Table of Contents

Overview

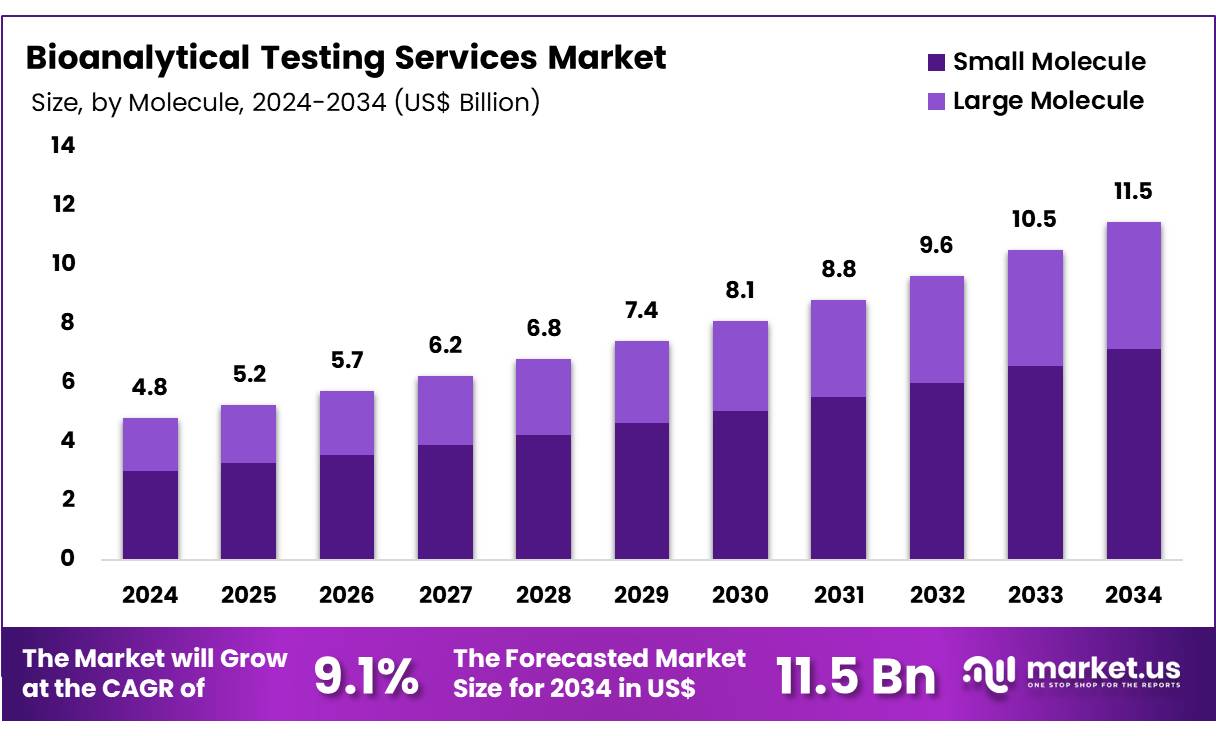

New York, NY – Nov 13, 2025 – Global Bioanalytical Testing Services Market size is expected to be worth around US$ 11.5 Billion by 2034 from US$ 4.8 Billion in 2024, growing at a CAGR of 9.1% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 39.6% share with a revenue of US$ 1.9 Billion.

The global bioanalytical testing services market has been witnessing steady expansion as the demand for high-precision analytical solutions continues to rise across pharmaceutical, biotechnology, and clinical research sectors. Growth in this market has been driven by increasing drug development activities, a rising volume of biologics and biosimilars, and the expansion of regulated laboratory environments. The adoption of advanced analytical platforms has been accelerating, ensuring higher accuracy, sensitivity, and compliance with international regulatory standards.

Bioanalytical testing services have been utilized extensively for the quantitative and qualitative assessment of drugs, metabolites, and biomarkers. These services support critical phases of preclinical and clinical development, including pharmacokinetics, pharmacodynamics, immunogenicity, and bioequivalence studies. The shifting focus toward complex molecules and personalized therapies has increased the need for specialized testing methodologies, strengthening the role of contract research organizations in delivering standardized and cost-effective solutions.

The advancement of chromatography, mass spectrometry, ligand-binding assays, and cell-based assays has enabled service providers to handle a broader spectrum of sample types and therapeutic categories. The growth of outsourcing trends among pharmaceutical companies can be attributed to the rising operational burden and the need for regulatory-compliant data generation. In addition, strict guidelines issued by authorities such as the FDA and EMA have reinforced the requirement for validated, high-accuracy testing environments.

Key Takeaways

- In 2024, the bioanalytical testing services market generated a revenue of US$ 4.8 billion, and the market has been expanding at a CAGR of 9.1%. Based on this trajectory, the market value is expected to reach US$ 11.5 billion by 2033.

- The market has been categorized by molecule type into small molecules and large molecules. The small molecule category remained the leading segment in 2023, accounting for 62.4% of the overall market share.

- Based on test type, the industry has been segmented into ADME, pharmacokinetics, pharmacodynamics, bioavailability, bioequivalence, and other test services. Among these, bioavailability testing held a notable position, representing 34.8% of the total share.

- In terms of workflow, the market has been divided into sample preparation, sample analysis, and other workflow-related processes. The sample analysis segment dominated the market landscape and contributed 49.2% to total revenue.

- The application segment includes oncology, neurology, infectious diseases, gastroenterology, cardiology, and other therapeutic areas. Oncology emerged as the primary application area, capturing 38.6% of the market.

- Regarding end users, the market comprises pharma and biotechnology companies, contract development and manufacturing organizations (CDMOs), and contract research organizations (CROs). Pharma and biotechnology companies held the leading share at 54.7%.

- Regionally, North America continued to dominate the global landscape, securing 39.6% of the market in 2023.

Regional Analysis

North America remains the leading regional market for bioanalytical testing services

North America maintained its dominant position by securing 39.6% of total revenue, driven by strong demand for advanced analytical capabilities across pharmaceuticals, biotechnology, and environmental sciences. The acquisition of Alpha Analytical by Pace Analytical Services in April 2023 strengthened its presence in the Northeastern United States, expanding testing capacity across 39 locations and supporting environmental and life sciences applications. The rising number of clinical trials and drug development initiatives increased the requirement for high-quality bioanalytical testing, ensuring adherence to stringent regulatory guidelines.

Continued advances in biologics, biosimilars, and gene therapies further supported the need for specialized and sensitive analytical approaches. The integration of automation and AI-enabled data processing enhanced operational efficiency and improved accuracy in bioanalytical workflows. In addition, increasing government-backed research programs and rising pharmaceutical investments contributed to sustained market expansion. The growing emphasis on contamination detection and quality control in the food and beverage sector strengthened the adoption of bioanalytical testing services across the region.

Asia Pacific is projected to register the fastest CAGR during the forecast period

Asia Pacific is expected to experience the highest growth rate due to expanding pharmaceutical manufacturing activities and rising regulatory compliance requirements. The establishment of SGS’s advanced testing facility in Pudong, Shanghai, in February 2023 demonstrated the region’s increasing focus on quality assurance and regulatory testing. Growing investment in drug discovery and clinical research is anticipated to drive the adoption of sophisticated analytical technologies.

Government efforts to promote biosimilar development and biologics production are expected to further support market expansion. Strategic collaborations between global CROs and regional biotechnology companies are improving access to cost-effective and high-quality testing services. Additionally, the adoption of digital laboratory systems and AI-supported data analysis is projected to enhance testing accuracy and efficiency. The rapid advancement of personalized medicine and cell-based therapies is likely to generate new opportunities, positioning Asia Pacific as a key center for innovation in bioanalytical testing.

Emerging Trends

- Harmonisation of Global Guidelines: A unified framework for bioanalytical method validation has been established through the ICH M10 guideline, which was adopted by the FDA in June 2024 and endorsed by WHO soon after. The guideline consolidates requirements that were previously presented in separate FDA and EMA documents. As a result, validation practices have become more consistent across major regulatory regions.

- Increased Automation and Data Digitalisation: High-throughput platforms and advanced analytical tools are being adopted to manage and interpret growing volumes of bioanalytical data. According to the FDA’s Office of Data, Analytics, and Research (ODAR), automated sample-handling systems and digital workflows are increasingly implemented to enhance throughput, precision, and reproducibility in method development and routine sample analysis.

- Rising Demand from Biologics and Advanced Therapies: The expansion of biologics, gene therapies, and personalized medicines has increased demand for complex bioanalytical assays. In support of the repotrectinib NDA, validated LC-MS/MS methods were used to quantify drug concentrations in 47 of 48 TKI-pretreated patients. This illustrates the essential role of bioanalysis in evaluating advanced therapeutic modalities.

- Strengthened Emphasis on Data Integrity: Regulatory agencies have intensified oversight of data quality in regulatory submissions. The FDA’s guidance on data-integrity assurance requires robust quality-management systems and standardized procedures to prevent errors, omissions, or manipulation within bioanalytical datasets.

Use Cases

- Clinical Pharmacokinetics: Quantitative assays are routinely employed to determine drug concentrations in human plasma and support dose-selection strategies. A recent FDA review cited the use of LC-MS/MS to analyze samples from 47 out of 48 patients, generating critical exposure data needed for regulatory decision-making.

- Comparative Bioavailability/Bioequivalence Studies: Validated bioanalytical methods are fundamental in BA/BE studies to compare plasma profiles of generic and reference formulations. WHO guidelines specify that a minimum of 100 study samples must be analyzed for each assay, with an additional 5 percent of samples subjected to incurred sample reanalysis to verify reproducibility.

- Forensic Toxicology and Public Health: External proficiency testing programs have been implemented to assess laboratory performance in detecting synthetic opioids. The CDC’s pilot initiative conducted two assessment events per year over a two-year period—four events in total evaluating analytical accuracy across urine, plasma, and whole-blood matrices to ensure dependable toxicology results.

Frequently Asked Questions on Bioanalytical Testing Services

- What are bioanalytical testing services?

Bioanalytical testing services involve the scientific measurement of drugs, metabolites, and biological molecules in biological samples. These services support drug development, ensuring regulatory compliance and providing validated analytical data required for preclinical and clinical studies across various therapeutic areas. - Why are bioanalytical testing services important in drug development?

These services are essential because accurate measurement of drug concentrations determines safety, pharmacokinetics, and efficacy. The data generated supports regulatory submissions, enabling informed decisions during early discovery, clinical trials, and post-approval surveillance while ensuring strict adherence to global quality standards. - Which analytical methods are commonly used in bioanalytical testing?

Common methods include LC-MS/MS, HPLC, immunoassays, ligand-binding assays, and hybrid techniques. These platforms provide high sensitivity and specificity, enabling reliable detection of small molecules, biologics, biomarkers, and biosimilars throughout development stages. - What industries primarily use bioanalytical testing services?

Pharmaceutical companies, biotechnology firms, contract research organizations, and academic research institutions rely on these services. The demand arises from expanding drug pipelines, complex biologics, and increasing regulatory requirements for validated analytical data supporting product safety and clinical performance. - What factors are driving growth in the bioanalytical testing services market?

Market growth is driven by expanding clinical trial volumes, rising biologics development, and increasing outsourcing trends. Strong regulatory pressures, demand for specialized analytical techniques, and the need for cost-efficient development further contribute to consistent global market expansion. - Which segments dominate the bioanalytical testing services market?

Services related to small-molecule testing, biologics analysis, pharmacokinetics, and biomarker studies dominate the market. The biologics segment shows strong expansion due to increasing monoclonal antibody pipelines and greater reliance on complex assays requiring specialized laboratory expertise. - Which regions are leading the bioanalytical testing services market?

North America leads due to strong pharmaceutical R&D spending, established CRO networks, and advanced analytical infrastructure. Europe follows closely, while Asia-Pacific demonstrates robust growth driven by outsourcing demand and expanding biopharmaceutical manufacturing capabilities.

Conclusion

The global bioanalytical testing services market is expected to demonstrate sustained growth as demand for high-precision analytical capabilities continues to rise across pharmaceuticals and biotechnology. Market expansion has been supported by increasing biologics development, stringent regulatory expectations, and advancements in analytical technologies.

Growing adoption of outsourcing strategies and the emergence of harmonized validation guidelines have reinforced service quality and operational efficiency. North America maintains leadership, while Asia Pacific is poised for rapid advancement due to expanding manufacturing and clinical research activity. Overall, consistent R&D investment and innovation in complex therapeutics are expected to drive long-term market progression.