Table of Contents

Overview

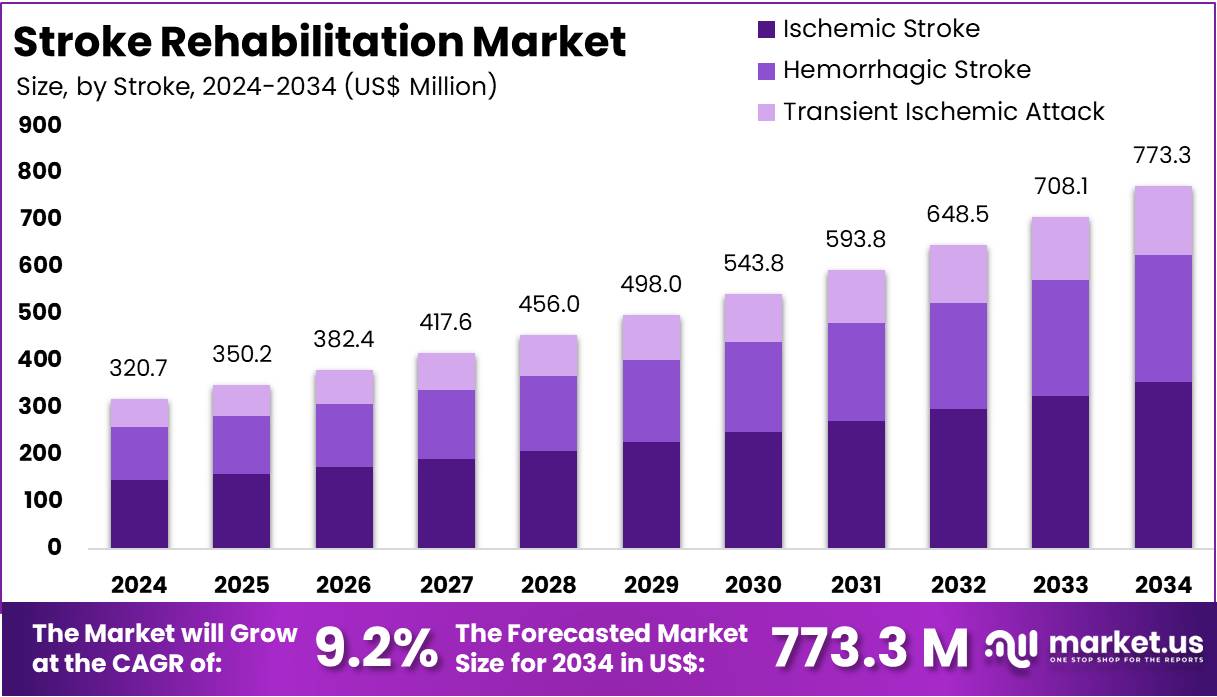

New York, NY – August 20, 2025: The Global Stroke Rehabilitation Market is projected to grow from US$ 320.7 million in 2024 to US$ 773.3 million by 2034, registering a CAGR of 9.2% during the forecast period. North America remains the largest regional market, holding a 45.5% share with a market value of US$ 145.6 million in 2024. Growth is fueled by the rising burden of stroke, as 11.9 million new cases and 93.8 million people living with stroke were reported in 2021. Stroke also accounts for a significant proportion of global cardiovascular deaths, underscoring the critical role of rehabilitation in healthcare systems.

Key Growth Drivers

The ageing population is a fundamental driver. By 2050, the global number of people aged 60 years and above will double to 2.1 billion, directly increasing stroke incidence and post-stroke disability rates. Alongside this, improved survival after acute stroke contributes to growing rehabilitation needs. In the United States, 795,000 people experience a stroke annually, while stroke prevalence rose 7.8% between 2011–2013 and 2020–2022. Early rehabilitation starts in hospitals and extends to outpatient and home settings, ensuring consistent demand for physiotherapy, occupational therapy, and speech-language therapy services.

Unmet Need and Policy Support

A large unmet need is recognized at the global level. The World Health Organization (WHO) estimates that 2.41 billion people, or one in three worldwide, could benefit from rehabilitation services—a 63% increase since 1990. To address this, policy momentum is strong. In May 2023, the World Health Assembly adopted Resolution WHA76.6, emphasizing the integration of rehabilitation at all levels of healthcare under universal health coverage. These developments encourage national governments to scale services, expand financing, and strengthen rehabilitation pathways, supporting industry growth across developed and emerging economies.

Clinical Guidelines and Care Models

Updated clinical guidelines are reinforcing demand for earlier and more intensive interventions. The NICE guideline on stroke rehabilitation (2023) highlights systematic assessment and goal-directed therapy across care settings. Similarly, the US National Institutes of Health promotes comprehensive, multidisciplinary rehabilitation to restore independence. Coverage reforms also support tele-rehabilitation and hybrid models. In the US, Medicare telehealth flexibilities extend until September 30, 2025, enabling payment for physiotherapy, occupational therapy, and speech-language therapy delivered remotely. These reforms promote equitable access, strengthen continuity of care, and expand opportunities for technology-driven rehabilitation services.

National Programs and Technology Adoption

National health systems are prioritizing post-stroke recovery pathways. NHS England promotes integrated stroke delivery networks and stronger community rehabilitation under its Long Term Plan and the National Stroke Service Model. In Australia, government data confirm high use of inpatient and community rehabilitation. Technology adoption also accelerates market expansion. Virtual reality, robotics, and other devices are increasingly recognized as effective adjuncts when they increase therapy intensity. Clinical evidence and policy guidance support the inclusion of these technologies in regulated care pathways, strengthening procurement of advanced rehabilitation solutions globally.

Geographic Opportunities and Outlook

Market growth will be reinforced by demand in low- and middle-income countries where access gaps are widest. WHO data show most stroke deaths and disability-adjusted life years occur in lower-income regions, where rehabilitation services remain limited. This creates a strong public health imperative and an opportunity for scalable, community-based, and technology-enabled care models. In summary, the sector’s expansion is driven by four reinforcing factors: the ageing survivor population, strong policy commitments, expanding reimbursement frameworks, and wider clinical adoption of intensive and technology-assisted rehabilitation. These dynamics ensure sustained long-term growth across inpatient, outpatient, and home-based care settings.

Key Takeaways

- The global stroke rehabilitation market is anticipated to grow from US$ 320.7 million in 2024 to US$ 773.3 million by 2034.

- A strong compound annual growth rate (CAGR) of 9.2% is expected between 2025 and 2034, indicating steady expansion opportunities for stroke rehabilitation solutions.

- In 2024, the ischemic stroke category held dominance in the stroke segment, contributing more than 78.3% of the total global market share.

- Hospitals represented the leading end-user category in 2024, capturing over 27.4% of the overall stroke rehabilitation market share across different regions.

- North America led the regional landscape in 2024, holding a 45.5% share valued at approximately US$ 145.6 million in stroke rehabilitation.

Regional Analysis

North America dominated the stroke rehabilitation market in 2024, holding over 45.5% share with a value of US$ 145.6 million. This leadership was supported by strong healthcare infrastructure and the early adoption of innovative technologies. The integration of AI-based and robotic systems increased acceptance rates. Specialized rehabilitation centers also played a crucial role. Early diagnosis and multidisciplinary care improved recovery outcomes. Together, these factors strengthened regional dominance and made North America the global leader in stroke rehabilitation services and solutions.

The high incidence of stroke cases has been a major driver. In the United States, more than 795,000 people suffer a stroke every year, with one occurring every 40 seconds. Canada reported about 108,700 cases annually, or one every five minutes, according to the Heart and Stroke Foundation. These figures highlight the growing at-risk aging population. Consistent demand for advanced stroke rehabilitation devices and services is being created, as patients require long-term recovery solutions and access to effective treatment pathways.

Economic capacity further supports market expansion. In 2023, U.S. healthcare spending reached US$ 13,432 per person, far above other high-income nations. Canada’s per-capita spending was US$ 6,319 (USD PPP). Stroke costs in the U.S. totaled US$ 56.2 billion between 2019 and 2020, including treatment, medicines, and lost productivity. This heavy financial burden has created a strong need for effective rehabilitation. Hospitals and payers are focusing on cost-effective solutions to reduce complications, enhance patient outcomes, and ensure efficient recovery processes across the stroke rehabilitation continuum.

Government initiatives and reimbursement frameworks have also fueled adoption. Medicare covers inpatient rehabilitation under defined clinical criteria. Certified Inpatient Rehabilitation Facilities are nationally listed, improving patient access and treatment standards. Acute-to-rehabilitation pathways have lowered 30-day mortality rates to 4.3% in the U.S., compared to the OECD average of 7.8%. Investments in tele-rehabilitation and home-based therapies are also increasing. Future growth is expected through personalized rehabilitation plans, which will improve outcomes, expand access in remote areas, and enhance overall market penetration.

Segmentation Analysis

In 2024, ischemic stroke maintained a dominant position in the stroke rehabilitation market, capturing more than 78.3% share. This was attributed to the higher occurrence of ischemic strokes compared with other types. Restricted blood flow to the brain often results in significant physical and mental impairment. Recovery is prolonged and demands a multidisciplinary approach. Physical rehabilitation, occupational therapy, and speech-language interventions remain critical. Hospitals and specialized centers are expanding services, while innovations in therapy techniques and greater awareness continue to drive growth in this segment.

Hemorrhagic stroke occupied a smaller share of the rehabilitation market but demonstrated steady growth. This condition, caused by bleeding in or around the brain, leads to severe neurological complications. Rehabilitation requirements are intensive, with many patients needing long-term inpatient care. Neurorehabilitation programs remain essential for regaining lost functionality. Although hemorrhagic strokes are less common, improved survival rates have expanded the pool of patients requiring treatment. Rising awareness of treatment options and the expansion of stroke care services are expected to support gradual demand growth in this segment.

The transient ischemic attack (TIA) segment accounted for the smallest share in stroke rehabilitation. Often referred to as a “mini-stroke,” TIA results from a temporary blockage of blood flow to the brain. Symptoms resolve quickly, so rehabilitation needs are comparatively lower. However, these events serve as early warning signs for future strokes. Preventive rehabilitation, lifestyle modifications, and patient education programs are critical in this category. Growth is moderate but supported by preventive healthcare initiatives, rising screening programs, and increasing adoption of early intervention strategies across healthcare systems.

Hospitals held the leading position in the end-user segment in 2024, with a 27.4% share of the stroke rehabilitation market. Their dominance was supported by advanced medical infrastructure and access to skilled professionals. Hospitals provided immediate post-stroke care along with comprehensive rehabilitation services. Specialty clinics contributed notably by offering focused, patient-centered rehabilitation plans. Ambulatory centers gained traction with cost-effective outpatient solutions, while long-term care centers supported patients with severe disabilities. Additionally, home care settings with tele-rehabilitation tools and community health facilities ensured greater access to rehabilitation, particularly in underserved areas.

Key Market Segments

By Stroke

- Ischemic Stroke

- Hemorrhagic Stroke

- Transient Ischemic Attack

By End-User

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

- Long-Term Centers

- Home Care Settings

- Rehabilitation Centers

- Others

Key Players Analysis

Amal XR is positioned as a provider of virtual reality rehabilitation targeting neuro and musculoskeletal conditions. Its gamified VR modules support upper and lower limb practice, balance, and cognition, with clinician dashboards enhancing monitoring. The solution is designed for hospitals, rehab centers, and home use, aiming to improve adherence in post-acute care. A strategic edge is its cost-efficient and scalable deployment. However, wider clinical validation is still required, and adoption in public healthcare may be delayed by lengthy procurement cycles.

Cognimate emphasizes hand function and cognitive rehabilitation with a sensorized smart glove and therapeutic games. Its strength lies in addressing the underserved fine-motor rehabilitation segment, supported by neuroplasticity, biofeedback, and gamification. Recurring revenue potential comes from clinic-to-home continuity. FDA listing enhances credibility, but scaling requires independent trial evidence and payer pathway alignment. Drop Digital Health adds AI-driven tele-rehabilitation through its K•HERO® platform, while HCAH leverages multi-city presence for large-scale out-of-hospital care. Growth relies on evidence, regulatory milestones, and integration into reimbursement models.

Top Leading Market Key Players

- Amal XR

- ARN Labs

- Cognimate

- Drop Digital Health

- Health Care at Home India Pvt. Ltd.

- IRegained Inc.

- Jefferson Health

- Jogo Health

- Pneumbra Inc.

- Restorative Therapies

- Saebo Inc.

- TeleRegain

- UT Southwestern Medical Center

- Zynex Medical Inc.

Key Drivers, Restraints, Opportunities, and Trends

Rising Global Stroke Burden Driving Rehabilitation Demand

Stroke cases are increasing worldwide, creating strong demand for rehabilitation services. According to the World Stroke Organization (2022), there are over 12.2 million new strokes each year, with more than 101 million people living with the condition. Stroke remains a leading cause of death, accounting for 6.5 million fatalities annually. Healthcare systems are therefore emphasizing post-stroke care to improve survival rates and reduce long-term disability. This rising burden directly fuels growth in stroke recovery and rehabilitation markets globally.

Aging Population Accelerating Market Growth

The growing elderly population is a major contributor to stroke rehabilitation demand. The United Nations’ World Population Prospects 2024 confirms that people aged 65 years and older are increasing rapidly. Older adults face higher stroke risks due to age-related health decline and chronic cardiovascular conditions. Survivors frequently require long-term care and structured rehabilitation. As this demographic expands, the demand for recovery services is set to rise significantly, creating opportunities for both public and private healthcare providers.

Lifestyle-Related Health Risks Increasing Stroke Incidence

Unhealthy lifestyle patterns are raising the global stroke burden. The World Health Organization (2022) highlights that 16% of adults are obese, and 43% are overweight, both major stroke risk factors. High prevalence of hypertension, diabetes, and smoking further increases vulnerability. Poorly managed blood pressure alone is a major contributor to strokes worldwide. These persistent risk factors ensure a steady flow of patients into rehabilitation services, creating sustained market demand for structured recovery programs and integrated care solutions.

Large Rehabilitation Gap in Low- and Middle-Income Nations

Access to rehabilitation remains uneven across regions. In many low- and middle-income countries, over half of stroke survivors lack proper rehabilitation support. Limited infrastructure, insufficient trained specialists, and funding gaps delay recovery and worsen disabilities. This unmet demand presents opportunities for investment in capacity-building. In the United States, the scale is also significant, with 162,890 stroke deaths reported in 2021. Cardiovascular disease consumes 12% of U.S. health expenditures, keeping rehabilitation at the forefront of healthcare priorities.

High Cost of Advanced Rehabilitation Restricting Adoption

The high expense of rehabilitation remains a key barrier to market expansion. Inpatient post-stroke care in the U.S. averages $40,243, with outpatient services costing $27,426. Rehabilitation alone can exceed $70,000 annually. Advanced technologies such as robotic-assisted systems cost approximately $150,000, excluding maintenance. These costs discourage adoption, particularly in low-resource settings. Hospitals and clinics face financial challenges in integrating advanced therapies, limiting patient access to innovative recovery solutions and creating disparities in treatment availability.

Limited Reimbursement Policies Slowing Market Penetration

Reimbursement structures remain inadequate, hindering wider adoption of advanced rehabilitation solutions. In many countries, insurance schemes cover only basic therapy and exclude expensive technologies. Patients often bear out-of-pocket expenses for advanced treatments such as exoskeleton training, costing $18 per session, or robotic therapy at $3,952 per patient. This cost burden restricts utilization and adoption of advanced solutions, reducing the market’s growth potential. The lack of comprehensive reimbursement policies continues to be a critical restraint in the global stroke rehabilitation industry.

AI and VR Integration Creating Significant Opportunities

Artificial intelligence (AI) and virtual reality (VR) are transforming stroke rehabilitation. Studies from 2022–2024 confirm that VR-enhanced therapy produces superior functional outcomes compared to conventional methods. AI applications enable personalized care, predictive triage, and adaptive therapy. Machine learning models can forecast recovery outcomes within 72 hours of stroke admission, supporting tailored interventions. Combining AI with VR-driven tele-rehabilitation has improved engagement, consistency, and scalability of home-based programs. These innovations represent a major commercial opportunity in the rehabilitation market.

Growing Trend Toward Home-Based Rehabilitation Programs

Home-based digital rehabilitation is a rising trend in stroke recovery. Tele-rehabilitation (TR) platforms and remote monitoring allow patients to undergo therapy at home while staying connected with healthcare providers. Clinical studies confirm that TR offers non-inferior results compared to in-clinic therapy, with strong adherence rates. Remote monitoring with wearables enables real-time tracking of progress and timely interventions. Although adoption is still modest—only 2.5% of patients had TR sessions in 2020–2021—this model shows high growth potential and aligns with digital health transformation.

Conclusion

The stroke rehabilitation market is set for steady expansion as rising stroke cases, longer life expectancy, and policy support create a strong demand for recovery services. Hospitals, specialty clinics, and home-based care models are driving wider access, while technologies such as robotics, AI, and virtual reality are making rehabilitation more effective and scalable. Despite cost and reimbursement challenges, the focus on early intervention, digital platforms, and community-based programs is strengthening recovery pathways. With aging populations, growing awareness, and supportive government initiatives, the sector is positioned for sustained growth, offering opportunities across advanced and emerging healthcare systems.

View More

Stroke Diagnostics And Therapeutics Market || Stroke Management Market || Acute Ischemic Stroke Therapeutics Market || Neurorehabilitation Devices Market || Rehabilitation Equipment Market || Physical Therapy Rehabilitation Solutions Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)