Table of Contents

Overview

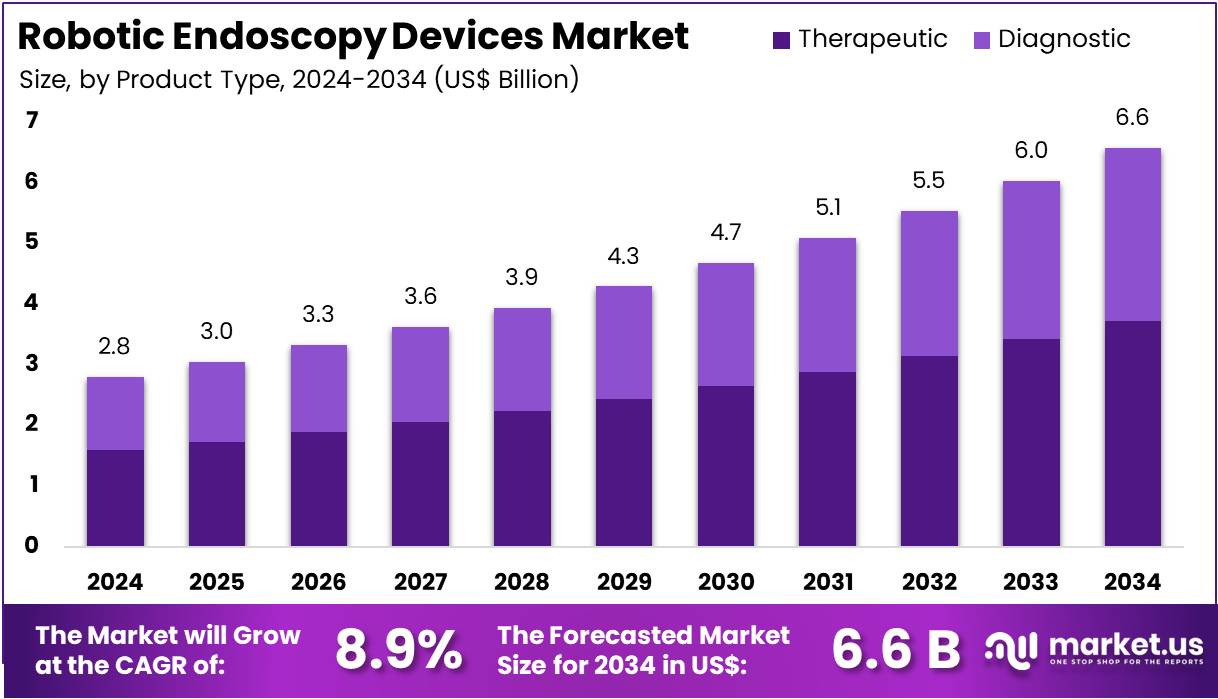

New York, NY – July 29, 2025 – The Robotic Endoscopy Devices Market size is expected to be worth around US$ 6.6 Billion by 2034 from US$ 2.8 Billion in 2024, growing at a CAGR of 8.9% during the forecast period 2025 to 2034.

The global robotic endoscopy devices market is experiencing substantial expansion, driven by increasing demand for precision-based minimally invasive procedures and rapid advancements in surgical robotics. Robotic endoscopy systems are redefining clinical outcomes by enabling enhanced visualization, superior maneuverability, and reduced patient recovery time across a range of gastrointestinal, urological, and respiratory interventions.

The integration of robotics with flexible endoscopes is enhancing procedural accuracy, especially in complex anatomies. These devices are increasingly being adopted in tertiary care hospitals, ambulatory surgical centers, and specialized clinics.

North America currently holds the largest market share, attributed to technological innovation, favorable reimbursement policies, and strong healthcare infrastructure. Meanwhile, Asia Pacific is expected to witness the fastest growth due to rising healthcare investment, increasing disease burden, and growing adoption of robotic-assisted surgeries.

Leading manufacturers are focusing on product innovation, AI-enhanced navigation, and strategic collaborations to expand their global footprint. The market is also supported by ongoing clinical trials and regulatory approvals that underscore safety, efficacy, and long-term benefits. The adoption of robotic endoscopy systems is poised to transform endoscopic procedures and improve patient care outcomes globally.

Key Takeaways

- In 2024, the global robotic endoscopy devices market generated a revenue of US$ 2.8 billion and is projected to reach US$ 6.6 billion by 2034, growing at a compound annual growth rate (CAGR) of 8.9% over the forecast period.

- By product type, the market is segmented into diagnostic and therapeutic devices. Among these, the therapeutic segment dominated in 2023, accounting for 56.7% of the total market share, driven by increasing demand for interventional endoscopic procedures.

- Based on application, the market comprises laparoscopy, colonoscopy, bronchoscopy, and others. The laparoscopy segment emerged as the leading application area in 2023, holding a market share of 38.5%, supported by its widespread use in minimally invasive surgeries.

- Regarding end users, the market is categorized into hospitals and outpatient facilities. Hospitals remained the primary end users, capturing the highest revenue share of 64.2%, owing to advanced infrastructure and higher adoption rates of robotic systems.

- Regionally, North America led the global market in 2023, contributing to 41.5% of the total revenue, attributed to strong healthcare infrastructure, favorable reimbursement frameworks, and early adoption of robotic technologies.

Segmentation Analysis

- Product Type Analysis: The therapeutic segment accounted for 56.7% of the market share, driven by the growing preference for minimally invasive surgical techniques. These devices offer enhanced precision, reduced recovery times, and improved surgical outcomes. Ongoing technological advancements have expanded the scope of complex interventions. Additionally, increased prevalence of chronic diseases, favorable reimbursement policies, and expanding insurance coverage are further supporting the adoption of robotic therapeutic systems across hospitals and surgical centers.

- Application Analysis: Laparoscopy represented 38.5% of the robotic endoscopy application market. Its dominance is attributed to rising demand for minimally invasive surgeries, which offer quicker recovery, fewer complications, and reduced patient discomfort. Robotic-assisted laparoscopy provides enhanced visualization and precision, benefiting procedures for gallbladder disease, appendicitis, and hernias. Surgeons favor these systems for their improved ergonomics and control. As more hospitals invest in minimally invasive surgical programs, laparoscopy is expected to retain a leading market position.

- End-user Analysis: Hospitals led the market with a 64.2% revenue share, driven by large-scale investments in advanced robotic technologies aimed at improving surgical outcomes and operational efficiency. Robotic endoscopy systems allow hospitals to reduce patient recovery time, increase procedural accuracy, and support higher patient throughput. Although outpatient facilities are expanding technologically, hospitals remain dominant due to their infrastructure, access to specialized surgical teams, and alignment with government-backed healthcare modernization and reimbursement initiatives.

Market Segments

By Product Type

- Diagnostic

- Therapeutic

By Application

- Laparoscopy

- Colonoscopy

- Bronchoscopy

- Others

By End-user

- Hospitals

- Outpatient Facilities

Regional Analysis

North America Leads the Robotic Endoscopy Devices Market

North America held the largest share of the robotic endoscopy devices market in 2023, accounting for 41.5% of total revenue. This dominance is attributed to the widespread adoption of minimally invasive diagnostic and therapeutic procedures and the region’s continual advancements in surgical technologies. Enhanced precision, surgeon dexterity, and high-definition visualization offered by robotic systems have made them increasingly popular among healthcare providers.

A key development reinforcing this trend was the FDA De Novo clearance granted to AnX Robotica’s NaviCam ProScan in January 2024 an AI-enabled colonoscopy system designed to improve diagnostic accuracy. This approval highlights the growing integration of artificial intelligence with robotic endoscopy, further elevating procedural efficiency and detection rates. The region’s strong inclination toward advanced, patient-centric surgical approaches continues to support robust market growth.

Asia Pacific Poised for Rapid Growth During the Forecast Period

The Asia Pacific region is projected to record the highest CAGR in the robotic endoscopy devices market over the forecast period. Growth is being driven by expanding investments in healthcare infrastructure, increasing demand for minimally invasive surgical solutions, and a rapidly aging population requiring safer and more efficient procedures.

Efforts to enhance early disease detection and improve procedural outcomes are accelerating the adoption of robotic systems. Additionally, the region’s thriving medical tourism sector particularly in countries such as India, Thailand, and Singapore is boosting demand for advanced surgical capabilities. As hospitals and specialized centers expand, and as healthcare professionals increasingly embrace robotic-assisted techniques, the market in Asia Pacific is expected to grow significantly in the coming years.

Emerging Trends

- Flexible and automated colonoscopy systems

- Next-generation robotic colonoscopy platforms are being developed that are softer, slimmer, and self-propelling. These reduce the need for manual pushing, thus enhancing patient comfort and reducing operator fatigue.

- Active capsule endoscopes with robotic guidance are advancing rapidly. They can be controlled externally, avoiding repeated manual navigation and improving diagnostic reach.

- Enhanced maneuverability and precision

- Robotic systems improve the maneuvering of endoscopes inside the gastrointestinal tract. This permits finer movement and better access to difficult areas compared to traditional scopes.

- These systems are increasingly integrating therapeutic tools (e.g. biopsy, clipping, ablation) to enable both diagnosis and treatment during the same procedure.

- Dose of automation and early autonomy

- Review of FDA-cleared surgical robots shows increasing autonomy levels (from assisted control to partial decision-making) in robot platforms. Robotic endoscopy systems are aligning with this trend, moving beyond manual control to semi-autonomous operation.

- Expansion of capsule robotics

- Robotic capsule devices are receiving regulatory approval. At least five wireless capsule models are FDA-approved for small bowel inspection. Next-generation versions are being designed to perform in-vivo actions (e.g. deploying clips or adhesives at bleeding sites).

- Increasing clinical adoption and procedural volume

- In the United States, physician payments and procedural volume for robot-assisted gastrointestinal procedures rose markedly: industry support to physicians grew from approximately $618 000 in 2015 to $1.54 million in 2019, and robotic GI surgery volume increased by an estimated 30 % in 2019 alone.

Use Cases

- Self-propelled colonoscopy for screening

- Robotic colonoscopes can advance through the colon without pushing.

- Example data: Volume of GI robotic procedures rose 30 % in 2019, indicating growing adoption for screening and diagnostic colonoscopy.

- Advantage: reduced discomfort, shorter procedure time, and lower sedation requirement.

- Robotic capsule performing therapeutic tasks

- Capsule endoscopes that can deploy a clip or apply a bio-adhesive patch in the small bowel.

- Regulatory update: five capsule models FDA-approved for bowel inspection. Next versions expected to add therapeutic capability.

- Numeric context: small bowel capsule systems already in clinical use; therapeutic capsule systems are entering early trials.

- Precision biopsy in narrow or tortuous anatomy

- Robotic flexible endoscopes allow fine control to access lesions in tight bends within GI tract.

- Clinical testing and pre-clinical models show improved reach and sampling accuracy over standard scopes.

- Semi-autonomous endoscopy assistance

- Platforms that support partial automation: the system can stabilize or guide itself while clinician supervises.

- Based on autonomy levels defined by FDA review of surgical robots (Levels 1–5).

- Use case: repetitive or steady maneuvers like navigation or positioning are delegated to the robot.

- Remote-assisted endoscopy and telesurgery(emerging proof-of-concept)

- While not yet widespread, there is documented experimental work where surgeons controlled an endoscope remotely with latency under 300 ms.

- Example: Swiss team performed pig endoscopy remotely using a PlayStation controller, transmitting control in real time (~5780 miles between sites).

- Potential: access to specialist care in remote or underserved regions, possibly even in space missions.

Conclusion

The global robotic endoscopy devices market is undergoing rapid transformation, driven by technological advancements, rising demand for minimally invasive procedures, and increased clinical adoption. With a projected CAGR of 8.9%, the market is expected to reach US$ 6.6 billion by 2034.

North America leads due to early technology adoption, while Asia Pacific is poised for the fastest growth. Innovations such as AI-assisted navigation, capsule robotics, and semi-autonomous systems are enhancing procedural efficiency and patient outcomes. As use cases expand across diagnostics and therapeutics, robotic endoscopy is set to become a standard in modern surgical and screening practices worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)