Table of Contents

Overview

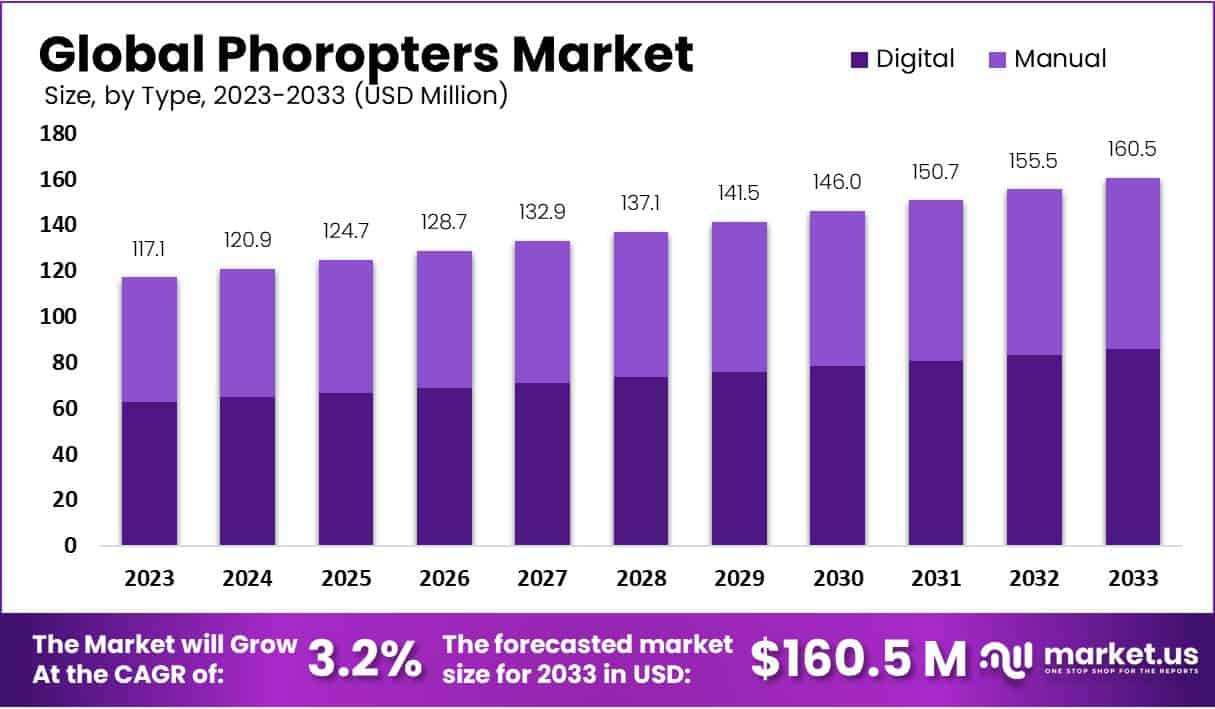

The global phoropters market is projected to grow from USD 117.1 million in 2023 to approximately USD 160.5 million by 2033, registering a CAGR of 3.2% during the forecast period. This steady growth is primarily driven by the rising prevalence of vision disorders and refractive errors worldwide. According to the World Health Organization (WHO), more than 2 billion people live with vision impairment, half of which are preventable or untreated. Increased screen exposure, urbanization, and changing lifestyles have amplified cases of myopia and astigmatism, particularly among children and young adults, thereby boosting the demand for accurate eye examination tools such as phoropters.

The expanding aging population is another major growth catalyst. As per the United Nations, the global population aged 60 years and above will double to 2.1 billion by 2050. Aging leads to conditions like presbyopia and cataracts, increasing the need for regular vision assessments. This demographic trend is driving hospitals and optometry centers to expand their diagnostic facilities, directly supporting the demand for advanced phoropters. The rise in routine eye check-ups among older adults contributes to the sustained adoption of precision refraction instruments in clinical settings.

Technological advancements have significantly transformed the phoropters market. The introduction of digital and automated models has improved diagnostic accuracy and workflow efficiency. Integration with electronic medical records (EMR) and tele-optometry platforms enables remote diagnostics and streamlined patient management. The post-pandemic emphasis on digital healthcare has accelerated the adoption of connected, software-driven phoropters. These systems offer enhanced precision, faster testing times, and greater ease of use for practitioners, ensuring long-term market relevance.

Emerging economies are witnessing rapid development in eye-care infrastructure through government and non-profit initiatives. Programs led by organizations such as the International Agency for the Prevention of Blindness (IAPB) and Vision 2020 have expanded access to vision screening and low-cost diagnostic tools. The introduction of portable and affordable phoropters in regions across Asia, Africa, and Latin America has further strengthened market penetration. Rising public awareness of preventive eye care, supported by school and workplace vision screening campaigns, continues to stimulate demand.

The phoropters sector is expected to maintain steady growth driven by demographic changes, healthcare expansion, and continuous innovation. Increasing investment in eye hospitals, optometry schools, and diagnostic centers, coupled with the growth of the eyewear and contact lens industry, reinforces the importance of phoropters in modern vision care. Future trends will likely focus on digital connectivity, miniaturization, and remote usability, ensuring that phoropters remain essential diagnostic tools in global eye-health management.

Key Takeaways

- The global phoropters market is projected to reach USD 160.5 million by 2033, growing at a steady 3.2% CAGR from 2024 to 2033.

- In 2023, the market was valued at USD 117.1 million, reflecting steady expansion supported by rising adoption in ophthalmic diagnostics.

- Digital phoropters dominated with 53.6% market share in 2023, driven by automation, precision, and seamless integration with digital ophthalmic systems.

- Manual phoropters trailed behind as healthcare providers favored advanced digital systems for accuracy and efficiency in refraction assessments.

- Specialty clinics led the end-user segment with 42.5% market share in 2023, underscoring the trend toward specialized diagnostic care environments.

- The increasing burden of eye disorders globally has significantly contributed to the rising adoption of advanced phoropter systems.

- Technological advancements, including automated measurement and digital connectivity, have been major catalysts for market growth.

- The aging global population has led to higher prevalence of vision impairments, increasing demand for precise refractive testing solutions.

- North America held a dominant 39.9% market share in 2023, valued at USD 46.7 million, due to strong technology adoption and infrastructure.

- Strategic partnerships among manufacturers and healthcare providers in North America have strengthened market presence and innovation.

- High initial investment requirements and maintenance costs remain key barriers to widespread adoption of phoropters globally.

- Limited reimbursement coverage for vision diagnostics has restricted accessibility, particularly in cost-sensitive healthcare markets.

- Disruptions in global supply chains have occasionally hindered production and timely distribution of phoropters.

- Emerging markets in Asia-Pacific and Latin America are expected to offer lucrative opportunities due to expanding healthcare access.

- The integration of teleophthalmology is anticipated to transform remote diagnostic capabilities and expand the phoropter’s application scope.

- Customization options in digital phoropters are gaining traction, enabling tailored solutions for specific clinical requirements.

- Collaborative research and development initiatives are driving innovation, focusing on improving accuracy, comfort, and data connectivity.

- Market participants are expected to prioritize digital transformation and remote connectivity features to maintain competitiveness.

- Continuous innovation in design and automation is projected to enhance clinical efficiency and patient satisfaction over the forecast period.

- Overall, the phoropters market demonstrates sustainable growth prospects supported by digital advancement, aging populations, and expanding global eye care infrastructure.

Regional Analysis

In 2023, North America led the Phoropters Market, holding a share of over 39.9% and reaching a market value of USD 46.7 million. The region’s dominance can be linked to its quick adoption of advanced ophthalmic technologies. The integration of automated and digital features in phoropters has enhanced diagnostic accuracy. This technological progress, combined with strong innovation from leading manufacturers, positioned North America as the most progressive and mature market in the global phoropter landscape.

The strong healthcare infrastructure across North America supports consistent market growth. Advanced healthcare facilities and high awareness levels among patients and practitioners have driven demand for modern vision care equipment. Regular eye examinations are promoted widely, strengthening the need for efficient diagnostic tools. The availability of skilled ophthalmologists and optometrists further supports the expansion of the phoropter market. Together, these factors contribute to sustained growth and ensure continued investment in ophthalmic device advancements in the region.

Rising cases of vision-related disorders, such as myopia and astigmatism, have significantly influenced the regional market. The aging population also contributes to increasing demand for accurate eye testing solutions. Early diagnosis of eye disorders is gaining importance, which boosts the adoption of digital and automated phoropters. This ongoing rise in eye health concerns underscores the growing need for precise, reliable equipment. As a result, North America remains a vital market for manufacturers focusing on technological innovation and patient-centered diagnostic systems.

Additionally, strategic collaborations and supportive regulations have fueled product development. Partnerships between healthcare providers, research institutions, and device manufacturers have encouraged innovation. Strict regulatory standards in the United States and Canada ensure product quality and safety, strengthening consumer trust. Economic stability and high disposable incomes allow greater spending on advanced medical devices. These favorable conditions collectively reinforce North America’s leadership in the global phoropter market and are expected to sustain its dominance in the forecast period.

Segmentation Analysis

In 2023, digital phoropters dominated the market with a commanding share of over 53.6%. The growing preference for digital technology among practitioners and patients has driven this shift. These devices offer enhanced precision and speed, improving the accuracy of eye examinations. Their integration with digital systems has streamlined workflows in clinics, enhancing patient satisfaction. The efficiency and reliability of digital phoropters have made them essential tools for modern optometrists and ophthalmologists, solidifying their leading position in the global phoropters market.

The rise of digital phoropters has marked a clear technological advancement in the eyecare industry. Their automated functions and digital interfaces simplify vision testing, reducing manual errors. Eye specialists prefer these devices for their consistency and data accuracy. They also enable faster results and better record management. This adoption trend highlights the industry’s transition toward digitalization, reflecting the increasing importance of advanced diagnostic tools in enhancing clinical precision and patient outcomes across various ophthalmic settings.

Manual phoropters, once the standard in vision testing, have experienced a gradual decline in market share. Their reliance on manual adjustments limits efficiency and precision compared to digital models. While still valued for basic eye examinations, they are increasingly viewed as outdated in advanced clinical environments. The lack of integration features and automation has further reduced their adoption. As a result, many eye care professionals are upgrading to digital systems to improve diagnostic quality and workflow management, signaling a continued shift toward modernization.

In terms of end-users, specialty clinics led the market in 2023 with a share exceeding 42.5%. Hospitals also accounted for a substantial portion, driven by their commitment to comprehensive diagnostics and patient care. Smaller healthcare facilities, including outpatient centers and independent practices, contributed notably to the overall adoption of phoropters. The expanding use of these devices across diverse medical environments reflects a growing focus on accurate vision assessment. This widespread adoption underlines the versatility and essential role of phoropters in contemporary eye care delivery.

Key Market Segments

Type

- Manual

- Digital

End-Use

- Specialty Clinics

- Hospitals

- Others

Key Players Analysis

Topcon stands as a leading player in the global phoropters market, recognized for its advanced optical technologies and precision engineering. The company’s products are designed with a focus on accuracy and user comfort, making them highly preferred among eye care professionals. Topcon’s continuous innovation and integration of digital interfaces have strengthened its competitive position. Its emphasis on quality and ergonomic design supports its strong global presence and enhances operational efficiency in clinical settings, contributing significantly to market growth and user satisfaction.

Nidek has established a strong reputation through consistent investment in research and development, driving the advancement of reliable and efficient phoropters. The company’s commitment to innovation ensures enhanced performance and usability across its product range. Nidek’s phoropters are widely adopted in ophthalmic practices due to their precision and durability. Its strategic focus on developing cost-effective yet technologically advanced products enables the company to maintain a strong foothold in both developed and emerging markets, thereby reinforcing its position as a major industry participant.

Reichert’s influence in the phoropters market is defined by its dedication to optical innovation and diagnostic excellence. The company’s products are engineered to deliver superior image clarity and measurement precision, enabling improved diagnostic outcomes. Reichert’s continuous focus on quality assurance and advanced design has solidified its reputation among healthcare providers. By integrating user-friendly interfaces and durable components, the company ensures optimal functionality and long-term reliability. Its strong distribution network further supports market penetration across multiple regions, contributing to steady revenue expansion.

Zeiss remains a prominent name in the optics industry, extending its expertise to phoropters known for their exceptional precision and visual performance. The company leverages decades of optical experience to develop instruments that enhance clinical accuracy and patient comfort. Zeiss’s commitment to technological refinement and high manufacturing standards has positioned it as a benchmark for quality. Alongside key players such as Rexxam, Essilor, Huvitz, and Marco, Zeiss contributes to a highly competitive market landscape, fostering innovation and encouraging continuous product advancement across the industry.

Market Key Players

- PTopcon

- Nidek

- Reichert

- Zeiss

- Rexxam

- Essilor

- Huvitz

- Marco

Challenges

1. Cost Pressures and Payment Friction

Refraction services often face payment challenges. In many U.S. insurance plans, CPT 92015 for refraction is excluded or not reimbursed separately. As a result, patients must pay out of pocket. This adds financial strain for both patients and clinics. Administrative tasks also increase, as practices must manage coding and modifiers for non-covered services. These extra steps slow down workflow. They can also discourage clinics from investing in digital phoropters and advanced refraction systems, despite their efficiency benefits.

2. Integration and Workflow Issues

Integrating digital phoropters with electronic medical records (EMR) remains uneven. While manufacturers promote seamless EMR transfer, clinics often face setup costs, IT challenges, and staff training needs. The process takes time and resources. Transitioning from manual to automated systems also requires workflow redesign. Staff must adapt to new procedures and learn how to manage automated refraction. During this period, productivity can temporarily decline. These integration hurdles slow digital adoption, even when long-term gains in accuracy and efficiency are clear.

3. Regulatory and Compliance Burdens

Regulatory changes add pressure to eye care providers. The U.S. Federal Trade Commission (FTC) updated the Eyeglass Rule in 2024, requiring prescribers to confirm that patients receive their eyeglass prescriptions. Clinics must now document each release accurately. This increases administrative work and requires changes in recordkeeping systems. Practices also need to train staff to meet compliance standards. While the rule aims to improve consumer transparency, it raises documentation workload and costs for providers, especially smaller practices with limited administrative capacity.

4. Product Quality and Reliability Risks

Device reliability remains a key concern. In 2025, a Class II recall was issued for the Phoroptor VRx due to issues with head stability and bracket detachment. Such events highlight potential risks in equipment safety. Clinics owning these devices may face service interruptions, inspections, and repair expenses. Downtime affects patient scheduling and operational efficiency. Although most recalls are resolved quickly, they underline the importance of quality assurance and regular maintenance to minimize disruption and maintain patient trust.

5. Workforce Constraints

The U.S. eye care workforce is under strain. Studies predict a 30% shortage of ophthalmologist full-time equivalents (FTEs) by 2035. This gap could limit the number of eye exams conducted annually. Even with rising patient demand, limited clinician availability restricts overall capacity. Practices may adopt digital tools to improve efficiency, but staffing shortages still affect throughput. The imbalance between demand and available professionals remains a critical challenge for sustaining timely eye care delivery nationwide.

6. Evidence and Standardization Gaps

Clinical evidence for digital phoropters continues to evolve. Some studies indicate faster testing times and improved accuracy compared to manual refraction. However, results vary across clinic types and patient populations. Standardized evaluation methods are still lacking. Broader validation in real-world settings is needed to confirm consistency. Without uniform standards, adoption decisions remain cautious. Continuous research, peer-reviewed data, and regulatory guidance will be essential to build confidence and support widespread use of digital refraction technologies.

Opportunities

1. Digital and High-Resolution Refraction

Modern phoropters now deliver greater precision and speed. Advanced models, such as the Essilor Vision-R 800 and Topcon CV-5000S, provide fine dioptric steps as small as 0.01 D. Faster lens switching allows smoother and more accurate refractions. These systems improve the overall patient experience by reducing discomfort and test duration. Studies show that digital refraction systems can shorten testing time compared to manual methods. As a result, clinics can increase the number of daily eye exams, boosting operational efficiency and patient throughput.

2. Remote and Hybrid Refraction

The rise of tele-optometry has created new opportunities in remote and hybrid refraction. Web-based systems enable eye exams to be performed or supervised remotely, improving access for patients in underserved areas. Such systems are especially effective for follow-ups and low-complexity cases. Clinics can operate in a hub-and-spoke model, using remote control interfaces similar to in-office systems. This approach allows flexible scheduling, after-hours service, and better resource utilization. Remote refraction solutions are gaining attention as they combine convenience, scalability, and professional oversight within a secure digital environment.

3. Demographic and Epidemiologic Tailwinds

Global demand for refraction services continues to grow. The World Health Organization (WHO) reports that over 800 million people still lack access to basic eyeglasses. This unmet need ensures strong and consistent demand for refraction technologies. At the same time, the rising prevalence of childhood myopia has increased the need for regular eye exams and continuous monitoring. These demographic trends are driving adoption of advanced refraction systems that improve workflow efficiency and diagnostic accuracy. The combination of unmet needs and growing awareness creates a long-term growth opportunity for the phoropter market.

4. Compliance-Linked Differentiation

Digital phoropters offer clear advantages in regulatory compliance and data management. Systems that automate prescription generation and maintain audit trails reduce manual work for clinics. Seamless integration with Electronic Medical Records (EMR) simplifies compliance with Federal Trade Commission (FTC) requirements. Automated documentation also minimizes human error and supports better patient data security. These capabilities are increasingly seen as differentiators, especially for large practices and retail chains. As compliance becomes more demanding, solutions that combine efficiency with transparency will gain competitive strength in the market.

5. Ergonomics and Staff Well-Being

Digital phoropters improve workplace ergonomics by reducing repetitive hand and wrist movements. Traditional manual systems often cause strain from constant adjustments and wheel rotations. Automated controls minimize these actions, reducing physical fatigue among eye care professionals. This enhancement supports staff health, satisfaction, and long-term retention. Moreover, less physical effort allows practitioners to focus more on patient interaction and clinical accuracy. The result is a more comfortable and productive working environment. Ergonomic advantages, combined with workflow efficiency, position digital phoropters as a modern standard for sustainable clinical operations.

Conclusion

The phoropters market is expected to show steady growth over the coming years, supported by increasing cases of vision disorders and expanding eye care infrastructure. The shift toward digital and automated systems is improving diagnostic accuracy and operational efficiency in clinics. Aging populations and rising awareness of preventive eye care continue to strengthen demand across regions. While cost and integration challenges persist, ongoing technological innovation and digital connectivity are enhancing clinical performance. Manufacturers are focusing on ergonomic design, remote functionality, and data integration to meet evolving healthcare needs. Overall, the phoropters market is positioned for sustainable expansion, driven by innovation and growing global eye health demand.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)