Table of Contents

Overview

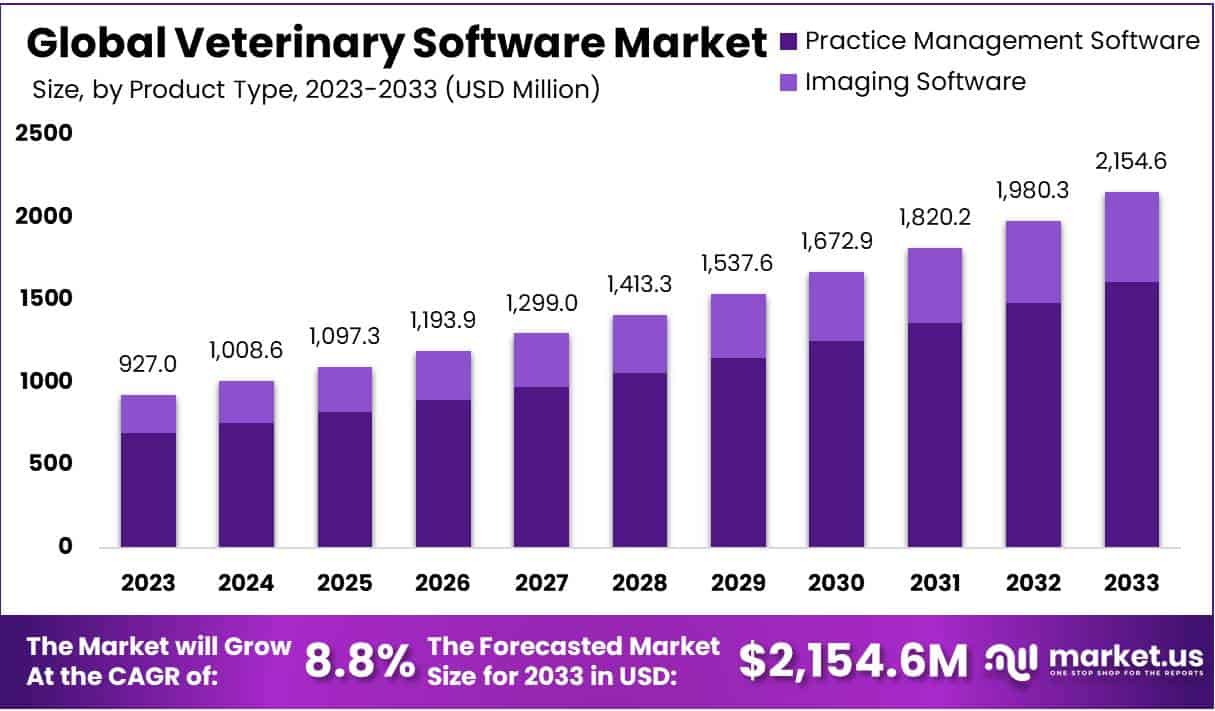

The Global Veterinary Software Market is projected to grow from USD 927 million in 2023 to approximately USD 2,154.6 million by 2033, registering a CAGR of 8.8% between 2024 and 2033. Growth is being fueled by rising pet ownership and increasing expenditure on animal healthcare across both developed and emerging economies. Households are allocating higher budgets for companion animals, which drives demand for efficient practice management and diagnostic tools. The shift in consumer attitudes toward pet well-being and preventive healthcare has strengthened the adoption of digital platforms in veterinary practices.

The digital transformation of veterinary clinics is another significant factor driving growth. Practices are increasingly adopting software for scheduling, billing, client communications, and patient record management. Cloud-based platforms, along with mobile access, have enhanced operational efficiency and enabled remote consultations. These solutions not only streamline day-to-day operations but also improve accessibility for clients seeking care. The adoption of digital tools reflects a broader modernization trend within veterinary services, aligning with the demand for fast and accurate care delivery.

Growing awareness of animal health and the importance of preventive care is also accelerating market expansion. Veterinary software supports advanced medical record management, diagnostic tracking, and personalized treatment planning. These features facilitate early disease detection and better patient outcomes. With pet owners prioritizing proactive care and wellness programs, veterinary practices are under pressure to adopt systems that improve treatment accuracy and monitoring. This shift strengthens the role of software in delivering quality veterinary services and building client trust.

The market is further shaped by the expansion of telemedicine and livestock management needs. Telehealth platforms gained momentum during the COVID-19 pandemic and continue to grow, supported by software integrations with remote monitoring tools and pet wearables. In parallel, large-scale farms are adopting herd management solutions to monitor breeding, vaccinations, and disease control. These systems enhance livestock productivity and sustainability, driving adoption across both companion animal and livestock segments. The dual role of software in pet care and farm operations broadens its application scope and growth potential.

Finally, regulatory compliance and technological advancements are strengthening market adoption. Veterinary software ensures secure record-keeping and adherence to privacy and reporting standards. Integration of artificial intelligence and data analytics is enabling predictive diagnostics, operational insights, and personalized treatment. In addition, the consolidation of veterinary practices into corporate networks is creating demand for scalable, centralized systems that manage multi-location operations. Together, these factors position veterinary software as a critical enabler of modern veterinary care and sustainable practice growth.

Key Takeaways

- The veterinary software market is forecasted to reach USD 2,154.6 million by 2032, expanding at a robust 8.8% CAGR from 2023.

- Advanced technologies such as AI and cloud computing are significantly enhancing software capabilities, driving efficiency and improving veterinary healthcare solutions worldwide.

- The COVID-19 pandemic accelerated the adoption of telemedicine, transforming veterinary services and reshaping the delivery of animal healthcare practices globally.

- Strict compliance and data security regulations are driving demand, ensuring electronic health records remain secure and aligned with international healthcare standards.

- Practice Management Software dominates with a 74.8% share, underscoring the industry’s emphasis on operational efficiency and streamlined practice workflows.

- Imaging Software, while smaller in share, is experiencing rapid growth, highlighting the rising significance of advanced diagnostic tools in veterinary healthcare.

- Small Animals represent 58% of market demand, benefiting from increasing awareness and investment in advanced healthcare solutions for companion animals.

- Mixed Animal software solutions are gaining traction, serving both small and large animals, and demonstrating the versatility required in veterinary practices.

- Veterinary hospitals and clinics lead the market with a 52.3% share, showcasing their reliance on advanced technological solutions for efficient healthcare delivery.

- North America holds a 41% market share, strengthened by technological integration, advanced veterinary practices, and a strong culture of pet ownership.

Regional Analysis

North America held a dominant share of over 41% in the veterinary software market in 2023, with a market value of USD 378.1 million. The region’s leadership can be attributed to its advanced digital infrastructure and strong integration of technology into veterinary practices. The adoption of innovative software solutions has been rapid, enabling clinics and hospitals to improve efficiency and patient outcomes. These factors collectively underline the region’s formidable position in shaping the growth trajectory of the veterinary software market.

The technological ecosystem in North America has played a decisive role in driving the adoption of veterinary software. Clinics and hospitals have embraced digital tools to streamline workflows and enhance service delivery. Advanced practice management systems, cloud-based platforms, and telemedicine solutions have been widely deployed. These technologies help veterinarians improve accuracy in diagnostics, ensure better record management, and facilitate faster decision-making. As a result, veterinary professionals are increasingly relying on software-driven approaches to improve both operational and clinical efficiency.

Growing awareness of animal welfare has been a key driver for the region’s strong performance. The culture of pet ownership in North America is characterized by high spending on animal healthcare and personalized care. Pet owners are increasingly seeking comprehensive veterinary services, creating strong demand for advanced management solutions. This demand has pushed veterinary practices to adopt specialized software to manage patient records, scheduling, and treatment plans. The growing emphasis on quality of care and preventive healthcare has accelerated software adoption across the region.

The regulatory environment in North America has also supported market growth. Compliance requirements regarding patient data management and healthcare standards have encouraged clinics to adopt secure, advanced platforms. Regulations have incentivized investment in state-of-the-art systems to ensure accuracy, compliance, and data protection. Furthermore, the presence of key players and strategic collaborations has reinforced market leadership. Established vendors and innovative startups have capitalized on this environment, offering solutions tailored to veterinary professionals’ evolving needs. Together, these dynamics continue to consolidate North America’s dominance in the global market.

Segmentation Analysis

In 2023, Practice Management Software dominated the Veterinary Software Market with a market share of over 74.8%. This segment has become essential in streamlining operations within veterinary practices. It simplifies critical tasks such as appointments, billing, and patient records management. The adoption of user-friendly interfaces and efficient tools highlights the sector’s emphasis on improving administrative efficiency. This strong performance indicates that the need for workflow optimization and digital management systems remains a top priority in veterinary care delivery worldwide.

Imaging Software also played a significant role in shaping the veterinary software market in 2023. Although its share was smaller compared to Practice Management Software, it recorded notable growth. This segment supports accurate diagnosis by providing detailed imaging solutions for veterinary practices. The growing reliance on advanced diagnostic tools underlines the importance of precision in animal healthcare. By enhancing the quality of assessments, Imaging Software is steadily strengthening its position, complementing administrative systems in supporting comprehensive veterinary services.

The practice type analysis highlighted the Small Animals segment as the market leader, holding over 58% share in 2023. Growing pet ownership and rising awareness about animal healthcare drove strong adoption of advanced software solutions. Veterinary practices focusing on pets such as dogs and cats increasingly implemented digital tools for patient care and operations. The Mixed Animals segment also contributed significantly. Its adoption reflected the value of versatile software solutions capable of managing varied patient types, from small pets to large animals, within integrated veterinary practices.

In terms of end-use, the Hospitals/Clinics segment emerged as the largest contributor, securing more than 52.3% of the market share in 2023. The demand for comprehensive patient management and streamlined workflows strongly supported adoption in these facilities. Veterinary hospitals and clinics remain the first point of care for most pet owners, making efficient software solutions indispensable. Reference Laboratories also gained traction, with growing demand for precision diagnostics and data-driven testing. Together, these end-use segments reflect the industry’s reliance on technology to enhance both patient outcomes and operational efficiency.

Key Players Analysis

IDEXX Laboratories Inc. holds a leading position in the veterinary software market. The company is recognized for its advanced diagnostic and practice management solutions. Its strong focus on innovation has resulted in products that improve efficiency and clinical outcomes. IDEXX’s commitment to technology adoption continues to strengthen its market presence. By integrating digital tools with veterinary care, the company helps practitioners deliver high-quality services. This strategic approach positions IDEXX as a frontrunner, setting industry standards and influencing competitive dynamics in the global veterinary software industry.

Hippo Manager Software Inc. contributes significantly through its practice-focused solutions. The company is known for offering intuitive and user-friendly software. Its emphasis on simplicity ensures smooth adoption by veterinary professionals. Hippo Manager enhances workflow efficiency by reducing administrative burdens and streamlining patient data management. Its affordability makes it accessible to smaller practices, supporting wider adoption. By combining usability with strong functionality, the company has carved a distinct niche. This focus on accessibility and efficiency positions Hippo Manager as a growth driver within the veterinary software ecosystem.

Antech Diagnostics Inc., a subsidiary of Mars Inc., plays a vital role in shaping the industry. The company’s strength lies in its extensive diagnostic services and global network. Its robust portfolio supports accurate and timely veterinary care. Through continuous innovation, Antech advances diagnostic capabilities for practitioners worldwide. The backing of Mars Inc. provides access to significant resources, strengthening its competitive edge. Together, these capabilities position Antech as a critical market force. Its leadership in diagnostics highlights its contribution to advancing veterinary medicine and supporting the overall growth of the software sector.

FAQ

1. What is veterinary software?

Veterinary software is a digital tool that helps manage clinical, administrative, and financial activities in veterinary practices. It simplifies tasks like appointment scheduling, patient records, billing, and inventory management. Many solutions also offer telemedicine, reminders, and diagnostic imaging features. The software allows veterinarians to save time, reduce errors, and improve the overall quality of care. By automating routine tasks, veterinary professionals can focus more on patient treatment. It creates smoother workflows, enhances efficiency, and supports better client communication.

2. What are the key types of veterinary software?

Veterinary software comes in several types, each serving different needs. Practice management systems focus on scheduling, billing, and client communication. Imaging software stores and analyzes diagnostic scans such as X-rays and ultrasounds. Electronic health records track a pet’s medical history in one place. Telemedicine platforms allow remote consultations and follow-ups. Together, these tools provide a complete solution for both clinical and business operations. Each type improves efficiency, reduces errors, and helps veterinarians deliver better services to pet owners and animals.

3. What are the benefits of using veterinary software?

The benefits of veterinary software are significant for both clinics and pet owners. It improves accuracy in recordkeeping and reduces paperwork. Clinics can streamline tasks like appointments, billing, and reminders. This saves time and increases staff efficiency. Software also supports better communication with clients through updates and alerts. It helps control inventory and manage finances. By integrating all these processes, clinics provide faster and more reliable services. Ultimately, veterinary software improves workflows, enhances customer satisfaction, and delivers better patient outcomes.

4. Who are the typical users of veterinary software?

Veterinary software is mainly used by professionals and organizations involved in animal care. Veterinarians and staff in small clinics rely on it for scheduling, billing, and patient records. Large animal hospitals use advanced systems for diagnostic imaging and telemedicine. Universities and research centers also benefit from it to manage data and track studies. Specialty care providers use it for detailed health monitoring. The users range from small practices to large institutions, all seeking efficiency, accuracy, and better management of services.

5. How is veterinary software deployed?

Veterinary software is usually deployed in two main ways. On-premise solutions are installed directly on clinic computers and servers. They give more control over data but often require high upfront costs. Cloud-based solutions are becoming more popular because they are flexible and accessible from any device. They also offer real-time updates and lower maintenance needs. Cloud systems allow easy scaling and reduce IT burdens. Clinics choose deployment based on budget, size, and preferences, but cloud platforms are growing rapidly worldwide.

6. What challenges are associated with veterinary software adoption?

The adoption of veterinary software is often slowed by challenges. High upfront costs and training expenses discourage small clinics. Some practices struggle with data security concerns, especially in cloud-based systems. Integrating new software with older systems may also be difficult. Smaller clinics may resist change due to budget limits or lack of digital skills. In some regions, internet connectivity adds to the problem. Overcoming these challenges requires proper planning, staff training, and choosing solutions that match the clinic’s unique needs.

7. What is the size of the global veterinary software market?

The global veterinary software market is valued between USD 2154.6 Million as of 2022. It is forecast to grow at a compound annual growth rate (CAGR) of 8.8 percent between 2023 and 2030. Growth is driven by rising pet ownership, increased spending on animal healthcare, and the demand for digital solutions. More clinics are adopting electronic medical records and telemedicine platforms. As awareness of animal wellness increases, software adoption expands globally. This makes the veterinary software market highly promising.

8. What factors are driving market growth?

The veterinary software market is growing due to several key factors. Rising pet ownership and adoption are increasing the demand for animal healthcare services. Pet insurance is also gaining popularity, encouraging spending on advanced treatments. Clinics need digital solutions for better management, which drives adoption of software. Technology advancements like artificial intelligence in diagnostics and telemedicine further support growth. Additionally, the growing livestock population and the spread of zoonotic diseases raise the need for veterinary care. These factors boost market expansion worldwide.

9. Which regions dominate the veterinary software market?

North America holds the largest share of the veterinary software market due to high pet ownership and advanced healthcare infrastructure. The region has widespread adoption of digital veterinary solutions. Europe is another strong market, supported by government animal health initiatives and organized veterinary networks. Asia-Pacific is the fastest-growing region because of increasing disposable incomes, urbanization, and growth in livestock farming. Latin America is also emerging as a growing market. Each region contributes differently, but North America and Asia-Pacific show strong dominance.

10. Who are the major players in the veterinary software market?

The veterinary software market includes several global and regional players. Leading companies include IDEXX Laboratories Inc., Hippo Manager Software Inc., Antech Diagnostics Inc. (Mars Inc.), Esaote SpA, Henry Schein Inc., Patterson Companies Inc., ClienTrax, Digitail Inc, Vetspire LLC (Thrive Pet Healthcare), DaySmart Software, VitusVet, Nordhealth AS, and Other Key Players. These companies compete by offering innovative solutions, cloud-based platforms, and integration with diagnostic tools. Many are expanding through partnerships, mergers, and acquisitions. They focus on improving customer experience, adding telemedicine features, and enhancing efficiency. The market remains competitive, with established brands and new entrants driving digital adoption in veterinary practices.

11. What are the emerging trends in the veterinary software market?

Several emerging trends are shaping the veterinary software market. Cloud-based platforms are gaining popularity due to their flexibility and lower cost. Telemedicine is becoming an important service, especially after the rise of remote care. Artificial intelligence is being integrated into imaging for faster diagnostics. Mobile-friendly apps are also expanding access to services. In addition, mergers and acquisitions are increasing as companies seek growth and expansion. These trends show that the industry is moving toward digital innovation, efficiency, and improved patient care.

12. What challenges does the veterinary software market face?

The veterinary software market faces challenges that slow its growth. High costs of advanced systems make adoption difficult for smaller clinics. In developing regions, limited digital skills and low awareness create barriers. Cybersecurity concerns also impact the use of cloud-based systems. The market is highly fragmented, with a lack of standardization in solutions. Some clinics prefer traditional methods, resisting change. Connectivity issues in rural areas also limit adoption. Addressing these challenges requires affordable solutions, strong security measures, and better awareness campaigns.

13. What are the opportunities for future growth?

The veterinary software market offers several opportunities for future growth. Artificial intelligence and machine learning can support predictive healthcare and faster diagnostics. Telehealth adoption is expected to expand in rural and underserved areas. Cloud-based systems with mobile apps will create better accessibility and lower costs. Emerging markets in Asia-Pacific and Latin America provide strong potential due to rising incomes and growing pet adoption. The demand for integrated solutions is also increasing. These opportunities will continue to drive innovation and adoption globally.

Conclusion

The global veterinary software market is moving toward strong and steady growth, supported by rising pet ownership, increasing healthcare spending, and rapid digital adoption. Veterinary practices are shifting to advanced software for managing patient records, diagnostics, telemedicine, and daily operations, which improves efficiency and client satisfaction. Cloud-based solutions, artificial intelligence, and mobile platforms are making services more accessible and precise, strengthening both preventive and diagnostic care. The demand is expanding across companion animals and livestock, showing a versatile application of these tools. With supportive regulations, ongoing innovation, and growing awareness of animal health, veterinary software is set to remain a key driver of modern veterinary care and sustainable practice growth.

View More

Veterinary Software Market || Veterinary Diagnostic Imaging Market || Veterinary Lasers Market || Veterinary Microchips Market || Veterinary Services Market || Veterinary Telehealth Market || Veterinary Pain Management Market || Veterinary Telemetry Systems Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)