Table of Contents

Overview

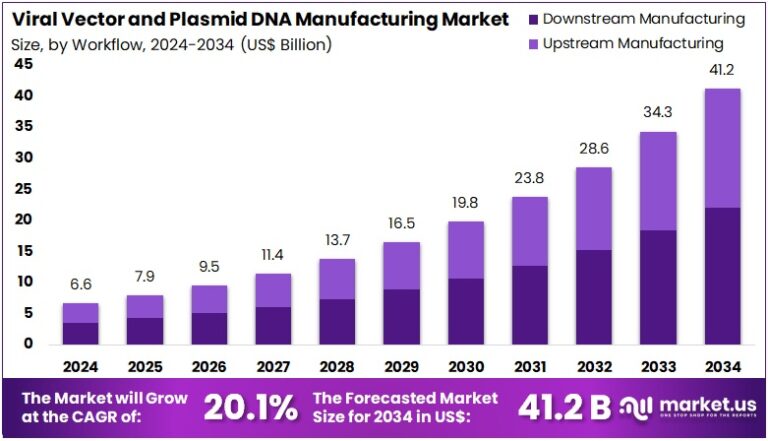

New York, NY – Aug 06, 2025 : Global Viral Vector and Plasmid DNA Manufacturing Market is projected to grow from US$ 6.6 Billion in 2024 to US$ 41.2 Billion by 2034. This reflects a strong CAGR of 20.1% during the forecast period. The surge is largely driven by growing demand for gene therapies and DNA vaccines. These technologies rely heavily on viral vectors and plasmid DNA as delivery and production tools. Increased focus on genetic medicine and improved funding across biopharmaceutical research is further accelerating this market’s upward trajectory.

Viral vectors play a crucial role in delivering therapeutic genes to target cells. They are widely used in the development of cell and gene therapies, especially for conditions like cancer and genetic disorders. Plasmid DNA, on the other hand, is a foundational tool for DNA vaccine development and gene editing processes. Their rising applications in personalized medicine and immunotherapy are pushing biopharmaceutical companies to invest in large-scale production facilities and more advanced technologies.

The market is witnessing notable expansion due to strategic moves by key players. For instance, in April 2022, FUJIFILM Diosynth Biotechnologies acquired a cell therapy manufacturing facility from Atara Biotherapeutics. Located in California, the site boosts its capacity to meet rising clinical and commercial demand. Such acquisitions highlight how companies are expanding their manufacturing capabilities to support the growing pipeline of gene and cell therapies. These actions also reflect the importance of having flexible and scalable infrastructure for next-generation treatments.

Rising prevalence of genetic diseases, cancer, and infectious illnesses is also driving market demand. As global health challenges evolve, the need for rapid and reliable treatment options grows. Gene therapy and DNA-based vaccines offer promising solutions, further fueling the need for viral vector and plasmid DNA manufacturing. Additionally, regulatory agencies are showing increasing support for gene-based therapies. This supportive regulatory environment is helping to speed up product approvals and development timelines.

The COVID-19 pandemic significantly boosted interest in mRNA and DNA-based vaccines. This has led to an increased demand for plasmid DNA, which is a vital component in vaccine production. Emerging technologies like CRISPR and advanced gene editing are also creating new use cases for viral vectors in both clinical and research applications. As these technologies mature, the demand for precise and scalable manufacturing solutions will grow. This creates long-term opportunities for manufacturers specializing in viral vector and plasmid DNA production.

Key Takeaways

- In 2024, the viral vector and plasmid DNA manufacturing market reached US$ 6.6 billion, projected to grow to US$ 41.2 billion by 2034.

- The market is experiencing a strong CAGR of 20.1%, driven by growing demand for gene therapies, vaccines, and advanced molecular medicine applications.

- Among vector types, adeno-associated virus (AAV) dominated in 2024, capturing 24.6% of the market due to its safety and broad therapeutic use.

- The workflow segment is split into upstream and downstream manufacturing, with downstream processes accounting for a leading 53.5% market share in 2024.

- In terms of application, vaccinology emerged as the largest segment, contributing 42.3% of total revenue due to increased vaccine development activity.

- Disease-wise, cancer-related applications took the top spot in 2024, generating 48.9% of market revenue owing to rising gene therapy research.

- End-user analysis shows research institutes led the market with a 59.3% share, highlighting their growing role in advancing therapeutic development.

- Regionally, North America led the global market with a commanding 46.9% share, driven by strong R&D investments and advanced healthcare infrastructure.

Regional Analysis

North America leads the viral vector and plasmid DNA manufacturing market, holding a 46.9% revenue share. This dominance is due to expanding clinical use of gene therapies. The U.S. FDA approved three gene therapy products in 2022 and two in 2023, each requiring large volumes of high-quality vectors. Strong support from the National Institutes of Health (NIH) also fuels growth. In 2023, NIH awarded over US$ 1.3 billion in gene therapy-related grants. A major part supported viral vector technology development, which is key for gene delivery applications.

Asia Pacific is projected to witness the highest CAGR in this market. This growth is driven by rising investments in biotech and biopharmaceutical research. China, for example, allocated 2.54% of GDP to R&D in 2022, with much of it focused on gene therapy. Increasing cases of genetic disorders across the region also raise demand for advanced treatments. Improved healthcare systems in countries like India and South Korea aid adoption. Regulatory progress and clear guidelines further boost confidence among researchers and manufacturers in this fast-growing market.

Segmentation Analysis

Vector Type Analysis

In 2024, the adeno-associated virus (AAV) segment led the market with a 24.6% share. AAV vectors are widely used in gene therapy due to their ability to deliver genes efficiently with low immune response. They enable long-term gene expression in various tissues, making them ideal for treating genetic disorders. The rise in rare disease therapies is fueling this growth. Improved AAV manufacturing methods and the increasing number of clinical trials are expected to boost demand for AAV vectors in coming years.

Workflow Analysis

Downstream manufacturing accounted for a 53.5% market share in 2024. This stage is crucial in purifying and formulating viral vectors and plasmid DNA. As gene therapies become more common, demand for scalable and efficient downstream processing is increasing. Innovations in purification technologies are improving the quality and yield of vectors. Large-scale production is becoming essential. The focus on safety and regulatory compliance is also pushing growth in this area, making downstream manufacturing a key workflow segment in the market.

Application Analysis

The vaccinology segment achieved a 42.3% revenue share due to rising demand for viral vector-based vaccines. The COVID-19 pandemic highlighted the importance of fast and effective vaccine development. Viral vectors can trigger both cellular and humoral immune responses, making them ideal for vaccine delivery. Their ability to provide long-lasting immunity drives their popularity. Successful clinical trials are encouraging further investments in this segment. This is expected to lead to the development of new vaccines targeting a wide range of infectious diseases.

Disease Analysis

The cancer segment represented 48.9% of the total revenue due to the growing use of gene therapies in oncology. Viral vectors are used to deliver therapeutic genes directly to tumor cells, enhancing treatment effectiveness. This targeted approach reduces side effects compared to traditional treatments. Immunotherapies and oncolytic viruses are driving this trend. With cancer being a global health burden, demand for novel therapies is high. Advancements in manufacturing technology are improving the scalability and stability of these vectors, supporting market growth.

End-user Analysis

Research institutes held the largest share at 59.3% in 2024. These institutions are central to the advancement of gene therapy and genomic research. Increased funding in areas like cancer, infectious diseases, and rare genetic disorders is driving demand for viral vectors. Academic labs often partner with biotech and pharma firms, accelerating innovation. Their need for high-quality plasmid DNA and vectors is growing. As research activity expands worldwide, this end-user segment will remain a major driver in the viral vector and plasmid DNA manufacturing market.

Key Players Analysis

Key players in the viral vector and plasmid DNA manufacturing market are focused on scaling production and improving efficiency. They invest in advanced technologies to enhance manufacturing processes and meet the rising demand for gene therapies and vaccines. These companies expand service offerings and form partnerships with biopharma firms, CDMOs, and research institutions. Strategic collaborations are central to their growth. Geographic expansion, especially in emerging markets, helps capture new business. Regulatory compliance and strict quality control remain top priorities to ensure global product consistency.

Lonza Group is a major player in this market, offering end-to-end services in cell and gene therapy manufacturing. The company supports clients from early process development to large-scale production of viral vectors and plasmid DNA. With cutting-edge facilities and deep industry expertise, Lonza plays a vital role in accelerating gene therapy development. Its focus on innovation, scalability, and high-quality manufacturing makes it a preferred partner for biotech firms. Lonza continues to grow its capacity and strengthen global partnerships to meet future demand.

Emerging Trends

- Rising Demand from Gene Therapy and Cell Therapy: Gene and cell therapies are gaining momentum as treatments for cancer, rare genetic conditions, and immune disorders. These therapies rely heavily on viral vectors and plasmid DNA as delivery tools. As more clinical trials and FDA approvals occur, the need for these components is growing fast. Biotech companies are increasing production to meet the demand. Hospitals and research labs also require a steady supply to support ongoing studies. This rising demand is pushing the market forward, encouraging manufacturers to expand capacity and streamline production methods to stay competitive.

- Shift Toward Scalable and Automated Manufacturing: Manufacturers are shifting toward scalable systems and automation to meet rising demand. Traditional manual methods are slower and more prone to human error. Automation improves consistency, boosts output, and helps lower contamination risks. Closed-system manufacturing is also becoming more common. These systems operate in a sterile, controlled environment. This makes them ideal for producing clinical-grade materials. Companies are also investing in advanced bioreactors and digital monitoring tools. These upgrades help scale production while maintaining high-quality standards, making the entire process faster, safer, and more cost-efficient.

- Growing Interest in Non-Viral Alternatives: While viral vectors are still the standard, non-viral delivery systems are gaining interest. These include lipid nanoparticles and other synthetic carriers. They are being studied as safer, easier-to-produce options. Non-viral methods reduce the risk of triggering immune responses in patients. They also simplify the regulatory process and lower production costs. As research grows, more companies are diversifying their capabilities. Manufacturers are expanding their technology platforms to include both viral and non-viral systems. This helps them stay flexible and competitive in a rapidly evolving market.

- Increased Focus on Quality and Regulatory Compliance: With more therapies moving to clinical and commercial stages, regulatory scrutiny is increasing. Manufacturers must meet strict quality standards, including GMP (Good Manufacturing Practice) guidelines. Facilities are being upgraded to ensure cleanroom environments and full traceability. Quality control systems are also being modernized to detect any issues early. Companies are hiring compliance experts and investing in audit readiness. This trend reflects the industry’s need to gain regulatory approval quickly. Failing to meet standards can lead to costly delays or product recalls, making compliance a top priority.

- Partnerships and Collaborations Are on the Rise: Strategic partnerships are playing a major role in market growth. Biotech firms, pharmaceutical companies, and CDMOs (Contract Development and Manufacturing Organizations) are joining forces. These collaborations allow companies to share technology, pool resources, and speed up development timelines. By working together, they can overcome complex manufacturing challenges and bring therapies to market faster. Academic institutions are also part of this trend, contributing research and innovation. These partnerships help companies stay ahead in a competitive market while reducing risk and improving cost-efficiency.

- Expansion into Emerging Markets: To reduce costs and meet growing demand, companies are expanding into emerging regions like Asia, Latin America, and Eastern Europe. These areas offer skilled labor, improving healthcare infrastructure, and government support. Setting up manufacturing plants in these regions helps companies get closer to local markets. It also lowers transportation costs and import taxes. Countries like India and Brazil are becoming attractive hubs due to strong biotech sectors. This expansion supports global supply chains and helps ensure access to life-saving therapies in developing countries.

- Use of Artificial Intelligence and Digital Tools: AI and digital technologies are transforming how viral vectors and plasmid DNA are made. Machine learning is used to predict equipment failures and optimize production processes. Real-time data helps manufacturers reduce downtime and improve batch yields. Digital tools also enhance quality control and automate documentation. These smart systems make production faster, more accurate, and more reliable. By adopting AI and digital monitoring, companies can stay ahead of problems and reduce waste. This tech-driven approach improves both cost-efficiency and product safety in a highly regulated industry.

Use Cases

- Gene Therapy Development: Viral vectors are vital tools in gene therapy. They carry corrected genes into a patient’s cells to fix genetic disorders. Diseases like hemophilia, muscular dystrophy, and cystic fibrosis are some examples. Plasmid DNA plays an essential role in this process. It provides the template to create the viral vectors needed for therapy. Without high-quality plasmid DNA, producing effective viral vectors would not be possible. As gene therapy becomes more popular, the demand for precise and efficient vector manufacturing continues to rise. This process requires strict quality control to ensure patient safety and successful treatment outcomes.

- CAR-T Cell Therapy for Cancer: CAR-T cell therapy is a breakthrough in cancer treatment. It uses a patient’s immune cells, which are genetically modified to fight cancer more effectively. Viral vectors are used to insert new genes into these immune cells. These genes help the immune system recognize and destroy cancer cells. Manufacturing these vectors is a complex but crucial step. Each batch must meet strict quality and safety standards. This ensures that the therapy is both safe and effective for patients. As CAR-T therapy expands to more types of cancer, the need for viral vector manufacturing is growing rapidly.

- mRNA Vaccine Production: Plasmid DNA is key to producing mRNA vaccines. It acts as the first step in the vaccine development process. The DNA contains instructions to create mRNA, which is used in vaccines like those for COVID-19. This mRNA teaches cells how to fight specific viruses. Without plasmid DNA, large-scale mRNA vaccine production would not be possible. The COVID-19 pandemic showed how important fast and reliable plasmid production is. Manufacturers are now investing in better technologies to meet future vaccine demands. This use case highlights the growing link between DNA tools and modern vaccine development.

- DNA-Based Vaccine Development: DNA vaccines are an emerging method to fight infectious diseases. These vaccines use plasmid DNA directly to train the immune system. The DNA includes genetic code that tells the body to make a specific antigen. This antigen then triggers an immune response. Plasmid DNA must be pure and safe, as it is injected into the body. Researchers are exploring DNA vaccines for diseases like Zika, HIV, and influenza. These vaccines are easy to produce and store. As a result, they are promising tools for use in global health emergencies and developing countries with limited cold-chain logistics.

- Animal and Agricultural Biotechnology: Viral vectors and plasmid DNA are not only used in human medicine. They also play a role in animal health and agriculture. In veterinary medicine, gene therapies help treat genetic conditions in pets and livestock. In agriculture, these tools are used to improve plants or animals. Scientists can enhance resistance to disease, boost growth rates, or increase productivity. Plasmid DNA and viral vectors are essential for these genetic improvements. As food security and animal welfare become more important, demand for advanced biotech solutions is rising. This sector continues to grow in both developed and developing regions.

- Personalized Medicine and Rare Diseases: Treating rare diseases often requires a custom approach. That’s where viral vectors and plasmid DNA come in. Each patient may need a unique genetic solution. Manufacturers create tailored vectors and DNA specifically for individual patients. This is especially important in personalized medicine. These treatments are designed to match a person’s genetic makeup. The manufacturing process must be flexible and precise. As technology advances, more rare diseases are becoming treatable through these custom therapies. This growing trend is pushing the market toward small-batch, high-precision production facilities for gene-based medicine.

- Basic Research and Clinical Trials: Academic and research institutions rely on viral vectors and plasmid DNA for discovery. These materials are used to study new therapies in labs and clinical trials. Early-stage research needs a steady supply of high-quality DNA and vectors. Without this, it’s hard to test or improve new treatments. Companies and universities both depend on these tools for innovation. As more trials move into clinical phases, demand for reliable manufacturing increases. Clean, scalable, and reproducible production is essential for regulatory approval and successful studies. This use case supports the entire biotech pipeline from lab bench to patient care.

Conclusion

In conclusion, the viral vector and plasmid DNA manufacturing market is growing quickly due to rising demand for gene therapies, vaccines, and personalized treatments. More research, better technology, and stronger regulatory support are helping this market expand worldwide. Companies are focusing on faster, safer, and more scalable production methods to meet future needs.

Key players are forming partnerships and entering new regions to stay competitive. From cancer care to vaccine development, these tools are becoming essential across healthcare and biotechnology. As the industry continues to grow, high-quality manufacturing and innovation will be the main drivers of success in this promising market.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)