Table of Contents

Overview

The Global Teleradiology Software Market has been expanding due to a steady shift toward digital healthcare systems. Hospitals and clinics have been replacing manual workflows with digital imaging platforms. This transition has enabled faster access to diagnostic images and smoother data exchange. The use of cloud-based archiving has supported remote interpretation, which has increased the reliability of teleradiology workflows. As a result, demand for advanced software solutions has grown consistently across diverse healthcare environments.

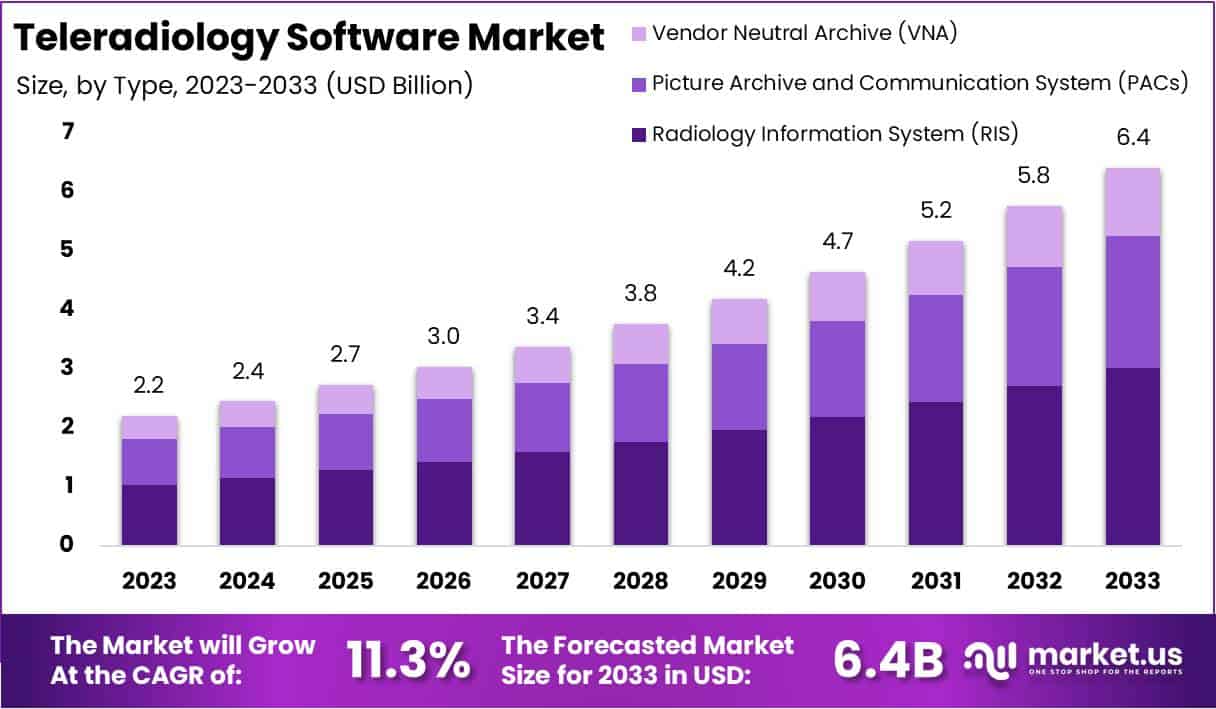

The Global Teleradiology Software Market size is expected to be worth around USD 6.4 Billion by 2033, from USD 2.2 Billion in 2023, growing at a CAGR of 11.3% during the forecast period from 2024 to 2033.

A major factor influencing market growth has been the rising shortage of radiologists in several regions. Many medical facilities have experienced gaps in diagnostic coverage. These shortages have led to slower reporting times and delays in patient evaluation. Teleradiology software has helped bridge these gaps by connecting sites with remote specialists. This capability has supported continuous reporting and improved patient management. Facilities have adopted these systems to ensure stable access to expert interpretation without time or location restrictions.

The increasing prevalence of chronic diseases has further contributed to the expansion of the market. Conditions such as cancer, cardiovascular disorders, and neurological illnesses require frequent diagnostic imaging. This rise in imaging volume has created a need for platforms that enable fast, secure, and coordinated image transfer. Teleradiology software has been used to streamline reporting, support multi-specialty collaboration, and enhance workflow efficiency. These improvements have strengthened the operational value of digital diagnostic systems in routine clinical use.

Technical advancements have also played an important role in market development. Improvements in internet bandwidth, cloud infrastructure, and cybersecurity have strengthened trust in remote radiology services. Faster data transmission and scalable storage have supported high-quality image sharing. Stronger security frameworks have ensured compliance with healthcare data standards. These developments have made teleradiology solutions dependable for large hospitals as well as smaller diagnostic centers seeking cost-effective digital transformation.

Cost optimization has remained an essential driver of adoption. Many healthcare providers have used teleradiology to reduce operational expenses and maintain continuous diagnostic coverage. Remote access to radiology expertise allows facilities to manage rising imaging workloads without major investment in on-site staffing. Supportive regulations for digital health and secure data exchange have further encouraged adoption. Overall, the market has been shaped by rising imaging demand, workforce shortages, and sustained advancements in digital healthcare infrastructure.

Key Takeaways

- The teleradiology software market was described as expanding steadily, rising from USD 2.2 billion in 2023 to an expected USD 6.4 billion by 2033 at 11.3% CAGR.

- The picture archive and communication system segment was identified as the leading contributor in 2023, capturing 47% of the total global revenue share.

- The web-based deployment model was noted as dominating the market, accounting for 39% of overall revenues during the same year.

- North America was recognized as the foremost regional market, generating more than 40% of global teleradiology software revenues in 2023.

Regional Analysis

North America led the global teleradiology software market in 2023. The region accounted for more than 40% of total revenue. This dominance was driven by a high burden of cancer and cardiovascular diseases. The United States reported nearly 1.9 million new cancer cases in 2023, which increased the need for efficient imaging solutions. Teleradiology software supported faster diagnosis, staging, and monitoring. The strong presence of major healthcare technology companies further strengthened adoption across hospitals and diagnostic centers.

The rising incidence of chronic diseases created continuous demand for advanced imaging platforms. Healthcare providers in North America relied on teleradiology software to improve diagnostic accuracy. The region also benefited from strong infrastructure and high digital readiness. Continuous investments in imaging technologies supported market expansion. The availability of skilled professionals enabled smooth integration of teleradiology systems. These combined factors sustained North America’s leadership position and created favorable conditions for long-term market growth within the global healthcare technology landscape.

Technological innovations have further accelerated market development in North America. For example, Royal Philips introduced its Ultrasound Workspace in March 2022 during the ACC Scientific Session. The platform unified cardiac ultrasound tools into one system. This improved workflow efficiency and enhanced clinical decision-making. Such advancements encouraged wider adoption of teleradiology solutions. Healthcare institutions increasingly focused on improving accuracy and reducing delays. As a result, innovative platforms strengthened diagnostic capabilities and supported the expansion of digital imaging across the region.

The Asia Pacific region is expected to record the highest growth rate during the forecast period. Rising cases of cancer and heart diseases increased the need for efficient imaging tools. A shortage of radiologists in countries such as India created strong demand for teleradiology services. Governments in the region promoted digital health initiatives, which improved adoption of advanced technologies. Modernizing healthcare systems further supported market growth. These developments enabled hospitals to improve diagnostic processes. The region is therefore positioned for substantial expansion in the coming years.

Segmentation Analysis

The picture archiving and communication systems segment accounted for 47% of global teleradiology software revenue. Its leading position is expected to continue during the forecast period. The demand for these systems has risen due to the growing burden of chronic diseases and an ageing global population. Teleradiology software enables medical images to be transmitted securely over long distances. This function supports remote interpretations by radiologists. Faster diagnosis and improved access to specialist expertise are achieved. These benefits strengthen the importance of PACS in clinical workflows.

Chronic diseases remain the primary drivers for the adoption of advanced teleradiology tools. In 2022, about 60% of American adults were reported to have at least one chronic illness. Conditions such as cancer, diabetes, and cardiovascular disease continue to cause most deaths in the United States. The high disease burden increases the need for timely diagnostic services. Teleradiology software supports this demand by enabling health facilities to address radiologist shortages. This capability ensures consistent, efficient, and accurate diagnostic support across locations.

Teleradiology platforms also enable collaborative care. Specialists can review and discuss cases in real time regardless of location. This cooperation improves diagnostic accuracy and speeds treatment decisions. The technology reduces geographical barriers and ensures wider access to radiology expertise. It enhances service quality in both urban and remote healthcare settings. As healthcare systems prioritise efficiency and accessibility, teleradiology has become essential. The shift toward digital imaging and remote diagnostics continues to reinforce its importance in modern clinical environments.

The web-based deployment segment held the largest share of 39% in 2023. Strong growth is expected due to high flexibility and scalability. These platforms operate through cloud computing, allowing providers to access applications through standard web browsers. This model removes the need for on-premises hardware and reduces maintenance costs. It integrates smoothly with systems such as EHRs, PACS, and HIS. Real-time access to images and patient data is provided. Radiologists can work remotely and offer timely interpretations, which supports rapid decision-making in critical situations.

Key Players Analysis

The teleradiology software market has been shaped by the active participation of major companies that aim to meet rising diagnostic imaging needs. Their efforts have focused on new product releases, technology upgrades, and regulatory approvals. These activities have strengthened their portfolios. Growth in imaging demand has encouraged firms to improve workflow efficiency. Strategic moves have also helped them widen their reach. This has supported steady adoption of advanced digital tools. As a result, competitive intensity has increased across global markets.

Several companies have introduced platforms that support faster image sharing and better collaboration. These tools have improved reporting accuracy and reduced turnaround times. Firms have invested in scalable cloud systems to support high data volumes. The move toward integrated solutions has created strong momentum. New partnerships between software providers and imaging centers have expanded access to digital services. Such developments reflect a shift toward flexible and cost-effective systems well suited for modern healthcare settings.

Key players such as Carestream Health, Telerad Tech, Comarch SA, and RamSoft, Inc. have strengthened their product offerings. They continue to focus on reliability, security, and compliance. Their systems support smooth communication between radiologists and healthcare teams. Companies like Radical Imaging LLC and OpenRad have invested in advanced technology. Their platforms offer improved workflow automation. Pediatrix Medical Group and Philips N.V. also hold strong positions. These firms rely on trusted brands and long clinical experience to maintain market relevance.

OpenRad’s Enterprise Edition launch in 2022 highlighted the importance of mobile fleet management and secure cloud workflows. The platform supports multiple organizations under one system. This shows a clear move toward centralized digital operations. Other firms, including smaller providers, have also expanded through targeted innovations. Their products meet specific workflow needs and niche demands. The market has benefited from these diverse offerings. As adoption increases, competitive strategies are expected to become even more focused.

Top Key Players in the Teleradiology Software Market

- Carestream Health

- Telerad Tech

- Comarch SA

- Medicentre Theme

- PERFECT IMAGING, LLC

- Impose Technologies Pvt Ltd.

- Radical Imaging LLC.

- OpenRad

- RamSoft, Inc.

- Koninklijke Philips N.V.

- Pediatrix Medical Group

- Other Key Players

Challenges

1. Concerns About Data Security

Adoption of teleradiology software has been slowed by strong concerns about data security. Medical images move across digital networks, which increases the risk of data leaks. Strict regulations such as HIPAA create pressure on healthcare providers to use secure systems. Many facilities hesitate to adopt new platforms because any breach can lead to legal and financial consequences. As a result, security gaps continue to limit wider acceptance of teleradiology solutions.

2. Limited Digital Infrastructure in Some Regions

Growth in the teleradiology software market has been affected by weak digital infrastructure in several regions. Low-bandwidth networks make image transmission slow and unreliable. This reduces the speed of diagnosis and disrupts efficient remote reporting. Healthcare facilities in rural or underserved areas face greater challenges. Limited investment in network upgrades and inconsistent connectivity continue to restrict the expansion of advanced imaging solutions.

3. Integration Issues With Existing Hospital Systems

Hospitals often rely on multiple systems such as PACS, RIS, and EHR platforms. Achieving smooth integration between these systems and teleradiology software is not always possible. Poor interoperability increases workflow complexity and results in operational delays. Staff often spend extra time correcting mismatched data or navigating disconnected interfaces. These issues reduce efficiency and discourage healthcare organizations from adopting new digital solutions.

4. Shortage of Skilled Radiologists

The global shortage of trained radiologists continues to affect the teleradiology software market. Many regions face uneven distribution of specialists, leading to heavy workloads for available radiologists. This causes delays in reporting and reduces the overall efficiency of remote diagnostic services. The imbalance between rising imaging demand and limited specialist availability remains a major barrier. As a result, software adoption is slowed by workforce gaps rather than technology limitations.

5. High Implementation and Maintenance Costs

High implementation costs pose a challenge for small and medium healthcare facilities. Advanced teleradiology platforms require significant initial investment in hardware, software, and secure networking tools. Ongoing maintenance expenses and frequent software upgrades add further financial strain. These costs discourage organizations with limited budgets from adopting modern solutions. As a result, price sensitivity remains a major factor affecting market penetration, especially in developing regions.

Opportunities

1. Rising Demand for Remote Diagnostics

The demand for remote diagnostics is increasing as more hospitals and clinics adopt digital imaging systems. Faster access to patient scans supports quick decisions in emergency care. Teleradiology software allows medical teams to receive expert reviews without delays. It also helps reduce waiting times and improves treatment accuracy. As care facilities focus on efficiency, the adoption of remote imaging services is expected to grow. This trend is creating strong opportunities in the market.

2. Growth in AI-Enabled Imaging Tools

AI-enabled imaging tools are becoming an important part of modern teleradiology platforms. These tools can help radiologists detect abnormalities quickly and support faster reporting. Automated features reduce the manual workload and improve overall accuracy. Hospitals are adopting AI systems to shorten diagnosis time and enhance patient outcomes. Continuous software upgrades are expanding the role of AI in imaging workflows. As adoption rises, AI-based tools are expected to create major growth opportunities in the sector.

3. Expansion of Healthcare Services in Rural Areas

Rural regions often lack qualified radiologists, creating long delays in diagnosis. Teleradiology software helps bridge this gap by allowing remote specialists to review medical images. The expansion of telehealth programs is improving access to care in underserved locations. Faster reporting helps rural clinics manage emergencies more effectively. Government support for digital healthcare is increasing the use of remote imaging systems. As connectivity improves, rural adoption is expected to create strong market opportunities.

4. Increasing Use of Cloud-Based Platforms

Cloud-based systems are becoming more popular because they allow hospitals to store and share large imaging files easily. These platforms reduce the need for expensive hardware and offer better flexibility. Radiologists can access patient data from any location, improving reporting speed. Cloud technology also supports smoother collaboration between medical teams. Its scalability makes it suitable for both small clinics and large hospitals. As cloud adoption accelerates, the market is expected to see strong growth.

5. Growing Need for 24/7 Reporting Services

Hospitals need round-the-clock reporting to manage large patient volumes and emergency cases. Teleradiology software supports continuous reporting by connecting global networks of radiologists. This ensures faster results even during night hours or peak seasons. The demand for uninterrupted workflows is pushing more facilities to adopt remote imaging solutions. Faster turnaround times help improve patient management. As healthcare systems aim for constant availability, this trend is expected to create steady market expansion.

6. Rising Investments in Healthcare Digitalization

Investments in digital healthcare solutions are growing across public and private sectors. These funds support the introduction of advanced teleradiology software, cybersecurity tools, and cloud solutions. Many hospitals are upgrading outdated systems to improve efficiency and patient care. Digitalization also enhances data security and supports the use of modern imaging tools. As spending increases worldwide, developers are focusing on more innovative software features. This environment is expected to create favorable opportunities for market growth.

Conclusion

The global teleradiology software market is expected to grow steadily as healthcare systems continue shifting toward digital imaging and remote diagnostics. Growth is being supported by rising imaging needs, a lack of radiologists, and strong adoption of cloud platforms. The demand for faster reporting, secure data exchange, and efficient workflows has strengthened the role of teleradiology in hospitals and diagnostic centers. Advances in digital infrastructure and AI tools are improving accuracy and workflow management. Despite challenges related to security, integration, and cost, the long-term outlook remains positive. Continuous investments in digital health are expected to support wider adoption and enhance the value of teleradiology solutions across global healthcare settings.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)