Table of Contents

Overview

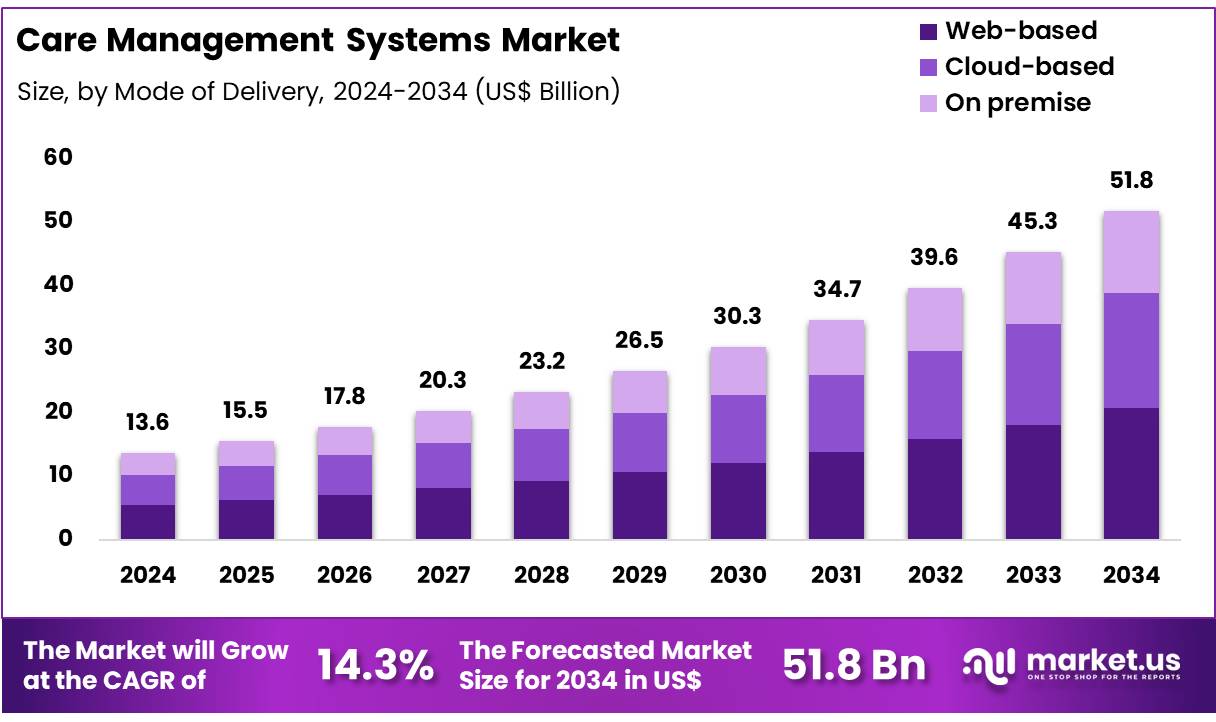

New York, NY – Dec 01, 2025 – Global Care Management Systems Market size is expected to be worth around US$ 51.8 Billion by 2034 from US$ 13.6 Billion in 2024, growing at a CAGR of 14.3% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 50.2% share with a revenue of US$ 6.8 Billion.

The global Care Management Systems market is witnessing steady expansion as healthcare providers prioritize coordinated care delivery, patient engagement, and value-based service models. The demand for integrated platforms has been strengthened by the increasing burden of chronic diseases and a rising shift toward digitized clinical workflows. The growth of the market has also been supported by the adoption of population health management strategies across hospitals, payers, and long-term care organizations.

Care Management Systems are being deployed to streamline clinical data, enhance communication among multidisciplinary teams, and improve patient outcomes through real-time monitoring and analytics. The integration of electronic health records, telehealth solutions, and AI-driven decision-support tools has been accelerated, thereby contributing to higher implementation rates across developed and emerging markets.

Increasing healthcare expenditure, favorable regulatory initiatives, and the expansion of cloud-based solutions have further strengthened market penetration. The need to reduce hospital readmissions and improve operational efficiency has been identified as a major driver, while data privacy concerns and interoperability challenges continue to restrict adoption in certain regions.

North America has been leading the market due to robust digital health infrastructure, while Asia-Pacific is expected to record the fastest growth, supported by government-led modernization of healthcare systems. Strategic collaborations, product innovations, and investments in advanced analytics are expected to shape the competitive landscape over the coming years. The Care Management Systems market is anticipated to maintain a positive trajectory as healthcare providers continue to adopt intelligent, patient-centered digital solutions.

Key Takeaways

- The global care management systems market was valued at USD 13.6 billion in 2024 and is projected to reach USD 51.8 billion by 2034, reflecting a CAGR of 14.3%.

- The software segment accounted for 56.4% of the total revenue share in 2024, indicating its dominant position.

- The web-based delivery model led the market with a 40.3% share of global revenue.

- The healthcare providers segment represented 55.3% of the total revenue, maintaining its leading role in the market.

- North America held over 50.2% of the global revenue share, sustaining its position as the largest regional market.

Regional Analysis

North America has maintained a leading position in the care management solutions market as the adoption of patient-centric digital platforms continues to expand across healthcare systems. The region has benefited from the increasing utilization of cloud-based software, which has improved data accessibility, enhanced provider collaboration, and supported the growth of remote patient monitoring capabilities. These advancements have enabled healthcare organizations to achieve key goals such as cost reduction, operational efficiency, and improved care quality.

Rapid technological progress in artificial intelligence, machine learning, and advanced data analytics has further strengthened the adoption of care management solutions. These technologies have supported higher levels of patient engagement, empowered personalized care plans, and improved clinical decision-making. Substantial investment activity within the healthcare technology sector has reinforced this momentum.

In February 2024, HealthSnap, a provider of Chronic Care Management (CCM) and Remote Patient Monitoring (RPM) solutions, secured USD 25 million in a Series B funding round. The investment, led by Acronym Venture Capital, Florida Opportunity Fund, and Sands Capital, illustrated the growing venture capital commitment to digital health platforms.

These developments, supported by government incentives and reforms promoting value-based care, have contributed significantly to North America’s continued dominance in the market. As healthcare providers across the region increasingly emphasize improved patient outcomes and cost-efficient service delivery, the demand for comprehensive and integrated care management solutions is expected to demonstrate sustained growth in the coming years.

Emerging Trends

- Digital Health Adoption for Equitable Access: The WHO’s Global Strategy on Digital Health emphasizes the use of digital technologies to improve efficiency, affordability, and equity in care delivery. Telemedicine, mobile health tools, and health information systems are being promoted to reduce access gaps in low- and middle-income regions and to support universal health coverage objectives.

- Expansion of Telehealth and Remote Services: HHS data show that 25 percent of Medicare fee-for-service beneficiaries used at least one telehealth service in 2023, indicating sustained demand. Policy updates extending telehealth flexibilities through September 30, 2025 ensure continued access for rural, elderly, and home-bound patients.

- Integration of Social Determinants of Health: The 2024–2025 Physician Fee Schedule final rule introduced four new care management services addressing health-related social needs. These services covering caregiver training, social risk assessments, community health integration, and illness navigation strengthen whole-person care and formalize efforts to address non-clinical barriers for Medicare beneficiaries.

- Administrative Burden Reduction via Technology: CMS’s five-year “Optimizing Care Delivery” strategy focuses on reducing administrative complexity through automation and interoperability improvements. Enhancements in prior authorization processes, data exchange, and clinical decision support are expected to improve provider workflow efficiency and the patient experience over the next decade.

Use Cases

- Chronic Conditions Management: Medicare data show that most beneficiaries live with multiple chronic diseases, representing significant healthcare spending. Care management systems use this information for risk stratification, multidisciplinary coordination, and targeted interventions designed to reduce hospitalizations and improve quality outcomes.

- Telehealth-Enabled Care Coordination: With a quarter of Medicare FFS beneficiaries accessing telehealth in 2023, care management platforms integrate virtual visits to support follow-ups, medication management, and patient education. This approach reduces transportation barriers and strengthens chronic disease monitoring in underserved communities.

- Accountable Care Organization (ACO) Integration: Under the Medicare Shared Savings Program, ACOs utilize care management systems to coordinate care across providers. In 2022, the program generated over US$1.8 billion in savings while improving key outcomes, demonstrating the value of integrated care management in population health initiatives.

Frequently Asked Questions on Care Management Systems

- How do Care Management Systems improve patient outcomes?

Care Management Systems improve patient outcomes by enabling continuous monitoring, timely interventions, and structured care plans. They support proactive decision-making, enhance patient engagement, and ensure that healthcare teams can collaborate effectively to deliver high-quality, coordinated care across different settings. - What features are commonly included in Care Management Systems?

Typical features include care planning tools, patient monitoring dashboards, risk stratification, communication modules, and analytics capabilities. These functionalities allow healthcare providers to track patient progress, identify potential complications, and deliver timely interventions that support better overall care outcomes. - Who uses Care Management Systems?

Care Management Systems are used by hospitals, clinics, payers, and long-term care organizations. These platforms assist physicians, nurses, care coordinators, and health administrators in improving workflow efficiency, reducing avoidable hospitalizations, and managing complex patient populations effectively. - What are the main benefits of implementing Care Management Systems?

The systems provide improved care coordination, reduced administrative burden, and enhanced patient satisfaction. Their analytical capabilities help providers identify risks earlier, reduce healthcare costs, and support the broader shift toward preventive, value-based care models in modern healthcare environments. - What is driving growth in the Care Management Systems market?

Market growth is driven by rising chronic disease prevalence, increasing demand for digital health tools, and expanding use of telehealth. Adoption of cloud-based platforms and advanced analytics further contributes to sustained demand from healthcare providers globally. - Which regions are leading the Care Management Systems market?

North America leads due to strong digital health infrastructure, high technology adoption, and supportive value-based care initiatives. Europe follows with growing investment in healthcare modernization, while Asia-Pacific is recording rapid expansion driven by government-led digital transformation programs. - What technological trends are shaping this market?

Artificial intelligence, machine learning, and predictive analytics are shaping market evolution. These technologies support personalized care, automate routine tasks, and enable real-time risk assessment, contributing to higher efficiency and improved clinical decision-making within healthcare systems.

Conclusion

The global Care Management Systems market is expected to maintain steady growth as healthcare organizations prioritize coordinated, data-driven, and patient-centered care delivery. The expansion of digital health infrastructure, rising chronic disease prevalence, and broader adoption of telehealth and analytics-driven platforms have strengthened system implementation across regions.

Supportive regulations, investment in advanced technologies, and the transition toward value-based care continue to reinforce market momentum. Although interoperability and data privacy challenges persist, ongoing modernization initiatives and increasing reliance on cloud-based solutions indicate a sustained trajectory, positioning care management technologies as essential components of future healthcare delivery models.