Table of Contents

Overview

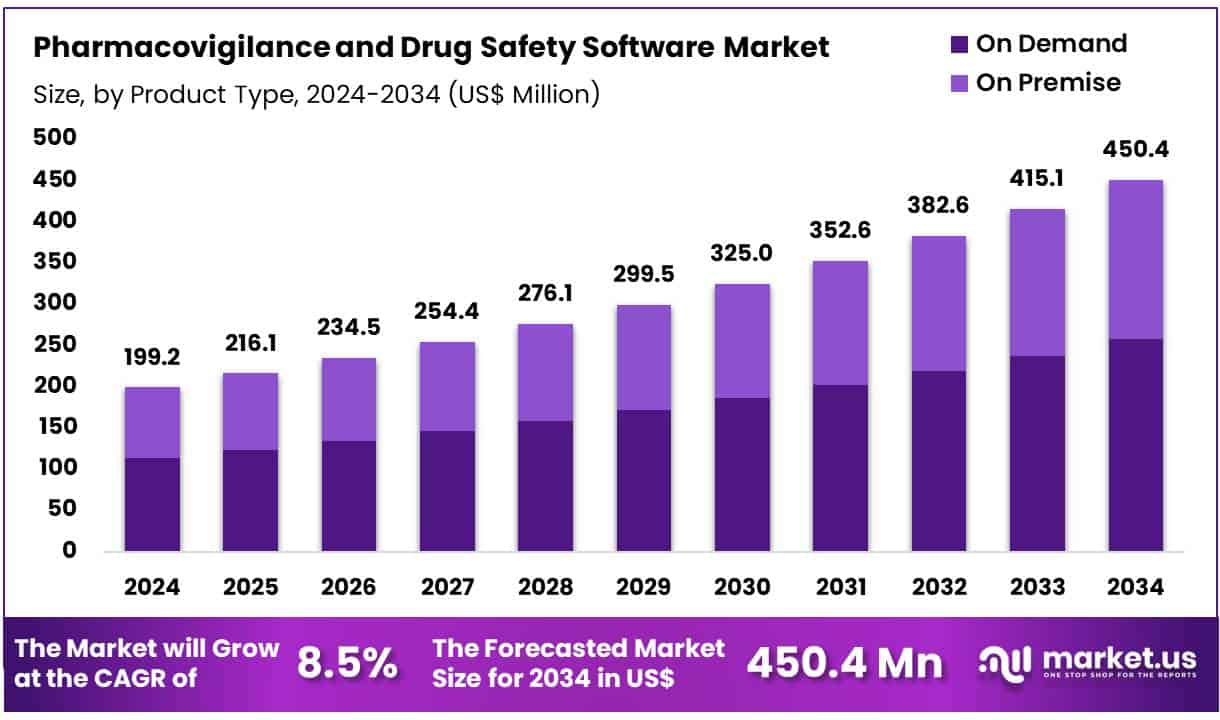

New York, NY – June 20, 2025 – Global Pharmacovigilance and Drug Safety Software Market size is expected to be worth around US$ 450.4 Million by 2034 from US$ 199.2 Million in 2024, growing at a CAGR of 8.5% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 36.5% share with a revenue of US$ 72.7 Million.

In 2024, the global pharmacovigilance and drug safety software market is witnessing robust expansion, driven by increased regulatory scrutiny, growing drug development activities, and the rising incidence of adverse drug reactions (ADRs). Pharmacovigilance software enables pharmaceutical companies, contract research organizations (CROs), and regulatory bodies to detect, assess, and prevent drug-related risks efficiently.

The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) have implemented stringent post-market surveillance frameworks, prompting the adoption of automated safety monitoring solutions. These platforms support real-time reporting, case management, signal detection, and compliance tracking, significantly improving patient safety and regulatory transparency.

Cloud-based deployment models and artificial intelligence (AI)-driven analytics are emerging as key trends, offering scalability, improved data integrity, and predictive risk assessment capabilities. Integration with electronic health records (EHRs) and clinical trial management systems (CTMS) is further enhancing pharmacovigilance workflows.

North America currently dominates the market due to its advanced healthcare IT infrastructure and strong pharmacovigilance regulations. Meanwhile, Asia-Pacific is expected to record the highest compound annual growth rate (CAGR), supported by expanding pharmaceutical manufacturing and harmonized drug safety guidelines. As the global demand for safer therapeutics rises, the pharmacovigilance and drug safety software market is expected to continue its upward trajectory, playing a critical role in ensuring public health and regulatory compliance.

Key Takeaways

- In 2024, the global pharmacovigilance and drug safety software market was valued at approximately US$ 199.2 million. The market is projected to grow at a compound annual growth rate (CAGR) of 8.5%, reaching an estimated US$ 450.4 million by 2034.

- By product type, the market is segmented into on-premise and on-demand solutions. Among these, the on-demand segment emerged as the leading category in 2023, accounting for a 57.3% share of total market revenue, attributed to its scalability, cost-efficiency, and ease of deployment.

- In terms of application, the market is classified into case data collection and management, adverse event reporting and analysis, and signal detection and other safety risk assessment. Of these, the signal detection and safety risk assessment segment held the largest share, contributing 39.6% of the total market in 2023, driven by increasing regulatory emphasis on proactive risk identification.

- Regarding end users, the market includes pharmaceutical and biotechnology companies, CROs/BPOs and pharmacovigilance service providers, and others. The pharmaceutical and biotechnology companies segment dominated in 2023, representing 55.4% of global revenue, reflecting the growing need for integrated safety monitoring systems in drug development pipelines.

- North America remained the leading regional market, capturing a 36.5% share in 2023, supported by robust regulatory frameworks and advanced healthcare IT infrastructure.

Segmentation Analysis

- Product Type Analysis: The on-demand segment, holding a 57.3% market share, is gaining traction due to the growing adoption of cloud-based pharmacovigilance solutions. These platforms offer greater flexibility, scalability, and cost-efficiency, enabling companies to reduce upfront IT investments. Real-time access to safety data and seamless integration with existing systems support timely regulatory compliance. As global drug safety standards evolve, on-demand software is expected to witness strong growth, particularly among organizations seeking agility and enhanced operational efficiency.

- Application Analysis: The signal detection and other safety risk assessment segment accounted for 39.6% of the market, reflecting increasing demand for early risk identification tools. Pharmaceutical companies are adopting advanced analytics and AI-driven algorithms to monitor adverse event trends more efficiently. This helps reduce the likelihood of drug recalls and enhances regulatory compliance. The growth in post-marketing surveillance data further reinforces the need for proactive risk mitigation, positioning this application segment for continued expansion in the drug safety software landscape.

- End-user Analysis: Pharmaceutical and biotechnology companies dominated the market with a 55.4% revenue share, driven by heightened regulatory demands for continuous drug safety oversight. These firms are investing in comprehensive pharmacovigilance platforms to improve adverse event reporting, streamline safety processes, and maintain compliance across product lifecycles. Additionally, outsourcing to CROs and PV service providers is expanding service capabilities. With a focus on accuracy, cost-efficiency, and data transparency, this end-user segment is expected to maintain robust growth momentum.

Market Segments

Product Type

- On Premise

- On Demand

Application

- Case Data Collection & Management

- Adverse Event Reporting & Analysis

- Signal Detection & Other Safety Risk Assessment

End-user

- Healthcare Companies (Pharmaceuticals & Biotechnology Companies)

- CROs/BPOs or PV service providers when outsourced.

- Others

Regional Analysis

North America Leads the Pharmacovigilance and Drug Safety Software Market

North America accounted for the largest share of the global market, securing 36.5% of total revenue in 2023. This dominance is attributed to the stringent regulatory framework established by the U.S. Food and Drug Administration (FDA) and the high volume of adverse event reports. The FDA’s Adverse Event Reporting System (FAERS) processes a significant number of case submissions annually, necessitating advanced software solutions to manage, monitor, and analyze safety data efficiently.

Pharmaceutical companies in the region are required to comply with rigorous pharmacovigilance standards, including post-marketing surveillance and timely adverse event reporting as outlined under 21 CFR Part 314. These regulatory obligations have led to widespread adoption of software platforms capable of supporting real-time signal detection, risk assessment, and regulatory compliance. Furthermore, the rising complexity of clinical trials and the growing emphasis on patient safety continue to drive software demand across North American markets.

Asia Pacific to Witness the Highest Growth Rate During Forecast Period

The Asia Pacific region is projected to register the highest compound annual growth rate (CAGR) during the forecast period. This growth is primarily driven by the expanding pharmaceutical manufacturing base, especially in countries like India, China, and South Korea, and increasing alignment with global pharmacovigilance standards. As more regional pharmaceutical companies pursue global market entry, compliance with international safety protocols becomes essential, prompting adoption of dedicated pharmacovigilance software.

Additionally, the rising incidence of adverse drug reactions (ADRs) across the region is creating a greater need for robust systems to manage and assess safety data effectively. Investments in healthcare IT infrastructure are also accelerating, enabling broader deployment of cloud-based drug safety solutions. The growing focus on regulatory harmonization, patient safety, and international compliance is expected to significantly bolster software adoption in Asia Pacific over the coming years.

Emerging Trends

- Adoption of Artificial Intelligence and Machine Learning: Pharmacovigilance systems are increasingly being enhanced with AI and ML algorithms to automate signal detection and case processing. Over the last decade, more than 20 million individual case safety reports (ICSRs) have been submitted to FAERS, creating a need for automated narrative summarization and trend analysis to reduce manual workload and improve timeliness of safety insights.

- Standardized Electronic Submissions (ICH E2B(R3)): The industry has been moving toward fully electronic transmission of ICSRs using the ICH E2B(R3) format. Public workshops held in April and November 2023 outlined technical specifications for upgrading e-submissions, enabling sponsors to submit pre- and post-market safety reports more efficiently and in a harmonized structure.

- Interactive Public Dashboards for Real-Time Access: Transparency initiatives have led to the creation of user-friendly, web-based dashboards. The FDA’s FAERS Public Dashboard offers interactive querying of adverse event data on a quarterly basis, allowing regulators, healthcare professionals, and the public to monitor safety signals in near real time.

- Integration of Diverse Data Sources and Advanced Analytics: Best practices guidelines emphasize the use of multiple data streams—such as electronic health records, claims data, and Sentinel System analyses alongside FAERS data. Advanced analytics techniques are being employed to correlate these sources, enhancing signal validation and enabling a more comprehensive view of drug safety.

Use Cases

- Routine Signal Detection and Quarterly Safety Reports: FDA staff conduct bi-weekly screening of FAERS data and publish quarterly lists of potential signals of serious risks or new safety information. These reports inform subsequent evaluations and regulatory actions, such as safety communications or label changes.

- Electronic Case Safety Report (ICSR) Submission by Sponsors: Pharmaceutical companies leverage the ICH E2B(R3) electronic submission standards to transmit adverse event data directly into FAERS. This process has been refined through public meetings, improving data consistency and reducing submission errors.

- Risk Evaluation and Mitigation Strategy (REMS) Planning: Data from FAERS and other surveillance systems are used to trigger modifications to REMS programs. When potential risks are identified such as new serious adverse events FDA may require sponsors to develop or update REMS, impose post-marketing studies, or alter product labeling to mitigate patient risk.

Conclusion

The global pharmacovigilance and drug safety software market is undergoing significant transformation, driven by stringent regulatory mandates, increased drug development, and the rising burden of adverse drug reactions. The integration of AI, standardized electronic submissions, and real-time dashboards is enhancing drug safety monitoring across the lifecycle.

North America remains the leading region, while Asia-Pacific is poised for the highest growth due to evolving compliance frameworks and expanding pharma manufacturing. As the global emphasis on patient safety intensifies, pharmacovigilance software will remain a critical tool for ensuring regulatory compliance and proactive risk mitigation in the pharmaceutical landscape.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)