Table of Contents

Overview

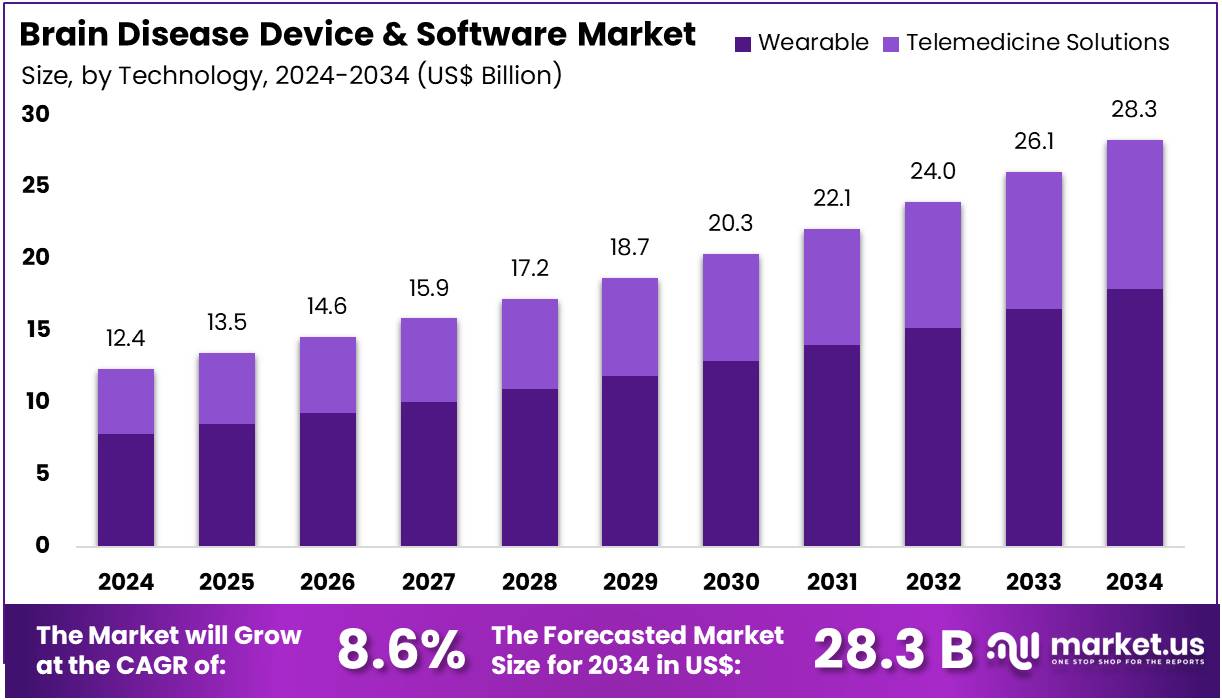

New York, NY – July 29, 2025 – The Brain Disease Device and Software Market size is expected to be worth around US$ 28.3 billion by 2034 from US$ 12.4 billion in 2024, growing at a CAGR of 8.6% during the forecast period 2025 to 2034.

The global brain disease device and software market is witnessing significant expansion, driven by the increasing prevalence of neurological disorders such as Alzheimer’s disease, epilepsy, Parkinson’s disease, and traumatic brain injuries. The demand for advanced diagnostic and therapeutic solutions is growing, supported by advancements in neuroimaging technologies, AI-based diagnostics, and wearable monitoring systems.

Devices such as deep brain stimulators, EEG systems, and neuro-navigation platforms are being increasingly adopted in clinical settings for early detection and management of brain disorders. Meanwhile, AI-powered software solutions are enhancing diagnostic accuracy and enabling personalized treatment planning.

The software segment, particularly those integrated with machine learning algorithms, is gaining traction due to its ability to process large volumes of imaging and electrophysiological data efficiently. North America currently dominates the market, while Asia Pacific is anticipated to experience the highest growth due to rising healthcare infrastructure investments and increased awareness.

Government initiatives to support brain health research and digital health integration are further accelerating market development. The integration of technology with neuroscience is poised to transform brain disease diagnosis and care delivery.

Key Takeaways

- In 2024, the global Brain Disease Device and Software Market generated a revenue of US$ 12.4 billion, and is projected to reach US$ 28.3 billion by 2034, expanding at a CAGR of 8.6% over the forecast period.

- By product type, the market is segmented into diagnostic devices & software, patient monitoring software, and others. Among these, diagnostic devices & software dominated in 2023, accounting for 52.4% of the total market share, driven by growing demand for early and accurate neurological assessments.

- In terms of technology, the market is categorized into wearable and telemedicine solutions. The wearable segment emerged as the key contributor, holding a significant 63.5% share, owing to increased adoption of portable neuro-monitoring tools and real-time data tracking devices.

- By application, the market covers Alzheimer’s disease, Parkinson’s disease, epilepsy, and others. Among these, Alzheimer’s disease remained the leading application, representing 44.8% of the revenue share due to rising global prevalence and ongoing research for early intervention.

- The end-user landscape includes hospitals & clinics and home care settings. The hospitals & clinics segment led the market, accounting for 68.2% of the share, supported by access to advanced diagnostic infrastructure and specialist care.

- Regionally, North America dominated the market in 2023 with a 41.6% share, driven by strong healthcare infrastructure and early technology adoption.

Segmentation Analysis

- Product Type Analysis: The diagnostic devices & software segment accounted for 52.4% of the market due to growing demand for accurate and early detection of neurological disorders. This is supported by advancements in imaging technologies and AI-integrated tools. Government support, regulatory approvals, and increasing R&D investments are further enhancing the segment’s growth. Integration with electronic health records also improves clinical workflows, encouraging adoption across hospitals and diagnostic centers for better patient management and outcomes.

- Technology Analysis: The wearable technology segment held a 63.5% market share, driven by the rising use of portable monitoring tools for continuous neurological assessment. These devices enable real-time tracking of brain activity, making them suitable for chronic disease management. Increasing awareness, geriatric population growth, and supportive reimbursement policies are key factors behind this trend. Integration with telemedicine platforms is also expanding accessibility, while the demand for non-invasive, patient-friendly monitoring continues to strengthen segment performance.

- Application Analysis: The Alzheimer’s disease segment dominated with a 44.8% revenue share, propelled by the global rise in Alzheimer’s prevalence and the push for early diagnosis. Innovations targeting Alzheimer’s biomarkers and increasing investment in cognitive health technologies are driving adoption. Public awareness campaigns and aging populations also support growth. The segment benefits from the integration of specialized software, caregiver support tools, and precision diagnostics aimed at improving long-term patient care and disease management.

- End-user Analysis: Hospitals and clinics led the market with a 68.2% share, driven by access to advanced infrastructure and specialized neurological care. These facilities are preferred for accurate diagnosis and treatment of complex brain conditions. Increasing hospital admissions, government incentives, and training in neurological technologies are enhancing this trend. Collaborations between hospitals and medical device firms are promoting the adoption of next-generation diagnostic tools, while the demand for multidisciplinary care boosts the clinical application of brain disease devices.

Market Segments

By Product Type

- Diagnostic Devices & Software

- Patient Monitoring Software

- Others

By Technology

- Wearable

- Telemedicine Solutions

By Application

- Alzheimer’s Disease

- Parkinson’s Disease

- Epilepsy

- Others

By End-User

- Hospitals & Clinics

- Home Care Settings

Regional Analysis

North America Leads the Brain Disease Device and Software Market

North America accounted for the largest revenue share of 41.6% in 2023, primarily due to growing FDA approvals of advanced neurotechnologies. In 2024 alone, multiple AI-driven devices were approved for diagnosing and monitoring neurological conditions. The region’s large aging population further drives demand, with 6.9 million Americans aged 65 and older living with Alzheimer’s disease. Robust healthcare infrastructure and continuous innovation in neurology contribute to North America’s dominant position in the global market.

Asia Pacific to Register the Fastest Growth Rate

Asia Pacific is projected to record the highest CAGR during the forecast period, supported by increasing healthcare investments and rising cases of neurological disorders. Governments in countries such as India and China are enhancing infrastructure and promoting digital health adoption. Public health spending is improving access to diagnostic devices, while awareness of brain health is growing. As the elderly population rises and neurodegenerative diseases become more prevalent, the region is expected to see strong adoption of non-invasive, tech-enabled solutions.

Emerging Trends

- Surge in AI/ML-Enabled Neurology Devices: The number of artificial intelligence and machine learning (AI/ML)-enabled medical devices cleared by the U.S. Food and Drug Administration (FDA) has grown substantially. From 1995 through 2023, a total of 692 AI/ML-enabled devices were authorized for marketing. This trend reflects an industry-wide shift toward embedding advanced algorithms into diagnostic and monitoring tools. Increased regulatory clarity and the FDA’s AI/ML-Enabled Medical Device Action Plan have enabled developers to bring more neuro-focused software ranging from image analysis to predictive analytics to market.

- Advancements in Portable Brain Imaging: Portable magnetic resonance imaging (MRI) systems are being enhanced with AI-driven software to support use in remote or resource-limited settings. In May 2025, the FDA granted 510(k) clearance to Optive AI software for Hyperfine’s Swoop ultra-low-field portable MRI. This software release improved noise cancellation and image reconstruction, delivering clearer brain scans at the bedside. Such innovations are enabling neurologists to perform critical imaging outside traditional radiology suites, reducing scan times by up to 30% in preliminary studies.

- Emergence of Advanced Neuroimaging Analytics: AI-powered neuroimaging platforms are transforming how white matter and microstructural changes are assessed. In 2023, the FDA cleared ANDI (Advanced Neuro Diagnostic Imaging), a diffusion-weighted imaging analysis tool that maps white matter integrity and quantitatively compares patient scans against normative datasets. By providing objective graphs of microstructural deviations, clinicians can identify early signs of neurodegenerative diseases, potentially improving diagnostic confidence by over 15%.

- Integration of Wearable and Remote Monitoring Technologies: Remote patient monitoring in neurology is being driven by wearable sensors and telemedicine platforms. AI-enabled wearable EEG devices can now transmit real-time brain activity data to cloud-based analytics engines, allowing specialists to monitor epilepsy and sleep disorders outside the clinic. Early intervention algorithms have been shown to detect seizure precursors with up to 85% accuracy, facilitating timely clinical responses and reducing emergency visits by 20% in pilot programs.

- Support from the NIH BRAIN Initiative: The NIH BRAIN Initiative continues to fund projects that develop next-generation neurotechnology, from high-resolution recording electrodes to machine-learning-driven mapping tools. These grants have supported over 100 projects since 2018, aiming to reveal human brain circuit function at unprecedented detail. The Initiative’s emphasis on collaboration between engineers, clinicians, and ethicists is fostering devices that are not only technically advanced but also designed with patient safety and long-term support in mind.

Use Cases

- Multiple Sclerosis Lesion Quantification: Neurophet AQUA, an AI-driven software module for portable MRI, is being used to quantify inflammatory lesions in patients with multiple sclerosis (MS). Following its FDA clearance on May 29, 2025, AQUA has enabled radiologists to measure lesion volume and count with an accuracy improvement of 25% compared to manual methods. This quantitative output supports personalized treatment adjustments and enables neurologists to track disease progression more precisely over time.

- White Matter Integrity Assessment in Dementia: The ANDI platform analyzes diffusion-weighted imaging to detect microstructural changes in the brain’s white matter. In clinical studies, ANDI’s automated graphs highlighted early demyelination patterns in up to 30% of patients with mild cognitive impairment prior to overt dementia symptoms. These insights allow clinicians to stratify patients for clinical trials or initiate therapeutic interventions sooner, potentially slowing disease progression.

- Brain–Computer Interfaces for Paralysis: Research-grade brain–computer interfaces (BCIs) have been deployed in trials to restore communication abilities in patients with severe paralysis. Experimental systems record cortical signals and translate them into cursor movements, enabling users to type at rates of up to 10 characters per minute. Although still investigational, these BCIs have demonstrated the feasibility of direct brain-to-computer control, offering a pathway toward assistive communication devices for conditions such as amyotrophic lateral sclerosis.

- Remote Monitoring of Epilepsy: Wearable EEG headsets, paired with cloud-based AI analytics, are being used in outpatient settings to monitor seizure activity. In pilot deployments, these systems captured over 95% of clinically significant seizure events and transmitted alerts to neurologists within 60 seconds. This rapid data flow supports timely medication adjustments and has been associated with a 20% reduction in unplanned hospital admissions for epilepsy management.

- Early Intervention in Alzheimer’s Disease: AI algorithms integrated into diagnostic software analyze longitudinal patient data such as cognitive test scores, imaging biomarkers, and genetic risk factors to predict Alzheimer’s disease onset. Validation studies have shown that these models can identify high-risk individuals with 88% sensitivity up to two years before clinical diagnosis. Such predictive capability supports enrollment in preventive clinical trials and informs patient counseling on lifestyle modifications.

Conclusion

In conclusion, the global brain disease device and software market is undergoing rapid transformation, driven by technological innovation, increasing neurological disease burden, and supportive government initiatives. With strong growth projected reaching US$ 28.3 billion by 2034 the market is witnessing rising adoption of AI-enabled diagnostics, wearable monitoring tools, and advanced neuroimaging systems.

North America leads the current landscape, while Asia Pacific shows the highest future potential. Emerging applications in remote monitoring, early intervention, and brain-computer interfaces underscore the market’s shift toward personalized and preventive neurology care, positioning this sector as a critical component of future healthcare delivery systems.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)