Table of Contents

Overview

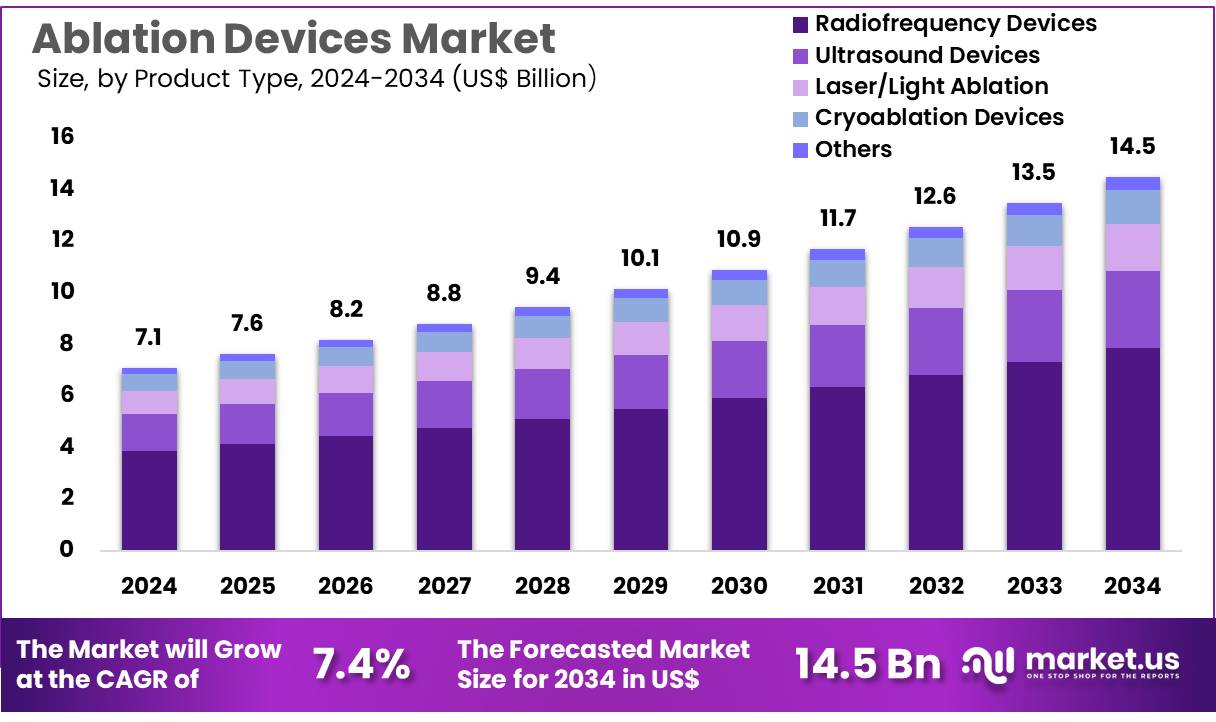

New York, NY – Nov 25, 2025 – Global Ablation Devices Market size is expected to be worth around US$ 14.5 billion by 2034 from US$ 7.1 billion in 2024, growing at a CAGR of 7.4% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 39.2% share with a revenue of US$ 2.8 Billion.

The global ablation devices market is witnessing steady expansion as the demand for minimally invasive procedures continues to rise across major healthcare economies. The adoption of ablation technologies has been supported by increasing prevalence of chronic diseases, growth in the geriatric population, and continuous advancements in energy-based treatment systems. A notable shift toward image-guided and robot-assisted procedures has further strengthened the market outlook.

The market value has been increasing at a consistent rate, driven by strong utilization in oncology, cardiology, and pain management applications. The growth of the market can be attributed to the clinical benefits associated with ablation procedures, including reduced surgical trauma, shorter hospital stays, and improved patient recovery timelines. Radiofrequency, microwave, cryoablation, and laser-based systems continue to dominate procedural volumes, while emerging modalities such as irreversible electroporation are gaining traction.

Manufacturers are focusing on technological innovation, regulatory approvals, and strategic collaborations to enhance product portfolios. Investments in next-generation ablation platforms, precision-based delivery systems, and improved safety features have been observed across the industry. Favorable reimbursement structures and rising procedure rates in hospitals and ambulatory surgical centers are expected to support sustained adoption.

North America continues to account for a significant share of the market, while Asia-Pacific is anticipated to exhibit the fastest growth due to expanding healthcare infrastructure and increasing awareness of minimally invasive treatments. Overall, the market is positioned for robust long-term development as demand for effective, minimally invasive ablation solutions strengthens globally.

Key Takeaways

- The ablation devices market generated revenue of US$ 7.1 billion in 2024, supported by a CAGR of 7.4%, and the market value is projected to reach US$ 14.5 billion by 2033.

- The product landscape is segmented into radiofrequency devices, ultrasound devices, laser/light ablation, cryoablation devices, and other technologies, with radiofrequency devices accounting for 54.3% of the market in 2024.

- Based on application, the market comprises cardiology, oncology, gynecology, ophthalmology, and other areas, with cardiology representing 49.2% of the total share.

- In terms of end users, hospitals, ambulatory surgery centers, and other healthcare facilities constitute the market structure, and hospitals dominated with a 56.8% revenue share.

- North America led the global market, capturing 39.2% of total revenue in 2024.

Regional Analysis

North America is leading the Ablation Devices Market

North America maintained the largest revenue share of 39.2%, driven by the rising incidence of chronic diseases, steady technological progress, and broader insurance coverage. According to the American Cancer Society, the United States recorded 2 million new cancer diagnoses in 2023, many of which required tumor ablation interventions.

Reimbursement support strengthened further, as the Centers for Medicare & Medicaid Services reported a 23% rise in approved ablation procedure reimbursements in 2023 compared with 2022, improving treatment accessibility. Regulatory momentum also remained strong, with the US Food and Drug Administration authorizing 15 new ablation technologies in 2023, including advanced systems for cardiac and neurological use.

Cardiac ablation volumes also increased, supported by a growing atrial fibrillation patient base. The American Heart Association reported an 18% rise in cardiac ablation procedures from 2022 to 2023. Leading medical institutions such as Mayo Clinic and Cleveland Clinic indicated a 30% increase in minimally invasive ablation surgeries in 2023. Additional market momentum was generated by the National Cancer Institute’s US$200 million funding expansion for interventional oncology in 2024.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is projected to register the fastest growth rate during the forecast period. China’s National Health Commission recorded a 25% increase in cancer ablation procedures since 2022, reflecting rising adoption across oncology departments. Regulatory activity in Japan also supported market expansion, with the Ministry of Health, Labour and Welfare approving 12 new ablation devices in 2023, particularly for liver and lung cancer applications.

Government initiatives continue to play a central role. India’s Ayushman Bharat program allocated US$150 million in 2023 for advanced surgical and ablation equipment in public hospitals. South Korea’s National Cancer Center observed a 40% rise in thyroid ablation cases between 2022 and 2023, while Australia’s Therapeutic Goods Administration expedited approval for 8 new ablation technologies in 2023.

The Asia Pacific Society of Cardiology projected a 35% increase in demand for cardiac ablation procedures by 2025, supported by aging populations and improved healthcare infrastructure. These advancements underline the region’s strong potential for accelerated market expansion.

Market Dynamics

- Driver: The rising prevalence of atrial fibrillation continues to support strong demand for ablation devices. Projections indicate that 12.1 million Americans will be affected by AFib by 2030, with over 454,000 hospitalizations and 232,030 deaths reported in 2021. Early catheter ablation is increasingly recommended over drug therapy for eligible patients, strengthening device utilization across cardiology settings.

- Trend: Regulatory momentum for pulsed field ablation (PFA) technologies is accelerating innovation in the market. The FARAPULSE™ PFA system received FDA premarket approval on January 30, 2024, following Medtronic’s PulseSelect™ PFA approval on December 13, 2023. These advancements highlight a clear shift toward irreversible electroporation platforms that enable faster, more precise treatment workflows and broader clinical adoption, setting the foundation for next-generation ablation solutions.

- Restraint: Market expansion faces challenges related to reimbursement variability and coding complexity. The new HCPCS code C8005, effective April 1, 2025, covers transbronchial pulsed electric field lung tumor ablation, yet OPPS coverage policies remain under development. Additionally, bundled CPT codes for intracardiac ablation procedures include essential monitoring services such as TEE, limiting separate billing and discouraging wider provider adoption.

- Opportunity: Growing use of ablation technologies in oncology provides significant growth potential. The IARC reported 905,700 global liver cancer diagnoses and 830,200 deaths in 2020, with cases expected to reach 1.4 million by 2040. Minimally invasive ablation modalities including radiofrequency, microwave, and PEF provide effective localized tumor control in hepatocellular carcinoma, positioning ablation devices as critical tools in addressing the expanding global cancer burden.

Frequently Asked Questions on Ablation Devices

- How do ablation devices work?

Ablation devices operate by delivering targeted energy to affected tissues, causing controlled destruction without significant damage to surrounding structures. This mechanism enables precise treatment of tumors, arrhythmias, and other conditions requiring localized tissue modification in clinical settings. - What medical conditions are treated using ablation devices?

Ablation devices are used to manage diverse conditions, including cardiac arrhythmias, liver and lung tumors, chronic pain disorders, and thyroid nodules. Their minimally invasive nature supports faster recovery and reduced complication risks across multiple therapeutic domains. - What types of ablation technologies are commonly used?

Common ablation technologies include radiofrequency, laser, ultrasound, cryotherapy, and microwave systems. Each modality offers specific benefits related to penetration depth, precision, and thermal control, enabling clinicians to select the most suitable approach for patient needs. - What advantages do ablation devices offer over conventional surgery?

Ablation offers smaller incisions, reduced hospital stays, and lower postoperative complications compared with traditional surgery. These benefits support improved patient outcomes, faster recovery, and broader adoption of minimally invasive treatment pathways across healthcare systems. - Which product segment leads the global market?

Radiofrequency ablation devices hold the leading share due to widespread clinical use, proven safety profiles, and strong adoption across cardiac and oncological applications. Their reliability and cost-effectiveness continue to strengthen their dominance in the product landscape. - Which application area contributes most to market demand?

Cardiology represents the largest application segment, supported by increasing atrial fibrillation cases and rising preference for minimally invasive cardiac procedures. Growing procedural volumes and expanded clinical guidelines reinforce the significance of this segment in market growth. - Who are the primary end users of ablation devices?

Hospitals serve as the dominant end-user group due to their advanced infrastructure, skilled workforce, and higher procedure volumes. Ambulatory surgery centers also contribute significantly as demand for outpatient minimally invasive treatments continues to increase worldwide. - Which region currently leads the global ablation devices market?

North America maintains leadership due to high disease prevalence, strong reimbursement frameworks, and rapid adoption of advanced technologies. Robust research funding and the presence of leading medical institutions further strengthen the region’s market position.

Conclusion

The global ablation devices market is positioned for sustained long-term growth as demand for minimally invasive treatments continues to increase across major clinical disciplines. Market expansion is supported by rising chronic disease prevalence, strong adoption in cardiology and oncology, and continuous innovation in energy-based systems.

Regulatory approvals, technological advancements, and expanding reimbursement pathways further enhance adoption across hospitals and ambulatory centers. North America remains a key revenue contributor, while Asia Pacific presents the fastest growth potential driven by improving healthcare infrastructure. Overall, the market is expected to advance steadily as next-generation ablation technologies gain broader clinical acceptance worldwide.