Table of Contents

Overview

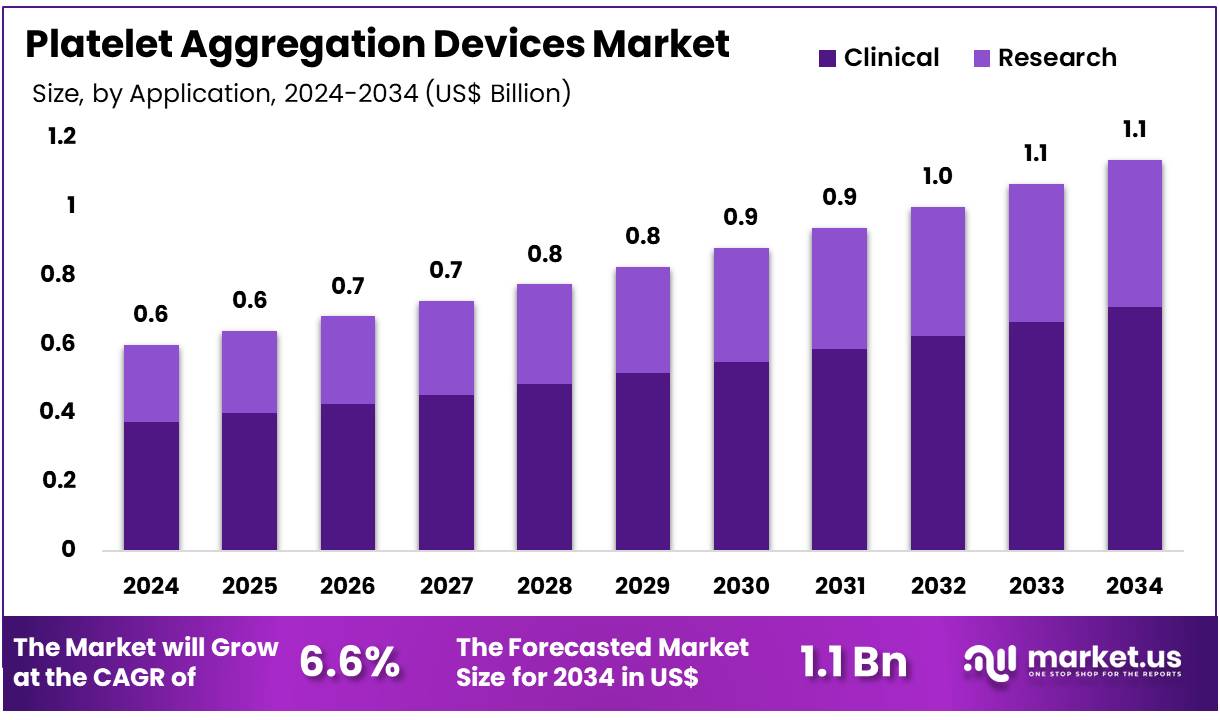

New York, NY – Nov 04, 2025 – The Global Platelet Aggregation Devices Market size is expected to be worth around US$ 1.1 Billion by 2034 from US$ 0.6 Billion in 2024, growing at a CAGR of 6.6% during the forecast period 2025 to 2034. In 2023, North America led the market, achieving over 40.1% share with a revenue of US$ 0.2 Billion.

The global platelet aggregation devices market is expected to witness notable expansion in the coming years. The growth of the market can be attributed to the increasing prevalence of cardiovascular disorders, diabetes, and blood coagulation abnormalities across developed and emerging economies. Technological advancements in automated systems and the rising adoption of point-of-care diagnostics have further supported market penetration.

Platelet aggregation devices are widely utilized in clinical laboratories, research centers, and hospital settings to evaluate platelet function for disease diagnosis, monitoring antiplatelet therapies, and pre-surgical assessment. The demand for precise hemostasis testing solutions has been strengthened due to the growing number of surgical procedures and heightened focus on personalized medicine. In addition, an increase in awareness regarding early diagnosis of thrombotic conditions has played a significant role in boosting market demand.

North America is expected to account for a dominant share of the market due to advanced healthcare infrastructure, high diagnostic adoption rates, and substantial investment in medical research. Meanwhile, Asia-Pacific is projected to record the fastest growth, supported by improving healthcare systems and rising patient awareness.

Leading market participants are undertaking product development initiatives, strategic partnerships, and regulatory approvals to strengthen their competitive position. Continuous innovation in platelet function testing technologies is anticipated to reinforce industry growth prospects. Growing focus on laboratory automation and demand for fast, accurate results are expected to sustain a positive market trajectory.

Key Takeaways

- In 2023, the global Platelet Aggregation Devices market recorded revenue of US$ 6 billion. The market has been expanding at a CAGR of 6.6% and is projected to achieve a valuation of US$ 1.1 billion by 2033.

- Based on product type, the market is segmented into systems, consumables, reagents, and accessories. Systems accounted for the highest share in 2023, representing 38.6% of total revenue.

- By application, the market is classified into clinical and research uses. The clinical segment dominated the industry, contributing 62.5% of the overall market share.

- In terms of end users, diagnostic laboratories, hospitals, and other facilities form the key segments. Hospitals emerged as the leading end-user category, holding a revenue share of 49.7% in 2023.

- Regionally, North America held the largest share of the market, representing 40.1% of global revenue in 2023.

Regional Analysis

North America remains the leading region in the Platelet Aggregation Devices market, capturing a 40.1% revenue share. The dominance of this region is attributed to the growing requirement for precise diagnostic solutions for blood-related disorders such as leukemia, lymphoma, and myeloma.

According to the Leukemia & Lymphoma Society, these conditions were projected to account for 9.4% of nearly 1.96 million new cancer cases in the United States. In addition, non-Hodgkin lymphoma alone represented approximately 4% of all cancer diagnoses, reinforcing the demand for advanced diagnostic and therapeutic equipment.

Platelet aggregation devices are essential for evaluating platelet function and supporting the diagnosis and management of hematologic disorders, particularly in patients receiving chemotherapy or experiencing bleeding complications.

Increased emphasis on personalized medicine, heightened health awareness, and continuous technological advancements have further strengthened market growth in North America. With expanding investments in advanced diagnostics across the healthcare system, the region is expected to sustain its leading position, supporting improved clinical outcomes for individuals with blood disorders.

Asia Pacific is projected to witness the fastest growth rate over the forecast period. This regional expansion is driven by rising cases of cardiovascular disorders, greater healthcare spending, and rapid advancements in diagnostic technologies. Major countries such as China, India, and Japan are expected to show strong uptake of platelet aggregation devices due to increasing incidences of heart disease, stroke, and thrombotic conditions.

Use Cases

- Antiplatelet Therapy Monitoring: Quantitative platelet aggregation testing assists in identifying resistance to antiplatelet medications, such as aspirin, which may affect up to 27% of users. This capability enables clinicians to tailor antithrombotic treatment plans and lower the risks of both excessive bleeding and thrombotic events.

- Cardiovascular Risk Stratification: Rapid bedside platelet function assessment plays a vital role in managing acute thrombotic events, including acute coronary syndrome. With over 356,000 out-of-hospital cardiac arrests reported annually in the United States, timely testing supports urgent therapeutic decisions, including P2Y12 inhibitor dosing and mechanical intervention requirements.

- Diagnosis of Bleeding Disorders: Testing of platelet–von Willebrand factor interaction is critical in diagnosing bleeding conditions such as von Willebrand disease, which affects an estimated 1% of the population, representing approximately 3.2 million individuals in the United States. This evaluation helps detect platelet adhesion and aggregation deficiencies.

- Transfusion and Perioperative Management: Point-of-care platelet function testing guides transfusion strategies during surgical and trauma care by offering real-time insight into platelet activity. These assessments support optimal transfusion utilization and enhance hemostatic management, reducing complications associated with excessive or insufficient blood product use.

- Personalized Antithrombotic Drug Development: Advanced platelet aggregation technologies facilitate personalized drug evaluation by measuring individual patient responses to emerging direct oral anticoagulants and antiplatelet therapies. This capability supports dose-optimization research and contributes to minimizing adverse events in clinical trials.

Frequently Asked Questions on Platelet Aggregation Devices

- What are platelet aggregation devices?

Platelet aggregation devices are diagnostic instruments used to evaluate platelet function by measuring how blood platelets clump together. These devices assist in identifying bleeding disorders, monitoring antiplatelet therapies, and supporting clinical decision-making in hematology and cardiovascular care. - How do platelet aggregation devices work?

These devices assess platelet activity by exposing blood samples to specific agonists and measuring the resulting platelet response. The analysis helps determine clotting efficiency and platelet function abnormalities, aiding clinicians in diagnosing and managing various hematologic and cardiovascular disorders. - Why are platelet aggregation devices important in clinical practice?

Their importance lies in accurate detection and management of platelet-related disorders, particularly in patients undergoing surgeries, chemotherapy, or antiplatelet therapy. They enable personalized treatment decisions, improving patient outcomes in bleeding disorders and thrombotic disease management. - What conditions require platelet aggregation testing?

Platelet aggregation testing is conducted for conditions such as bleeding disorders, platelet dysfunction, cardiovascular diseases, and monitoring of antiplatelet medication effects. This testing is also valuable in patients with suspected clotting abnormalities or undergoing hematologic evaluation. - What types of platelet aggregation devices are available?

Available devices include optical aggregometers, impedance aggregometers, and flow cytometry-based systems. Consumables, reagents, and accessories support testing. Advanced automated models offer higher accuracy, reduced manual intervention, and enhanced clinical workflow efficiency in diagnostic settings. - Which product segment holds the largest share in this market?

Systems currently represent the largest product segment, supported by widespread utilization in clinical laboratories and hospitals. Their advanced features, automation benefits, and high diagnostic accuracy have contributed significantly to market leadership in recent years. - Which end-user segment leads the platelet aggregation devices market?

Hospitals dominate the end-user segment due to higher patient inflow, advanced laboratory infrastructure, and greater adoption of sophisticated diagnostic systems. Increasing emphasis on accurate platelet function assessment in critical care settings reinforces hospital-based demand. - Which region currently dominates the platelet aggregation devices market?

North America holds the leading market share, attributed to strong healthcare infrastructure, high prevalence of hematologic and cardiovascular disorders, and early adoption of advanced diagnostic technologies. Continuous investments in healthcare innovation further strengthen regional leadership.

Conclusion

The platelet aggregation devices market is positioned for sustained expansion, driven by rising incidences of cardiovascular diseases, coagulation disorders, and diabetes across major global regions. Increasing reliance on precision diagnostics, growing surgical volumes, and demand for personalized medicine continue to elevate adoption in clinical and research environments.

Technological innovations, including automated platforms and point-of-care systems, are enhancing accuracy and efficiency, strengthening market prospects. North America currently leads due to advanced healthcare systems and strong research focus, while Asia Pacific is set for rapid growth supported by improving medical infrastructure. Overall, continuous product advancements and strategic industry initiatives are expected to support long-term market growth.