Table of Contents

Overview

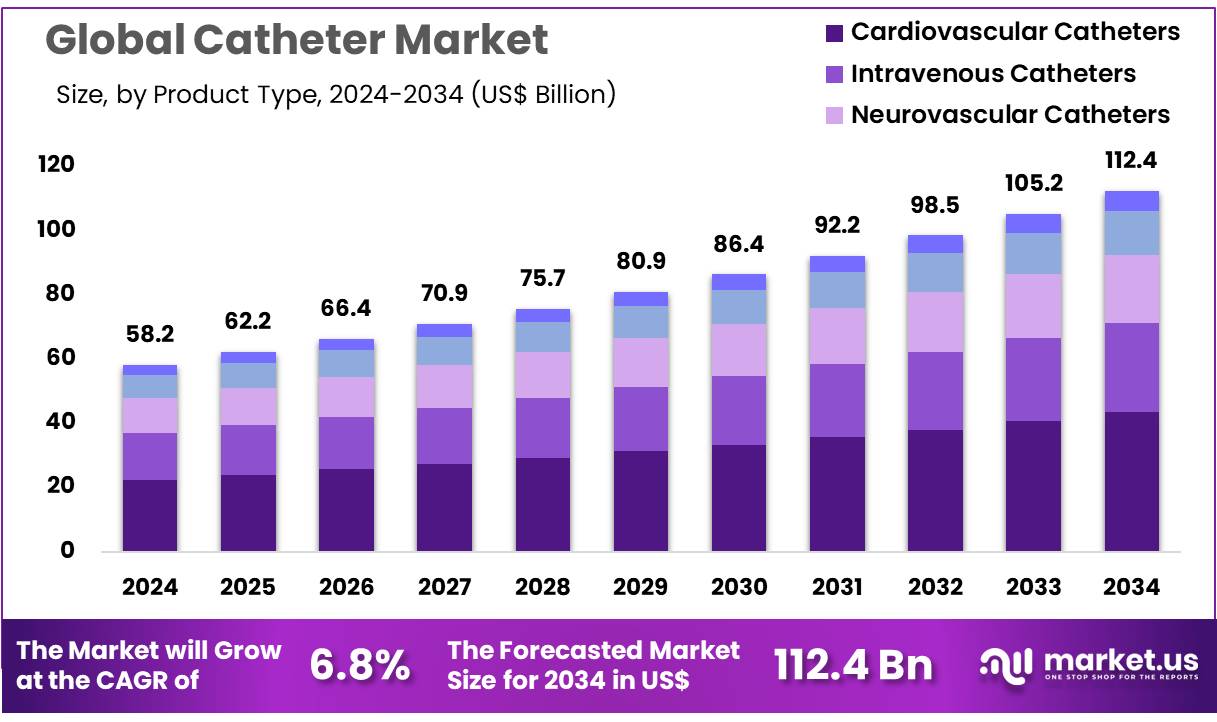

New York, NY – Nov 10, 2025 – Global Catheter Market size is expected to be worth around US$ 112.4 Billion by 2034 from US$ 58.2 Billion in 2024, growing at a CAGR of 6.8% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.7% share with a revenue of US$ 23.1 Billion.

The global catheter market has been expanding as demand for advanced medical devices continues to rise across healthcare settings. The increasing incidence of chronic diseases, the growing need for minimally invasive procedures, and expanded hospital infrastructure have contributed to the steady adoption of catheter solutions worldwide. Product development has been focused on improved safety, precision, and patient comfort, leading to a shift toward technologically enhanced designs.

Catheters have been utilized for a wide range of clinical applications, including cardiovascular intervention, urology, neurology, and general surgery. The growth of the market has been attributed to the rising number of diagnostic and therapeutic procedures that require reliable vascular and non-vascular access. Enhanced material technologies have supported the production of catheters with improved biocompatibility and durability, strengthening overall performance in critical care environments.

Manufacturers have directed investment toward research and innovation, enabling the introduction of antimicrobial coatings, steerable navigation systems, and products designed for long-term use. These advancements have been recognized as crucial in reducing procedure-related complications and supporting better clinical outcomes. Regulatory approvals have further facilitated product availability across major healthcare markets.

Hospitals and specialty clinics have remained the primary end users, although demand in home healthcare settings has increased due to the rising preference for personalized care. Market growth is expected to continue as healthcare providers prioritize devices that enhance efficiency, reduce infection risks, and support advanced therapeutic interventions.

The catheter segment is positioned for sustained expansion, supported by continuous technological progress and increasing global healthcare needs.

Key Takeaways

- In 2024, the catheter market generated revenue of US$ 58.2 billion, with a CAGR of 6.8%, and it is projected to reach US$ 112.4 billion by 2033.

- The product type segment includes cardiovascular catheters, intravenous catheters, neurovascular catheters, urology catheters, and specialty catheters, with cardiovascular catheters leading the market in 2023 by accounting for 38.6% of the share.

- By end user, the market is categorized into hospital stores, retail stores, and others, where hospital stores contributed 54.4% to the overall share.

- North America dominated the global market in 2023, securing a 39.7% share.

Regional Analysis

North America is leading the Catheter Market

North America accounted for the largest revenue share of 39.7 percent, supported by the rising prevalence of cardiovascular diseases and steady progress in minimally invasive procedures. According to the American College of Cardiology, more than 12 million individuals in the United States were living with peripheral artery disease (PAD) as of July 2023, indicating increasing reliance on catheter-based interventions.

The growing incidence of heart arrhythmias, coronary blockages, and congenital heart defects has continued to elevate the need for advanced vascular access devices. Technological improvements, including drug-coated and bioresorbable catheters, have been associated with better clinical outcomes and reduced procedural risks. The expanding geriatric population, which experiences a higher rate of cardiovascular complications, further strengthened market adoption.

Strong research and development investments by medical device manufacturers have resulted in next-generation catheters with improved flexibility and precision. Supportive government initiatives focused on early diagnosis and favorable reimbursement frameworks have contributed to the expansion of catheter usage across the United States and Canada.

Asia Pacific is expected to witness the highest CAGR during the forecast period

Asia Pacific is projected to register the fastest growth rate due to rising healthcare spending and increasing cardiovascular disease incidence. Improvements in healthcare infrastructure in China, India, and Japan are expected to enhance access to advanced medical interventions. Government efforts to promote early detection and preventive healthcare are likely to support greater adoption of minimally invasive procedures.

Partnerships between global manufacturers and regional providers are anticipated to increase availability and affordability of innovative vascular devices. The rising impact of lifestyle-related disorders such as diabetes and hypertension is expected to stimulate demand for advanced cardiovascular tools.

Growing utilization of robotic-assisted and AI-integrated interventional systems is projected to improve surgical precision and patient outcomes. Additionally, expanding medical tourism, particularly in countries offering cost-efficient cardiac care, is expected to support market growth across the region.

Emerging Trends in the Catheter Market

- Advanced Device Approvals: The approval of several catheter devices by the U.S. Food and Drug Administration in 2024 indicated a transition toward technologies with specialized clinical functions. Devices such as the VARIPULSE platform, cleared in November 2024, and the Sphere-9 catheter, cleared in October 2024, were developed to enhance precision during electrophysiology procedures. These advancements highlight a growing focus on integrated systems that combine diagnostic and therapeutic capabilities within a single catheter.

- Real-Time Tip Guidance and Reduced Radiation Exposure: A noticeable shift toward radiation-free navigation methods has been observed, driven by technologies that rely on the patient’s intrinsic cardiac signals. The ECGuide technology, cleared in 2024, enables clinicians to confirm catheter tip location by analyzing ECG waveforms, reducing dependence on X-ray imaging. With an estimated 8.5 million PICCs placed globally each year, including more than 3 million in the United States, these real-time confirmation systems support safer workflows and minimize radiation exposure during central venous and PICC procedures.

- Enhanced Safety Features: Safety-oriented catheter designs have gained prominence, with new devices incorporating automatic needlestick protection and improved blood control functionality. A notable 2024 clearance introduced an IV catheter with passive, fully automatic needlestick protection and extended-length options for deeper vein access. The device was designed to maintain catheter patency for longer durations, supporting patients with challenging vascular access and reducing complications related to frequent catheter replacement.

- Infection Prevention and Evidence-Based Selection Guidelines: In 2024, infection prevention efforts increasingly emphasized structured, evidence-based catheter selection. Updated CDC recommendations advised choosing catheter types based on therapy duration, suggesting midline or PICC placement when IV treatment exceeds six days. The guidelines also reinforced ultrasound-guided insertion to reduce mechanical complications and improve first-attempt success rates. These measures align with broader initiatives aimed at lowering CAUTI and central line–associated bloodstream infection rates through standardized clinical protocols.

Frequently Asked Questions on Catheter

- What are the main types of catheters?

The primary catheter types include urinary, cardiovascular, intravenous, and neurovascular catheters. Each type is developed for specialized clinical functions, and its selection is based on patient condition, procedural needs, and therapeutic requirements. - What materials are commonly used in catheter manufacturing?

Catheters are commonly manufactured using silicone, latex, polyurethane, and PVC. These materials are selected for flexibility, patient safety, and biocompatibility, ensuring reliable performance across diagnostic, therapeutic, and long-term care applications in diverse clinical environments. - How is catheter safety ensured?

Catheter safety is ensured through sterile manufacturing processes, biocompatible materials, strict regulatory testing, and usage guidelines. Infection control protocols and proper handling techniques are followed to minimize complications such as catheter-associated infections or device-related injuries. - What complications are associated with catheter use?

Common complications include infections, blockages, discomfort, and accidental dislodgement. These issues are managed through regular monitoring, proper hygiene, timely replacement, and adherence to clinical protocols designed to maintain device performance and patient safety. - Which segments dominate the catheter market?

The urinary and cardiovascular catheter segments dominate due to high procedural volumes and increasing incidence of urological and cardiac disorders. Continuous product innovation and rising demand for minimally invasive treatments further strengthen their market share. - What regions are leading the catheter market?

North America leads due to advanced healthcare infrastructure, high treatment rates, and strong adoption of innovative devices. Europe follows closely, while Asia-Pacific is experiencing rapid expansion driven by improving healthcare access and rising patient populations. - Who are the major players in the catheter market?

Major companies include Boston Scientific, Medtronic, Bard, Teleflex, and Coloplast. Their market presence is supported by broad product portfolios, continuous R&D investment, and strong distribution networks across hospitals, clinics, and home care settings.

Conclusion

The catheter market is expected to maintain steady growth as demand for advanced, minimally invasive solutions continues to rise. Expansion has been supported by increasing procedural volumes, technological improvements, and greater emphasis on safety and infection control.

Strong adoption in hospitals and growing use in home care settings have reinforced overall market performance. Advancements in materials, navigation systems, and antimicrobial technologies are enhancing clinical outcomes and reducing complication risks.

North America remains the leading region, while Asia Pacific is projected to grow rapidly due to improving healthcare infrastructure. Continued innovation and supportive regulations are expected to sustain long-term market expansion.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)