Table of Contents

Overview

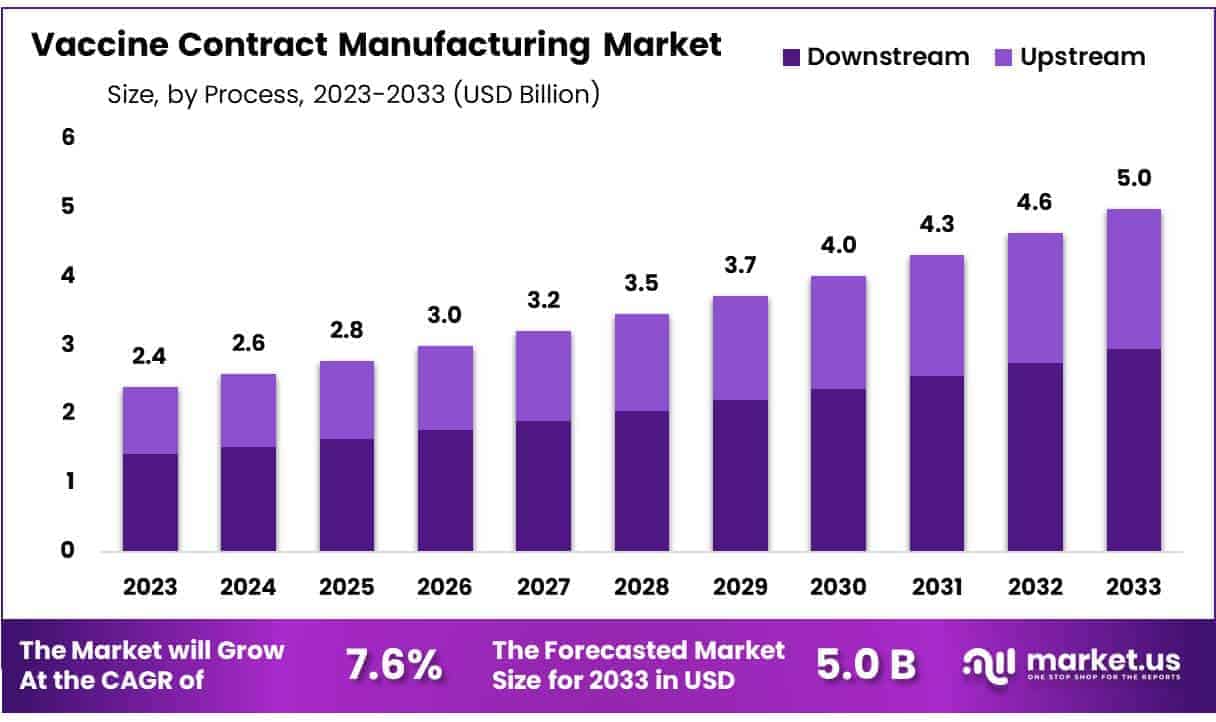

New York, NY – Oct 20, 2025 – Global Vaccine Contract Manufacturing Market size is expected to be worth around US$ 5.0 Billion by 2033 from US$ 2.4 Billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025 to 2033.

A leading biopharmaceutical solutions provider has announced the establishment of comprehensive Vaccine Contract Manufacturing services aimed at supporting global vaccine developers from early-stage development to large-scale commercial supply. This strategic initiative strengthens end-to-end biomanufacturing capabilities for viral vector, mRNA, recombinant protein, and conjugate vaccine platforms.

The facility integrates process development, technology transfer, GMP production, aseptic fill–finish, and quality assurance within a unified operational framework. With advanced single-use bioreactor systems, scalable production capacity, and automated quality controls, the service ensures regulatory compliance with FDA, EMA, and WHO guidelines.

The contract manufacturing model has been designed to reduce production timelines, optimize yield, and maintain consistent product quality across development stages. A robust digital infrastructure supports electronic batch records, data traceability, and real-time project monitoring for client transparency.

According to the company, the expansion of vaccine manufacturing capacity is a response to growing global demand for reliable supply chain solutions, particularly in pandemic preparedness and public health programs. The dedicated team of experts provides regulatory documentation, analytical testing, and logistics support for global distribution.

Initial production capacity will focus on clinical and commercial-scale vaccine batches, with future expansions planned to enhance output and technology diversity. The initiative underscores the company’s commitment to advancing vaccine accessibility and innovation through strategic biomanufacturing partnerships.

Key Takeaways

- Global Vaccine Contract Manufacturing Market size is expected to be worth around US$ 5.0 Billion by 2033 from US$ 2.4 Billion in 2024, growing at a CAGR of 7.6% during the forecast period 2025to 2033.

- Based on vaccine type, the market is categorized into inactivated vaccines, attenuated vaccines, RNA vaccines, subunit vaccines, and toxoid-based vaccines. Among these, attenuated vaccines dominated the segment, accounting for a 35.7% share in 2023.

- In terms of process, the market is classified into upstream and downstream operations. The downstream process segment held a significant portion of the market, representing 59.2% of total revenue.

- Considering the scale of operations, the market is segmented into preclinical, clinical, and commercial scales. The commercial segment emerged as the leading category, capturing 66.4% of the market share in 2023.

- By end use, the market is divided into human use and veterinary applications. The human use segment remained dominant, contributing 72.6% of the overall revenue.

- From a regional perspective, North America led the global vaccine contract manufacturing market, securing the largest share of 40.1% in 2023, driven by advanced biomanufacturing infrastructure and strong regulatory frameworks.

Regional Analysis

North America Leading the Vaccine Contract Manufacturing Market

North America held the dominant position in the global vaccine contract manufacturing market in 2023, accounting for the largest revenue share of 40.1%. The growth in the region is primarily attributed to the rising demand for large-scale vaccine production, supported by strategic collaborations between governments and pharmaceutical manufacturers.

A notable development contributing to this expansion was Moderna, Inc.’s announcement in April 2022 regarding the establishment of a state-of-the-art mRNA vaccine manufacturing facility in Quebec, Canada. This initiative, undertaken in collaboration with the Canadian government, substantially enhanced Moderna’s production capacity and strengthened the region’s vaccine manufacturing ecosystem. The urgent need for rapid vaccine production during the pandemic, along with technological advancements in mRNA platforms, has further accelerated the adoption of contract manufacturing services across North America.

In addition, significant investments in infrastructure expansion and increased government funding directed toward vaccine research and development have been key factors supporting regional market growth.

Asia Pacific Expected to Record the Fastest Growth Rate

The Asia Pacific region is projected to register the highest CAGR during the forecast period, driven by the growing demand for biologics and advanced therapies. In June 2023, FUJIFILM Corporation established a new commercial office in Tokyo to strengthen sales and customer support for its contract development and manufacturing services. This initiative aims to reinforce partnerships with pharmaceutical and biotechnology companies across Asia by offering customized manufacturing solutions.

Furthermore, the region’s expanding pharmaceutical industry, coupled with rising R&D investments and government initiatives to enhance local manufacturing capabilities, is expected to fuel sustained market growth. Efforts to reduce dependency on imports and promote self-sufficiency in vaccine production are anticipated to further strengthen Asia Pacific’s position in the global vaccine contract manufacturing landscape.

Emerging Trends

- Rapid Expansion of Regional Vaccine Capacity: Under the WHO’s Global Action Plan (GAP) for pandemic influenza, regional vaccine manufacturing capacity has expanded significantly. Total pandemic dose capacity increased from 338 million doses in 2015 to over 900 million by 2018–2019, highlighting rising investment in local production facilities, particularly within low- and middle-income nations.

- Growth of mRNA Technology Transfer Hubs: A dedicated mRNA Technology Transfer Hub was established in South Africa in 2021 to promote local vaccine innovation. By January 2025, technology transfer initiatives had extended to 15 countries, including six across Africa, strengthening local expertise and infrastructure for mRNA vaccine manufacturing.

- Expansion of WHO Prequalification for Local Sites: In 2024, WHO expanded its list of prequalified vaccine manufacturing facilities by adding a new site in Africa. This milestone enhanced regional producers’ global credibility, enabling them to meet international quality and regulatory standards.

- Ambitious Targets for African Vaccine Sovereignty: The African Vaccine Manufacturing Accelerator initiative was launched to boost self-sufficiency in vaccine production. The program aims for 60% of vaccines used in Africa to be manufactured locally by 2040, promoting resilience and reducing dependence on imports.

Use Cases

- Seasonal Influenza Vaccine Production: Contract Manufacturing Organizations (CMOs) have played a pivotal role in meeting annual influenza vaccine requirements. During the 2003–2004 flu season, approximately 87 million doses were produced through CMO partnerships, ensuring consistent vaccine supply for global immunization efforts.

- Global Pandemic Response via COVAX: During the COVID-19 crisis, COVAX utilized a coordinated network of contract manufacturing capacities. From February 2021 onward, more than 1.8 billion vaccine doses were distributed to 146 countries, demonstrating the indispensable role of CMOs in scaling up emergency vaccine production.

- mRNA Vaccine Technology Transfer and Scale-Up: Following its initial successful technology transfer to Biovac in September 2024, the mRNA Hub expanded its efforts by partnering with three additional manufacturers within the same year. This accelerated regional preparedness and strengthened global capacity for mRNA vaccine production.

Frequently Asked Questions on Vaccine Contract Manufacturing

- Why is vaccine contract manufacturing important?

It allows vaccine developers to accelerate production timelines, reduce capital investment, and access advanced manufacturing technologies, making it crucial for scaling up vaccine supply during pandemics or large immunization campaigns globally. - What are the main services offered by vaccine contract manufacturers?

These include process development, technology transfer, analytical testing, large-scale GMP manufacturing, aseptic filling, packaging, storage, and distribution support, ensuring end-to-end management from research to market-ready vaccine production. - What factors are driving growth in the vaccine contract manufacturing market?

Rising demand for vaccines, advancements in mRNA technology, government funding, and increased outsourcing by pharmaceutical companies are key factors propelling the growth of the global vaccine contract manufacturing market. - Which vaccine types are commonly produced through contract manufacturing?

Contract manufacturers commonly produce inactivated, attenuated, subunit, toxoid-based, and RNA vaccines, with attenuated vaccines currently holding a major market share due to their proven efficacy and widespread use in immunization programs. - Which region dominates the vaccine contract manufacturing market?

North America dominates the global market, accounting for the largest revenue share, owing to advanced biomanufacturing infrastructure, strategic industry collaborations, and strong regulatory frameworks supporting large-scale vaccine production. - Which region is expected to grow fastest in the forecast period?

The Asia Pacific region is projected to witness the fastest growth, driven by increasing R&D investments, government initiatives promoting local manufacturing, and the rapid expansion of the regional biopharmaceutical industry. - How does mRNA technology influence the vaccine contract manufacturing market?

The emergence of mRNA-based vaccines has transformed the market by creating demand for specialized manufacturing capabilities, advanced lipid nanoparticle formulation, and high-throughput production systems to meet global vaccine needs. - What is the future outlook for the vaccine contract manufacturing market?

The market outlook remains positive, with continuous investments in advanced manufacturing technologies, expansion of production capacities, and rising collaborations expected to drive steady growth and innovation through 2033.

Conclusion

The global vaccine contract manufacturing market is witnessing strong growth, driven by increasing demand for large-scale vaccine production, technological advancements, and strategic partnerships. Valued at US$ 2.4 billion in 2024, the market is projected to reach US$ 5.0 billion by 2033, growing at a CAGR of 7.6%.

North America leads the market, while Asia Pacific is expected to record the fastest growth. Expanding manufacturing infrastructure, rising government support, and the emergence of mRNA technology hubs are shaping the industry’s future, fostering innovation, self-sufficiency, and resilience in global vaccine supply chains.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)