Table of Contents

- Introduction

- Editor’s Choice

- Still Wine Market Overview

- Average Revenue Per Capita Generated from Still Wine Statistics

- Still Wine Consumption Volume Statistics

- Still Wine Price Statistics

- Winery Sales Channels Statistics

- Demographics of Still Wine Consumers Statistics

- Consumer Choice Factors in Selecting Wine

- Key Trends Related to Still Wine Owners Statistics

- Supply Difficulties in the Wine Industry

- Recent Developments

- Conclusion

- FAQs

Introduction

Still Wine Statistics: Still wine, derived from fermented grape juice, is a staple alcoholic beverage produced from various grape varieties.

It includes red, white, rosé, and orange wines, each with distinct flavors and characteristics. Red wines, crafted from dark grapes, offer a range of flavors, from fruity to earthy, while white wines, made from green or yellow grapes, exhibit fruity and floral notes.

Rosé wines, produced with limited skin contact from red grapes, feature a pink hue and diverse flavor profiles. Fermented with grape skins, orange wines boast an amber color and fuller body.

Terroir, encompassing factors like soil, climate, and winemaking practices, shapes the wine’s unique attributes. Still wine pairs well with various foods, making it a versatile and beloved choice for wine enthusiasts worldwide.

Editor’s Choice

- The global still wine market revenue is projected to reach USD 363.8 billion in 2028.

- Rosé wine is projected to reach USD 23.3 billion in 2024 and USD 31.3 billion by 2028. White wine is forecasted to rise to USD 86.4 billion in 2024 and USD 107.1 billion by 2028.

- By 2025, offline sales are anticipated to drop to 96.8%, with online sales increasing to 3.2%. A trend that is expected to remain consistent through 2027.

- The global still wine market revenue varies significantly by country. With the United States leading the market with a revenue of USD 31,230 million.

- By 2028, the prices are projected to reach USD 16.65 for red wine, USD 10.65 for rosé wine, and USD 12.39 for white wine.

- According to wine industry statistics, the highest winery sales channel is the tasting room, accounting for 29% of total sales.

- Among individuals aged 21 to 34 years, who constitute 25.2% of the total population, 19.8% are wine consumers.

Still Wine Market Overview

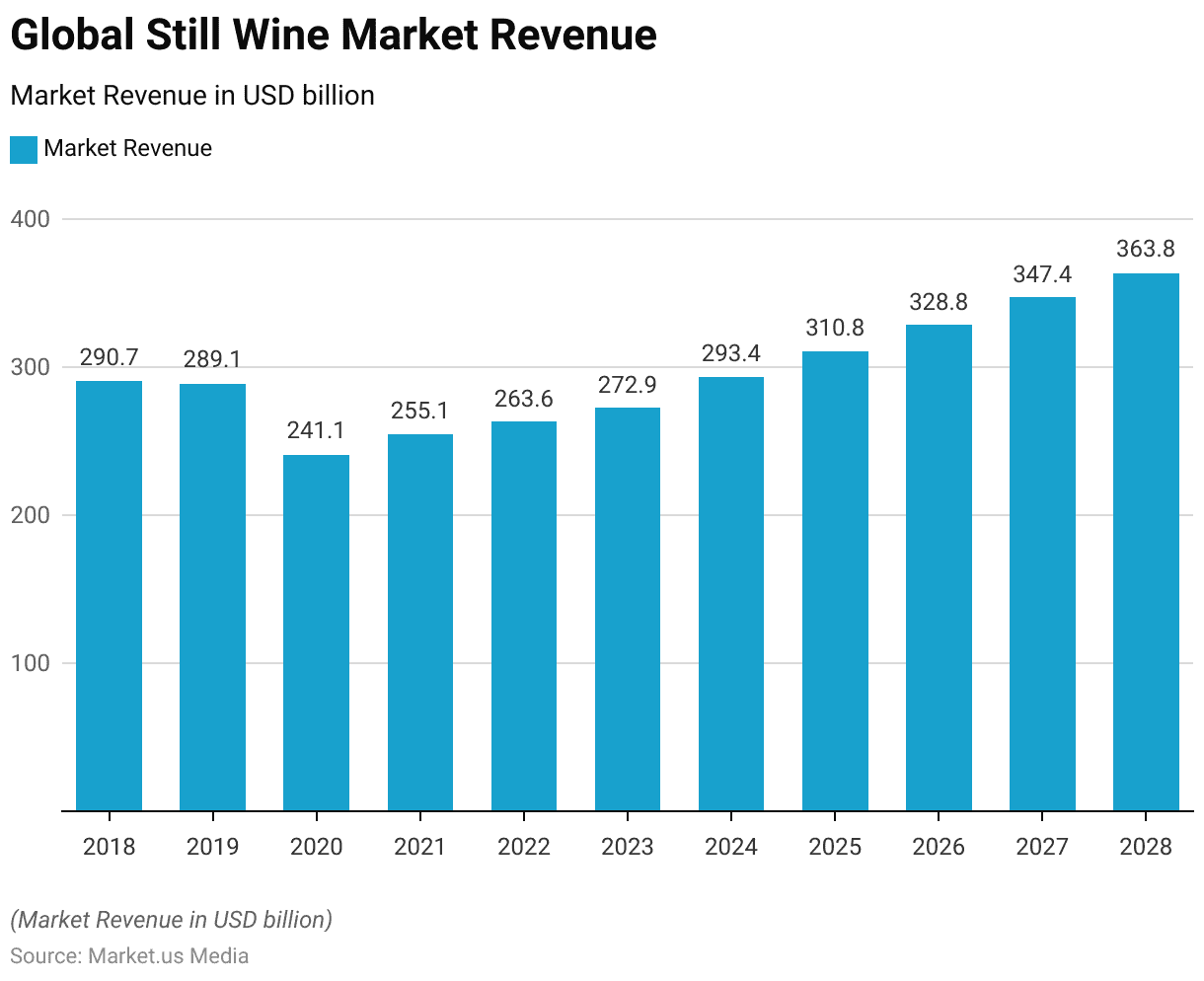

Global Still Wine Market Size Statistics

- The global still wine market has exhibited a fluctuating revenue trend over the past years.

- In 2018, the market revenue stood at USD 290.7 billion, slightly declining to USD 289.1 billion in 2019.

- A significant drop was observed in 2020, with revenues falling to USD 241.1 billion. Largely attributed to the impacts of the COVID-19 pandemic.

- However, the market demonstrated a recovery in subsequent years. With revenue rising to USD 255.1 billion in 2021 and further increasing to USD 263.6 billion in 2022.

- The upward trend continued, reaching USD 272.9 billion in 2023.

- Projections indicate that the market will continue to grow, with expected revenues of USD 293.4 billion in 2024, USD 310.8 billion in 2025, USD 328.8 billion in 2026, USD 347.4 billion in 2027, and USD 363.8 billion in 2028.

(Source: Statista)

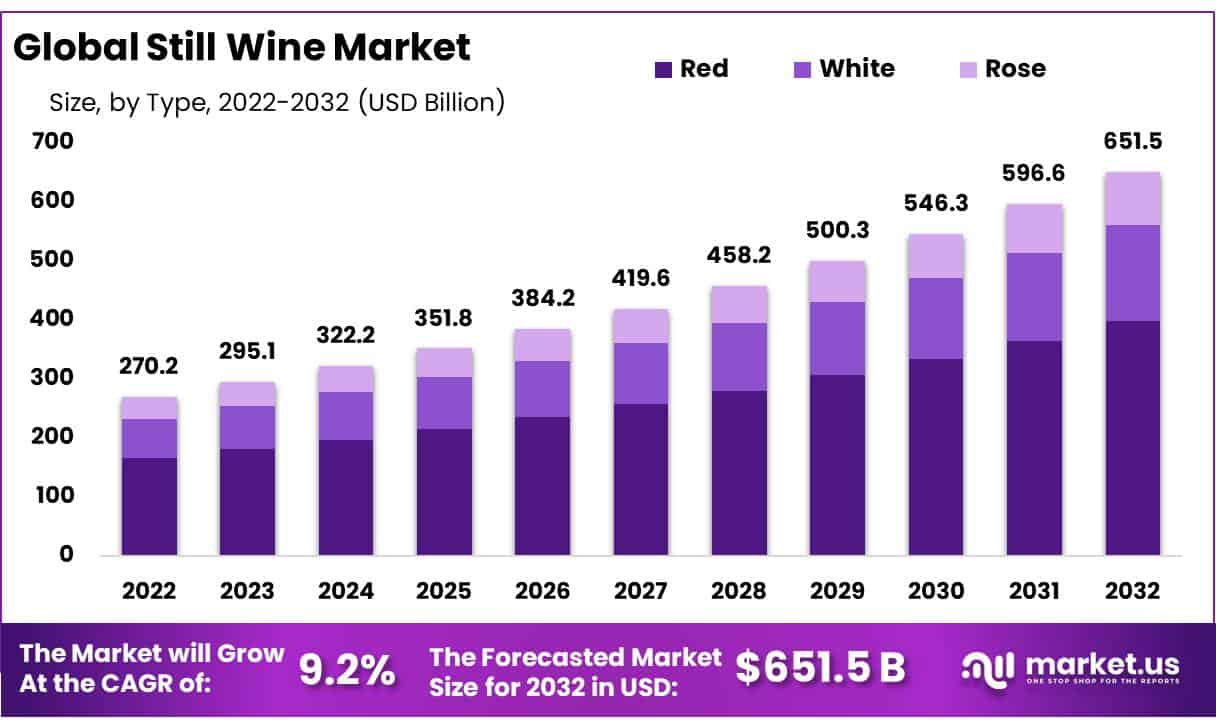

Still Wine Market Size – By Type Statistics

- The global still wine market, segmented by type, has shown varied revenue trends across red, rosé, and white wines from 2018 to 2028.

- In 2018, red wine led the market with a revenue of USD 184.2 billion. Followed by white wine at USD 85.4 billion and rosé wine at USD 21.1 billion.

- In 2019, red wine revenue slightly decreased to USD 182.2 billion. White wine saw a marginal increase to USD 85.9 billion, and rosé wine remained stable at USD 21.0 billion.

- The impact of the COVID-19 pandemic in 2020 caused a significant revenue drop across all types. With red wine at USD 152.7 billion, rosé wine at USD 17.7 billion, and white wine at USD 70.7 billion.

- The market began to recover in 2021, with revenues for red, rosé, and white wines rising to USD 161.2 billion, USD 18.8 billion, and USD 75.1 billion, respectively.

- This upward trend continued through 2022 and 2023, with red wine reaching USD 165.6 billion and USD 170.9 billion, rosé wine at USD 19.9 billion and USD 21.1 billion, and white wine at USD 78.1 billion and USD 80.9 billion.

- Future projections indicate continued growth, with red wine expected to generate USD 183.8 billion in 2024, USD 194.0 billion in 2025, and USD 225.4 billion by 2028.

- Similarly, rosé wine is projected to reach USD 23.3 billion in 2024 and USD 31.3 billion by 2028. White wine is forecasted to rise to USD 86.4 billion in 2024 and USD 107.1 billion by 2028.

(Source: Statista)

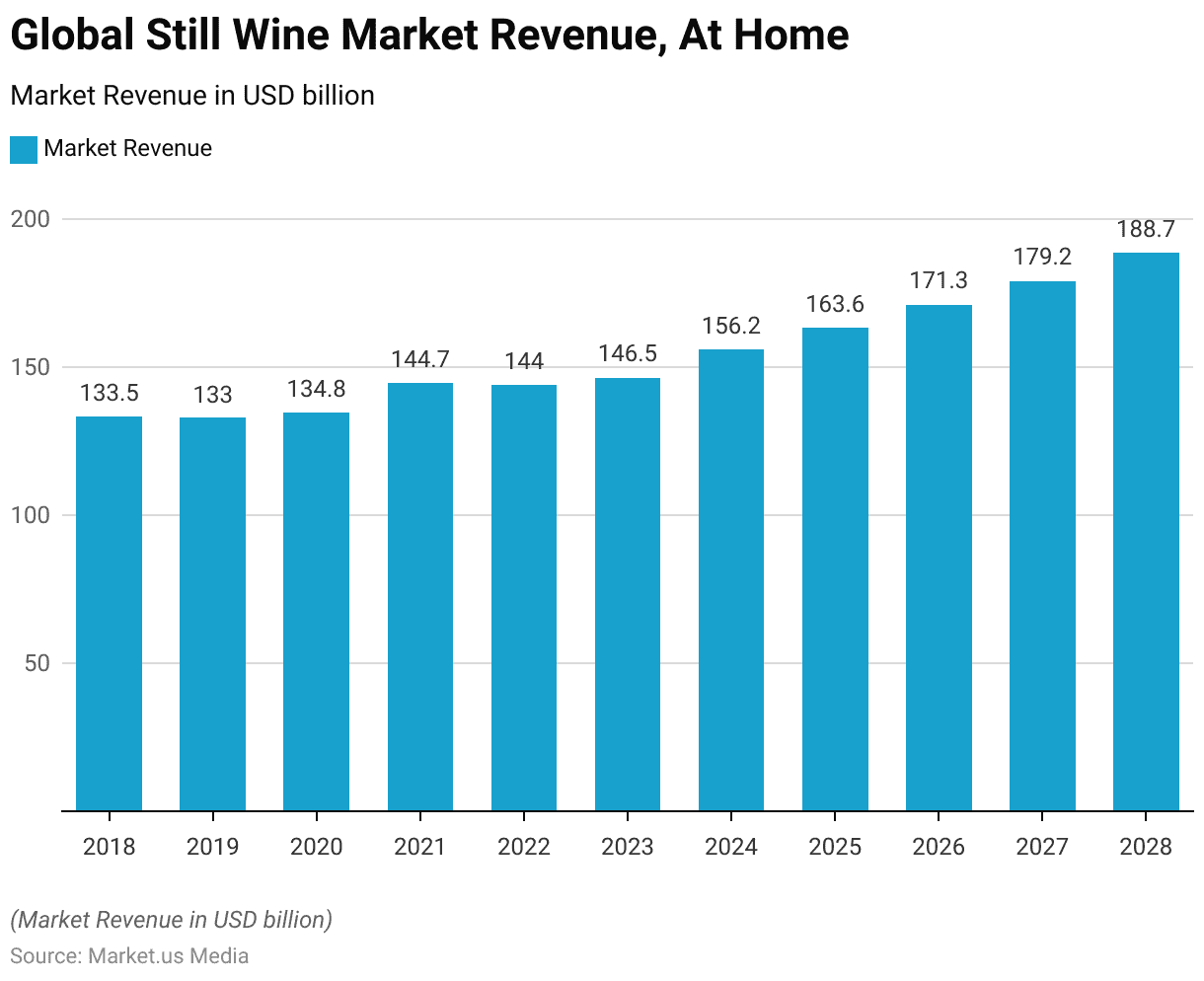

Global Still Wine Market Revenue – At-Home Statistics

- The revenue generated from global still wine sales at home, such as in supermarkets and convenience stores, has shown a steady growth trend from 2018 to 2028.

- In 2018, the revenue was USD 133.5 billion, slightly decreasing to USD 133.0 billion in 2019.

- Despite the challenges posed by the COVID-19 pandemic. The at-home wine market experienced a minor increase in 2020, reaching USD 134.8 billion.

- The market saw significant growth in 2021, with revenue climbing to USD 144.7 billion. Followed by a slight decrease to USD 144.0 billion in 2022.

- In 2023, the revenue increased to USD 146.5 billion.

- Projections for the coming years indicate continued growth, with expected revenues of USD 156.2 billion in 2024, USD 163.6 billion in 2025, USD 171.3 billion in 2026, USD 179.2 billion in 2027, and USD 188.7 billion by 2028.

(Source: Statista)

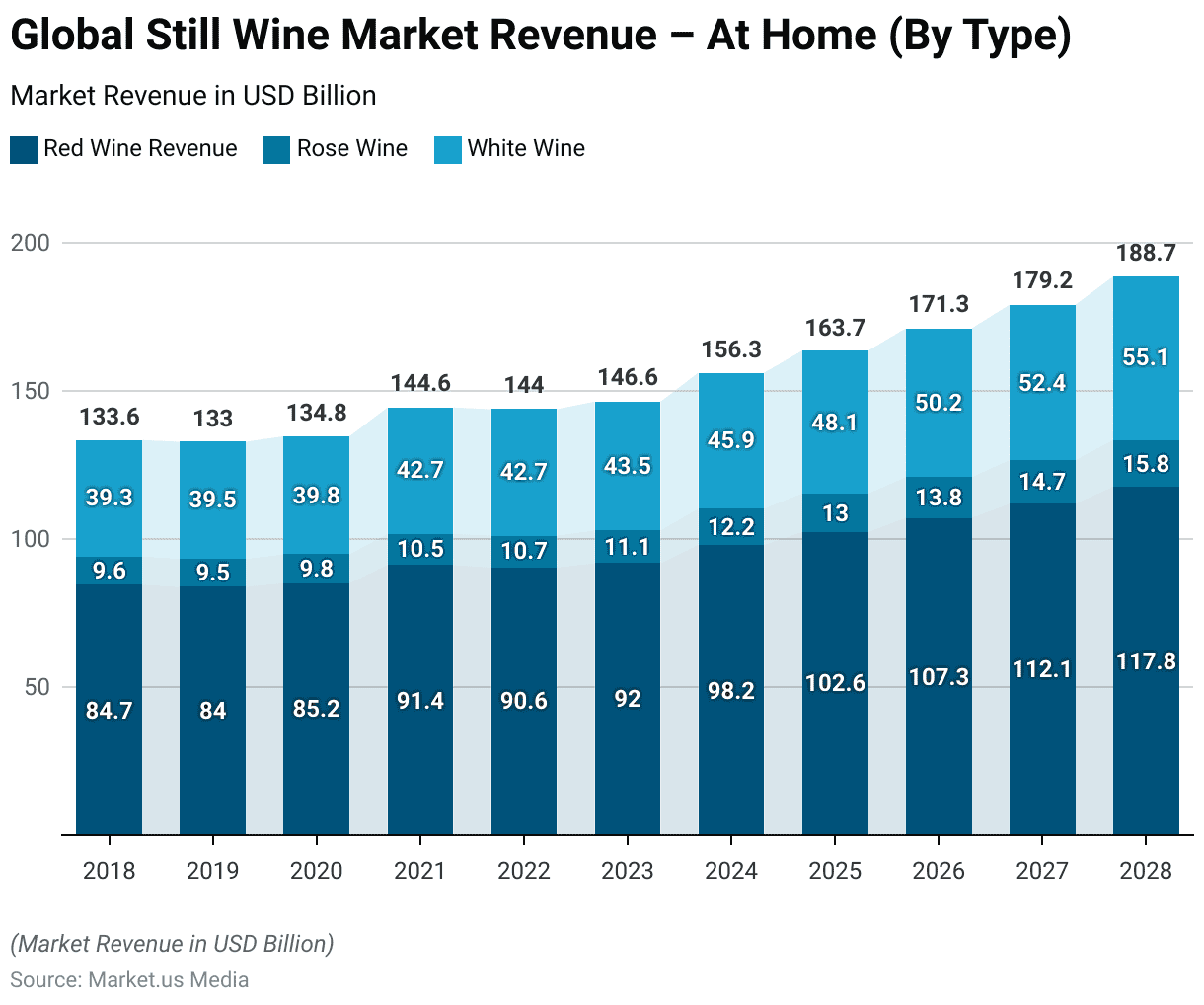

Still Wine Market Revenue – At Home (By Type) Statistics

- The global still wine market revenue for at-home consumption, segmented by type, has shown a steady increase from 2018 to 2028.

- In 2018, red wine revenue was USD 84.7 billion, rosé wine USD 9.6 billion, and white wine USD 39.3 billion.

- The following year, red wine revenue slightly decreased to USD 84.0 billion, rosé wine remained stable at USD 9.5 billion, and white wine increased marginally to USD 39.5 billion.

- In 2020, red wine revenue grew to USD 85.2 billion, rosé wine to USD 9.8 billion, and white wine to USD 39.8 billion.

- The market saw a notable increase in 2021, with red wine revenue reaching USD 91.4 billion, rosé wine USD 10.5 billion, and white wine USD 42.7 billion.

- In 2022, red wine revenue slightly decreased to USD 90.6 billion, while rosé wine and white wine remained steady at USD 10.7 billion and USD 42.7 billion, respectively.

- The upward trend continued in 2023, with revenues rising to USD 92.0 billion for red wine, USD 11.1 billion for rosé wine, and USD 43.5 billion for white wine.

- Projections indicate sustained growth, with red wine expected to generate USD 98.2 billion in 2024, USD 102.6 billion in 2025, and USD 117.8 billion by 2028.

- Similarly, rosé wine revenue is projected to increase to USD 12.2 billion in 2024 and USD 15.8 billion by 2028, while white wine revenue is forecasted to rise to USD 45.9 billion in 2024 and USD 55.1 billion by 2028.

(Source: Statista)

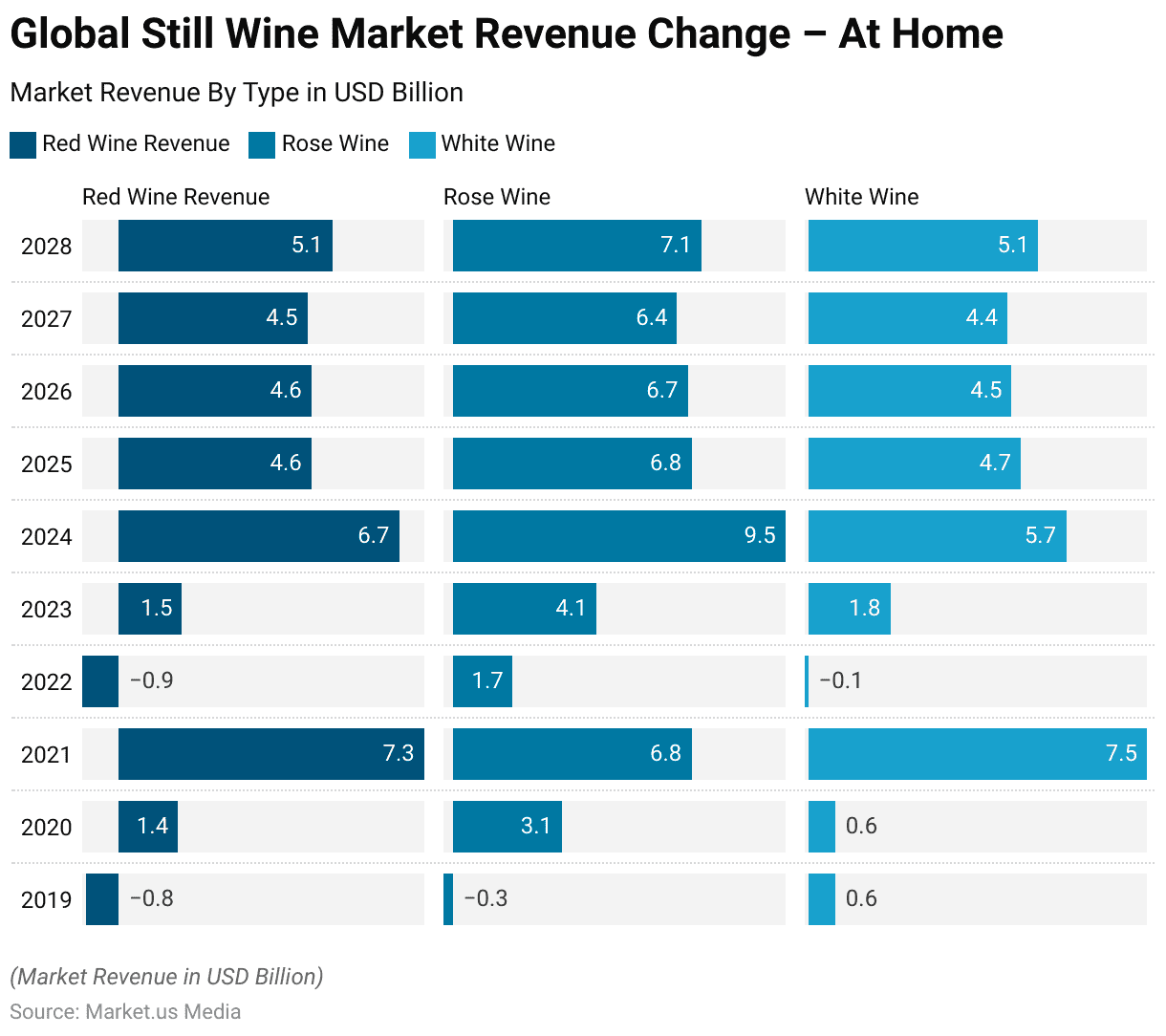

Still Wine Market Revenue Change – At Home (By Type) Statistics

- The global still wine market revenue changes for at-home consumption, segmented by type, have shown varying trends from 2019 to 2028.

- In 2019, red wine revenue decreased by 0.8%, and rosé wine by 0.3%. While white wine revenue saw a slight increase of 0.6%. In 2020, red wine revenue grew by 1.4%, rosé wine by 3.1%, and white wine by 0.6%.

- Significant growth was observed in 2021, with red wine revenue increasing by 7.3%, rosé wine by 6.8%, and white wine by 7.5%.

- However, 2022 experienced a decline in red wine revenue by 0.9% and a marginal decrease in white wine revenue by 0.1%, while rosé wine revenue increased by 1.7%.

- In 2023, the upward trend resumed, with red wine revenue growing by 1.5%, rosé wine by 4.1%, and white wine by 1.8%.

- Projections for the following years indicate continued growth across all types: in 2024, red wine revenue is expected to rise by 6.7%, rosé wine by 9.5%, and white wine by 5.7%; in 2025, red wine by 4.6%, rosé wine by 6.8%, and white wine by 4.7%; in 2026, red wine by 4.6%, rosé wine by 6.7%, and white wine by 4.5%; in 2027, red wine by 4.5%, rosé wine by 6.4%, and white wine by 4.4%; and in 2028, red wine by 5.1%, rosé wine by 7.1%, and white wine by 5.1%.

(Source: Statista)

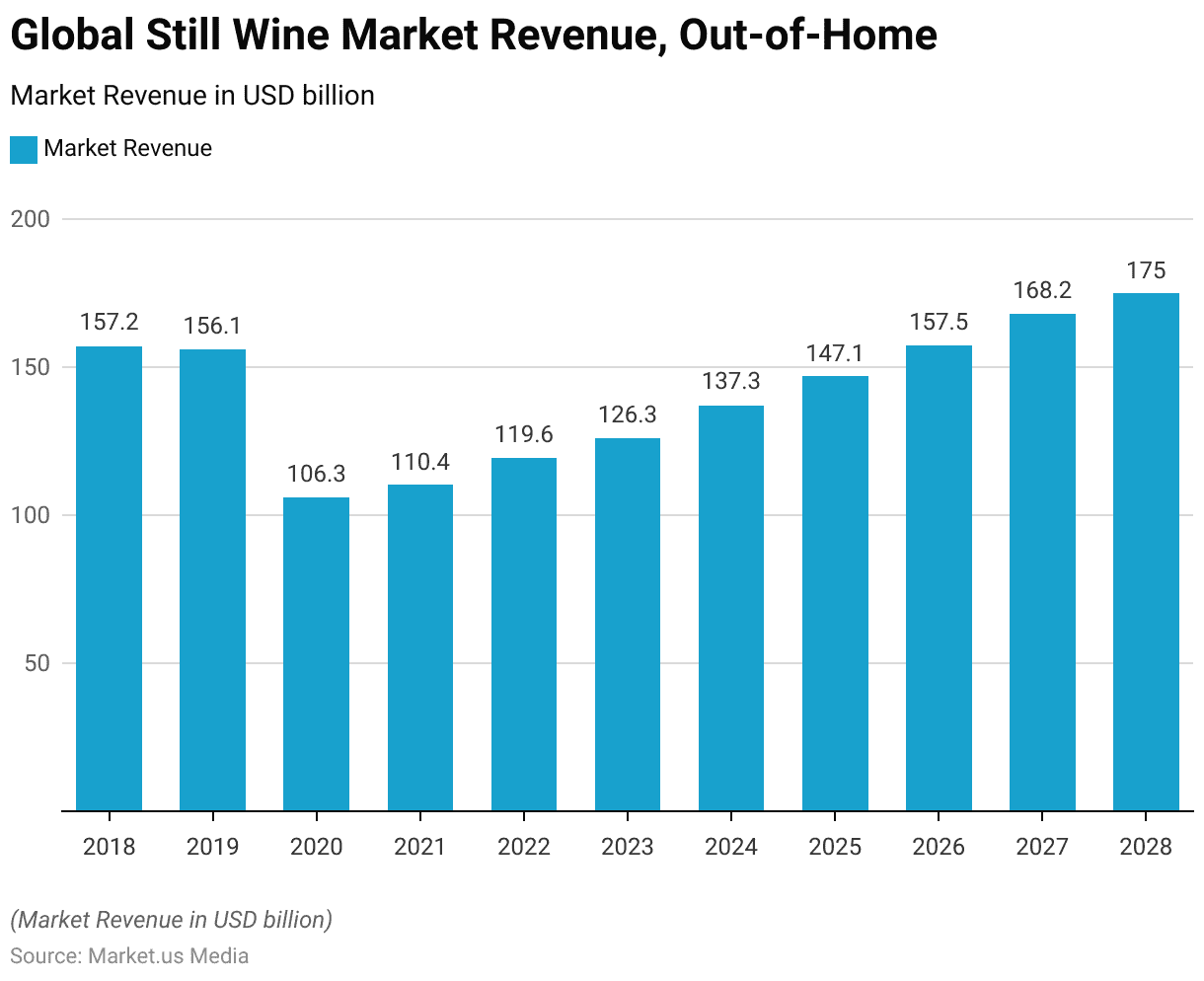

Global Still Wine Market Revenue – Out-of-Home Statistics

- The global still wine market revenue generated from out-of-home (e.g., revenue generated in restaurants and bars) consumption has experienced significant fluctuations from 2018 to 2028.

- In 2018, the revenue was USD 157.2 billion, slightly decreasing to USD 156.1 billion in 2019.

- The market faced a steep decline in 2020 due to the COVID-19 pandemic, with revenue dropping to USD 106.3 billion.

- A gradual recovery began in 2021, with revenues increasing to USD 110.4 billion.

- This upward trend continued in 2022, reaching USD 119.6 billion and further to USD 126.3 billion in 2023.

- Future projections indicate sustained growth, with revenues expected to rise to USD 137.3 billion in 2024, USD 147.1 billion in 2025, USD 157.5 billion in 2026, USD 168.2 billion in 2027, and USD 175.0 billion by 2028.

(Source: Statista)

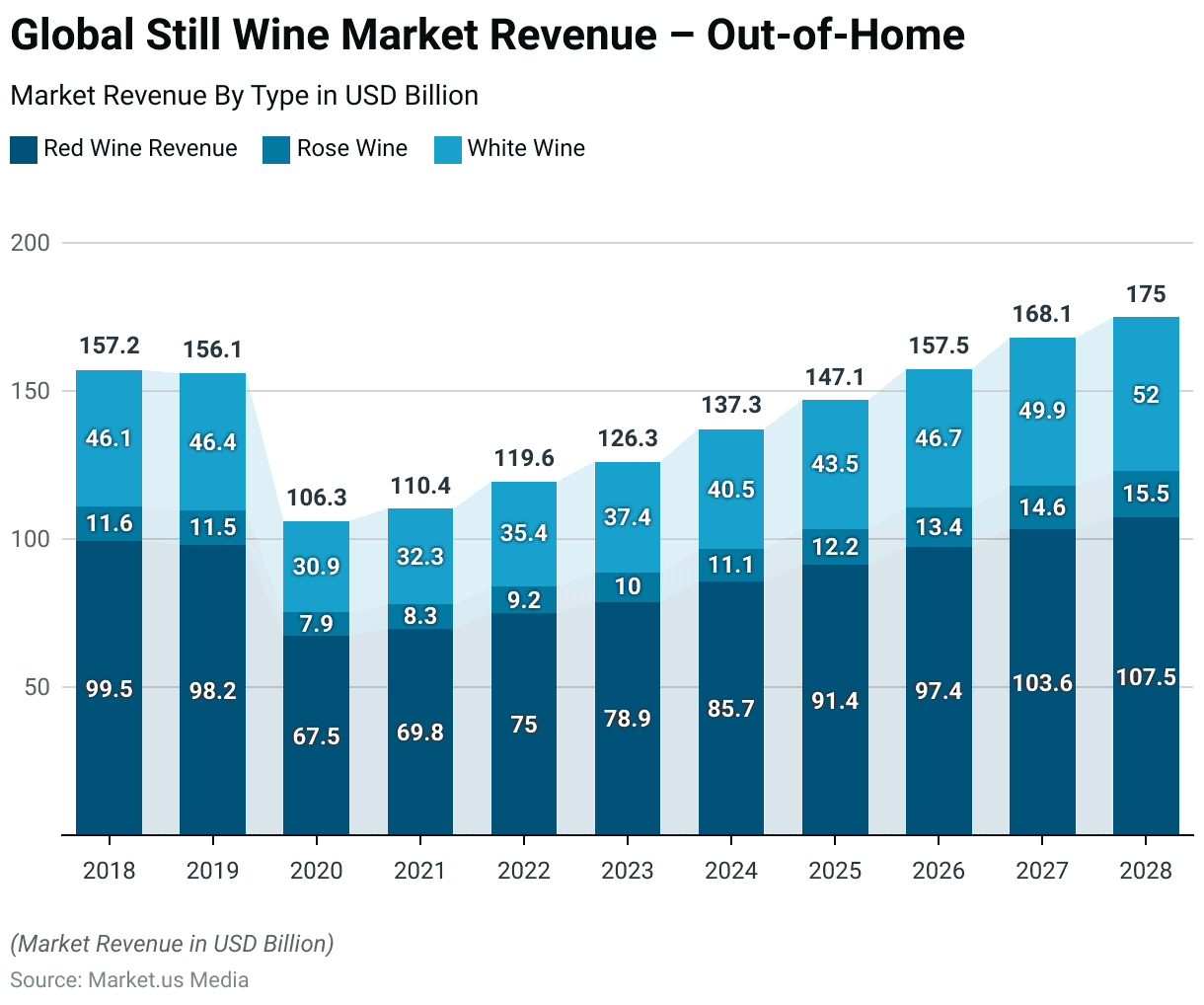

Still Wine Market Revenue – Out-of-Home (By Type) Statistics

- The global still wine market revenue from out-of-home consumption, such as in restaurants and bars. It has demonstrated varied trends across different wine types from 2018 to 2028.

- In 2018, red wine generated USD 99.5 billion, rosé wine USD 11.6 billion, and white wine USD 46.1 billion.

- The following year, red wine revenue slightly decreased to USD 98.2 billion, rosé wine to USD 11.5 billion, while white wine saw a marginal increase to USD 46.4 billion.

- The COVID-19 pandemic in 2020 caused a significant decline, with red wine revenue dropping to USD 67.5 billion, rosé wine to USD 7.9 billion, and white wine to USD 30.9 billion.

- A gradual recovery began in 2021, with revenues rising to USD 69.8 billion for red wine, USD 8.3 billion for rosé wine, and USD 32.3 billion for white wine.

- This positive trend continued in 2022, with red wine reaching USD 75.0 billion, rosé wine USD 9.2 billion, and white wine USD 35.4 billion.

- By 2023, revenues increased further to USD 78.9 billion for red wine, USD 10.0 billion for rosé wine, and USD 37.4 billion for white wine.

- Future projections indicate continued growth, with red wine expected to generate USD 85.7 billion in 2024, USD 91.4 billion in 2025, and USD 107.5 billion by 2028.

- Similarly, rosé wine revenue is projected to increase to USD 11.1 billion in 2024 and USD 15.5 billion by 2028, while white wine revenue is forecasted to rise to USD 40.5 billion in 2024 and USD 52.0 billion by 2028.

(Source: Statista)

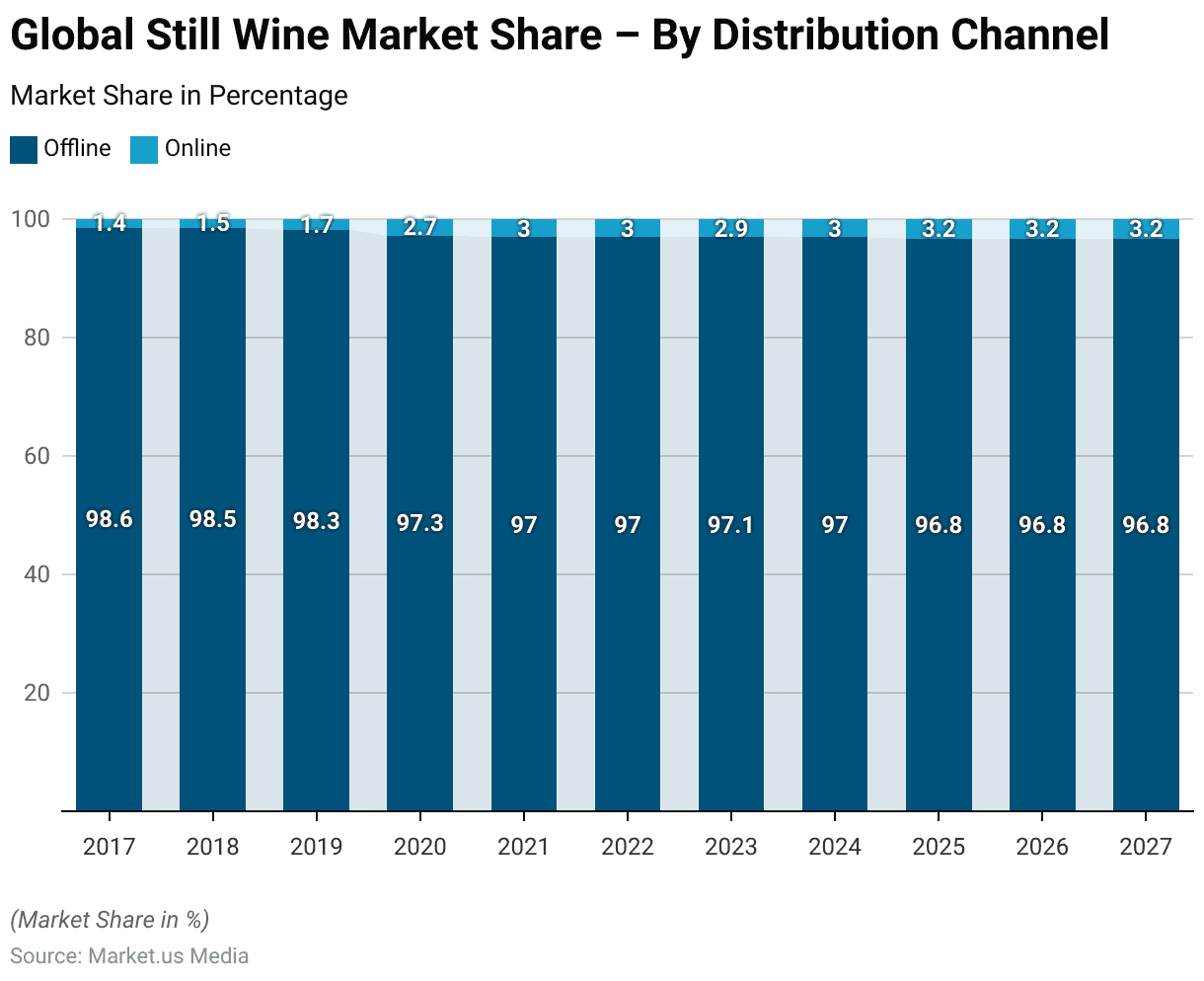

Global Still Wine Market Share – By Distribution Channel Statistics

- The global still wine market share by distribution channel has shown a gradual shift from offline to online sales from 2017 to 2027.

- In 2017, the market was predominantly offline, with 98.6% of sales occurring through this channel, while online sales accounted for only 1.4%.

- This trend continued in 2018, with offline sales at 98.5% and online sales increasing slightly to 1.5%.

- In 2019, offline sales constituted 98.3% of the market, with online sales rising to 1.7%.

- The COVID-19 pandemic in 2020 accelerated the shift towards online sales, with offline sales dropping to 97.3% and online sales increasing to 2.7%.

- By 2021, offline sales further decreased to 97.0%, while online sales grew to 3.0%, a trend that remained stable in 2022.

- In 2023, offline sales accounted for 97.1% of the market, with online sales slightly decreasing to 2.9%.

- Projections for the coming years indicate a continued shift towards online sales, with offline sales expected to be 97.0% in 2024 and online sales at 3.0%.

- By 2025, offline sales are anticipated to drop to 96.8%, with online sales increasing to 3.2%, a trend that is expected to remain consistent through 2027.

(Source: Statista)

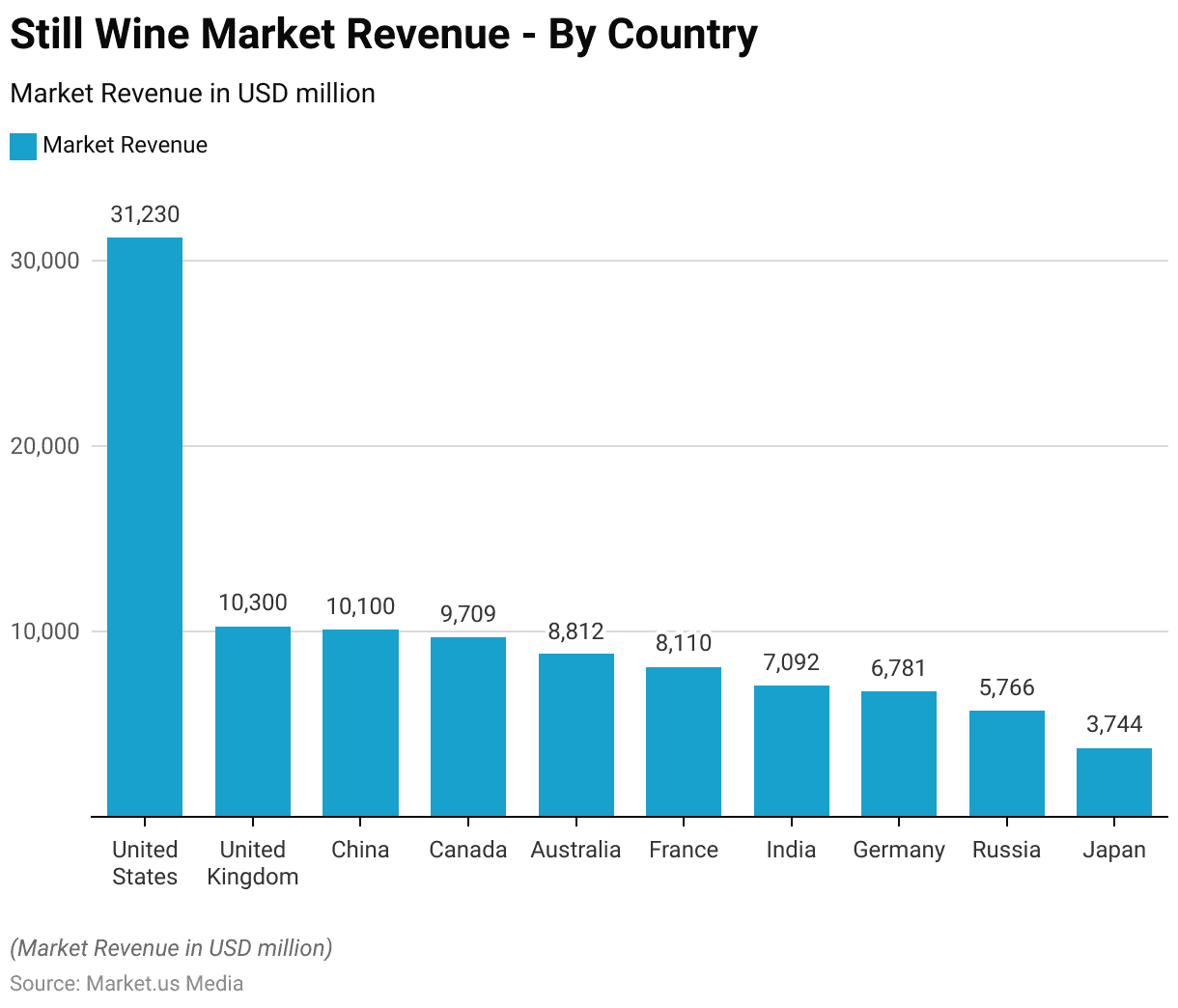

Regional Analysis of the Global Still Wine Market

- The global still wine market revenue varies significantly by country. The United States is leading the market with a revenue of USD 31,230 million.

- The United Kingdom and China follow, generating revenues of USD 10,300 million and USD 10,100 million, respectively.

- Canada also holds a significant share with USD 9,709 million.

- Australia’s still wine market revenue stands at USD 8,812 million, while

- France, known for its rich wine culture, contributes USD 8,110 million.

- India, a growing market for still wine, generates USD 7,092 million.

- Germany’s revenue is USD 6,781 million, and Russia’s is USD 5,766 million.

- Japan has a still wine market revenue of USD 3,744 million. Rounds out the list of top countries in this sector.

(Source: Statista)

Average Revenue Per Capita Generated from Still Wine Statistics

Overall Average Revenue Per Capita

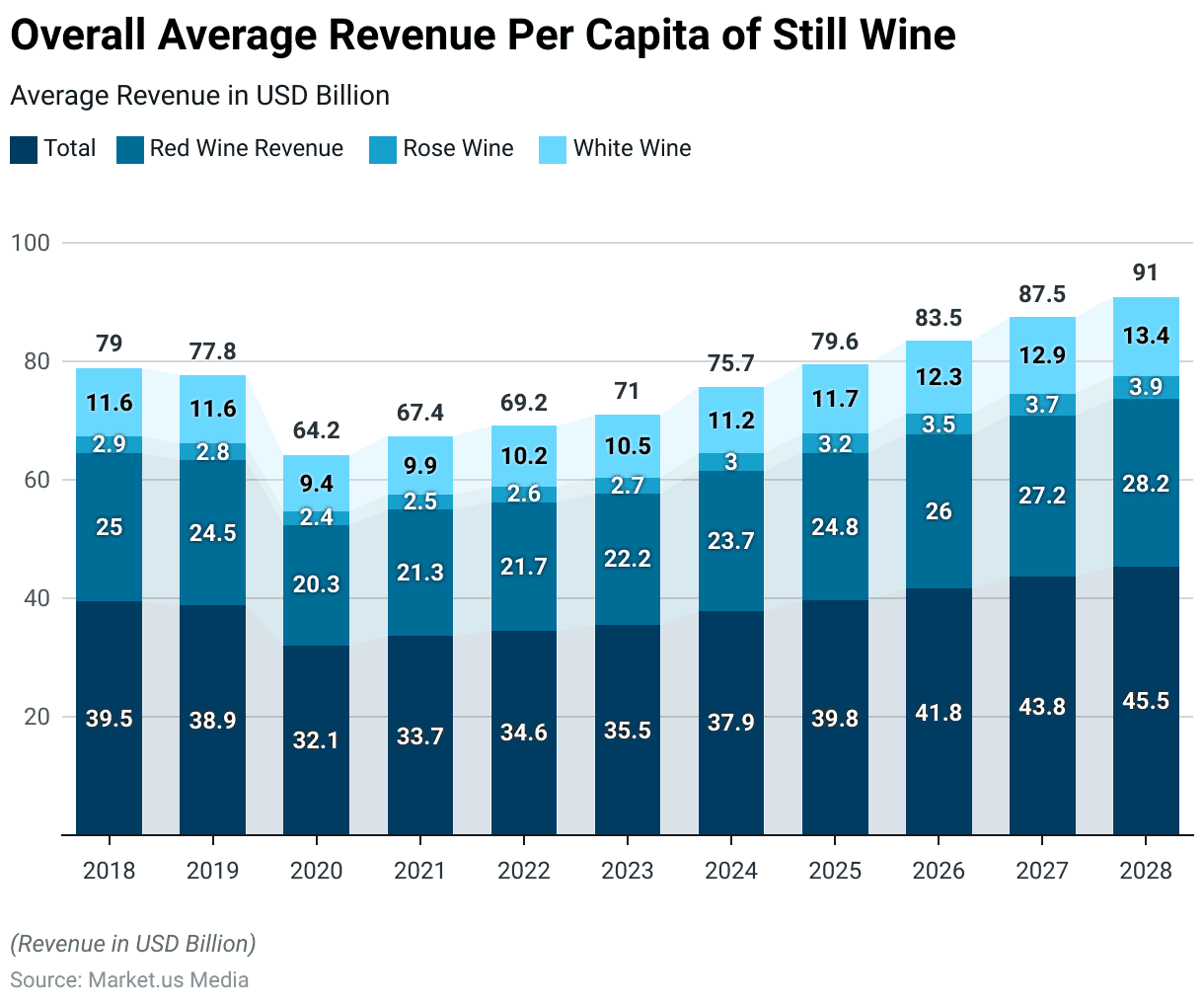

- The global still wine market has displayed discernible fluctuations in average revenue per capita across various wine categories from 2018 to 2028.

- In 2018, total average revenue per capita stood at USD 39.49. With red wine leading at USD 25.02, followed by white wine at USD 11.60 and rosé wine at USD 2.87.

- Subsequently, a slight decline was observed in 2019, followed by a significant drop in 2020 due to the COVID-19 pandemic.

- However, a steady recovery ensued from 2021 onwards, with each subsequent year witnessing an increase in average revenue per capita.

- Projections indicate sustained growth, with the total expected to reach USD 45.48 by 2028, led by red wine at USD 28.18. Followed by white wine at USD 13.39, and rosé wine at USD 3.91.

- This trajectory underscores a resilient market poised for continued expansion in the coming years.

(Source: Statista)

Average Revenue Per Capita – At Home

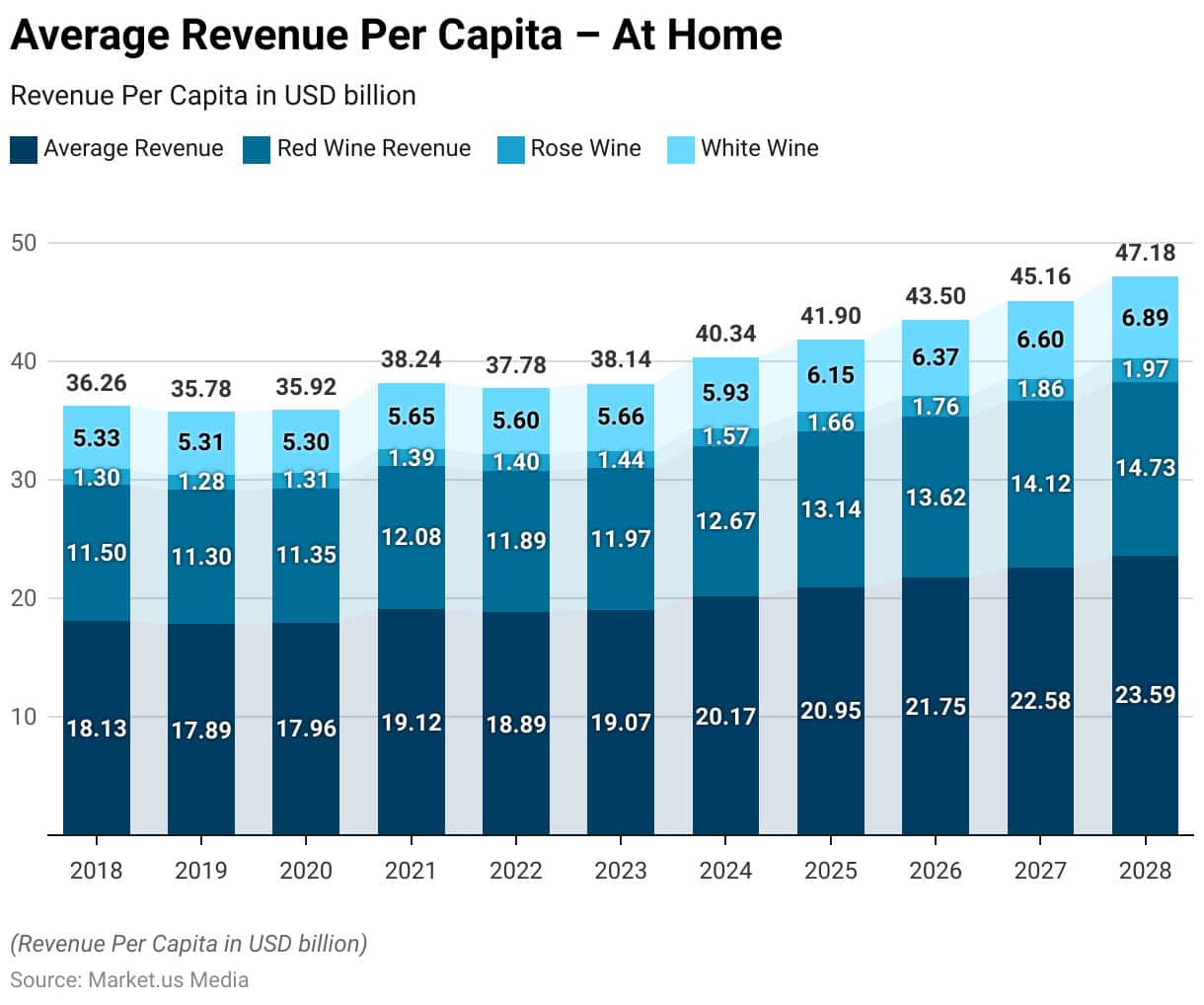

- From 2018 to 2028, the average revenue per capita for at-home consumption of still wine has displayed consistent growth.

- In 2018, the total average revenue amounted to USD 18.13, with red wine leading at USD 11.50, followed by white wine at USD 5.33 and rosé wine at USD 1.30.

- Despite minor fluctuations in subsequent years, the overall trend has been upward.

- Notably, by 2028, the total average revenue per capita is projected to reach USD 23.59, driven by increases in red wine to USD 14.73, white wine to USD 6.89, and rosé wine to USD 1.97.

- These projections indicate a steady rise in consumer spending on still wine for at-home consumption over the forecast period.

(Source: Statista)

Revenue Per Capita – Out-of-Home

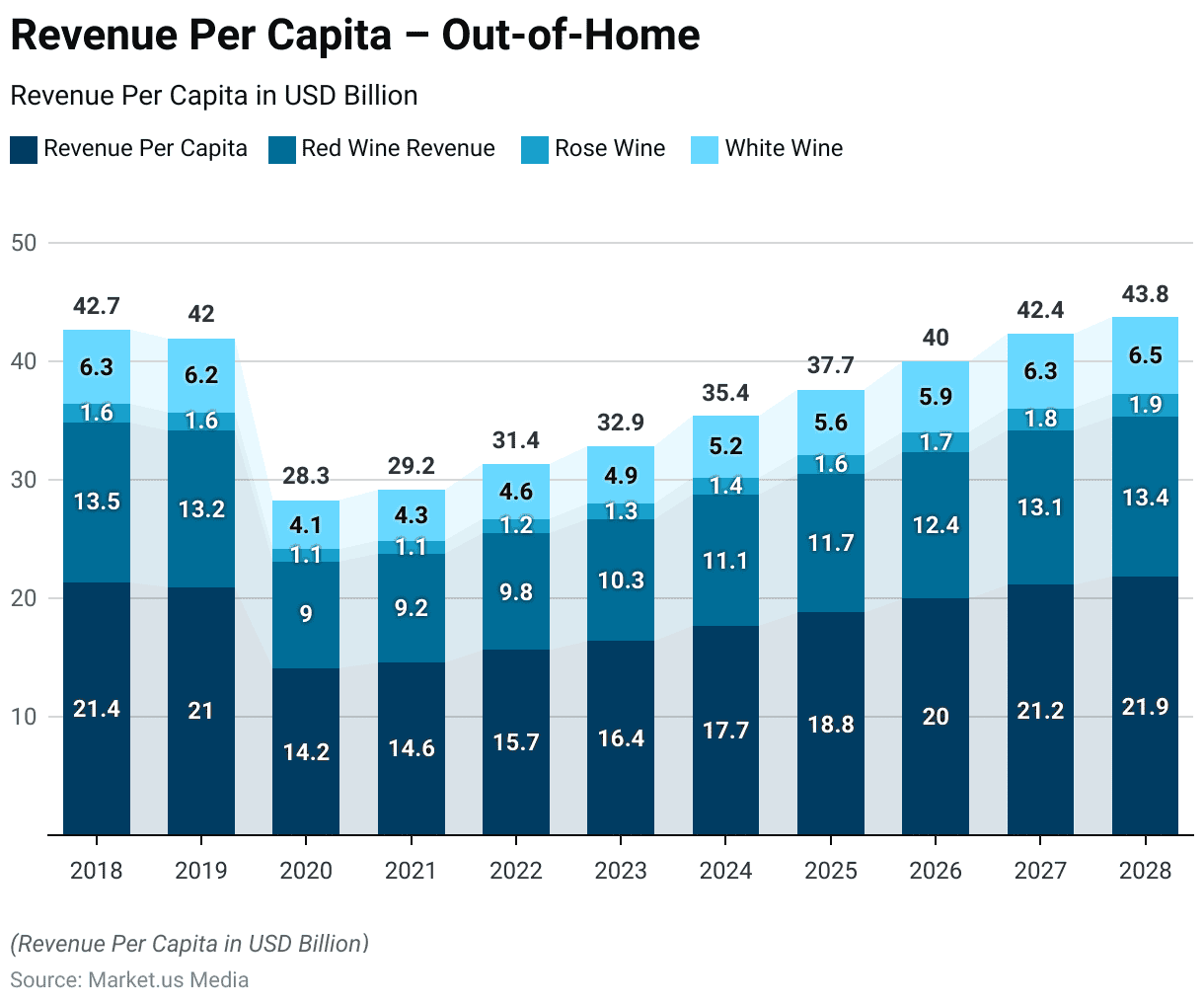

- The average revenue per capita for out-of-home consumption of still wine has witnessed various fluctuations and growth from 2018 to 2028.

- In 2018, the total average revenue per capita stood at USD 21.36, with red wine leading at USD 13.52, followed by white wine at USD 6.27 and rosé wine at USD 1.57.

- However, the onset of the COVID-19 pandemic in 2020 led to a significant decline, with the total average revenue per capita plummeting to USD 14.16.

- Nevertheless, a gradual recovery began in 2021 and continued through subsequent years.

- Projections suggest sustained growth, with the total expected to reach USD 21.89 by 2028, driven by increases in red wine to USD 13.44, white wine to USD 6.51, and rosé wine to USD 1.94.

- These projections indicate a resilient market rebounding from pandemic-induced setbacks and poised for further expansion in the out-of-home consumption sector.

(Source: Statista)

Still Wine Consumption Volume Statistics

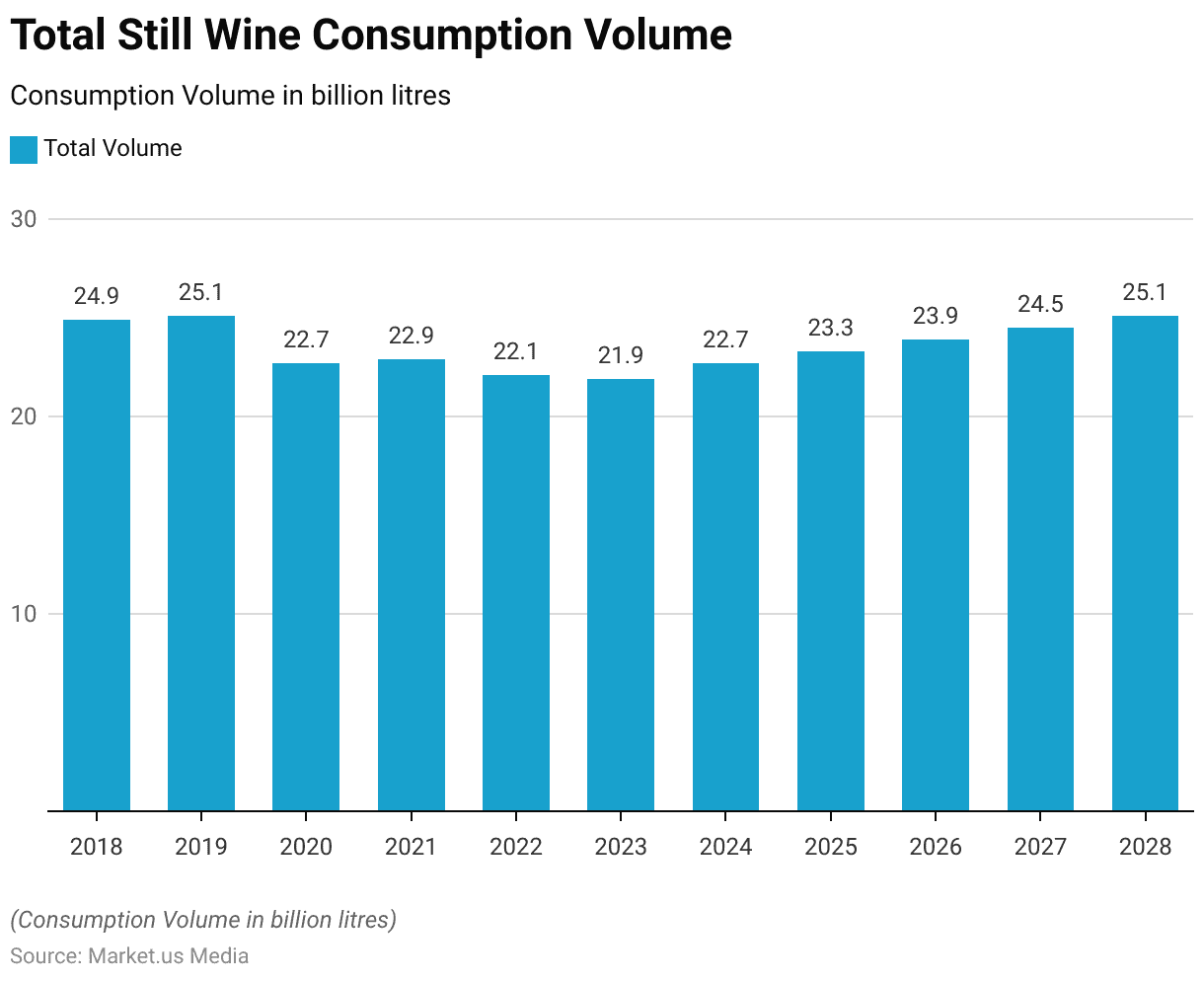

Total Volume

- The global consumption volume of still wine has shown varying trends from 2018 to 2028.

- In 2018, the total volume consumed was 24.9 billion liters, slightly increasing to 25.1 billion liters in 2019.

- The COVID-19 pandemic in 2020 led to a significant decline, with consumption dropping to 22.7 billion liters.

- A minor recovery was observed in 2021, with the volume increasing to 22.9 billion liters.

- However, consumption decreased again in 2022 to 22.1 billion liters and further to 21.9 billion liters in 2023.

- Projections indicate a positive turnaround, with the volume expected to rise to 22.7 billion liters in 2024, 23.3 billion liters in 2025, and 23.9 billion liters in 2026.

- The upward trend is anticipated to continue, reaching 24.5 billion liters in 2027 and returning to 25.1 billion liters by 2028.

(Source: Statista)

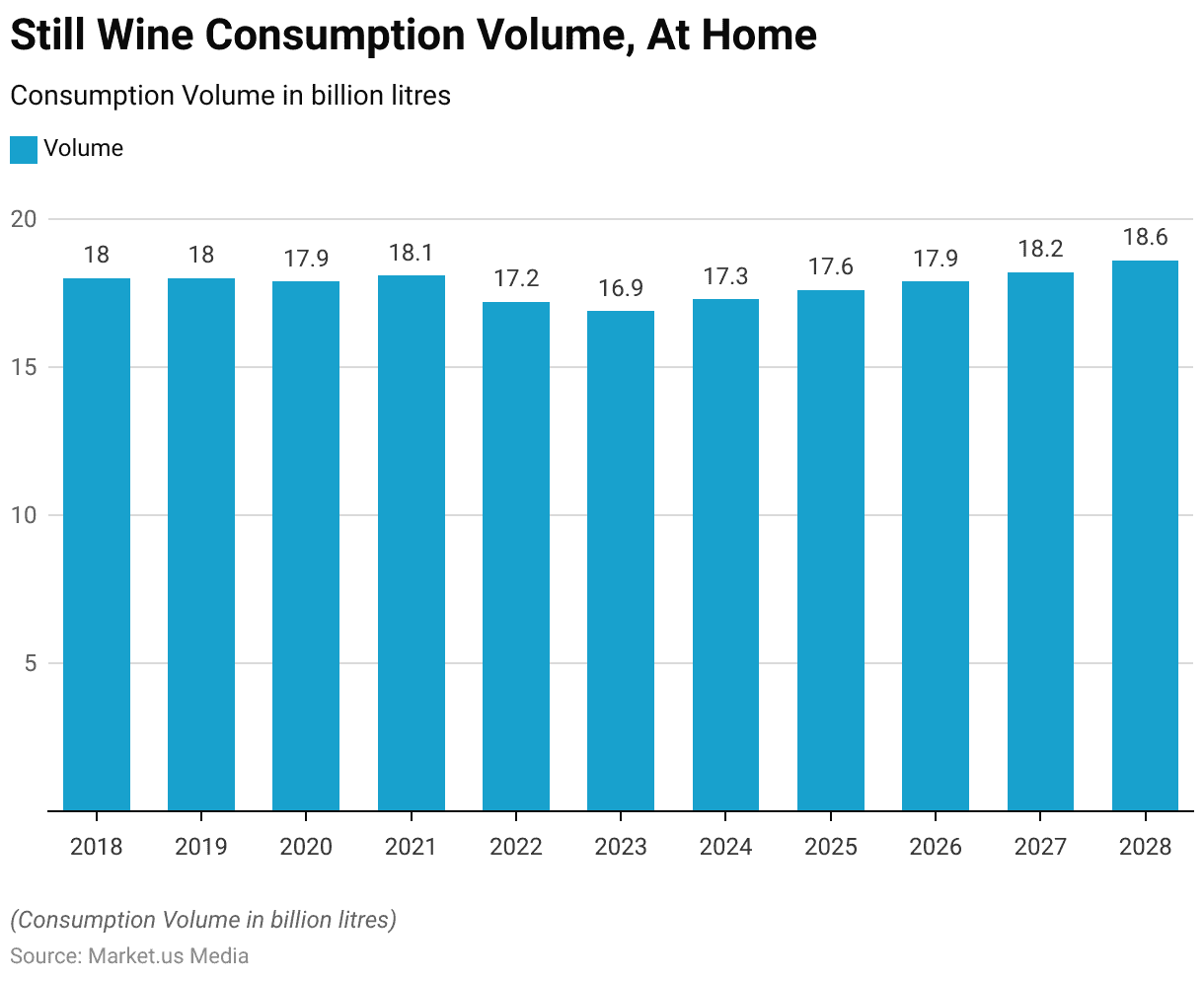

Volume – At Home

- The volume of still wine consumed at home has demonstrated slight fluctuations from 2018 to 2028.

- In 2018 and 2019, the volume remained stable at 18.0 billion liters.

- A minor decrease occurred in 2020, with consumption falling to 17.9 billion liters.

- In 2021, the volume slightly increased to 18.1 billion liters.

- However, 2022 saw a more noticeable decline to 17.2 billion liters, followed by a further decrease to 16.9 billion liters in 2023.

- Projections for the coming years indicate a gradual recovery, with the volume expected to rise to 17.3 billion liters in 2024, 17.6 billion liters in 2025, and 17.9 billion liters in 2026.

- The upward trend is anticipated to continue, with at-home consumption reaching 18.2 billion liters in 2027 and 18.6 billion liters by 2028.

(Source: Statista)

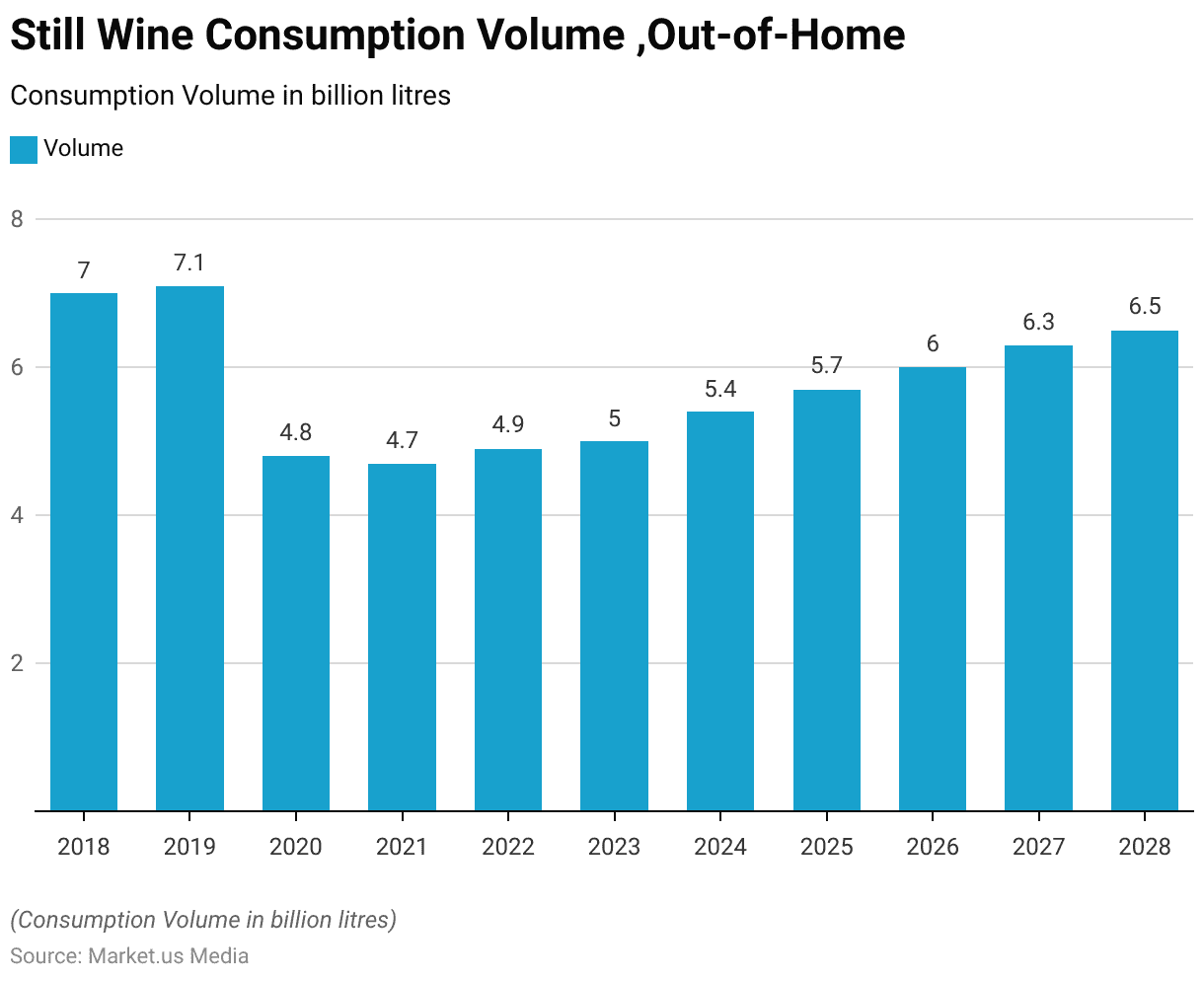

Volume – Out-of-Home

- The volume of still wine consumed out-of-home has experienced notable changes from 2018 to 2028.

- In 2018, the volume was 7.0 billion liters, increasing slightly to 7.1 billion liters in 2019.

- The COVID-19 pandemic in 2020 led to a significant reduction in out-of-home consumption, with the volume dropping to 4.8 billion liters and further decreasing to 4.7 billion liters in 2021.

- A recovery began in 2022, with the volume rising to 4.9 billion liters, followed by an increase to 5.0 billion liters in 2023.

- Projections indicate continued growth in out-of-home consumption, with the volume expected to reach 5.4 billion liters in 2024, 5.7 billion liters in 2025, and 6.0 billion liters in 2026.

- The upward trend is anticipated to continue, with consumption projected to reach 6.3 billion liters in 2027 and 6.5 billion liters by 2028.

(Source: Statista)

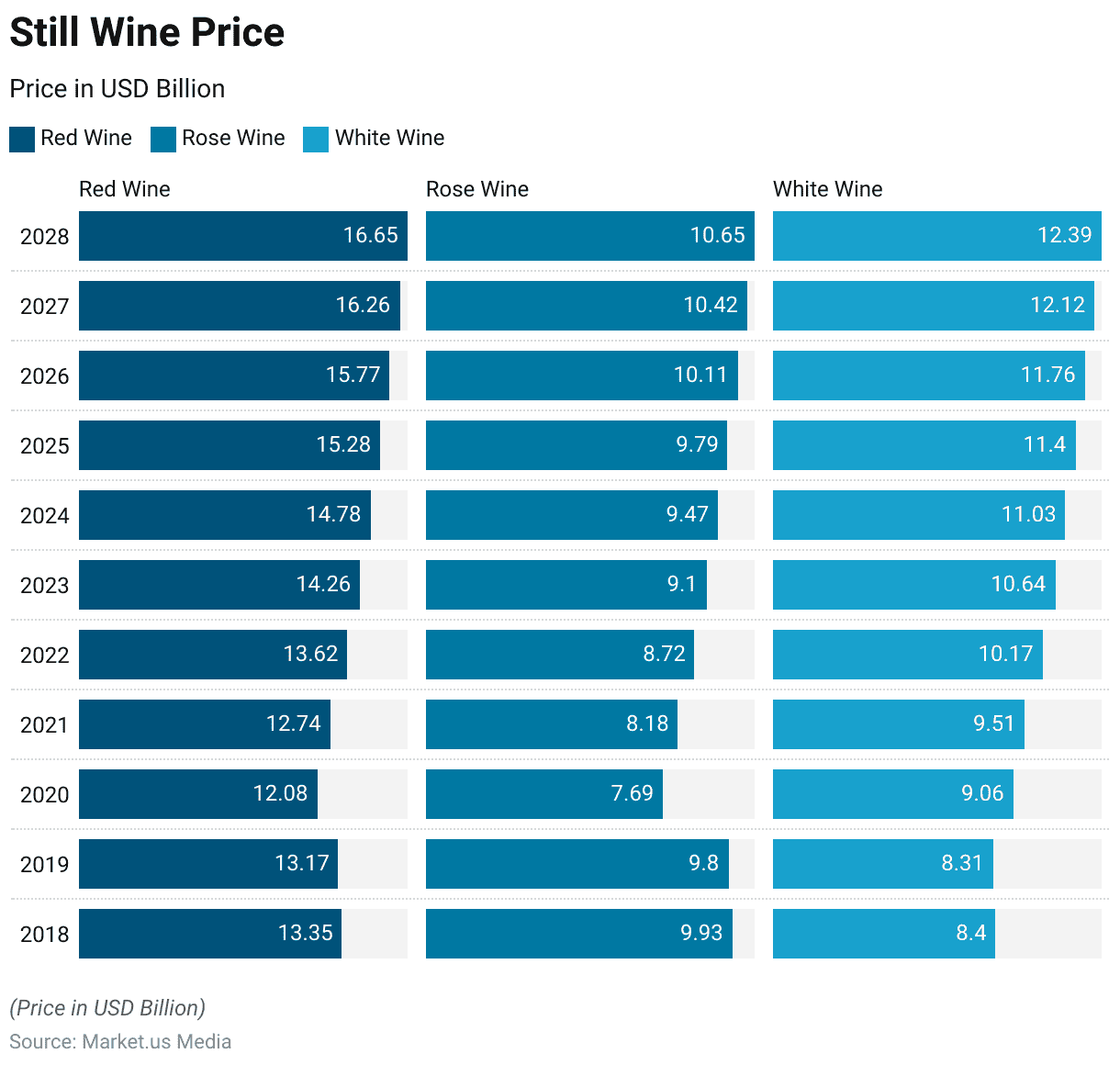

Still Wine Price Statistics

- The prices of still wine have shown varied trends across red, rosé, and white wines from 2018 to 2028.

- In 2018, the price of red wine was USD 13.35, rosé wine USD 9.93, and white wine USD 8.40.

- In 2019, the prices slightly decreased to USD 13.17 for red wine, USD 9.80 for rosé wine, and USD 8.31 for white wine.

- The year 2020 saw a notable decline in red wine prices to USD 12.08 and rosé wine to USD 7.69, while white wine increased to USD 9.06.

- Prices began to recover in 2021, with red wine at USD 12.74, rosé wine at USD 8.18, and white wine at USD 9.51.

- In 2022, prices continued to rise, reaching USD 13.62 for red wine, USD 8.72 for rosé wine, and USD 10.17 for white wine.

- By 2023, the prices had further increased to USD 14.26 for red wine, USD 9.10 for rosé wine, and USD 10.64 for white wine.

- Projections for the coming years indicate a steady upward trend: in 2024, the price of red wine is expected to be USD 14.78, rosé wine USD 9.47, and white wine USD 11.03.

- By 2025, the prices are projected to be USD 15.28 for red wine, USD 9.79 for rosé wine, and USD 11.40 for white wine.

- In 2026, prices are anticipated to reach USD 15.77 for red wine, USD 10.11 for rosé wine, and USD 11.76 for white wine.

- By 2027, the prices are expected to be USD 16.26 for red wine, USD 10.42 for rosé wine, and USD 12.12 for white wine.

- Finally, by 2028, the prices are projected to reach USD 16.65 for red wine, USD 10.65 for rosé wine, and USD 12.39 for white wine.

(Source: Statista)

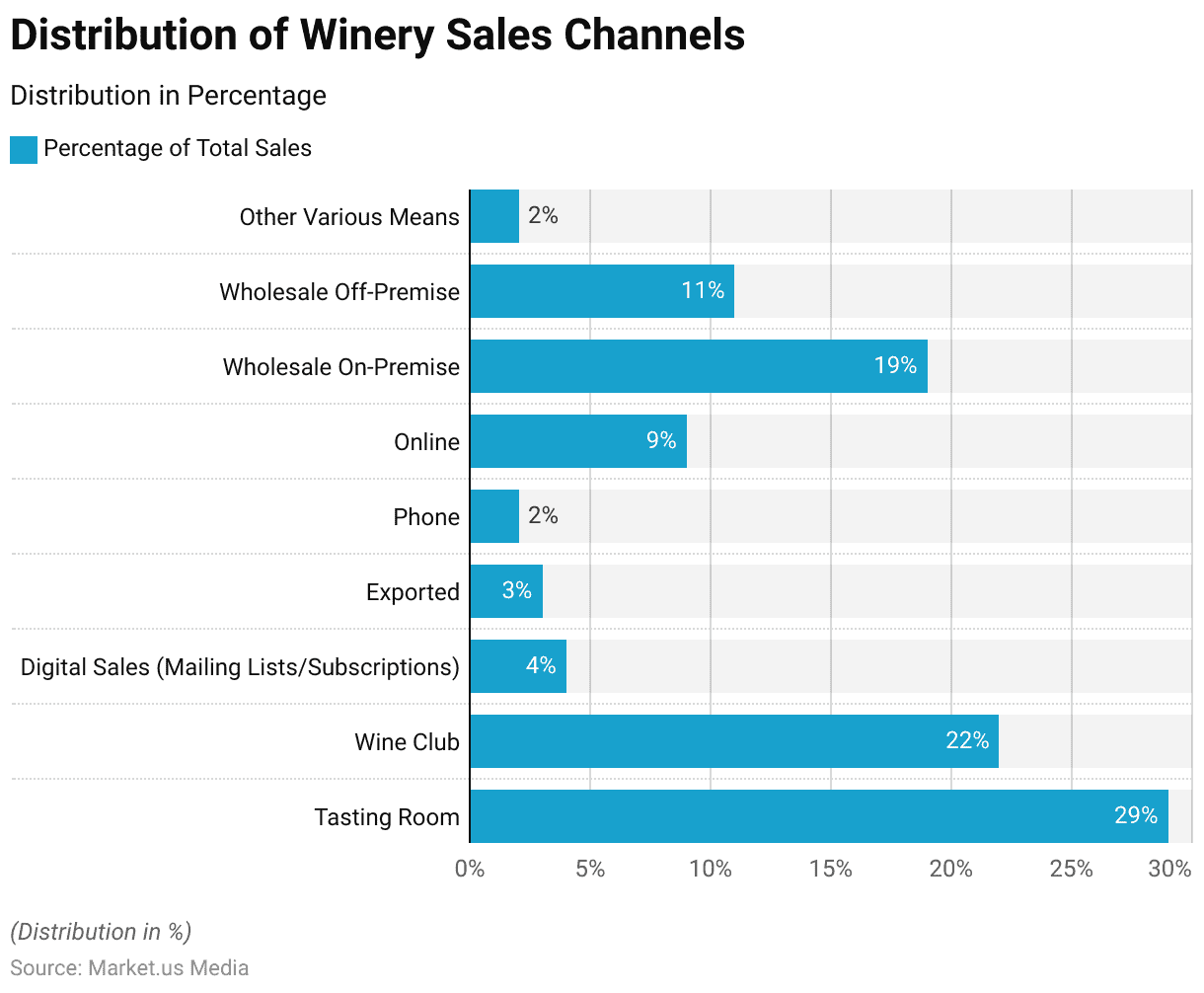

Winery Sales Channels Statistics

- According to wine industry statistics, the highest winery sales channel is the tasting room, accounting for 29% of total sales.

- Wine clubs contribute to 22% of the overall sales.

- Digital sales, including those from mailing lists or subscriptions, represent 4% of the market.

- Other sales channels include exported sales at 3%, phone sales at 2%, online sales at 9%, wholesale on-premise sales at 19%, and wholesale off-premise sales at 11%.

- Additionally, various other means account for 2% of the overall winery sales channels.

(Source: Silicon Valley Bank)

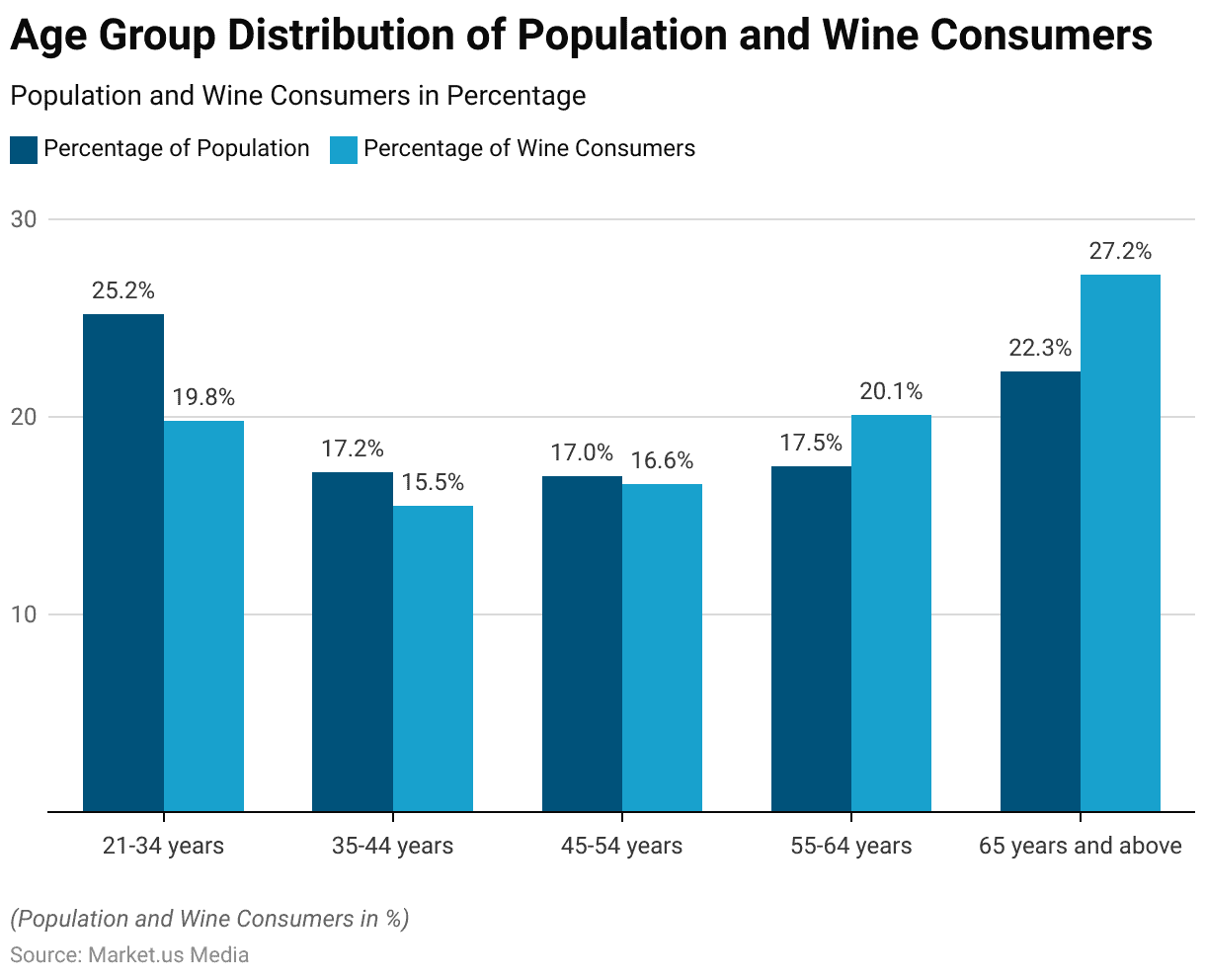

Demographics of Still Wine Consumers Statistics

By Age

- The wine consumption demographics reveal distinct trends across various age groups.

- Among individuals aged 21 to 34 years, who constitute 25.2% of the total population, 19.8% are wine consumers.

- In the 35 to 44 years age group, 15.5% of wine consumers belong to the 17.2% of the population in this age bracket.

- The 45 to 54 years age group shows a minor difference between the overall population (17.0%) and wine consumers (16.6%).

- For those aged 55 to 64 years, 17.5% of the population accounts for a higher percentage of wine consumers at 20.1%.

- Notably, the population aged 65 years and above, which represents 22.3% of the total population, has the highest proportion of wine consumers at 27.2%.

(Source: Silicon Valley Bank)

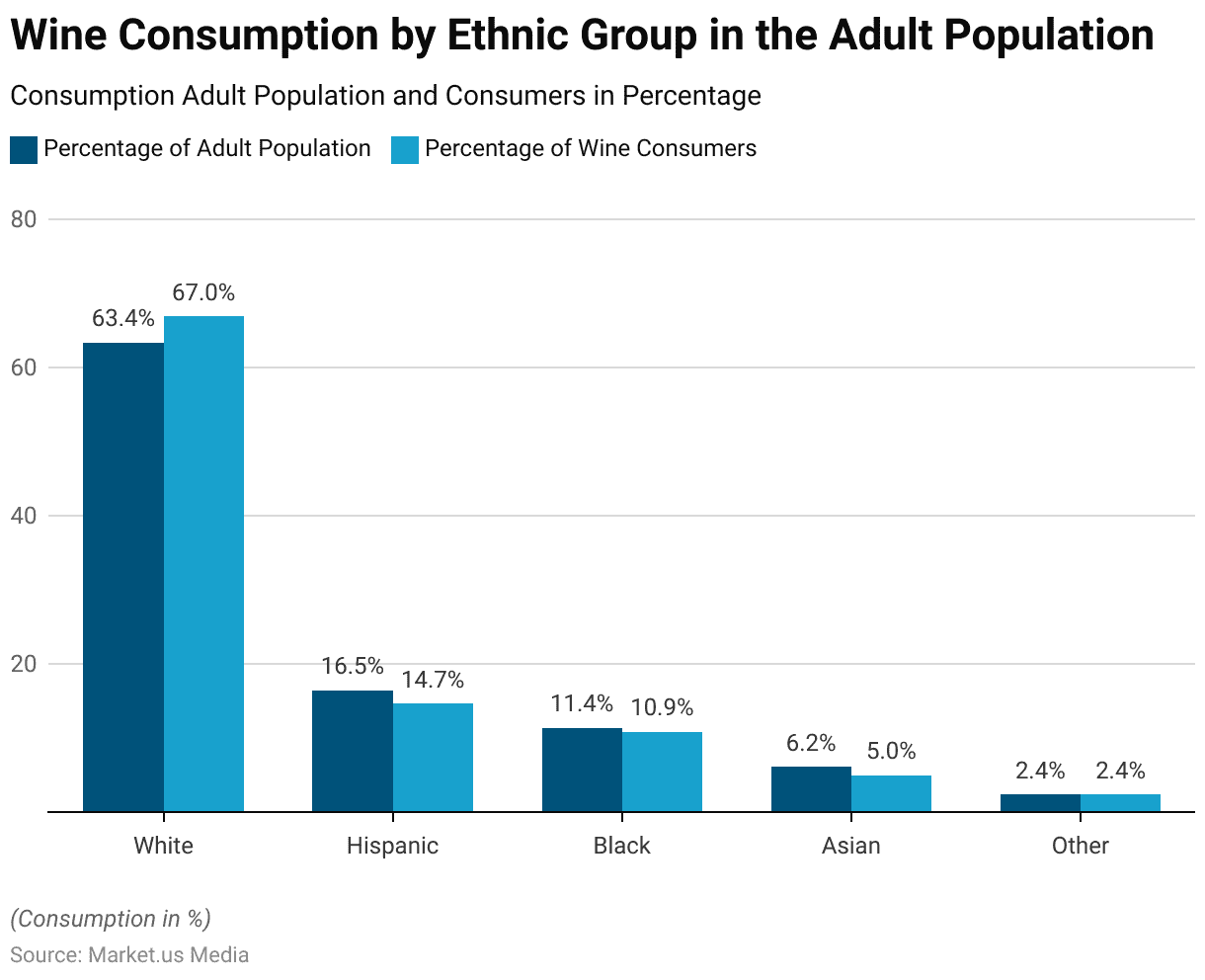

By Ethnicity

- The distribution of wine consumption among different ethnic groups shows distinct patterns.

- White people comprise 63.4% of the adult population and represent 67% of wine consumers.

- Hispanic people account for 16.5% of the adult population, with 14.7% being wine drinkers.

- Black people make up 11.4% of the adult population, and 10.9% are wine consumers.

- Among Asian people, 6.2% of the adult population corresponds to 5% of wine consumers.

- Other ethnic groups have a similar share of the adult population and wine consumers, both at 2.4%.

(Source: Silicon Valley Bank)

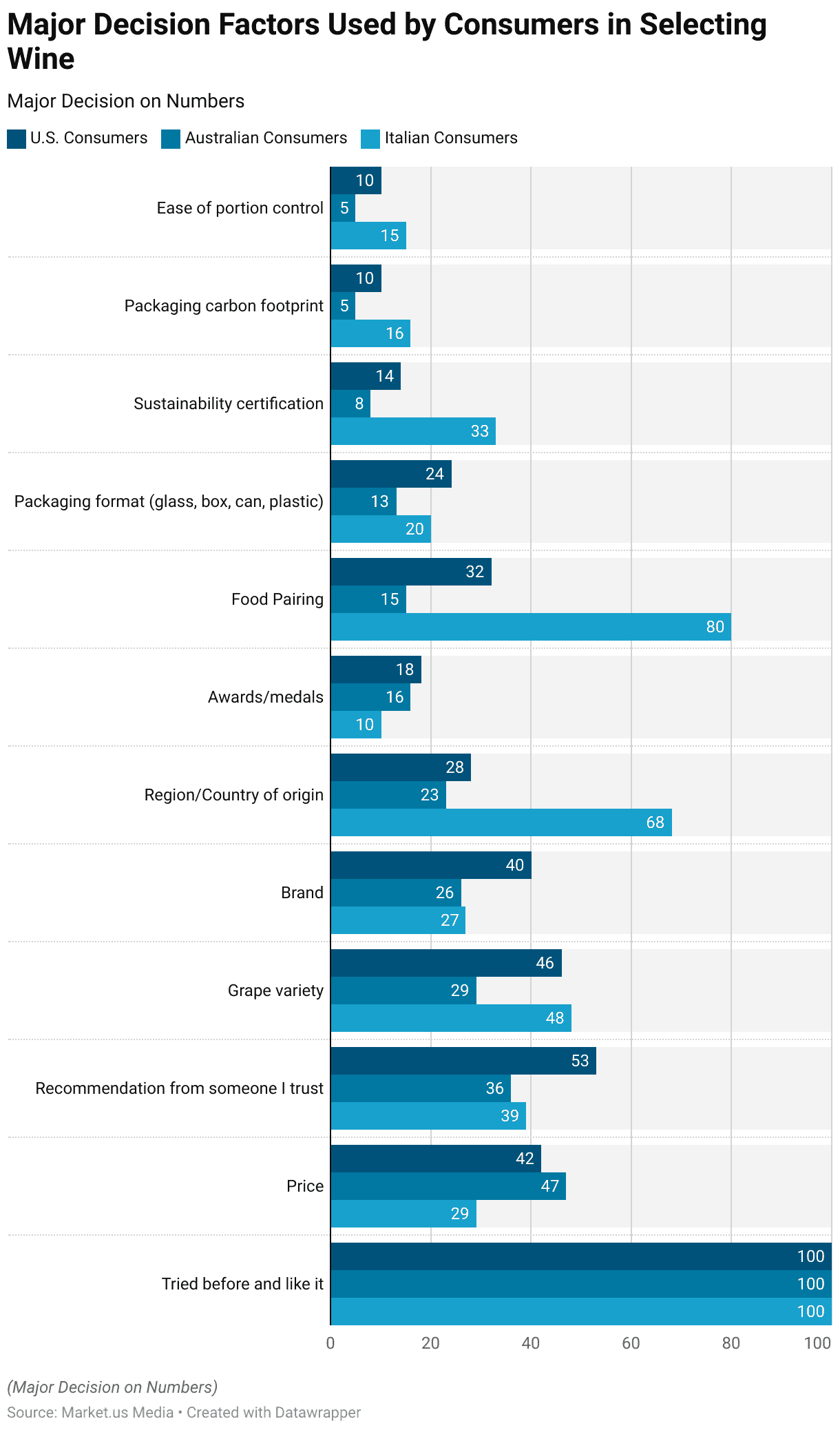

Consumer Choice Factors in Selecting Wine

- When selecting wine, consumers in the U.S., Australia, and Italy consider various decision factors with differing levels of importance.

- Universally, all consumers prioritize having tried the wine before and liking it, each scoring a perfect 100.

- Price is a significant factor, with U.S. consumers rating it at 42, Australians at 47, and Italians at 29.

- Recommendations from trusted sources are more influential among U.S. (53) and Italian (39) consumers compared to Australians (36).

- Grape variety holds high importance for Italian consumers (48), moderately for U.S. consumers (46), and less so for Australians (29). Brand importance scores are 40 for U.S. consumers, 26 for Australians, and 27 for Italians.

- The region or country of origin is highly significant for Italian consumers (68) but less so for U.S. (28) and Australian (23) consumers.

- Awards and medals have lower importance scores, with 18 for U.S. consumers, 16 for Australians, and 10 for Italians.

- Food pairing is notably important for Italian consumers (80), while U.S. (32) and Australian (15) consumers rate it lower.

- Packaging format scores are 24 for U.S. consumers, 13 for Australians, and 20 for Italians.

- Sustainability certification is more important to Italian consumers (33) than to U.S. (14) and Australian (8) consumers.

- The packaging’s carbon footprint scores are 10 for U.S. consumers, 5 for Australians, and 16 for Italians.

- Lastly, ease of portion control scores are 10 for U.S. consumers, 5 for Australians, and 15 for Italians.

(Source: Forbes)

Key Trends Related to Still Wine Owners Statistics

Insurance Premiums and Coverage Trends for Wineries

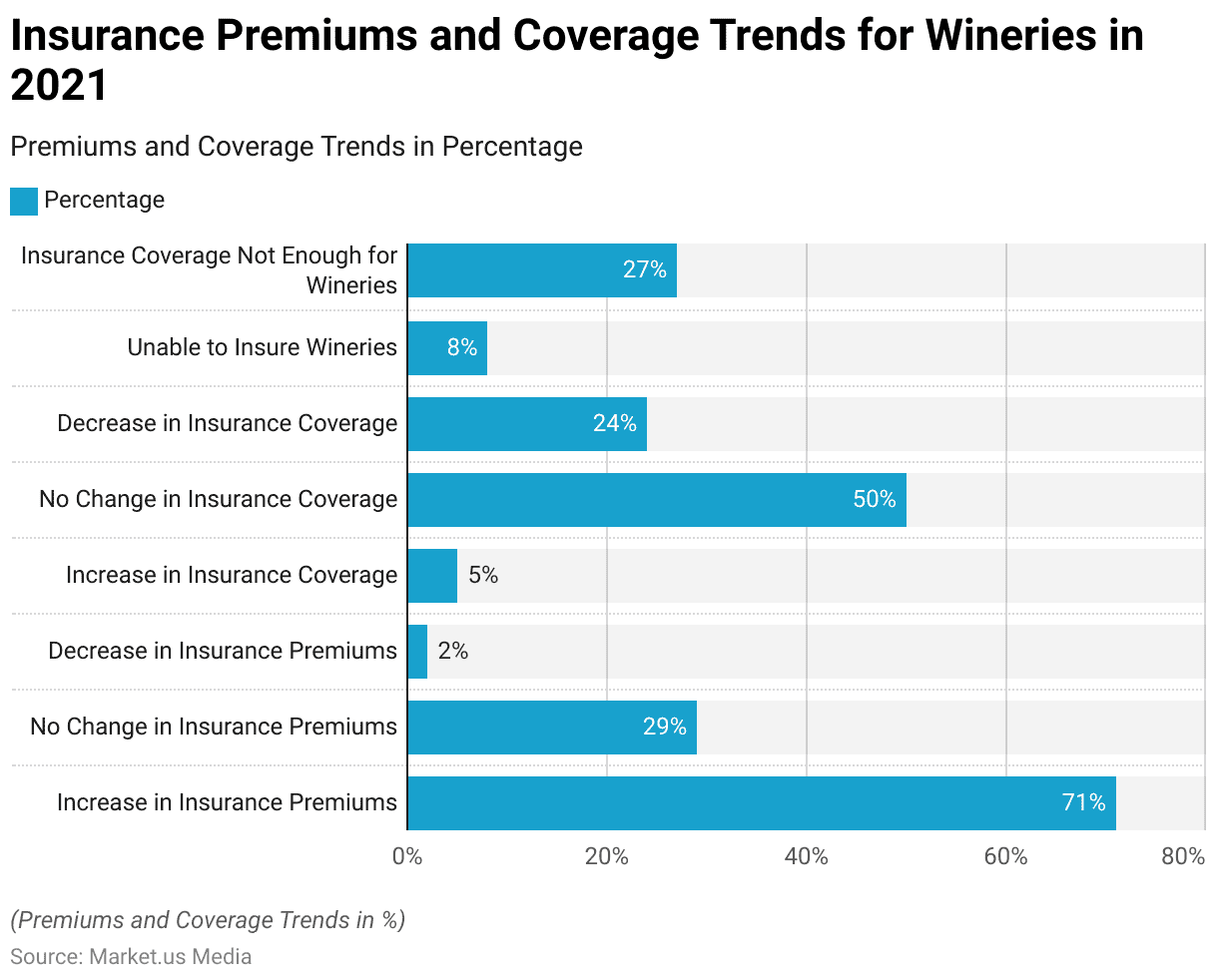

- According to wine industry statistics for the year 2021, 71% of winery owners reported an increase in their insurance premiums, while 29% indicated no change in their premiums.

- Only 2% of owners experienced a decrease in insurance premiums.

- Regarding insurance coverage, 5% of owners stated that their coverage had increased, whereas 50% reported that their coverage remained the same.

- Meanwhile, 24% of owners experienced a decrease in coverage, and 8% were unable to insure their wineries.

- Additionally, 27% of owners felt that their insurance coverage was not sufficient for their wineries.

(Source: Silicon Valley Bank)

Supply Difficulties in the Wine Industry

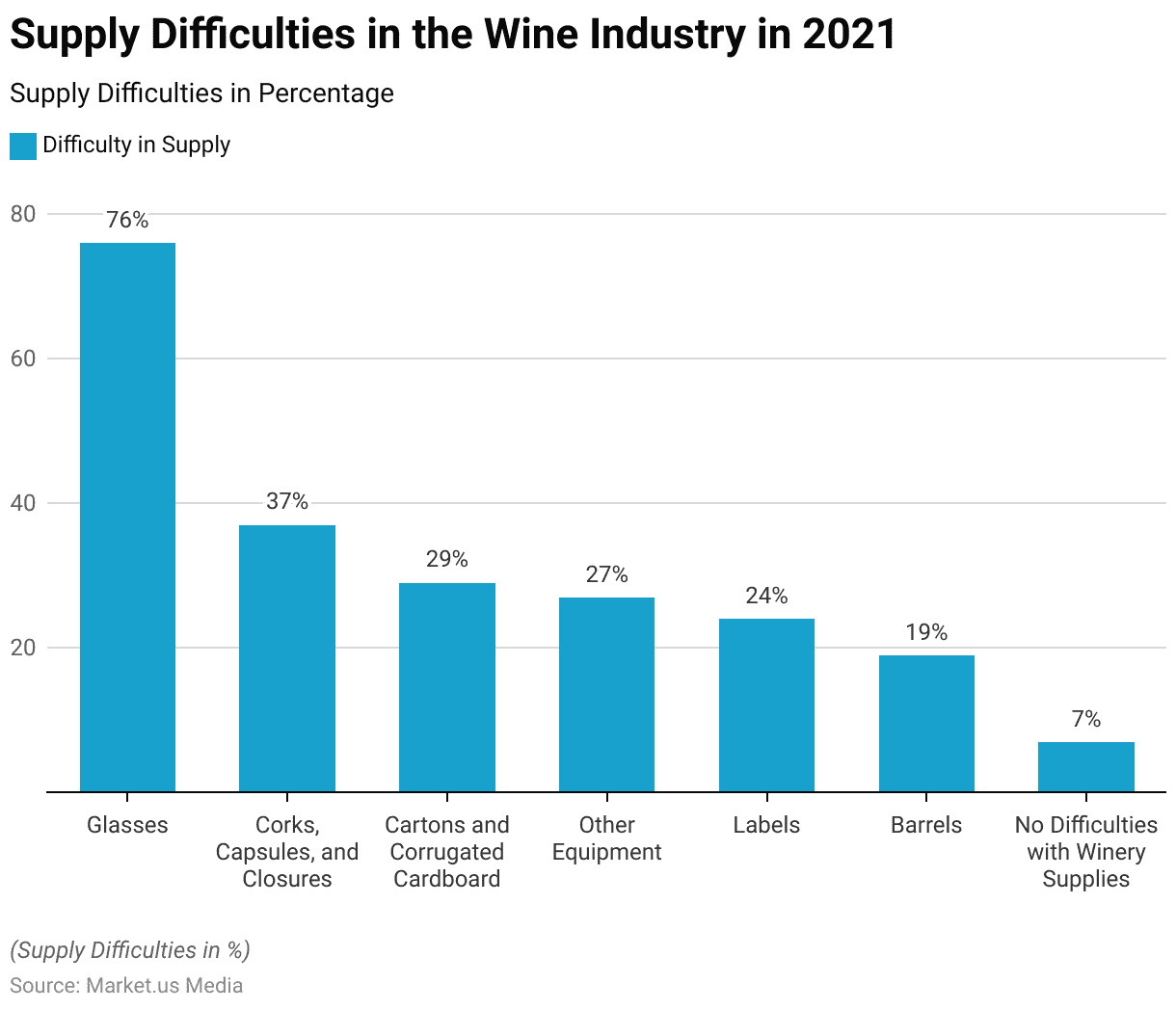

- As of 2021, the wine industry faced significant supply challenges, with glasses being the most difficult to supply, as reported by 76% of respondents.

- Corks, capsules, and closures followed, with a 37% difficulty rate.

- Cartons and corrugated cardboard recorded a 29% difficulty rate.

- Other equipment required in wineries had a supply difficulty rate of 27%.

- Labels and barrels were also challenging to supply, with difficulty rates of 24% and 19%, respectively.

- Notably, 7% of respondents reported no difficulties with winery supplies.

(Source: Silicon Valley Bank)

Recent Developments

Acquisitions:

- Brown‑Forman’s Acquisition of Diplomático Rum: Although primarily a rum acquisition, this move signifies a strategic expansion into premium spirits that complement their wine portfolio. Brown‑Forman’s continued investments in high-end brands enhance its market presence in both the wine and spirits industries.

- LVMH’s Acquisition of Joseph Phelps Vineyards: LVMH, a global luxury goods conglomerate, acquired Joseph Phelps Vineyards in Napa Valley for an estimated $400-$750 million. This acquisition underscores LVMH’s strategy to bolster its portfolio with high-quality wines, particularly in prestigious wine regions.

New Product Launches:

- JaM Cellars’ Expansion of Butter Line: JaM Cellars introduced two new wines, the 2023 Butter Sauv Blanc and the 2022 Butter Pinot Noir. These additions to the Butter line cater to the growing demand for easy-to-drink, flavorful wines.

- Innovations in Wine Packaging and Flavors: Companies are continuously innovating in terms of packaging and flavors. For example, several brands have introduced canned wines and eco-friendly packaging to appeal to environmentally conscious consumers.

Funding:

- Investment in Sustainable Practices: Many wineries are receiving funding to enhance sustainable wine production practices. This includes investments in organic vineyards, renewable energy sources, and water conservation technologies, aligning with the increasing consumer demand for eco-friendly products.

Market Growth:

- Growth of the Global Wine Market: The growth is driven by the rising popularity of premium wines and an expanding consumer base in emerging markets.

- Premium Wine Segment: Premium wines (priced above $12) continue to show positive sales growth, even as the overall wine market faces challenges. The premium segment benefits from increasing consumer interest in high-quality, authentic wine experiences.

Innovation and Trends:

- Blockchain for Traceability: The use of blockchain technology in the wine industry is being explored to enhance traceability and ensure the authenticity of wine products. This technology provides transparent documentation of each production stage, appealing to consumers seeking verified and certified wines.

- Rise of Non-Alcoholic and Low-Alcohol Wines: There is a growing trend towards non-alcoholic and low-alcohol wines, driven by health-conscious consumers. This segment is expanding rapidly, with innovations focusing on maintaining flavor while reducing alcohol content.

Conclusion

Still Wine Statistics – The still wine market has shown significant fluctuations and growth from 2018 to 2028, with revenue recovering post-pandemic and projected to increase.

Consumption volumes dipped during the pandemic but are gradually rising. Consumer preferences vary across age groups and ethnicities, with younger adults (21-34 years) and older adults (65+ years) being significant wine consumers and white individuals representing the largest ethnic group of wine drinkers.

The industry faces supply challenges, particularly with glass and corks, impacting production. Regional differences in consumer decision-making emphasize factors such as price, recommendations, and grape variety. Adapting to these changes and supply issues is crucial for continued growth.

FAQs

Still, wine is a type of wine that is not carbonated, meaning it does not have bubbles like sparkling wine or champagne. It is the most common type of wine and includes red, white, and rosé varieties.

Still wine is made by fermenting grape juice without carbonation. The fermentation process involves yeast converting the sugars in the grape juice into alcohol and carbon dioxide, which is allowed to escape, leaving the wine still.

The main types of still wine are red, white, and rosé. Each type is made using different grape varieties and winemaking techniques, resulting in a wide range of flavors and styles.

Consumers often consider factors such as taste, price, recommendations, grape variety, brand, region of origin, and food pairing when selecting still wine. Sustainability certifications and packaging format are also important for some buyers.

Recent trends in the still wine market include a growing preference for organic and sustainable wines, increased digital sales, and a rise in wine consumption among younger adults and older populations. Additionally, there are ongoing supply challenges, particularly with glass and corks.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)