Table of Contents

Overview

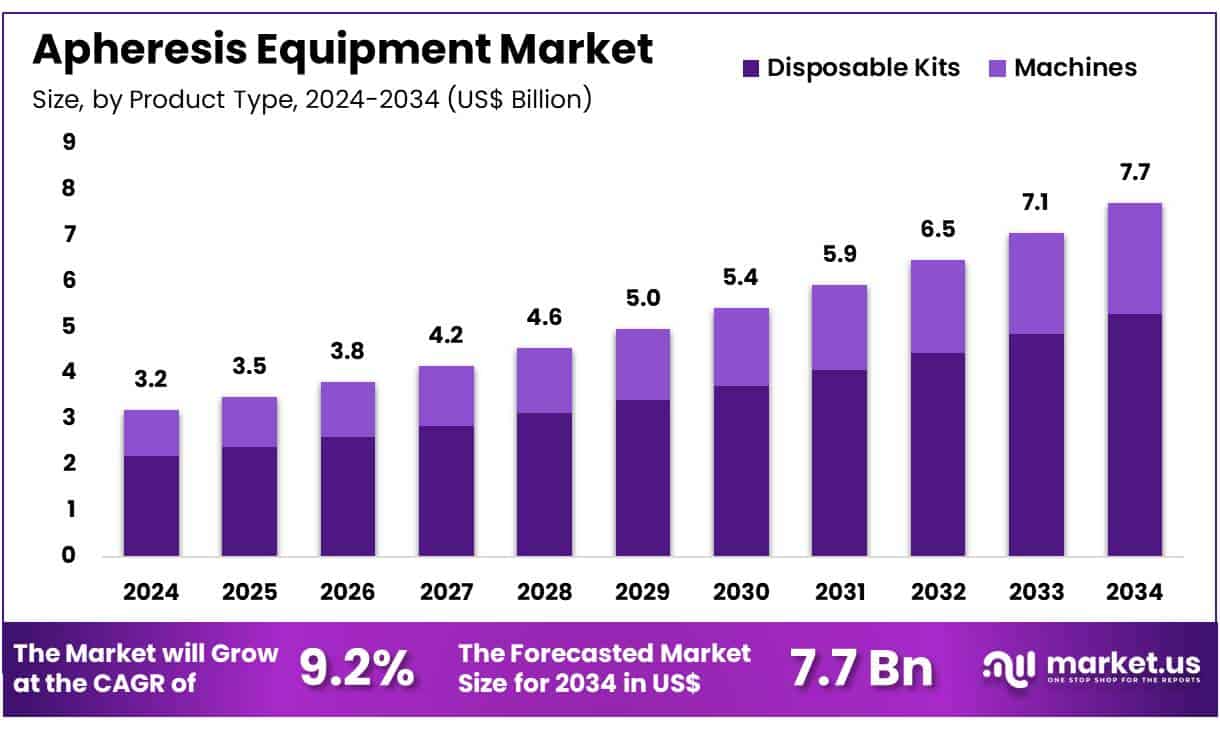

New York, NY – June 13, 2025 – Global Apheresis Equipment Market size is expected to be worth around US$ 7.7 Billion by 2034 from US$ 3.2 Billion in 2024, growing at a CAGR of 9.2% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 38.7% share with a revenue of US$ 1.2 Billion.

The global apheresis equipment market is experiencing significant expansion, driven by rising cases of chronic diseases, increasing demand for blood components, and technological innovations in therapeutic apheresis procedures. Apheresis used to separate blood components for treatment or donation is critical in managing conditions like leukemia, multiple sclerosis, and autoimmune disorders.

According to data from the World Health Organization (WHO), global blood demand continues to rise, with over 118 million blood donations collected worldwide annually. The increasing use of plasma-derived therapies, along with growth in platelet and leukocyte collection procedures, is boosting the adoption of apheresis systems in hospitals and blood centers.

Technological advancements such as automated, closed-loop apheresis machines with real-time monitoring are enhancing procedural efficiency and patient safety. Governments in regions like North America, Europe, and parts of Asia-Pacific are expanding their healthcare infrastructure to support these therapies. In the U.S., the FDA supports therapeutic apheresis through approved indications for diseases such as Guillain-Barré syndrome and thrombotic thrombocytopenic purpura (TTP).

With rising global healthcare expenditure and strategic collaborations between medical device companies and healthcare providers, the apheresis equipment market is set to witness robust growth in the coming years. Emerging economies are expected to play a vital role as awareness and accessibility of advanced blood treatment technologies increase.

Key Takeaways

- In 2023, the global apheresis equipment market generated revenue of approximately US$ 3.2 billion and is projected to reach US$ 7.7 billion by 2033, growing at a CAGR of 9.2%.

- By product type, disposable kits dominated the market in 2023, capturing a significant share of 68.7% due to high usage frequency and one-time application benefits.

- Based on technology, membrane filtration led the segment with a commanding 75.4% market share, driven by its precision and efficiency in selective component separation.

- In terms of application, neurological disorders emerged as the leading segment, accounting for 56.5% of the total market share in 2023, owing to increasing use in conditions like multiple sclerosis and Guillain-Barré syndrome.

- Among procedures, plasmapheresis held the highest revenue share at 66.3%, supported by its widespread use in autoimmune and hematological treatments.

- Regarding end-users, hospitals and clinics were the primary consumers, representing 72.1% of the market in 2023 due to their advanced infrastructure and procedural volume.

- Regionally, North America dominated the global market with a share of 38.7%, attributed to high healthcare spending, technological advancement, and strong regulatory support.

Segmentation Analysis

- Product Type Analysis: In 2023, disposable kits dominated the product segment with a 68.7% market share. Their growing popularity is attributed to increased demand for single-use, cost-effective medical tools that reduce infection risks. These kits eliminate the need for complex sterilization, offering convenience and safety. The rising adoption of apheresis procedures in hospitals and outpatient clinics, alongside innovations in disposable kit technology, is expected to sustain the segment’s growth throughout the forecast period.

- Technology Analysis: Membrane filtration led the technology segment in 2023, accounting for a 75.4% market share. This method is favored for its precision, high-volume processing capability, and improved component recovery. It plays a crucial role in treating renal and neurological disorders. As healthcare providers seek efficient therapeutic solutions, membrane filtration is increasingly integrated into apheresis systems. Its reliability and clinical effectiveness are expected to support the segment’s dominance in future apheresis equipment advancements.

- Application Analysis: The neurological disorders segment held the largest application share at 56.5% in 2023. Apheresis treatments like plasmapheresis are widely adopted for conditions such as multiple sclerosis and Guillain-Barré syndrome. The rising incidence of autoimmune neurological diseases and increasing clinical confidence in apheresis therapies are major contributors to this growth. As the medical field explores innovative ways to manage complex neurological conditions, the demand for apheresis equipment in this application area is projected to rise steadily.

- Procedure Analysis: In 2023, plasmapheresis accounted for 66.3% of the procedure segment revenue. Its effectiveness in removing harmful antibodies in autoimmune, hematological, and neurological disorders underpins its widespread use. Growing awareness of its clinical benefits, combined with continuous advancements in filtration systems, supports segment expansion. As therapeutic strategies evolve, plasmapheresis is expected to remain central to treatment protocols, reinforcing its role as a key driver of demand in the apheresis equipment market.

- End-user Analysis: Hospitals and clinics were the leading end-users in 2023, holding a 72.1% share. These facilities remain the core setting for apheresis treatments due to their infrastructure and broad patient base. The growing burden of chronic illnesses like kidney disease and blood disorders is increasing the need for specialized procedures. As hospitals aim to enhance clinical efficiency and patient outcomes, demand for advanced apheresis equipment in these settings is expected to remain strong over the coming years.

Market Segments

Product Type

- Disposable Kits

- Machines

Technology

- Centrifugation

- Membrane Filtration

Application

- Neurological Disorders

- Renal Disorders

- Hematological Disorders

- Others

Procedure

- Plasmapheresis

- Photopheresis

- LDL Apheresis

- Leukapheresis

- Others

End-user

- Hospitals & Clinics

- Blood Donation Centers

- Ambulatory Surgical Centers

- Others

Regional Analysis

North America Leads the Apheresis Equipment Market

In 2023, North America held the largest revenue share of 38.7% in the global apheresis equipment market. This dominance can be attributed to the high prevalence of chronic and autoimmune diseases, which has driven the demand for therapeutic apheresis procedures across the region. Technological advancements in equipment have further enhanced procedural accuracy and safety, supporting increased adoption in clinical settings.

The aging population in North America, particularly in the United States and Canada, is more prone to conditions requiring apheresis, such as neurological and hematological disorders. Government initiatives, including support from the Centers for Medicare & Medicaid Services (CMS), have improved healthcare accessibility and incentivized the adoption of advanced medical technologies. Additionally, the presence of leading industry players such as Terumo BCT Inc., Fresenius SE & Co. KGaA, and Haemonetics Corporation has bolstered market growth through innovation and regional expansion strategies.

Asia Pacific Poised for Fastest Growth During the Forecast Period

The Asia Pacific region is projected to witness the highest compound annual growth rate (CAGR) in the apheresis equipment market over the forecast period. This growth is driven by rising incidences of hematological conditions, growing awareness of blood component therapy, and expanding access to specialized treatments.

Technological improvements in apheresis systems are enhancing procedural efficiency and making treatments more accessible across emerging healthcare markets. Government-backed initiatives such as India’s efforts to strengthen healthcare infrastructure and promote advanced therapeutic technologies are also facilitating market expansion. Key industry players, including Terumo BCT Inc., Haemonetics Corporation, and Fresenius SE & Co. KGaA, are actively investing in the region by introducing products tailored to regional clinical needs. These collective factors are expected to propel significant growth in Asia Pacific’s apheresis equipment market in the coming years.

Emerging Trends

- Rising Plateletpheresis Usage: The use of automated plateletpheresis has continued to grow. In 2019, 2 359 000 units of apheresis-collected platelets were distributed in the United States, marking a 0.9 % increase from 2017 levels. This trend reflects broader adoption of machine-based collection to ensure higher platelet purity and reduced donor exposure.

- Automation in Red Blood Cell Collection: Automated apheresis for red blood cells (RBCs) has become more prevalent. During 2021, 10 764 000 units of whole blood-derived and apheresis RBCs were transfused in U.S. hospitals. FDA guidance issued in January 2025 has further streamlined recommendations for collecting single and double RBC units with automated separators.

- Adoption of Pathogen Reduction Technologies: Safety-enhancing pathogen reduction methods are being applied to apheresis platelets. By 2019, 175 017 pathogen-reduced apheresis platelet units had been transfused (95 % CI, 115 346–234 544). Although these units cost roughly US$ 100 more per unit than standard leukoreduced platelets, their use is increasing to minimize transfusion-transmitted risks.

Use Cases

- Plateletpheresis for Thrombocytopenia: Automated platelet collection is widely used to treat patients with low platelet counts (thrombocytopenia). In 2019, 2 359 000 units of apheresis platelets were supplied for transfusion, ensuring targeted therapy and reduced donor exposures.

- Red Blood Cell Apheresis for Transfusion Support: Apheresis machines are employed to collect single or double RBC units for patients with severe anemia or acute blood loss. In 2021, 10 764 000 RBC units—including both whole blood-derived and apheresis collections—were transfused in U.S. healthcare settings.

- Pathogen-Reduced Platelet Transfusions: To enhance transfusion safety, pathogen reduction devices are integrated with apheresis equipment. By 2019, 175 017 pathogen-reduced apheresis platelet units had been used, representing a growing commitment to lowering transfusion-transmitted infections.

Conclusion

The global apheresis equipment market is poised for robust growth, driven by rising chronic disease prevalence, increased demand for blood components, and advancements in filtration technologies. With North America leading the market and Asia Pacific projected to grow rapidly, the sector is benefiting from improved healthcare infrastructure, supportive government initiatives, and innovation by key players.

The growing adoption of procedures like plasmapheresis and plateletpheresis, along with emerging trends in automation and pathogen reduction, reflects the evolving therapeutic landscape. As clinical awareness increases, apheresis equipment is expected to play a vital role in modern, safe, and efficient blood management practices worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)