Table of Contents

Overview

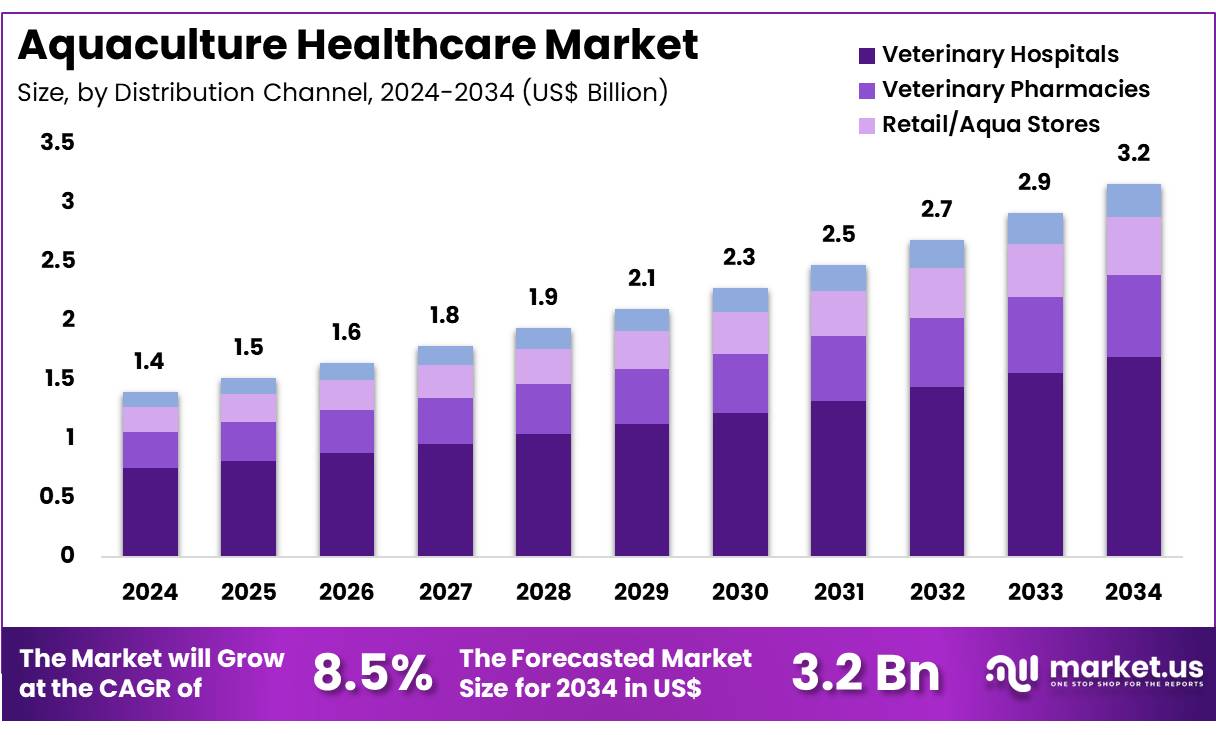

New York, NY – Nov 27, 2025 – Global Aquaculture Healthcare Market size is expected to be worth around US$ 3.2 billion by 2034 from US$ 1.4 billion in 2024, growing at a CAGR of 8.5% during the forecast period 2025 to 2034. In 2024, Asia Pacific led the market, achieving over 36.9% share with a revenue of US$ 0.5 billion.

The global aquaculture healthcare market is witnessing steady expansion as aquatic production systems continue to scale worldwide. The growth of the sector is being driven by increasing seafood consumption, higher awareness of aquatic animal health, and the adoption of preventive health solutions across farming operations. A shift toward sustainable and biosecure aquaculture practices has been observed, supporting the demand for vaccines, therapeutics, diagnostics, and advanced farm management tools.

The prevalence of bacterial, viral, and parasitic diseases in farmed species has resulted in a stronger focus on health management. As a result, investments in research and development have intensified, enabling the introduction of innovative vaccines and environmentally responsible treatment solutions. The market value is projected to rise consistently over the next decade, supported by the expansion of intensive farming systems and the modernization of aquaculture infrastructure in emerging economies.

Regulatory frameworks are being strengthened across key producing nations, promoting responsible antimicrobial use and improved surveillance. This regulatory direction has created favorable conditions for biologics and non-antibiotic alternatives. Furthermore, the integration of digital tools, including real-time water monitoring and data-driven health assessment platforms, has enhanced disease prevention and early-detection capabilities.

Strategic partnerships between pharmaceutical companies, biotechnology firms, and aquaculture producers have contributed to product innovation and wider accessibility of healthcare solutions. The growth of sustainable aquaculture has been recognized as a critical component of global food security, and the aquaculture healthcare market is expected to play a central role in supporting healthy, high-quality aquatic production.

Key Takeaways

- In 2024, the aquaculture healthcare market generated revenue of US$ 1.4 billion, recorded a CAGR of 8.5%, and is projected to reach US$ 3.2 billion by 2033.

- The product type segment comprises vaccines, antibiotics, antifungals, anti-viral drugs, and others, with vaccines leading the market in 2024, accounting for 55.5% of total share.

- Based on species, the market includes fishes, crustaceans, and others, with fishes representing 63.8% of the overall market share.

- In terms of route of administration, the market is categorized into topical, spray, parenteral, oral, and immersion, where the topical segment dominated, contributing 47.2% of revenue.

- The distribution channel segment covers veterinary hospitals, veterinary pharmacies, retail/aqua stores, and online pharmacies, with veterinary hospitals holding the largest share at 53.5%.

- By infection type, the market is segmented into bacterial, viral, parasitic, and fungal infections, with bacterial infections accounting for 56.3% of the share.

- The Asia Pacific region emerged as the leading regional market, securing 36.9% of the total share in 2024.

Regional Analysis

Asia Pacific Remains the Leading Region in the Aquaculture Healthcare Market

Asia Pacific maintained its position as the dominant regional market, accounting for 36.9% of total revenue. According to 2022 data from the Network of Aquaculture Centres in Asia-Pacific (NACA), the region contributes more than 90% of global aquaculture production by volume. This extensive scale of aquaculture activity across major producing countries—such as China, India, Indonesia, Vietnam, and Bangladesh—creates consistent demand for a broad portfolio of aquaculture healthcare solutions, including vaccines, antibiotics, and water treatment products.

A sustained focus on food security, coupled with ongoing investments in expanding and modernizing aquaculture facilities, is strengthening the region’s market position. Rising awareness of the financial impact associated with disease outbreaks has encouraged the adoption of preventive healthcare measures among farmers. Additionally, the wide presence of aquaculture farms and the increasing availability of veterinary services and specialized aquaculture health professionals support the region’s continued leadership.

North America Expected to Record the Fastest Growth Rate

North America is projected to exhibit the highest CAGR during the forecast period. Although the region’s production volume is comparatively smaller than that of Asia Pacific, the aquaculture sector in the United States and Canada emphasizes high-value species, including salmon, shrimp, and trout. Data published in 2023 by the US Department of Commerce’s National Marine Fisheries Service (NMFS) reported a steady increase in the value of US aquaculture output.

The region’s strong regulatory focus on sustainability, health management, and biosecurity drives demand for advanced aquaculture healthcare products. Well-developed veterinary infrastructure, along with a proactive approach to disease prevention, supports market expansion. Moreover, growing consumer interest in sustainably sourced seafood continues to reinforce the adoption of comprehensive healthcare practices across North American aquaculture operations.

Emerging Trends

- Rise of Biosecurity and Disease Control Protocols: Biosecurity has gained prominence as disease outbreaks remain a major constraint to sustainable aquaculture. The FAO emphasizes that transboundary aquatic diseases impose significant socio-economic and biodiversity impacts, encouraging countries to adopt standardized disease-control systems across farming operations.

- Shift Toward Sustainable and Alternative Feeds: Rising production needs estimated by the FAO to require a 35–40% increase by 2030—are driving the development of alternative feed resources. Plant-based proteins, microbial meals, and other substitutes are being explored to reduce fishmeal dependence and lower antibiotic usage.

- Digital Innovation for Real-Time Monitoring: The adoption of smart aquaculture systems is increasing, supported by government initiatives promoting sensor-based monitoring tools. FAO highlights progress in technologies such as water-quality sensors and automated decision-support systems that enable early detection of stressors and enhance disease-management efficiency.

- Growth of Integrated Multi-Trophic Aquaculture (IMTA): NOAA-led IMTA demonstration projects show the benefits of multispecies production systems that incorporate fish, shellfish, and seaweeds. These systems integrate disease-control and containment measures to maintain animal health while supporting environmentally balanced, high-density aquaculture.

Use Cases

- Fish Vaccination Programs: Vaccination programs have expanded globally, with vaccines now available for over 17 fish species against more than 22 bacterial and 6 viral infections. Adoption across more than 40 countries has contributed to reduced mortality and decreased antibiotic dependency in aquaculture.

- Antibiotic Reduction in Trout Farming: Targeted health-management improvements in Scotland’s trout sector have led to an estimated 69% reduction in antibiotic use between 2017 and 2021. This demonstrates how refined husbandry practices and responsible medicine use can support productivity while limiting antimicrobial reliance.

Frequently Asked Questions on Aquaculture Healthcare

- Why is aquaculture healthcare important?

Aquaculture healthcare is essential because disease outbreaks can significantly reduce yield and profitability. Effective health management improves survival rates, ensures product quality, and supports sustainable farming practices, which are critical as global demand for aquaculture products continues to rise. - What types of products are used in aquaculture healthcare?

Aquaculture healthcare relies on vaccines, antibiotics, antifungals, antivirals, probiotics, and water treatment solutions. These products help control infections, improve immunity, and maintain optimal water conditions, thereby ensuring healthier and more productive aquaculture systems. - Which species benefit the most from aquaculture healthcare solutions?

Fishes, crustaceans, and mollusks benefit significantly from aquaculture healthcare solutions. Fishes dominate due to their large-scale production, making disease control essential to maintaining farm output and ensuring sustainable growth across aquaculture operations. - What are the common diseases in aquaculture?

Common aquaculture diseases include bacterial, viral, parasitic, and fungal infections. These diseases can rapidly spread in dense farming environments, making early detection and preventive health strategies essential for minimizing mortality and maintaining production stability. - What is driving the growth of the aquaculture healthcare market?

Market growth is being driven by rising global seafood consumption, expanding aquaculture production, and increasing awareness of disease management. Investments in modern farming systems and improved veterinary services are further supporting demand for advanced healthcare solutions. - Which product type dominates the aquaculture healthcare market?

Vaccines dominate the product segment, capturing 55.5% of the market share in 2024. Their effectiveness in preventing major diseases and reducing antibiotic dependence has encouraged widespread adoption across various aquaculture species. - Which region leads the aquaculture healthcare market?

Asia Pacific leads with a 36.9% revenue share in 2024 due to its vast aquaculture production capacity. The region’s strong focus on food security, disease prevention, and infrastructure development supports sustained demand for healthcare products. - What factors are influencing future market trends?

Future trends are being shaped by increasing adoption of sustainable practices, stricter biosecurity regulations, advancements in vaccine development, and rising use of digital monitoring technologies. These factors are expected to drive long-term demand for comprehensive aquaculture healthcare solutions.

Conclusion

The aquaculture healthcare market is positioned for sustained expansion as global aquaculture production continues to rise and disease-management requirements become more critical. Increasing reliance on preventive healthcare, strengthened regulatory frameworks, and advancements in vaccines and digital monitoring systems are supporting market growth across regions.

Asia Pacific maintains clear leadership due to its large-scale production, while North America is set to record strong growth driven by high-value species and stringent biosecurity practices. Emerging innovations such as IMTA systems, sustainable feeds, and smart monitoring technologies further reinforce the sector’s evolution. Overall, aquaculture healthcare will remain essential for ensuring resilient, safe, and sustainable aquatic production worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)