Table of Contents

Overview

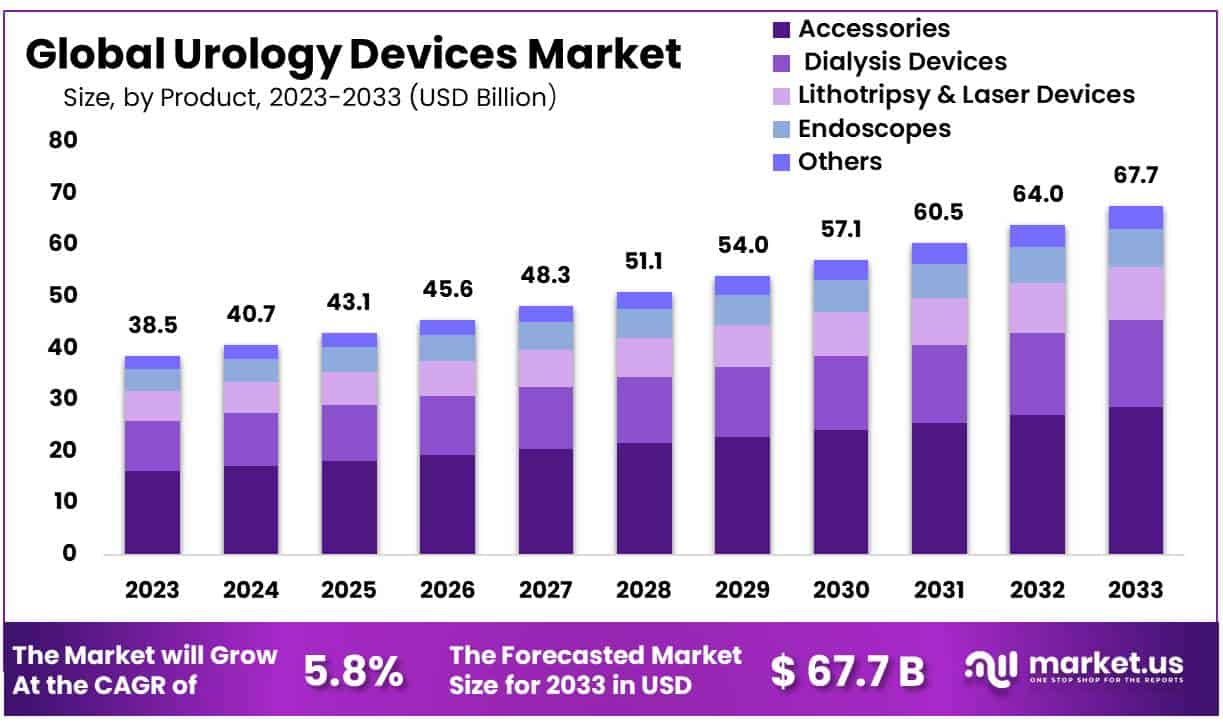

The Global Urology Devices Market is projected to reach around USD 67.7 billion by 2033, up from USD 38.5 billion in 2023. This growth will occur at a CAGR of 5.8% during the forecast period from 2024 to 2033. The increasing prevalence of urological diseases, rising healthcare spending, and ongoing technological advancements are shaping this trajectory. Aging demographics, especially in developed countries, continue to fuel demand for diagnostic and therapeutic solutions, as conditions like benign prostatic hyperplasia (BPH) and prostate cancer remain more common among older men.

The burden of urological conditions such as kidney stones, incontinence, and urologic cancers is rising globally. These disorders significantly affect quality of life, making diagnosis and treatment devices essential. Increased awareness campaigns and better access to healthcare services have enhanced early detection of prostate and bladder disorders. Early intervention not only improves patient outcomes but also expands the adoption of devices in clinical and outpatient settings. This rising disease burden is a consistent market driver across regions.

Technological innovation remains a critical growth enabler for this market. Minimally invasive and robotic-assisted procedures have gained wide acceptance due to their accuracy, faster recovery times, and reduced complications. The integration of smart sensors, advanced imaging, and AI-driven platforms into urology equipment is improving precision. Devices like AI-powered diagnostic systems and robotic surgical tools are transforming the sector. Their increasing adoption is expected to raise treatment efficiency, reduce hospital stays, and accelerate demand among both patients and healthcare providers.

The growing geriatric population further reinforces market expansion. Elderly individuals are more likely to experience bladder disorders, incontinence, and renal dysfunction. As life expectancy rises globally, the long-term demand for urology devices is expected to remain strong. This demographic shift underpins sustained revenue opportunities for diagnostic systems, catheters, and minimally invasive surgical tools. Together with healthcare policy reforms and insurance coverage, the expansion of senior healthcare services will continue to boost device utilization.

Emerging Opportunities and Strategic Trends

Healthcare expenditure continues to rise globally, creating favorable conditions for the adoption of advanced urology devices. Well-structured reimbursement schemes and broader health insurance coverage are improving affordability. Developed regions, particularly North America and Europe, are already benefiting from this trend. At the same time, emerging markets are catching up rapidly, supported by government-led healthcare programs and private investment. These financial frameworks not only improve patient access but also encourage hospitals and clinics to adopt cutting-edge diagnostic and therapeutic technologies.

Emerging economies present substantial untapped potential for market players. Asia-Pacific and Latin America are witnessing robust demand due to urbanization, improving healthcare infrastructure, and rising disposable incomes. Patients in these regions are increasingly seeking modern treatment options. Multinational device manufacturers are expanding their presence through partnerships and distribution networks to meet this demand. Addressing unmet medical needs in these markets will be central to future growth. Expansion strategies focused on affordability and accessibility are expected to strengthen global market reach.

The preference for minimally invasive procedures has become a defining trend in this sector. Patients and physicians increasingly favor these interventions due to reduced costs, faster recovery, and lower risk of complications. Devices such as lithotripters, ureteroscopes, and laser systems are being adopted more widely in both hospitals and outpatient centers. This shift in treatment patterns is generating consistent revenue growth, while encouraging device manufacturers to invest further in advanced minimally invasive solutions.

Strategic collaborations and R&D initiatives are shaping the competitive landscape. Industry leaders are pursuing mergers, acquisitions, and partnerships to strengthen their product portfolios and geographic presence. Continuous investment in innovation has led to the development of smart catheters, disposable cystoscopes, and AI-integrated diagnostic devices. These advancements enhance clinical outcomes and patient comfort. Companies that focus on innovation and collaboration are well positioned to gain competitive advantage. This ongoing cycle of R&D investment and market expansion is expected to sustain long-term industry growth.

Key Takeaways

- The global urology devices market is projected to reach USD 67.7 billion by 2033, growing from USD 38.5 billion in 2023.

- The market is expected to register a compound annual growth rate of 5.8% during the forecast period spanning from 2024 to 2033.

- Among product categories, the accessories segment remains most lucrative, capturing 42.4% share and driving substantial revenue contributions within the global urology devices market.

- In terms of applications, kidney diseases represent the leading segment, accounting for 39.5% share of the overall global urology devices market in 2023.

- Hospitals and ambulatory surgical centers dominate the end-user landscape, securing a 59.8% market share, thereby highlighting their critical role in urology device adoption.

- Geographically, North America leads the market, holding 33.7% share and generating USD 12.9 billion in revenue from urology devices in 2023.

- Increasing prevalence of kidney failures and chronic conditions worldwide continues to drive sustained demand for advanced urology devices across diverse healthcare settings globally.

Regional Analysis

North America is projected to dominate the global urology devices market. The region accounted for the largest share of 33.7%, representing USD 12.9 billion in revenue. Growth is driven by the rising number of patients diagnosed with kidney-related conditions who require consultation and treatment from urologists. The demand for specialized care, combined with higher awareness levels about urological health, continues to support the expansion of the market in this region.

The market in North America is further supported by the growing adoption of single-use cystoscopes. Rising preference for disposable instruments reduces infection risk and enhances patient safety. Additionally, the introduction of advanced technologies by key players has strengthened the regional market. Frequent launches of innovative devices are expanding treatment options, thereby improving clinical outcomes and increasing adoption rates. These factors position North America as the most lucrative region in the urology devices industry.

In comparison, Europe holds a smaller share of the market. However, it is anticipated to register a strong growth rate during the forecast period. The increase is attributed to the growing number of patients with urology-related disorders, including urolithiasis and bladder diseases. Rising prevalence of these conditions is creating demand for effective treatment solutions. Furthermore, ongoing technological advancements in the region are expected to improve healthcare delivery and fuel steady market growth across European countries.

Segmentation Analysis

The global urology devices market is segmented by product into dialysis devices, lithotripsy and laser devices, endoscopes, accessories, and other devices. Among these, the accessories segment holds the largest share, accounting for 42.4% of the global market. Growth in this segment is attributed to continuous product launches by key players and the increasing demand for catheters and dilators in urology clinics. The endoscopes segment is also expected to grow significantly, driven by the rising prevalence of urolithiasis and the adoption of disposable cystoscopies in developed countries.

By application, the market is categorized into urolithiasis, bladder disorders, kidney diseases, urethral malignancies, and others. The kidney diseases segment dominates the market with a 39.5% share, supported by the rising prevalence of end-stage renal disorders and the increasing demand for dialysis and minimally invasive surgeries. Bladder disorders are projected to grow considerably from 2023 to 2032, influenced by the aging population and higher incidence of diabetes and urinary infections. Furthermore, the demand for urology devices in hospitals and ambulatory centers is expected to contribute to sustained growth.

The market is also analyzed by end-user, which includes dialysis centers, hospitals and ambulatory surgical centers, and others. Hospitals and ambulatory surgical centers lead the market with 59.8% share, driven by the rising patient base with urological disorders. Increasing utilization of ureteroscopes and cystoscopies for diagnosis and treatment in these facilities further accelerates growth. Dialysis centers are anticipated to expand at a notable pace due to the growing number of patients with kidney failure. Additionally, rising awareness of dialysis and greater involvement of market players are likely to strengthen growth prospects in this segment.

Key Players Analysis

Emerging key players in the urology devices market are implementing multiple strategic policies to expand their global presence. These strategies include product launches, mergers, acquisitions, and collaborations. The emphasis is placed on entering foreign markets to strengthen their competitive edge. Increasing investments are being observed in both production capacity and distribution networks. The adoption of these growth-driven initiatives is expected to accelerate market development. Consequently, industry participants are focusing on positioning themselves as frontrunners in the forecast period.

Companies are investing heavily in research and development to diversify their product portfolios. Substantial spending is being directed toward technological innovations and product enhancements. By introducing advanced devices, these companies aim to cater to growing patient demand and medical professional requirements. The enhancement of product lines allows firms to address a wider range of urological conditions. The continuous pipeline expansion provides opportunities to secure larger market shares. As a result, the commitment to innovation has become a defining factor of competition.

Collaborations with healthcare providers, hospitals, and research organizations are being prioritized to improve market penetration. Strategic agreements and long-term contracts with regional partners support access to new geographies. Such alliances allow companies to combine technical expertise with localized market knowledge. Increased investments in R&D remain a primary strategy to deliver cost-effective and innovative solutions. This approach ensures improved treatment outcomes for patients. The integration of strong partnerships and innovation-driven growth strategies is anticipated to significantly strengthen the urology devices market.

Market Key Players

- Terumo Corporation

- Teleflex Inc.

- Stryker

- Bard

- Olympus Corporation

- Nxstage Medical Inc.

- Nipro Corporation

- Medtronic

- KARL STORZ GmbH & Co. KG

- Hollister Incorporated

- Fresenius Medical Care AG & Co. KGaA

- Dornier MedTech

- Cook Group

- ConvaTec Group

- Coloplast

- R. Bard Inc.

- Boston Scientific Corporation

- Baxter

- Braun AG

- Asahi Kasei Corp.

- Other Key Players

FAQ

1. What are urology devices?

Urology devices are medical tools used to diagnose and treat urinary tract and male reproductive system disorders. These include catheters, stents, endoscopes, and lithotripters. The devices help in managing kidney stones, urinary incontinence, prostate conditions, and other related diseases. Their role is critical in providing accurate diagnosis and effective treatment. With advancements in technology, urology devices are becoming more efficient, safer, and easier to use. They are used widely in hospitals, clinics, and specialized healthcare centers across the globe.

2. What are the main applications of urology devices?

The main applications of urology devices include managing kidney disorders, urinary tract infections, and urological cancers. They are also widely used for treating urinary incontinence, benign prostatic hyperplasia, and bladder control problems. These devices are vital for both surgical and non-surgical treatments. They enable physicians to perform minimally invasive procedures with higher precision. Patients benefit from quicker recovery, fewer complications, and better outcomes. The wide use of these devices highlights their importance in modern healthcare for urological and renal care.

3. Who are the end-users of urology devices?

The primary end-users of urology devices are hospitals, ambulatory surgical centers, and dialysis centers. These facilities depend on advanced tools to deliver specialized care for urology patients. Specialty clinics and research institutes also rely on these devices for diagnosis, treatment, and clinical trials. Their use ensures faster recovery and improved patient safety. End-users demand devices that are safe, effective, and easy to operate. With rising awareness, even home healthcare setups are starting to adopt urology devices for long-term patient management.

4. What types of urology devices are most commonly used?

The most commonly used urology devices include urinary catheters, ureteral stents, dialysis machines, and lithotripters. Catheters and stents are essential for managing urinary flow and obstructions. Dialysis equipment supports patients with kidney failure, while lithotripters are widely used for stone treatment. Other devices like cystoscopes and robotic systems are also gaining adoption. These tools are designed to improve accuracy, minimize complications, and enhance patient comfort. Their versatility makes them essential in hospitals, clinics, and outpatient care centers worldwide.

5. What technological advancements are influencing urology devices?

Technological advancements in urology devices focus on improving precision, safety, and patient outcomes. Robotic-assisted surgeries allow for minimally invasive procedures with faster recovery times. Smart catheters are being developed to reduce infection risks and improve monitoring. Laser-based technologies have improved stone management and treatment efficiency. Artificial intelligence in imaging and diagnostics is enabling faster and more accurate results. These innovations are transforming urology care by making devices more user-friendly and reliable. The trend indicates strong future growth in this field.

6. What is the size of the global urology devices market?

The Global Urology Devices Market size is expected to be worth around USD 67.7 Billion by 2033 from USD 38.5 Billion in 2023, growing at a CAGR of 5.8% during the forecast period from 2024 to 2033. Growth is supported by rising cases of urological conditions and greater demand for advanced devices. Increased awareness and preference for minimally invasive procedures also contribute. The market outlook remains positive with innovations and new product launches driving strong adoption in both developed and emerging markets.

7. What factors are driving market growth?

The urology devices market is growing due to several key factors. The rising prevalence of kidney stones, prostate disorders, and urinary incontinence is driving demand. An aging global population further increases the need for advanced care. Technological innovations such as robotic surgeries and smart devices boost adoption. The availability of minimally invasive options is improving treatment outcomes. Additionally, the increasing use of outpatient and home-based urology care solutions is encouraging wider use. Together, these factors create steady and sustainable market growth.

8. Which regions dominate the urology devices market?

North America currently dominates the global urology devices market. The region benefits from advanced healthcare systems, higher spending, and early adoption of new technologies. Europe is another leading region, supported by rising cases of kidney and bladder disorders. The Asia-Pacific region is expected to see the fastest growth over the forecast period. This is due to large patient populations, better healthcare investments, and growing awareness. Emerging economies are focusing on expanding healthcare infrastructure, which strongly supports market expansion.

9. Who are the key players in the urology devices market?

Key players in the urology devices market include Boston Scientific, Medtronic, Olympus, and Stryker. Other important companies are Siemens Healthineers, Karl Storz, Baxter, and B. Braun. These companies hold strong positions due to their wide product portfolios and global reach. They invest heavily in research and development to create advanced devices. Partnerships, mergers, and acquisitions are common strategies to expand market presence. Competition is intense, but innovation and product quality remain the main drivers of leadership in this market.

10. What challenges does the market face?

The urology devices market faces challenges that slow its growth. High costs of advanced robotic systems and devices limit access in many regions. The risk of infections, particularly with catheters, remains a concern. Complex regulatory approval processes delay product launches and adoption. In developing regions, limited awareness and affordability also hinder growth. Manufacturers must address these challenges through innovation, cost-efficient solutions, and improved training. Overcoming these barriers will ensure stronger market penetration and wider acceptance of advanced devices worldwide.

11. What trends are shaping the future of the market?

The urology devices market is shaped by strong emerging trends. Robotic and AI-powered surgical systems are improving precision and outcomes. Single-use devices are gaining popularity due to lower infection risks. Home healthcare adoption is expanding, especially for dialysis and urinary incontinence management. Sustainability and cost-effectiveness are becoming priorities for manufacturers. The integration of digital health solutions is also driving patient engagement and better monitoring. These trends indicate a future where technology, safety, and affordability will define the market direction.

Conclusion

The global urology devices market is set for steady expansion, driven by rising cases of urological diseases, an aging population, and ongoing innovations in minimally invasive and AI-enabled technologies. Growing awareness and wider healthcare access are improving early detection and treatment, boosting device adoption across hospitals and clinics. North America remains the leading market, while Asia-Pacific and Latin America are emerging as high-growth regions due to better healthcare infrastructure and rising incomes. Strategic collaborations, product innovations, and stronger reimbursement frameworks are further strengthening market opportunities. Overall, continuous demand for safer, efficient, and patient-friendly solutions will ensure sustained growth for the urology devices market.

View More

Urology Devices Market || AI In Neurology Operating Room Market || Neurology Market || Urology Imaging Systems Market || Botulinum Toxin-A in Urology Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)