotechnology sectors further strengthen regional dominance.

What are the key applications of cell analysis?

Key applications include studying cell interaction, viability, proliferation, identification, and signaling pathways. These applications support deeper understanding of cellular responses and are essential for drug development, toxicology assessments, and disease research.

Who are the major end users of cell analysis tools?

Major end users include pharmaceutical and biotechnology companies, academic research institutions, and clinical laboratories. These stakeholders rely on advanced tools to support drug discovery, biological studies, and diagnostic testing activities.

Conclusion

The global cell analysis market is positioned for sustained expansion as demand for advanced analytical technologies continues to strengthen across research, clinical, and industrial environments. Growth has been supported by rising investment in life science infrastructure, increasing emphasis on precision research, and continued advancements in single-cell and high-throughput systems.

Dominance of North America and accelerated development in Asia Pacific reflect broad global adoption. Strong utilization within pharmaceutical and biotechnology organizations is expected to maintain momentum, supported by expanding applications in drug discovery, diagnostics, immunology, and regenerative medicine. The market is projected to remain on a steady upward trajectory through the forecast period.