Table of Contents

Overview

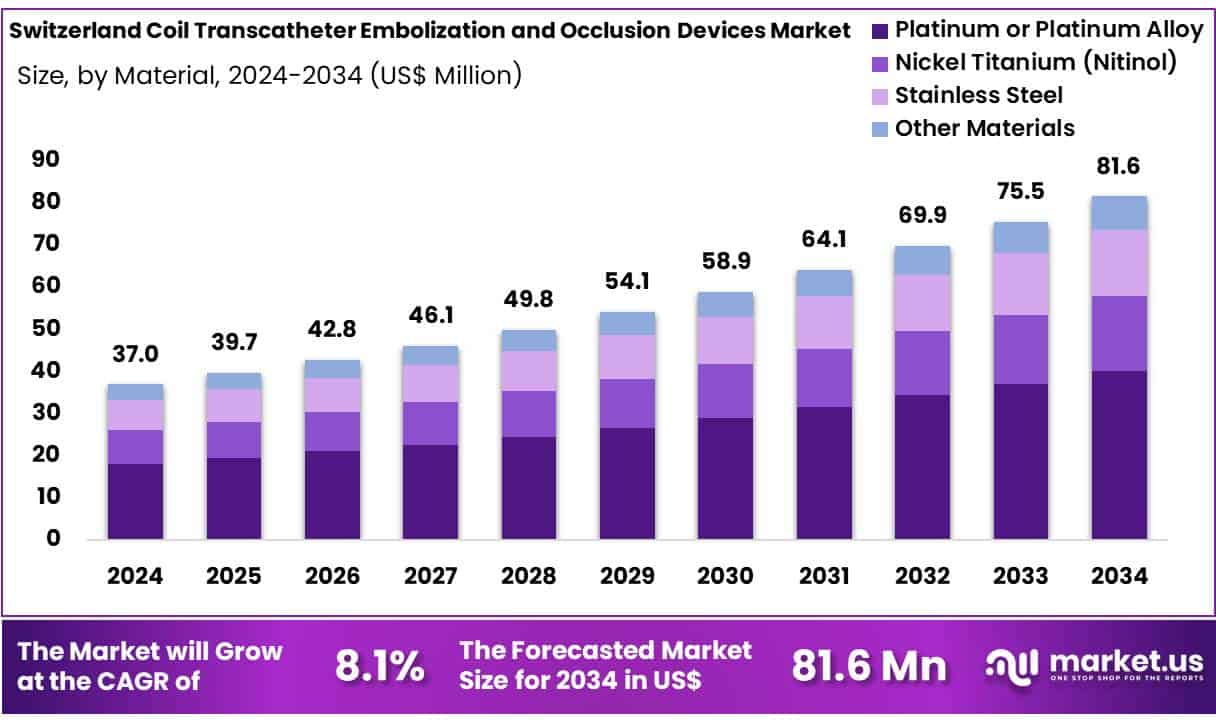

New York, NY – June 10, 2025 – The Switzerland Coil Transcatheter Embolization and Occlusion Devices Market size is expected to be worth around US$ 81.6 Million by 2034 from US$ 37.0 Million in 2024, growing at a CAGR of 8.1% during the forecast period from 2025 to 2034.

The Switzerland market for coil-based transcatheter embolization and occlusion (TEO) devices is experiencing measured growth, driven by advancements in interventional radiology, an aging population, and rising incidence of aneurysms and arteriovenous malformations. Hospitals across Zurich, Geneva, and Basel are increasingly adopting coil embolization procedures for the treatment of cerebral aneurysms, gastrointestinal bleeding, and vascular malformations.

The Swiss Federal Office of Public Health (FOPH) notes a steady annual increase in neurovascular interventions, particularly among adults aged 55 and above. Coil embolization is preferred due to its minimally invasive nature, precise occlusion control, and reduced postoperative complications. Both bare platinum and detachable coils are widely used, with demand increasing for bioactive and hydrogel-coated variants that improve clotting efficiency.

Local procurement policies, combined with Switzerland’s high healthcare expenditure per capita, have ensured broad availability of advanced coil systems. Leading hospitals such as University Hospital Zurich and Lausanne University Hospital have integrated these devices into routine endovascular care. In addition, continuous physician training in interventional radiology is enhancing clinical adoption.

Regulatory support from Swissmedic and cross-border collaboration with EU medical device standards continue to streamline market entry for new technologies. As chronic disease rates increase and healthcare infrastructure evolves, the Switzerland TEO devices market is expected to maintain positive growth momentum through 2030.

Key Takeaways

- In 2024, the Switzerland coil transcatheter embolization and occlusion devices market was valued at USD 37.0 million. It is projected to grow significantly and reach USD 81.6 million by 2034, expanding at a compound annual growth rate (CAGR) of 8.1% during the forecast period.

- Among product types, the detachable coils segment emerged as the dominant category, accounting for 53.2% of the total market revenue in 2024. This reflects a growing preference for precise and repositionable embolization tools in complex interventional procedures.

- In terms of application, hemorrhage control held the largest share of the market, capturing 26.9% of total revenue. This is primarily driven by the increasing demand for minimally invasive techniques in acute bleeding scenarios across trauma and surgical settings.

- By material, platinum and platinum alloy-based coils led the segment with a 40.9% revenue share, attributed to their superior visibility under fluoroscopy and excellent biocompatibility in vascular occlusion.

- On the basis of end-user, the hospitals segment maintained a leading position, representing 58.9% of total market revenue. This dominance is due to the high adoption of advanced embolization procedures across major Swiss healthcare institutions, supported by comprehensive radiology infrastructure and experienced interventional teams.

Segmentation Analysis

- Product Type Analysis: In 2024, the detachable coils segment held the largest share of 53.2% in Switzerland’s coil transcatheter embolization and occlusion devices market. These coils are favored for their precision, safety, and ability to reposition before final deployment. Widely used in treating aneurysms and vascular tumors, they offer enhanced control during procedures. The rise of bioactive and hydrogel-coated coils, combined with growing neurovascular disease incidence, supports strong market demand and technological advancements in the detachable segment.

- Procedure Type Analysis: The hemorrhage control segment led the Switzerland market in 2024, accounting for 26.9% of revenue share. This dominance is attributed to the urgent need for effective, minimally invasive solutions for acute bleeding caused by trauma, gastrointestinal issues, and postpartum complications. Coil embolization offers targeted vessel occlusion, reducing blood loss while preserving healthy tissue. Increasing trauma cases, liver diseases, and the preference for faster recovery times have driven the adoption of these procedures across hospitals and emergency care units.

- Material Analysis: Platinum and platinum alloy coils captured 40.9% of the Swiss market in 2024 due to their superior radiopacity, flexibility, and long-term stability. These materials allow precise placement under fluoroscopy, critical in complex embolization procedures. Their durability and biocompatibility enhance treatment safety. Alloy combinations with nitinol or tungsten further improve performance by boosting elasticity and vessel adherence. With rising use in neurovascular and hemorrhage-related treatments, platinum-based coils remain central to innovation in embolization device manufacturing.

- End-User Analysis: Hospitals accounted for 58.9% of the Swiss market in 2024, making them the dominant end-user of coil embolization devices. This is due to their high patient volume, availability of advanced imaging systems, and experienced interventional radiology teams. Hospitals frequently perform complex vascular interventions, particularly for aneurysms and hemorrhages. Enhanced reimbursement systems, infrastructure investments, and integration of hybrid operating rooms have further strengthened the hospital segment, positioning it as the primary hub for cutting-edge embolization treatments.

Market Segments

Product Type

- Detachable Coils

- Pushable Coils

- Other Product Types

Procedure Type

- Hemorrhage Control

- Vascular Occlusion

- Aneurysm Treatment

- Tumor Embolization

- Other Procedure Types

Material

- Platinum or Platinum Alloy

- Nickel Titanium (Nitinol)

- Stainless Steel

- Other Materials

End-User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics

- Research and Academic Institutes

Market Opportunity: Rise in Medical Tourism

The rising trend of medical tourism is opening new opportunities for the Switzerland coil transcatheter embolization and occlusion devices market. Patients from various countries are increasingly choosing destinations that offer high-quality yet cost-effective interventional care.

Nations such as India, Thailand, and Mexico provide embolization procedures for aneurysms, hemorrhages, and vascular disorders at a fraction of the cost seen in developed economies. These countries attract international patients with advanced facilities, experienced medical professionals, and short waiting times. Comprehensive treatment packages—including diagnostics, procedures, and recovery care—are further increasing demand for innovative embolization technologies.

Macroeconomic and Geopolitical Impact

The Switzerland market is significantly affected by macroeconomic and geopolitical dynamics that influence production, pricing, and device availability. Economic stability and increased healthcare spending in high-income countries support faster adoption of embolization devices. In contrast, developing regions often face budget constraints and limited reimbursement policies, hindering access to advanced interventional procedures.

Additionally, geopolitical tensions, trade barriers, and tariffs can disrupt the global supply chain, particularly in sourcing platinum and other key components. Currency volatility, inflation, and inconsistent regulations across borders also delay approvals and slow market expansion.

Latest Market Trends

The Switzerland coil embolization and occlusion devices market is undergoing dynamic transformation due to the rise of minimally invasive techniques and the growing burden of vascular diseases. There is increasing preference for non-surgical embolization using advanced coils with enhanced flexibility, visibility, and clotting efficiency.

Innovations such as hydrogel-coated and bioactive coils are improving outcomes by accelerating vessel occlusion and reducing procedure time. Moreover, AI-integrated imaging and automated deployment systems are enhancing precision and safety. Growing awareness, regulatory support, and a focus on personalized vascular care are driving wider clinical adoption across both developed and emerging healthcare markets.

Emerging Trends

- Centralized, High-Volume Treatment: Management of aneurysmal subarachnoid hemorrhage has been centralized in eight specialized neurovascular centers under the Swiss Study on Subarachnoid Hemorrhage (Swiss SOS). This model supports consistent use of endovascular coiling techniques and enables robust data collection for outcome analysis. From 2009 to 2014, 1 787 consecutive aSAH patients were recorded, with a nationwide incidence of 3.7 per 100 000 persons per year.

- Dominance of Endovascular Coiling: Endovascular coil embolization—including balloon-assisted approaches—has become the primary treatment modality. In ruptured intracranial aneurysms, coiling (with or without balloons) was used in 97.8 % of cases, reflecting a clear shift from surgical clipping toward less invasive options.

- Adoption of Adjunctive Device Technologies: Beyond simple coiling, advanced adjunctive techniques are on the rise. In unruptured aneurysms, flow diversion was applied in 11.6 % of cases, flow disruption in 6.9 %, and stent-assisted coiling in 7.8 %. This diversification of device usage indicates growing confidence in tailored, hybrid approaches to complex vascular anatomies.

- Data-Driven Outcome Prediction and Quality Improvement: Nationwide registry data have enabled development of predictive models for functional outcomes after coiling interventions. High follow-up rates (91.3 % at one year) and detailed discharge metrics (independent living in 58.8 % of cases) facilitate continuous quality improvement and device optimization across centers.

Use Cases

- Treatment of Ruptured Intracranial Aneurysms: Coil embolization is the standard of care for ruptured aneurysms in Switzerland. Between 2009 and 2014, 1 787 patients with aSAH underwent endovascular treatment. Of these, 97.8 % received coiling (with or without balloon assistance). At one year, 58.8 % of patients achieved an independent functional state (mRS 0–2), and case fatality was 22.1 %.

- Management of Unruptured Aneurysms: For unruptured intracranial aneurysms, device selection is tailored to aneurysm morphology. In a multicenter cohort, flow diversion was used in 11.6 % of cases, flow disruption devices in 6.9 %, and stent-assisted coiling in 7.8 %. Simple coiling remained predominant, illustrating the versatility of coil technology across varying aneurysm complexities.

- Aortic Pseudoaneurysm Embolization: In cases where open or endograft repair is contraindicated, coil embolization of aortic pseudoaneurysms has been successfully applied. Reported case series demonstrate complete thrombosis of the aneurysmal cavity with no peri-procedural complications, highlighting coil embolization as a safe alternative in selected vascular beds.

- Peripheral Vascular Embolization: Coil devices are increasingly used for embolization of visceral and peripheral arteries—such as in gastrointestinal bleeding or post-surgical vascular lesions. Published clinical reports indicate technical success rates above 95 % and low rates of non-target embolization, underscoring the reliability of coils in diverse anatomical applications.

Conclusion

The Switzerland coil transcatheter embolization and occlusion devices market is poised for steady expansion, supported by technological advancements, high clinical adoption, and increasing demand for minimally invasive vascular interventions. Favorable reimbursement frameworks, a robust hospital infrastructure, and evolving treatment protocols are reinforcing the dominance of coil-based therapies, particularly for neurovascular and hemorrhagic conditions.

Emerging trends such as the centralization of care, adoption of adjunctive devices, and data-driven quality improvement further highlight Switzerland’s leadership in embolization practices. With a projected CAGR of 8.1% through 2034, the market is expected to remain a key focus in the country’s interventional radiology landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)