Table of Contents

Overview

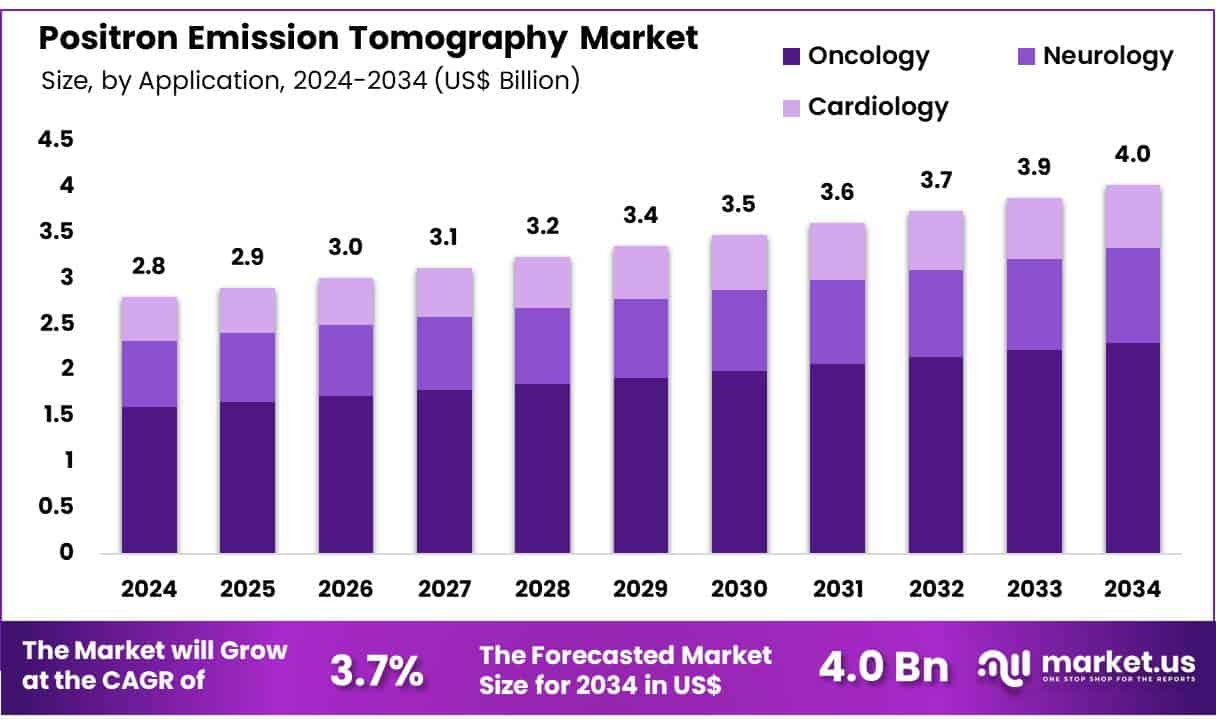

New York, NY – June 03, 2025 – Global Positron Emission Tomography Market size is expected to be worth around US$ 4.0 billion by 2034 from US$ 2.8 billion in 2024, growing at a CAGR of 3.7% during the forecast period 2025 to 2034

Positron Emission Tomography (PET) is a highly advanced nuclear imaging technique that plays a crucial role in diagnosing and monitoring a range of diseases, including cancer, neurological disorders, and cardiovascular conditions. PET scans provide real-time, three-dimensional imaging of metabolic and biochemical activity within the body, offering superior sensitivity compared to traditional imaging methods.

The global demand for PET technology is rising steadily due to the increasing prevalence of chronic illnesses, particularly cancer, where early and accurate detection is critical for treatment planning. PET imaging is widely used in oncology for tumor detection, staging, and therapy response assessment. Additionally, its application in neurology is expanding, especially for evaluating conditions such as Alzheimer’s disease and epilepsy.

Advancements in radiotracer development, the integration of PET with CT and MRI systems, and growing investment in precision diagnostics are driving market expansion. The growing adoption of hybrid imaging systems and AI-enabled image analysis tools is enhancing diagnostic accuracy and workflow efficiency across medical facilities.

Hospitals, diagnostic centers, and research institutions are the primary end users of PET systems, supported by favorable reimbursement policies and rising healthcare infrastructure investments. As the focus on early disease detection and personalized medicine intensifies, PET technology continues to be a vital component in advancing clinical diagnostics and improving patient care outcomes worldwide.

Key Takeaways

- Market Overview (2023): The global positron emission tomography (PET) market generated a revenue of USD 8 billion in 2023 and is projected to reach USD 4.0 billion by 2033, registering a CAGR of 3.7% during the forecast period.

- By Product Type: The market is segmented into PET-CT and PET-MRI systems. PET-CT emerged as the leading product type in 2023, accounting for a market share of 68.4%, due to its widespread clinical adoption and diagnostic precision.

- By Application: PET systems are utilized across oncology, neurology, and cardiology. Among these, oncology remained the dominant application in 2023, contributing 57.2% of the total market share, supported by increasing cancer prevalence and demand for precise tumor imaging.

- By End User: The end-user segment includes hospitals, academic & research institutes, and diagnostic imaging centers. Hospitals held the leading position in 2023 with a 62.7% revenue share, reflecting the high volume of imaging procedures and integration of PET in clinical workflows.

- By Region: North America led the global PET market in 2023, capturing a 40.3% share, attributed to advanced healthcare infrastructure, favorable reimbursement policies, and rising adoption of hybrid imaging technologies.

Segmentation Analysis

- Product Type Analysis: In 2023, the PET-CT segment dominated the market with a 68.4% share, driven by its ability to merge functional and anatomical imaging for accurate diagnostics. The rising cancer burden and demand for precise staging and treatment planning are key growth drivers. Additionally, continuous advancements in hybrid imaging technologies and increasing clinical adoption are expected to further accelerate the use of PET-CT systems in diagnostic and therapeutic applications.

- Application Analysis: Oncology held the largest application share at 57.2% in 2023, as PET scans play a central role in cancer detection, staging, and treatment monitoring. The growth of this segment is supported by rising global cancer incidence, innovations in radiotracer development, and the increasing shift toward personalized medicine. PET imaging enables more accurate and individualized cancer care, which is expected to further increase its utilization in oncology practices worldwide.

- End-User Analysis: Hospitals accounted for 62.7% of the PET market revenue in 2023 due to their advanced infrastructure and high patient throughput. The growing need for accurate diagnostic tools in critical care, particularly for oncology and neurology, supports this dominance. Increased healthcare investments and technological advancements are enhancing PET adoption in hospital settings, allowing for more effective diagnosis, improved treatment planning, and better patient outcomes in complex medical conditions.

Market Segments

Product Type

- PET-CT

- PET-MRI

Application

- Oncology

- Neurology

- Cardiology

End-user

- Hospitals

- Academic & Research Institutes

- Diagnostic Imaging Centers

Regional Analysis

North America led the positron emission tomography (PET) market in 2023, accounting for 40.3% of the global revenue. This dominance is attributed to technological advancements, rising adoption of innovative diagnostic systems, and a strong presence of key players in the U.S. and Canada. Innovations like CDL Nuclear Technologies’ Mobile Cardiac PET/CT Trailer have improved imaging access, especially in underserved areas.

The increasing prevalence of chronic diseases such as cancer and cardiovascular disorders, along with government support for early diagnosis and rising healthcare spending, continues to drive demand. Collaborative efforts between manufacturers and research institutions have resulted in improved imaging precision and reduced radiation exposure, supporting market growth.

Meanwhile, the Asia Pacific region is projected to register the fastest CAGR during the forecast period. This growth is driven by expanding healthcare infrastructure, rising cancer incidence, and increasing demand for early diagnostic solutions. Launches such as Minfound Medical’s ScintCare TOF PET/CT system in China highlight the region’s commitment to cutting-edge technology. Factors including growing healthcare expenditure, local manufacturing initiatives, medical tourism, and advancements in PET/CT and PET/MRI are expected to further boost market expansion.

Emerging Trends

Recent advancements in time-of-flight (TOF) technology have markedly enhanced image resolution and accuracy in PET scans. The growth of TOF-PET systems can be attributed to their ability to reduce noise and improve signal to noise ratio, leading to clearer images of small lesions.

Dual tracer acquisition methods are gaining prominence, allowing simultaneous imaging of two radiotracers to capture multiple physiological processes in one session. This approach can reduce total scanning time by up to 30% compared to sequential scans and offers more comprehensive insights into tumor metabolism versus perfusion.

Hybrid imaging systems that combine PET with magnetic resonance imaging (PET/MRI) are increasingly adopted in clinical settings. These systems leverage MRI’s superior soft tissue contrast alongside PET’s metabolic data, improving characterization of brain, liver, and prostate lesions. One study noted up to a 15% improvement in lesion detectability in head and neck cancers when using PET/MRI compared with PET/CT.

Novel radiotracers continue to expand PET’s diagnostic scope. For example, PSMA-targeted agents such as Ga-68 PSMA-11 and piflufolastat F-18 have been approved for detecting prostate cancer recurrence, demonstrating detection rates above 85% in men with suspected recurrence. Additionally, tracer developments for imaging neuroinflammation and gliosis using ligands specific to activated microglia are under investigation to better understand neurodegenerative diseases.

Artificial intelligence (AI) is increasingly integrated into PET reconstruction and image analysis workflows. FDA-approved AI tools now provide semi-automated lesion segmentation, reducing interoperator variability by approximately 20% and accelerating reporting times by 25%.

Use Cases

Oncologic imaging remains PET’s primary application. In lymphoma staging, ^18F-FDG PET/CT correctly identified B-cell lymphoma in 92% (12/13) of cases and diffuse large B-cell lymphoma (DLBCL) in 100% (9/9) of cases, guiding more accurate treatment plans. PSMA-targeted PET has improved detection of prostate cancer lesions: one trial reported that ^68Ga-PSMA-11 PET identified lesions in 78% of men with biochemical recurrence at PSA levels below 1 ng/mL.

In cardiology, PET myocardial perfusion imaging (MPI) is used to assess coronary artery disease. Recent research focuses on multiparametric PET MPI to evaluate both perfusion and metabolic markers of plaque activity; early studies show this dual parameter approach can improve risk stratification by 12% over conventional MPI alone.

Neurology benefits from PET tracers that target β-amyloid in Alzheimer’s disease. Florbetapir F-18 (Amyvid) received FDA clearance for estimating cortical amyloid plaque density; in clinical trials, Amyvid PET had 96% sensitivity and 95% specificity for detecting moderate to frequent plaque density.

PET/CT is also employed to detect infectious and inflammatory conditions. During the COVID-19 pandemic, PET/CT scans demonstrated 93.8% specificity and 92.9% accuracy for identifying COVID-related pulmonary inflammation in asymptomatic cancer patients, aiding early intervention.

In preclinical research, PET combined with electron paramagnetic resonance imaging (EPRI) is used to assess tumor hypoxia. In mouse models, ^18F-FMISO PET/EPRI systems quantified tumor oxygenation with under 5 mmHg precision, facilitating the development of hypoxia-targeted therapies.

Cervical cancer staging utilizes PET to evaluate lymph node status. A meta-analysis of 445 patients reported pooled sensitivity of 83% and specificity of 88% for ^18F-FDG PET in preoperative lymph node assessment, improving surgical planning. Overall, PET’s broadening radiotracer repertoire and integration with AI and hybrid imaging are driving its use beyond traditional oncology, into neurology, cardiology, infectious diseases, and translational research.

Conclusion

The global positron emission tomography (PET) market is advancing steadily, driven by rising chronic disease prevalence, innovation in radiotracers, and the integration of hybrid imaging technologies. Its critical role in oncology, neurology, and cardiology is being reinforced by emerging trends such as time-of-flight PET, AI integration, and dual tracer imaging.

Expanding applications, supportive healthcare investments, and regional growth particularly in Asia Pacific underscore PET’s evolving significance in precision diagnostics. As the demand for early detection and personalized treatment intensifies, PET imaging is expected to remain an indispensable tool for enhancing diagnostic accuracy and improving patient outcomes worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)