Table of Contents

Overview

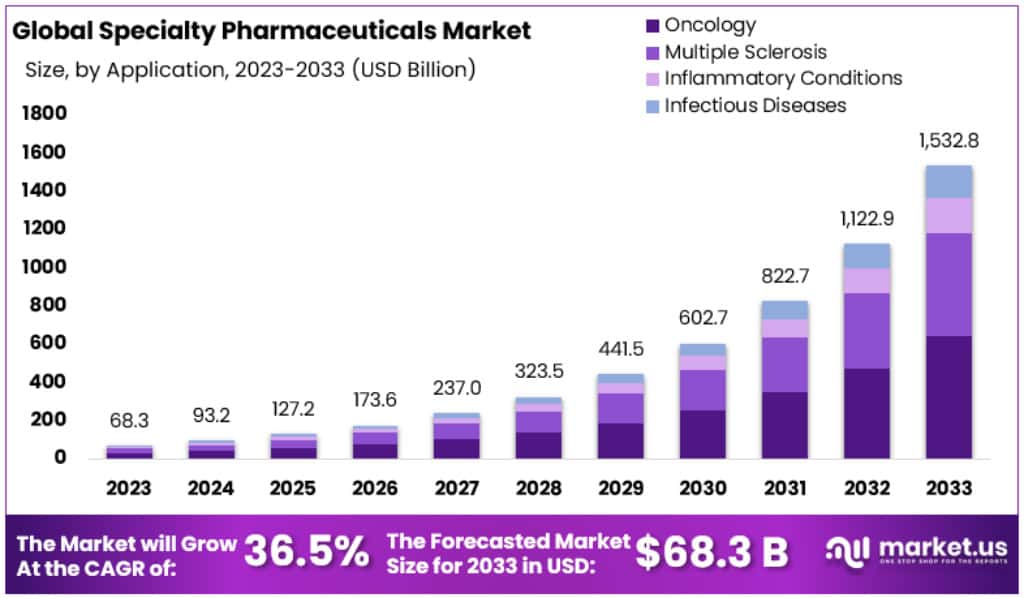

The Global Specialty Pharmaceutical Market is projected to expand from USD 68.3 billion in 2023 to approximately USD 1,532.8 billion by 2033, at a CAGR of 36.5%. Growth is being supported by the rising prevalence of chronic and rare diseases, particularly cancer, diabetes, autoimmune, and genetic conditions. These diseases create demand for advanced therapies where traditional drugs fail to deliver results. The steady increase in orphan drug approvals reflects the industry’s focus on addressing unmet medical needs, which is further reinforcing market expansion.

Advancements in biotechnology and precision medicine are creating new opportunities in specialty pharmaceuticals. Biologics, gene therapies, and cell-based therapies are being developed to target specific genetic profiles, improving treatment outcomes. This shift toward personalized medicine is attracting greater research and development investments. The acceleration of specialty drug pipelines is expected to drive significant innovation in the coming decade, establishing these therapies as essential components of modern healthcare.

Supportive regulatory frameworks are also contributing to growth. Governments and agencies are granting orphan drug designations, fast-track approvals, and tax incentives to stimulate innovation. These measures reduce the time and cost of development while offering market exclusivity to manufacturers. High therapy prices, combined with favorable approval pathways, make specialty drugs commercially viable despite smaller patient populations. This environment has positioned specialty pharmaceuticals as a profitable and competitive market segment.

Healthcare expenditure is rising globally, with payers acknowledging the long-term benefits of specialty drugs. These treatments reduce hospitalizations and improve patient outcomes, supporting value-based pricing and reimbursement models. At the same time, expanding distribution networks, including specialty pharmacies and digital health platforms, are enhancing access to high-cost therapies. Cold-chain management and logistics improvements are enabling the efficient supply of biologics and injectables across regions, which further strengthens market penetration.

Demographic shifts and strategic business activities are reinforcing market growth. The aging global population is driving demand for therapies in oncology, neurology, and immunology. Pharmaceutical firms are pursuing mergers, acquisitions, and partnerships to enhance their specialty drug portfolios and accelerate commercialization. With extended market exclusivity and premium pricing, specialty pharmaceuticals continue to generate high profit margins. This combination of demographic demand, scientific innovation, and strong financial incentives is expected to ensure sustained growth for the sector.

Key Takeaways

- The global specialty pharmaceutical market is projected to reach approximately USD 1,532.8 billion by 2033, showcasing strong expansion from its 2023 valuation.

- In 2023, the specialty pharmaceutical market was valued at USD 68.3 billion, reflecting the growing significance of advanced therapies and niche treatments worldwide.

- The market is expected to register a robust compound annual growth rate (CAGR) of 36.5% between 2023 and 2033, demonstrating accelerated industry momentum.

- Oncology emerged as the largest therapeutic segment in 2023, capturing over 42% market share, driven by rising cancer prevalence and innovative treatment approvals.

- Oral drug administration held the largest market share in 2023 at more than 45%, underscoring patient preference and ease of use compared to alternatives.

- Offline distribution channels dominated in 2023, representing over 56% market share, highlighting the continued reliance on pharmacies, hospitals, and physical healthcare infrastructure.

- North America led the global specialty pharmaceutical market with 54% share, equivalent to USD 36.8 billion, driven by advanced healthcare infrastructure and innovation.

Regional Analysis

North America led the specialty pharmaceutical market in 2023, with a 54% share valued at USD 36.8 billion. The strong position of this region was driven by high prevalence of chronic and rare diseases such as cancer, sickle cell disease, and HIV. The United States dominated within the region due to rising cancer cases, which reached over 2.2 million in 2020, and the significant impact of genetic disorders. Strong healthcare infrastructure and active pharmaceutical initiatives further reinforced this market leadership.

The region’s growth was supported by strategic industry initiatives and strong funding. Pharmaceutical companies focused on product launches, innovative collaborations, and FDA-backed orphan drug designations, particularly for rare conditions like multiple myeloma. Investments were also visible, including USD 13.5 million raised by Free Market Health in 2022. Furthermore, North America benefited from extensive R&D investments exceeding USD 149.8 billion annually. These initiatives positioned the region as a hub for pharmaceutical innovations, mergers, acquisitions, and advanced specialty pharmacy services.

Asia Pacific is projected to witness strong market expansion due to demographic trends and healthcare developments. The region’s large population, rising burden of chronic diseases, and rapid adoption of advanced technologies are key factors. According to the WHO, cardiovascular diseases alone are expected to cause 23.6 million deaths by 2030, mostly in low- and middle-income countries. Alongside this, government support, rising healthcare expenditure, and the presence of pharmaceutical manufacturers are expected to drive growth, positioning Asia Pacific as an emerging competitor in the specialty pharmaceutical industry.

Segmentation Analysis

In 2023, oncology held a dominant position in the specialty pharmaceutical market, capturing over 42% of the share. This growth was supported by the rising global prevalence of cancer and the growing need for targeted therapies. Personalized medicine also contributed, with treatments being designed according to patient genetic profiles. The multiple sclerosis segment also recorded significant expansion, due to rising incidence rates and active research in disease-modifying therapies. A robust pipeline targeting both relapsing-remitting and progressive forms of MS further supported its growth trajectory.

Inflammatory conditions formed another important segment, with demand supported by increased awareness of autoimmune disorders and chronic inflammation-related diseases. The availability of biologics and biosimilars has broadened treatment choices, leading to increased adoption. The infectious diseases segment continued to evolve, especially after the COVID-19 pandemic, focusing on antiviral drugs, vaccines, and antibiotics. Growing investment was observed to address drug-resistant infections and emerging pathogens. Together, these therapeutic areas highlighted the strong diversification of the specialty pharmaceutical market.

The oral route of administration dominated with more than 45% market share in 2023, largely driven by patient convenience and preference. Advances in formulation have improved oral treatment effectiveness in chronic disease management. The parenteral route, vital for biologics and rapid-acting therapies, also accounted for a significant share. Meanwhile, the transdermal route gained attention due to its non-invasive approach and sustained release features. In distribution channels, offline modes led with over 56% share, supported by trust and immediate access, while online platforms grew rapidly, reflecting digital transformation in healthcare delivery.

Key Players Analysis

The specialty pharmaceutical market is highly concentrated, with ten companies controlling around 60% of the global share. Teva Pharmaceutical Industries Ltd. is the largest player, holding nearly 40% of the market. The company relies heavily on specialty pharmaceuticals as a major revenue source. Pfizer Inc. is another strong competitor, with a market share of about 35%. Pfizer’s specialty portfolio mainly emphasizes oncology and biopharmaceuticals. Together, Teva and Pfizer dominate the segment, accounting for a substantial portion of overall market activity.

AbbVie Inc. has established a strong position in specialty pharmaceuticals, with around 85% of its total revenue derived from this segment. The company’s portfolio in biopharmaceuticals continues to strengthen its global presence. Similarly, Amgen Inc., a biotechnology firm, generates nearly all of its revenue—close to 100%—from specialty pharmaceutical products. Both AbbVie and Amgen maintain focused strategies, highlighting their dependence on specialty drug innovation. Their dominance underlines the importance of targeted therapeutic solutions in sustaining growth within this competitive market.

Other significant players include Johnson & Johnson and Bristol-Myers Squibb Company. Johnson & Johnson, a diversified healthcare leader, earns about 25% of its total revenue from specialty pharmaceuticals. Meanwhile, Bristol-Myers Squibb derives nearly 65% of its income from this sector, supported by its strong biopharmaceutical pipeline. These firms, though less concentrated in specialty drugs than AbbVie or Amgen, contribute considerably to overall market expansion. Their continued investments in innovative therapies are expected to support long-term growth, ensuring that competition within the specialty pharmaceutical industry remains intense.

Key Market Players

- Teva Pharmaceutical Industries Ltd.

- Pfizer Inc.

- AbbVie, Inc.

- Amgen Inc.

- Johnson and Johnson

- Bristol-Myers Squibb Company

- Novo Nordisk

- Novartis AG

- Gilead Sciences, Inc.

- Sanofi S.A.

FAQ

1. What are specialty pharmaceuticals?

Specialty pharmaceuticals are advanced medicines designed to treat complex, chronic, or rare conditions. These drugs are often prescribed for diseases such as cancer, multiple sclerosis, and genetic disorders. They usually require special storage, handling, or administration and may need ongoing monitoring for safety. Unlike common medications, specialty drugs are more targeted and personalized. They play a vital role in improving patient outcomes, especially when standard treatments fail. Their development has become essential for modern healthcare systems.

2. How are specialty pharmaceuticals different from traditional drugs?

Specialty pharmaceuticals differ from traditional drugs in cost, complexity, and treatment approach. Traditional drugs are mass-produced and widely prescribed, while specialty medicines are developed for specific diseases or smaller patient groups. They are often biologics, made from living cells, which makes them harder to produce. Many require refrigeration, injection, or hospital-based care. They also need patient monitoring to ensure safety and effectiveness. Because of their precision and impact, these therapies are changing how chronic and rare diseases are treated.

3. What are some examples of specialty pharmaceuticals?

Examples of specialty pharmaceuticals include biologics, monoclonal antibodies, and cell or gene therapies. Well-known drugs such as Humira for rheumatoid arthritis, Keytruda for cancer, and CAR-T therapies for blood disorders are part of this category. Enzyme replacement therapies and oral oncology drugs are also considered specialty medicines. These treatments address conditions that often lack alternatives, offering patients new hope. Their highly specific design makes them powerful tools in personalized medicine. These drugs continue to transform treatment approaches worldwide.

4. Why are specialty pharmaceuticals expensive?

Specialty pharmaceuticals are expensive because their development and production are complex. Research and development often take years and involve high costs, especially for rare or orphan diseases. Manufacturing biologics or gene therapies requires advanced technology and careful handling. The patient population is usually small, so costs must be recovered through higher prices. Strict regulations also increase expenses, as safety and monitoring are essential. These combined factors make specialty medicines some of the costliest drugs available on the global market.

5. How are specialty pharmaceuticals distributed?

Specialty pharmaceuticals are distributed mainly through specialty pharmacies rather than regular retail outlets. These pharmacies are equipped to handle drugs requiring refrigeration or special packaging. They also provide patient support, such as education, adherence programs, and follow-up care. Many specialty medicines require prior authorization, so these pharmacies help patients manage insurance approvals. Distribution channels are closely monitored to ensure safety and compliance. This system ensures patients receive the right medicine, along with the support needed to use it effectively.

6. What role do payers and insurers play?

Payers and insurers play a central role in determining patient access to specialty pharmaceuticals. Due to their high cost, insurers often require prior authorization or step therapy before approving coverage. They may also use formulary placement to control availability and cost-sharing. Patients often face higher copays for these medicines, making insurance coverage critical. By managing reimbursement and pricing negotiations, insurers influence how quickly and widely these drugs reach patients. Their decisions directly affect affordability and market access worldwide.

7. What is the size of the specialty pharmaceutical market?

The specialty pharmaceutical market represents a significant portion of global drug spending. Specialty Pharmaceutical Market size is expected to be worth around USD 1532.8 billion by 2033, from USD 68.3 billion in 2023, growing at a CAGR of 36.5% during the forecast period from 2023 to 2033. The market is expanding as more patients require advanced therapies for chronic and rare conditions. Rising demand for biologics, gene therapies, and personalized medicine supports this growth. Global healthcare systems continue to allocate larger budgets to specialty drugs, making them central to future medical care.

8. What factors are driving market growth?

Market growth in specialty pharmaceuticals is driven by rising cases of chronic and rare diseases. The growing demand for biologics, biosimilars, and gene therapies also plays a strong role. Advancements in precision medicine allow treatments tailored to specific patients, boosting effectiveness. Ongoing research and development pipelines introduce innovative drugs each year. Improved healthcare access in emerging economies further supports adoption. Together, these factors create steady demand. As healthcare providers and patients seek more targeted therapies, the market continues to expand.

9. What are the major challenges in the market?

The specialty pharmaceutical market faces several challenges that limit its growth. High costs remain the biggest barrier for patients and healthcare systems. Regulatory approval processes are complex and take time, delaying drug availability. Distribution requires specialized logistics, making supply chains difficult to manage. Payers often restrict access through strict reimbursement policies, affecting patient affordability. Competition from biosimilars is growing, but adoption varies by region. These challenges must be managed carefully to balance innovation, patient access, and cost control.

10. Which regions dominate the specialty pharmaceutical market?

North America, particularly the United States, dominates the specialty pharmaceutical market due to high spending, advanced healthcare systems, and strong innovation pipelines. Europe follows with widespread adoption of biologics and favorable reimbursement policies in certain countries. The Asia-Pacific region is experiencing rapid growth, driven by expanding healthcare infrastructure and increasing patient demand. Latin America and the Middle East are also emerging markets with improving access. Global differences in regulation, cost, and healthcare systems influence how each region develops.

11. Who are the key players in the specialty pharmaceutical market?

Key players in the specialty pharmaceutical market include leading pharmaceutical giants and specialty pharmacies. Companies such as Roche, Johnson & Johnson, Novartis, AbbVie, Bristol-Myers Squibb, and Pfizer dominate with strong portfolios in biologics and oncology. Specialty pharmacies like CVS Specialty, Walgreens Boots Alliance, and OptumRx provide distribution and patient support services. These organizations work together to improve access and affordability. Collaborations between manufacturers, payers, and pharmacies are becoming essential for ensuring market growth and delivering effective patient care.

12. What is the future outlook for the specialty pharmaceutical market?

The future outlook for the specialty pharmaceutical market is positive, with steady growth expected worldwide. Advances in gene and cell therapies are likely to drive innovation. Expansion of biosimilars will help reduce costs and increase accessibility. Rising demand for precision medicine ensures continued investment in targeted therapies. Collaborations between drugmakers, insurers, and specialty pharmacies will improve access and affordability. With healthcare systems prioritizing advanced treatments, specialty pharmaceuticals are set to remain a central part of modern medical care.

Conclusion

The specialty pharmaceutical market is set to grow rapidly as demand for advanced treatments continues to rise. Growth is being fueled by the increasing prevalence of chronic and rare diseases, greater adoption of biologics and gene therapies, and the steady push toward personalized medicine. Supportive regulations, strong R&D pipelines, and higher healthcare spending are creating a favorable environment for innovation and market expansion. Strategic collaborations, mergers, and acquisitions are also strengthening competitive positions. With strong opportunities in oncology, neurology, and immunology, specialty pharmaceuticals are becoming central to modern healthcare, ensuring better patient outcomes and driving sustainable long-term growth in the industry.

View More

Radiopharmaceuticals Market || Pharmaceutical Excipients Market || Generic Pharmaceuticals Market || NanoPharmaceuticals Market || Generative AI In Pharmaceutical Market || Pharmaceuticals Market || Pharmaceutical Manufacturing Market || Pharmaceutical Quality Management Software Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)