Table of Contents

Overview

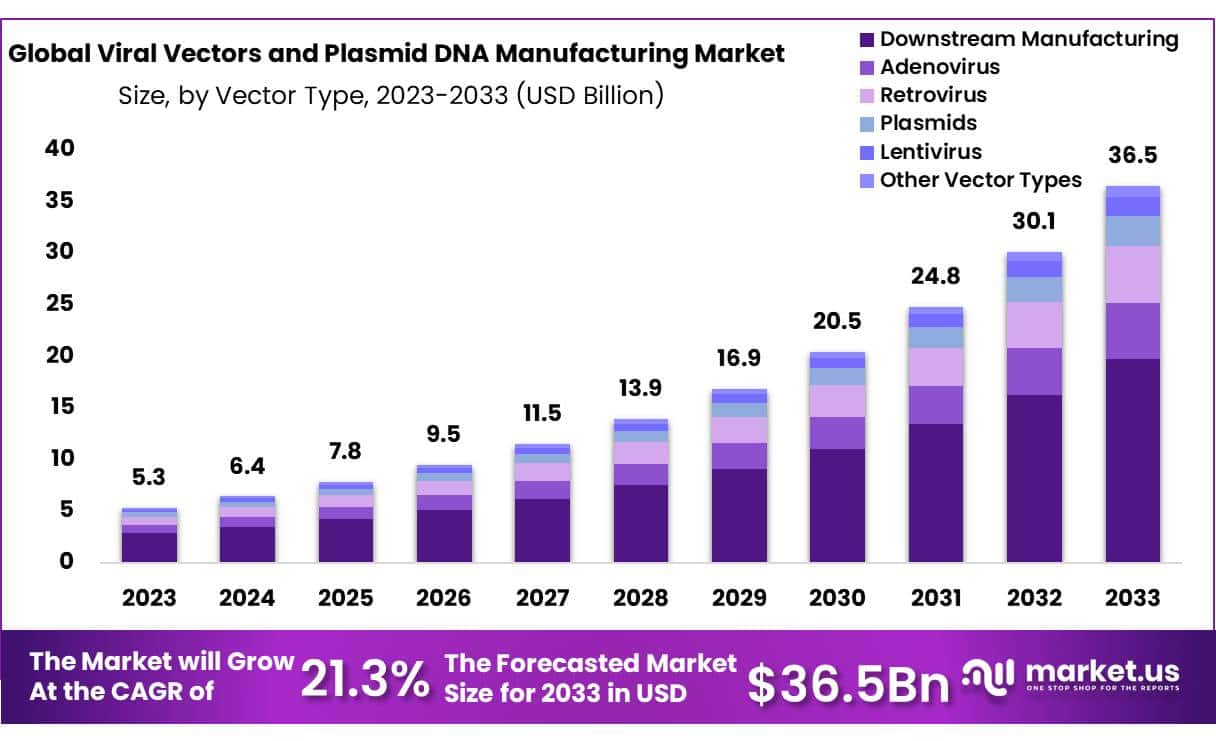

New York, NY – Sep 30, 2025 – The Global Viral Vectors and Plasmid DNA Manufacturing Market size is expected to be worth around USD 36.5 Billion by 2033 from USD 6.4 Billion in 2024, growing at a CAGR of 21.3% during the forecast period from 2025 to 2033.

The global demand for advanced therapies has accelerated the importance of robust viral vector and plasmid DNA (pDNA) manufacturing. These platforms form the backbone of gene therapies, vaccines, and cell-based treatments, enabling the delivery of genetic material with precision and safety.

Viral vectors, including adeno-associated virus (AAV), lentivirus, and adenovirus, are engineered to introduce therapeutic genes into patient cells. Their high efficiency and targeted delivery capabilities have made them indispensable in the development of innovative treatments for cancer, rare diseases, and infectious disorders. In parallel, plasmid DNA serves as a critical starting material for the production of viral vectors and mRNA-based therapeutics. Its scalability, stability, and ability to carry large genetic payloads have positioned it as a cornerstone of next-generation biopharmaceuticals.

The expansion of manufacturing capacity is being driven by rising clinical trial volumes and regulatory approvals in advanced therapies. Investments in state-of-the-art facilities, single-use technologies, and automation are ensuring high yields, reproducibility, and compliance with stringent regulatory standards.

Market growth is expected to be fueled by strategic collaborations between biopharmaceutical companies and contract development and manufacturing organizations (CDMOs). The integration of advanced analytics and process intensification is further optimizing production timelines and lowering costs. Viral vectors and plasmid DNA manufacturing represent a vital enabler of the biopharma industry’s progress toward personalized medicine, offering new hope to patients worldwide.

Key Takeaways

- Market Size: Viral Vectors and Plasmid DNA Manufacturing Market size is expected to be worth around USD 36.5 Billion by 2033 from USD 6.4 Billion in 2024.

- Market Growth: The market growing at a CAGR of 21.3% during the forecast period from 2025 to 2033.

- Vector Type Analysis: Downstream Manufacturing leads the Viral Vectors and Plasmid DNA Manufacturing Market with 54% market share.

- Application Analysis: In 2023, vaccinology will account for 23% of the market.

- End-Use Analysis: Research Institutes represent 59% of the end-users in the Viral Vectors and Plasmid DNA Manufacturing Market.

- Regional Analysis: North America held a 47.8% global market share and held USD 2.5 billion.

- Technological Advancements: Innovations in manufacturing technologies, such as improved vector design and scalable production methods, are driving efficiency and quality in the production process.

- Investment Surge: Significant investments from pharmaceutical companies and venture capitalists are fueling research and development in this sector.

- Strategic Collaborations: Partnerships and collaborations among biotechnology companies, research institutions, and contract manufacturing organizations (CMOs) are enhancing production capabilities and market reach.

- Customization and Flexibility: The trend towards personalized medicine is leading to a higher demand for customized and flexible manufacturing solutions tailored to specific therapeutic needs.

Regional Analysis

By 2023, North America accounted for 47.8% of the global market share, valued at USD 2.5 billion. The dominance of the region can be attributed to the presence of numerous research centers and institutes dedicated to advanced therapy development. In addition, substantial federal government investments aimed at strengthening the cell therapy research base are anticipated to further support regional growth.

In contrast, Asia Pacific is projected to register the fastest growth rate over the forecast period. The expansion is being driven by a rising patient population, coupled with increasing research and development activities in the region. The large population base and untapped resources have made Asia Pacific an attractive market for multinational corporations. Furthermore, patients from Western countries are increasingly opting for stem cell therapies in Asia due to its comparatively less restrictive regulatory framework.

The availability of low-cost manufacturing and research facilities further enhances the region’s competitive advantage. These factors are expected to accelerate the advancement of stem cell research in Asia Pacific and contribute significantly to overall market expansion.

Frequently Asked Questions on Viral Vectors and Plasmid DNA Manufacturing

- What are viral vectors and plasmid DNA?

Viral vectors are engineered viruses used to deliver genetic material into cells, while plasmid DNA are circular DNA molecules utilized as templates in gene therapy and vaccine production. Both are crucial in advanced therapeutic applications. - Why are viral vectors important in gene therapy?

Viral vectors are vital in gene therapy because they enable the safe and efficient transfer of therapeutic genes into patient cells. This mechanism supports treatment of genetic disorders, cancer, and rare diseases through targeted and controlled delivery. - What are the main types of viral vectors?

The most commonly used viral vectors include adeno-associated viruses, lentiviruses, retroviruses, and adenoviruses. Each vector type possesses unique properties, making them suitable for specific therapeutic applications such as cancer immunotherapy, rare disease treatment, or vaccine development. - How is plasmid DNA manufactured?

Plasmid DNA is manufactured through bacterial fermentation, followed by purification and quality testing. The process ensures high purity, consistency, and scalability to meet regulatory standards, particularly for use in cell and gene therapies or vaccine platforms. - What challenges exist in viral vector and plasmid DNA manufacturing?

Key challenges include scalability, high production costs, maintaining product consistency, and meeting strict regulatory requirements. Limited manufacturing capacity and technical complexities also contribute to supply bottlenecks in this rapidly expanding biopharmaceutical sector. - Which end-users dominate the market?

Biopharmaceutical companies dominate the market, followed by academic research institutes and contract development and manufacturing organizations (CDMOs). These players are extensively investing in large-scale production and research to meet rising therapeutic demand. - Which regions are leading in this market?

North America leads due to strong R&D infrastructure, significant investments, and favorable regulations. Europe follows closely, while Asia-Pacific shows the fastest growth, driven by expanding biotechnology hubs, supportive government initiatives, and increasing clinical trials. - What are the major challenges in the market?

Challenges include high production costs, technical complexities, limited skilled workforce, and stringent regulatory compliance. Supply chain limitations and capacity constraints further create bottlenecks, affecting timely delivery of viral vectors and plasmid DNA products.

Conclusion

The viral vectors and plasmid DNA manufacturing industry is positioned as a cornerstone of advanced therapies, enabling the development of gene therapies, vaccines, and cell-based treatments. Market growth is fueled by rising clinical trial volumes, regulatory approvals, and strong investments in manufacturing technologies.

North America dominates due to robust research infrastructure, while Asia Pacific is emerging as the fastest-growing region. Despite challenges such as scalability, costs, and regulatory complexities, strategic collaborations and innovations are enhancing capacity and efficiency. Overall, the sector represents a vital enabler of personalized medicine, offering transformative opportunities for patients and driving the future of biopharma.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)