Table of Contents

Overview

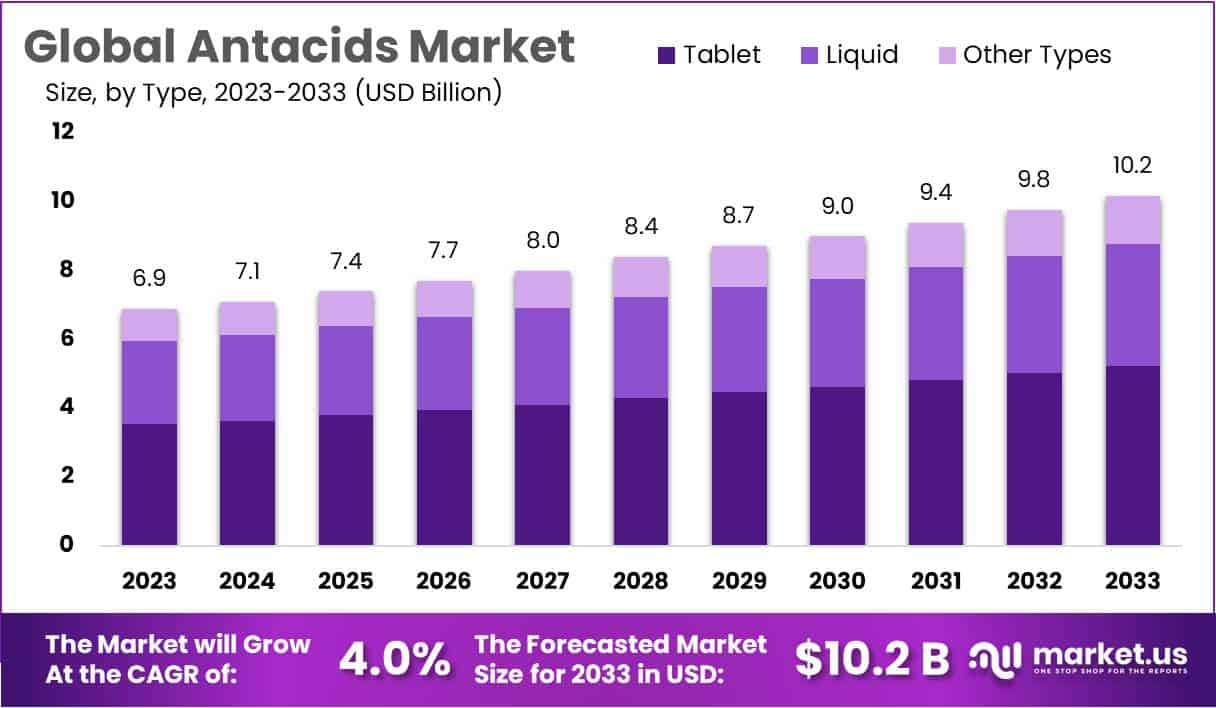

The Global Antacids Market is projected to reach USD 10.2 billion by 2033, rising from USD 6.9 billion in 2023. Growth is driven by increasing gastrointestinal disorders across diverse age groups and regions. Higher cases of gastroesophageal reflux disease, acidity, and indigestion have been widely reported. These conditions are linked to diet, stress, and lifestyle transitions. As a result, demand for fast-acting and easily accessible treatment options has increased, strengthening market expansion during the forecast period.

Lifestyle patterns have shifted significantly due to urbanization and rising consumption of processed foods, caffeinated drinks, and high-fat meals. These habits have elevated the prevalence of acid-related discomfort, increasing the need for over-the-counter relief. The expansion of the market can be attributed to the growing preference for convenient treatment solutions that fit into busy daily routines. Continuous reliance on quick symptom management is expected to sustain market growth.

The rising global geriatric population has created a structural source of demand. Age-related physiological changes often lead to frequent digestive issues, which increases reliance on antacid formulations. A noticeable rise in elderly populations in regions such as North America, Europe, and Asia Pacific has reinforced long-term consumption patterns. The demographic shift is supporting stable product uptake, resulting in consistent market traction across mature and emerging economies.

Self-medication trends have strengthened product penetration across pharmacy, supermarket, and online channels. Consumers prefer accessible OTC products for mild and moderate symptoms, reducing dependence on clinical consultation. Growing online retail activity has improved product visibility and availability. Subscription models, promotional pricing, and rapid delivery have enhanced consumer engagement. These factors have supported higher purchasing frequency and broadened market reach, particularly in price-sensitive regions.

Innovation has played an important role in widening adoption. Reformulated products, including flavored chewable tablets, sugar-free variants, and combination therapies, have improved user experience and compliance. Liquid antacids offering faster relief and better taste have improved acceptance among younger and older consumers. Favorable regulatory support permitting OTC sales of multiple formulations has reduced access barriers. As distribution networks expand, product availability and convenience are expected to strengthen overall market performance.

Key Takeaways

- The global antacids market was valued at USD 6.9 billion in 2023, expanding at a 4.0% CAGR toward USD 10.2 billion by 2033.

- The product landscape was characterized by tablets, liquids, and other formats, with tablets capturing 51.3% share and establishing dominance across the market in 2023.

- The end-use structure showed retail pharmacies holding 41.5% revenue share, reinforcing their position as the primary distribution channel within the antacids market.

- Regional performance indicated North America leading the industry with 45.6% share in 2023, supported by strong healthcare systems and broad consumer access.

Regional Analysis

North America has been identified as the leading regional market for antacids, and it accounted for an estimated 45.6% revenue share in 2022. This position has been supported by a mature healthcare system and reliable access to treatment. Strong purchasing power among consumers has further strengthened demand. A large aging population has increased vulnerability to digestive problems, which has raised product use. The rising incidence of acid-related disorders has also contributed to stable market expansion across the region.

The prevalence of gastroesophageal reflux disease has been considered a major factor in market growth. A study published in the Gut journal estimated that 18 to 28 percent of adults in North America experience this condition. This high burden has stimulated sustained use of antacid products. Continuous product availability and broad retail coverage have reinforced consumer adoption. These combined elements have ensured consistent demand and have supported North America’s dominant position in the global industry.

Asia Pacific is projected to record the highest compound annual growth rate of 5.4 percent during the forecast period. This growth outlook has been supported by high unmet clinical needs across several countries. Access to treatment options has been improving, and awareness of digestive health has been rising steadily. Higher disposable income among consumers has encouraged greater adoption of over-the-counter products. The evolving healthcare environment has created favorable conditions for market development throughout the region.

The presence of established companies such as GlaxoSmithKline, Pfizer, and Abbott is expected to accelerate market expansion in Asia Pacific. Their distribution networks and investment strategies have improved product penetration. Healthcare infrastructure upgrades have been observed across emerging economies, which has strengthened access to antacids. Rising private and public investment has further supported industry growth. Together, these factors have created a strong foundation for sustained regional advancement and have positioned Asia Pacific as a key contributor to future global market gains.

Segmentation Analysis

The market is segmented into tablets, liquids, and other forms, with tablets holding a 51.3% share in 2023. This dominance is supported by the use of chewable tablets that come in multiple flavors. These flavored formats improve patient compliance and support regular use. Tablets also provide accurate dosage control, which is valued in clinical settings. Their stable structure and long shelf life further strengthen their position. These combined benefits are expected to sustain the growth of the tablets segment during the forecast period.

Chewable tablets are gaining traction due to their pleasant taste and ease of consumption. These attributes make them suitable for individuals who avoid swallowing traditional pills. The improved palatability supports adherence and increases repeat purchases. Traditional tablet formats also offer reliable dosing. This consistency ensures effective treatment outcomes and reduces the risk of improper intake. Healthcare providers prefer tablets for their predictable performance. As a result, steady demand is anticipated for both chewable and conventional tablet forms across the antacids market.

The market is also segmented by distribution channel, including hospital pharmacy, retail pharmacy, and online pharmacy. Retail pharmacies held a 41.5% revenue share, reflecting strong consumer reliance on these outlets. Their widespread presence in residential and commercial areas supports easy access. This accessibility allows customers to obtain antacids quickly. The ability to make immediate purchases without waiting for shipping is valued. Retail pharmacies also provide clear product visibility, which encourages informed decisions. These factors continue to strengthen the retail channel’s market position.

Retail pharmacies offer a broad selection of healthcare products, and this variety benefits consumers seeking antacids alongside other essentials. The presence of trained pharmacists enhances the credibility of the purchasing process. Customers receive guidance on dosage, product selection, and safe use. Such professional support builds trust and encourages repeat visits. The combination of convenience, product availability, and expert consultation drives sustained demand. As consumer expectations rise, retail pharmacies are expected to maintain their lead in the distribution landscape of the antacids market.

Key Market Segments

By Type

- Tablet

- Liquid

- Others

By Distribution Channel

- Retail pharmacy

- Hospital pharmacy

- Online pharmacy

Key Players Analysis

The competitive structure of the antacids market has been shaped by broad product portfolios, wide distribution networks, and continuous investment in innovation. Market growth has been supported by strong brand positioning, extensive promotional strategies, and rising consumer demand for fast-acting gastrointestinal solutions. Key participants have been focusing on strengthening their formulations and enhancing product availability across multiple retail channels. Companies such as GlaxoSmithKline plc and Bayer AG have been recognized for consistent portfolio expansion and sustained efforts to maintain leadership within the global landscape.

Strategic initiatives have been widely adopted to improve market penetration and operational efficiency. The introduction of advanced antacid formats, including chewable tablets and liquid suspensions, has been prioritized to meet diverse consumer requirements. Expansion across emerging economies has also been accelerated to tap into increasing self-medication trends. Firms like Boehringer Ingelheim International GmbH and Dr. Reddy’s Laboratories Ltd. have demonstrated active participation in product development and regional expansion to secure stronger competitive positions.

Partnerships and collaborative ventures have become essential tools for broadening market reach and enhancing research capabilities. These alliances have enabled rapid regulatory approvals and improved access to global supply chains. Continuous investments in consumer-centric formulations have been observed across major companies. Sanofi, Reckitt Benckiser Group plc, and Sun Pharmaceuticals Ltd. have been noted for adopting cooperative strategies to strengthen their brand presence and reinforce their product portfolios in both developed and developing markets.

The competitive scenario has also included innovation-led initiatives, pricing optimization, and targeted promotional activities. Companies have aimed to reinforce trust by ensuring consistent quality and regulatory compliance. Technological advancements in drug formulation and packaging have further supported market differentiation. Organizations like Takeda Pharmaceutical Company Limited, Pfizer Inc., and Procter & Gamble have been actively involved in refining product lines and improving global distribution, while other key players continue to contribute to overall market expansion through focused investments.

Top Key Players in Antacids Market

- GlaxoSmithKline plc

- Bayer AG

- Boehringer Ingelheim International GmbH

- Reddy’s Laboratories Ltd.

- Sanofi

- Reckitt Benckiser Group plc

- Sun Pharmaceuticals Ltd.

- Takeda Pharmaceutical Company Limited

- Pfizer Inc.

- Procter & Gamble

- Other Key Players

Challenges

1. Increasing Preference for Long-Term Treatment Options

Demand for long-term relief solutions has been rising in recent years. More consumers prefer proton pump inhibitors and H2-blockers for sustained control of symptoms. These therapies are seen as effective for chronic digestive issues. As a result, basic antacid products face slower market growth. Antacids are mainly chosen for short-term or occasional relief, which restricts their overall use. This shift in consumer preference reduces the long-term revenue potential for companies focused on traditional formulations. The trend has created a competitive pressure that limits market expansion and affects product differentiation strategies.

2. Rising Awareness of Side Effects

Awareness of the possible side effects linked to frequent antacid use has increased. Concerns about mineral imbalance and excessive intake encourage more cautious consumer behavior. This situation has reduced confidence in certain product segments. Many consumers now look for options with fewer risks or clearer safety profiles. As a result, product adoption may slow in markets with high awareness levels. This shift impacts demand and creates challenges for companies attempting to maintain steady sales. The trend also increases the need for transparent labeling and stronger communication about product safety.

3. Availability of Low-Cost Alternatives

Low-cost generic antacids are widely available across many regions. These products offer similar benefits at lower prices. As a result, strong price competition has become a major challenge for branded manufacturers. The presence of multiple substitutes limits premium pricing strategies. Companies often face pressure to reduce costs while maintaining product quality. This situation restricts profit margins and affects long-term sustainability. The market becomes more competitive, and differentiation becomes difficult. Manufacturers must adopt efficient production and distribution practices to remain competitive in this environment. Price-sensitive consumers continue to drive demand toward generic products.

4. Regulatory Compliance Requirements

Antacid products must meet strict safety and quality regulations. These requirements are often updated to ensure consumer protection. Compliance involves rigorous testing and documentation. Such processes increase production costs for manufacturers. Changes in regulatory frameworks may cause delays in product approvals. These delays slow the launch of new formulations and extensions. Companies must invest in continuous monitoring to meet evolving standards. This situation adds operational challenges and limits flexibility in product development. The need for regulatory adherence influences both time-to-market and overall competitiveness in the industry.

5. Changing Dietary Habits

Irregular eating patterns have increased digestive discomfort among consumers. This trend could support higher demand for antacid products. However, many self-care remedies are now easily accessible. The presence of multiple solutions makes consumer behavior harder to predict. This unpredictability affects demand forecasting for manufacturers. Companies must adjust production planning to avoid shortages or oversupply. Shifts in lifestyle and food habits continue to influence usage patterns. Market participants need to track these changes closely. The complexity of consumer preferences creates long-term challenges for accurate demand estimation.

Opportunities

1. Growth in Self-Medication Trends

The rise in self-medication has been driving strong demand for antacids. Consumers now prefer quick and accessible solutions for common digestive issues. Over-the-counter products are chosen because they offer relief without the need for medical visits. The growth of this behavior has supported steady market expansion. Antacids are widely recognized and trusted for immediate relief from acidity and heartburn. Their availability across local stores and pharmacies has reinforced this trend. The shift toward self-care practices is expected to continue. This movement creates a favorable environment for companies offering safe and efficient antacid formulations.

2. Expansion in Retail and Online Pharmacies

Retail and online pharmacies have expanded at a rapid pace. This expansion has increased the visibility of antacid products. Consumers now have easy access to a wide range of brands and formats. Online platforms offer convenient shopping and quick delivery. These factors have supported consistent market demand. Improved distribution networks have reduced regional availability gaps. Digital pharmacies also provide product comparisons and reviews. These features guide consumers toward faster purchase decisions. The broader reach of retail and e-commerce channels is expected to strengthen long-term market growth. This shift enhances both consumer engagement and brand penetration.

3. Rising Incidence of Digestive Disorders

Digestive disorders have increased due to stress, poor diets, and inactive lifestyles. This rise has driven higher consumption of antacid products. Fast-food habits and irregular meals have contributed to acidity and heartburn cases. These conditions often require quick relief, which antacids provide. The growing prevalence of such disorders has created a steady demand base. Healthcare professionals also recommend antacids for mild symptoms. The trend is expected to continue as lifestyle pressures increase. This situation supports consistent market growth. Antacid manufacturers benefit from continuous product use among diverse age groups. The increased awareness of digestive health also adds momentum.

4. Product Innovation Opportunities

Product innovation has created significant openings for market expansion. Consumers now look for improved taste, faster action, and natural compositions. These preferences encourage companies to develop advanced formulations. New formats such as chewable tablets, gels, and liquid suspensions attract wider users. Natural and herbal ingredients are gaining interest among health-conscious consumers. Better flavor profiles and easy dosing enhance user experience. Innovation helps brands strengthen their competitive position. It also allows manufacturers to address unmet needs in the digestive care segment. Continuous research and development activities are expected to support future growth. This trend boosts market diversification.

5. Emerging Market Penetration

Developing regions offer strong potential for antacid market expansion. Many of these markets remain underserved. Rising healthcare awareness has improved demand for basic digestive care products. Better distribution networks allow companies to reach new consumer groups. Affordability and availability influence purchase behavior in these regions. As incomes rise, consumers show higher interest in OTC digestive solutions. Local retail growth also increases product access. These factors support long-term opportunities for global and regional brands. Market penetration strategies can generate sustained revenue growth. The expansion into emerging markets is expected to remain a key driver for industry development.

Conclusion

The global antacids market is expected to show steady growth, supported by rising digestive health concerns and wider use of fast-acting relief products. Demand has been strengthened by lifestyle changes, greater self-care practices, and improved access through retail and online channels. The growing older population has also increased consistent product use across regions. Continued product innovation, including better-tasting and user-friendly formats, is improving acceptance among diverse consumers. Expansion in emerging markets is expected to offer added momentum as awareness and purchasing power increase. Overall, the market outlook remains positive, with stable consumption patterns and broader distribution networks supporting long-term development.

View More

Digestive Health Market || Digestive Health Drinks Market || Over The Counter Analgesics Market || Over the Counter (OTC) Drugs Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)