Table of Contents

Overview

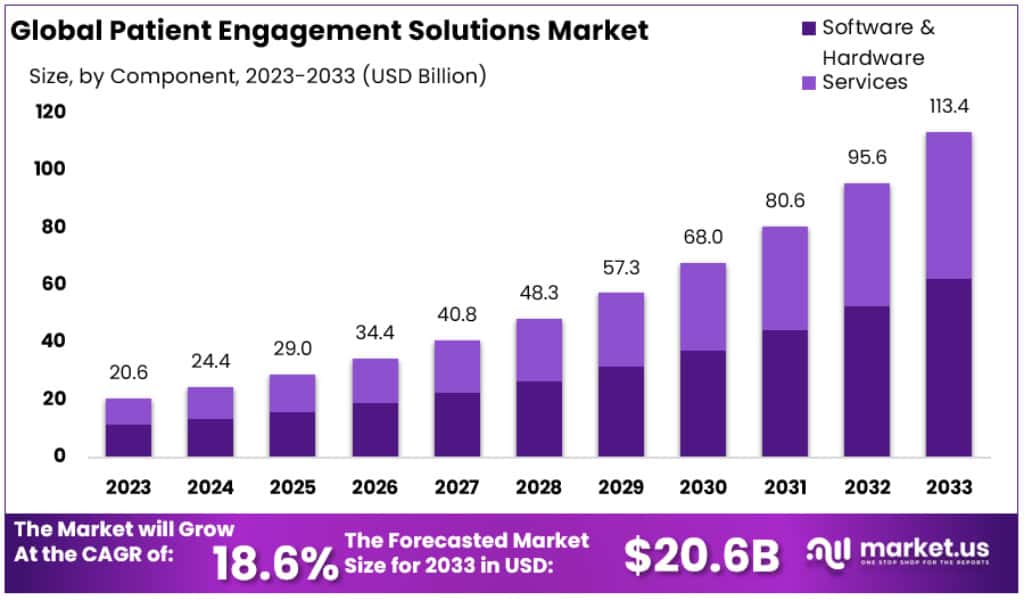

The Global Patient Engagement Solutions Market is projected to reach USD 113.4 billion by 2033, increasing from USD 20.6 billion in 2023. This represents a compound annual growth rate of 18.6% between 2023 and 2033. The expansion is being fueled by the rising need for digital interactions in healthcare, which has become crucial for system performance. Patient engagement platforms now serve as an essential bridge between providers and patients, ensuring continuity of care beyond traditional hospital settings.

The burden of noncommunicable diseases (NCDs) acts as a strong catalyst for market growth. Approximately three-quarters of global deaths are caused by NCDs, including diabetes, cardiovascular diseases, and cancer. These conditions require continuous monitoring, long-term self-management, and frequent follow-up care. To address this demand, providers are increasingly deploying portals, telehealth tools, and remote monitoring platforms that improve treatment adherence and reduce avoidable hospital admissions.

Another structural factor is the rise in the aging population. Global data show a consistent increase in people aged 65 years and above, who typically require more frequent care. Managing multiple conditions demands simplified access to information and care coordination. Patient engagement solutions make it easier for older adults to track health records, appointments, and medication schedules, creating a reliable driver for adoption.

At the same time, global internet connectivity has enabled wider reach. According to the International Telecommunication Union (ITU), about 5.5 billion people, or 68% of the world population, were online in 2024. With greater access, patients can use secure portals, request prescription refills, and attend virtual consultations. The expansion of internet availability has lowered barriers to digital engagement and reduced costs for providers, making scalable adoption possible worldwide.

Policy, Technology, and Behavioral Shifts

Government regulations are accelerating the adoption of patient engagement platforms. In the United States, the ONC’s Cures Act Final Rule ensures patients can electronically access their health information, preventing information blocking. In the European Union, the European Health Data Space regulation strengthens rights to digital health access across member states. Such policies make engagement tools not optional, but mandatory, thereby raising adoption levels across regions.

Advances in healthcare digitization also provide a strong foundation for engagement growth. Data from the OECD show widespread adoption of electronic medical records (EMRs), especially in primary and inpatient care. As EMR systems become standardized, they create a strong data backbone for patient portals, enabling real-time access to test results, care plans, and booking systems. This availability improves patient trust and engagement with digital services.

Shifting patient behavior further reinforces the trend. In the U.S., federal analyses highlight increasing use of smartphone applications for accessing records. Mobile-first preferences have risen since 2020, reflecting a permanent change in how patients engage with providers. The normalization of telehealth during the pandemic also created new habits, with many patients now comfortable with virtual consultations and related digital services such as e-triage and remote monitoring.

Operational challenges are another driver. The World Health Organization (WHO) projects a shortage of 11 million health workers by 2030. This pressure is pushing health systems to automate administrative functions, reduce no-shows, and support preventive care through engagement solutions. National platforms such as the NHS App in England illustrate how large-scale engagement can lower costs and increase efficiency. Combined with steady growth in global health expenditure, patient engagement platforms are now recognized as critical for sustainability and improved outcomes.

Key Takeaways

- The Patient Engagement Solutions Market is projected to achieve approximately USD 113.4 billion by 2033, reflecting substantial long-term growth potential in healthcare technologies.

- In 2023, the Patient Engagement Solutions Market was valued at USD 20.6 billion, marking the foundation for the forecasted expansion over the decade.

- The market is expected to register a strong Compound Annual Growth Rate (CAGR) of 18.6% during the forecast period from 2023 to 2033.

- Software and Hardware solutions collectively accounted for more than 55% market share in 2023, demonstrating their leading role in driving adoption across healthcare organizations.

- Cloud deployment dominated the Patient Engagement Solutions Market with over 59% market share in 2023, underscoring the sector’s shift toward scalable, cost-efficient platforms.

- Health Management applications secured more than 36% of market share in 2023, highlighting growing demand for tools supporting preventive care and patient-centered healthcare.

- Communication functionality emerged as a significant segment, capturing more than 37% share in 2023, emphasizing the importance of digital interaction between patients and providers.

- Chronic Disease Management remained the leading application, holding over 41% share in 2023, driven by rising global prevalence of long-term health conditions.

- North America dominated the global market with a 36% share, valued at USD 7.4 billion in 2023, supported by advanced healthcare infrastructure.

Regional Analysis

North America leads the patient engagement solutions market with a 36% share, valued at USD 7.4 billion in 2023. The dominance of this region is supported by government initiatives and healthcare spending. In the United States, healthcare costs reached USD 3.9 trillion in 2020, accounting for 18.8% of GDP. Policies such as the CARES Act increased Medicare coverage and boosted digital health adoption. These factors created strong demand for patient engagement tools, strengthening the region’s position in the global market.

Europe holds the second-largest market share, driven by its strong healthcare systems and public funding. Initiatives such as the National Health Service (NHS) in the United Kingdom are advancing digital transformation in healthcare. Efforts to expand electronic health records (EHRs) and modernize hospital services have encouraged the adoption of patient engagement solutions. The focus on improving access to healthcare services across different countries has supported growth. Investments in advanced health technology further sustain Europe’s steady presence in the global market.

The Asia-Pacific region is expected to record the fastest growth, with a forecasted CAGR of 19% during the analysis period. Rising internet and smartphone penetration, coupled with large patient populations, has accelerated market expansion. Economic progress in countries such as India and China is improving healthcare delivery and infrastructure. This environment increases the adoption of mobile health and telemedicine solutions. Government support and private investments in digital health also add momentum. The region is set to play a critical role in shaping future market dynamics.

Segmentation Analysis

In 2023, the Software and Hardware segment held the leading position in the Patient Engagement Solutions Market with more than 55% share. This segment includes standalone and integrated systems. Standalone systems are widely used by smaller healthcare providers due to their cost-effectiveness and easy setup. Integrated solutions combine multiple functions into one cohesive system. Larger healthcare organizations prefer integrated models for comprehensive strategies. This makes Software and Hardware the cornerstone of the market, meeting diverse healthcare needs with both affordability and advanced integration options.

The Services segment represents another important part of the Patient Engagement Solutions Market. It is divided into consulting, implementation and training, and other supportive services. Consulting is vital for providers to tailor strategies and optimize engagement tools. Implementation and training ensure healthcare staff can use these systems effectively. The “others” category includes ongoing maintenance and support. Together, these services play a crucial role in enhancing patient outcomes and ensuring smooth adoption of engagement technologies across different healthcare facilities.

Deployment mode analysis highlights cloud solutions as the largest segment in 2023, holding over 59% share. Cloud deployment offers scalability, cost savings, and easy access to patient tools without large IT investments. Enhanced security measures further increase its adoption. On-premise solutions, however, remain important for providers preferring higher control and customization. These require significant investment and IT support but offer strong data management. The growing preference for cloud highlights the digital shift, while on-premise continues to serve specialized healthcare organizations with unique operational requirements.

Within applications, Health Management dominated the market in 2023, with more than 36% share. This segment focuses on chronic disease management and wellness programs. Adoption is driven by the need for continuous monitoring and personalized care. Social and Behavioral Management is also growing, targeting lifestyle choices and mental health. Other applications include patient education, appointment scheduling, and medication adherence. These segments reflect the market’s broad focus on enhancing patient health and supporting proactive, personalized healthcare delivery strategies across multiple areas of patient engagement.

By functionality, communication tools held a strong position with over 37% share in 2023. These tools include messaging systems and telehealth platforms that improve patient-provider interaction. Health Tracking & Insights follows closely, helping track vital signs and generate recommendations for preventive care. Billing and payments functionality streamlines claims and transactions, easing the financial experience for patients. Other functions such as prescription management and education add further value. Collectively, these functions enhance care delivery, simplify processes, and promote proactive healthcare engagement through digital and patient-centered solutions.

In terms of therapeutic areas, chronic disease management led the market in 2023, holding over 41% share. Rising prevalence of conditions such as diabetes and heart disease drives demand for continuous monitoring and adherence tools. Health and wellness solutions are also growing, focusing on nutrition, fitness, and preventive care. Other therapeutic areas include maternal care, pediatric support, and elder care. Providers are also key end-users, holding more than 46% share. Payers and patients are adopting solutions rapidly, while governments and corporates add further support, expanding patient engagement opportunities.

Key Players Analysis

The patient engagement solutions market is witnessing strong competition, driven by leading companies such as Allscripts Healthcare, LLC. This company plays a pivotal role in advancing electronic health records (EHR) and patient engagement solutions. Their offerings focus on strengthening communication between patients and healthcare providers, improving care coordination, and reducing overall healthcare costs. Orion Health also contributes significantly, offering global healthcare IT solutions designed to manage patient information efficiently, enhance provider collaboration, and support large-scale population health management initiatives.

Cerner Corporation is another dominant participant in this market, with expertise in healthcare IT solutions. The company provides systems for patient record management, clinical decision support, and financial management in healthcare organizations. McKesson Corporation also adds value with its robust healthcare technology services, while IBM stands out with its advanced digital health and data analytics platforms. Wolters Kluwer N.V. further strengthens the market by delivering clinical decision support tools, compliance solutions, and evidence-based medical content.

Other notable players in the market include Greenway Health, LLC, CureMD Healthcare, Nuance Communications, Inc., and Solutionreach, Inc. These companies focus on specialized areas such as practice management systems, voice recognition technologies, cloud-based EHR, and patient communication platforms. Collectively, these key participants are accelerating the adoption of patient engagement solutions, thereby improving healthcare outcomes. Their strategic innovations and continuous technological advancements are expected to drive market growth and intensify competition among global and regional providers.

Market Key Players

- Allscripts Healthcare, LLC

- Orion Health

- Cerner Corporation

- McKesson Corporation

- IBM

- Wolters Kluwer N.V.

- Greenway Health, LLC

- CureMD Healthcare

- Nuance Communications, Inc.

- Solutionreach, Inc.

- And Other Key Players

Challenges

1) Interoperability Gaps

Health data still do not move smoothly between systems. Standards are improving, but adoption is inconsistent across providers. The Trusted Exchange Framework and Common Agreement (TEFCA) is designed to link networks nationwide. However, full-scale exchange using FHIR standards is not yet achieved. This creates delays and limits seamless information flow. Patients often face incomplete records when moving between providers. Clinicians may lack access to critical information at the point of care. Without strong interoperability, engagement tools cannot deliver their full value. Progress is being made, but nationwide integration remains a key challenge.

2) Information Blocking Risks and Compliance Burden

The 21st Century Cures Act requires that patients gain quick access to their electronic health information. Delays or restrictions are considered information blocking. Organizations that fail to comply face heavy penalties. Fines can reach up to $1 million per violation. This creates a significant compliance burden for health systems. Providers must align workflows, policies, and technology to meet the rule. At the same time, they must balance privacy, security, and operational demands. Many organizations struggle with meeting requirements while avoiding risks. Compliance is essential, but the pressure adds complexity to patient engagement initiatives.

3) Cybersecurity Threats and Trust

Cybersecurity remains one of the largest risks in healthcare. Large-scale data breaches and ransomware attacks are increasing each year. In 2024, hundreds of major breaches were reported to the U.S. Department of Health and Human Services. Hacking incidents now account for most reported breaches. These disruptions undermine patient trust and delay care. Federal agencies have warned about persistent ransomware targeting health systems. As digital engagement expands, security gaps become more dangerous. Strong defenses are critical for protecting sensitive data. Without security and trust, patient engagement platforms risk losing adoption and credibility.

4) Digital Divide and Usability

Technology access remains uneven across populations. Internet and smartphone use are high but not universal. Older adults, rural residents, and low-income groups may face barriers. Skills also vary by age and education. This creates risk of exclusion if platforms are not designed inclusively. The CDC advises using user-centered design for older adults. Interfaces should be simple, intuitive, and accessible. Poor design can discourage adoption, even when access exists. Addressing the digital divide requires clear instructions, multilingual support, and inclusive features. Engagement solutions must work for everyone, not just the digitally skilled.

5) Portal and App Fragmentation

Patients now often have multiple portals from different providers, insurers, and pharmacies. This creates confusion and reduces consistent use. Switching between platforms is frustrating and time-consuming. Some patients forget login details or stop using portals altogether. As a result, engagement drops and information becomes scattered. The lack of integration reduces continuity of care. A single, unified view of health data is rarely available. Patients want convenience and simplicity, but fragmentation delivers the opposite. Without coordination, digital tools can add complexity instead of solving problems. Consolidation and interoperability are needed to improve engagement.

6) Workflow Burden for Clinicians

Digital engagement tools often add new demands to clinicians. Secure messages, patient alerts, and device-generated data can overwhelm workflows. Without proper prioritization, this leads to inefficiency and stress. Poor integration into clinical systems makes the problem worse. Burnout among healthcare providers is widely reported, especially alongside cyber disruptions. If tools are seen as extra work, adoption will be limited. To succeed, solutions must reduce, not increase, the burden on staff. Streamlined workflows, smart automation, and clear triage are essential. Otherwise, engagement tools risk harming the very care they aim to support.

7) Reimbursement Complexity

Reimbursement rules for digital health services remain complex. Remote patient monitoring (RPM) and telehealth have specific billing requirements. For example, RPM requires a minimum number of days of data collection. Only one billing practitioner may claim services in a 30-day period. Programs can fail if rules are not followed precisely. Incorrect coding or missing documentation leads to denied claims. Providers face administrative challenges in managing these details. This complexity discourages wider adoption of engagement tools. Simplifying reimbursement and offering clear guidance would support growth. Without it, financial barriers remain a critical challenge.

Opportunities

1. Rising access and use of digital records

Most adults in the United States now have online access to their health records. Uptake is improving each year, as more patients log in to view test results, care summaries, or visit notes. This expansion is creating a larger addressable base for Patient Engagement Solutions (PES). With more individuals already familiar with digital records, vendors can integrate additional services such as reminders, personalized education, or scheduling tools. The growth of this digital foundation means less friction in adoption. It allows PES providers to build on existing habits rather than starting from scratch.

2. National interoperability tailwinds

Healthcare interoperability is gaining momentum. National frameworks like the Trusted Exchange Framework and Common Agreement (TEFCA) are expanding. At the same time, FHIR (Fast Healthcare Interoperability Resources) standards are being required for exchange networks. Vendors that align early with these initiatives can gain speed. They reduce the need for complex, costly custom interfaces and shorten deployment times. Early adopters also signal compliance and readiness to providers. This builds trust with hospitals and health systems seeking reliable partners. Interoperability is no longer optional—it is becoming a competitive necessity. PES vendors who embrace it can position themselves as leaders.

3. Reimbursed home monitoring and telehealth

The Centers for Medicare & Medicaid Services (CMS) continues to support telehealth and remote patient monitoring (RPM). Defined fees and coding guidance are already in place for 2024 and 2025. This gives providers a financial incentive to adopt these tools. Patient Engagement Solutions that connect to telehealth and home monitoring services can generate measurable return on investment (ROI). For example, structured RPM data can improve chronic condition management and reduce hospital visits. By tying engagement platforms to reimbursed services, vendors help providers meet clinical goals while benefiting financially. This creates a strong growth driver for PES adoption.

4. Security-by-design as a differentiator

Cybersecurity breaches are becoming more frequent in healthcare. As a result, providers and patients are placing higher value on strong data protection. Solutions that go beyond baseline HIPAA compliance stand out in the market. PES vendors that embed security-by-design, rapid recovery capabilities, and tested incident response playbooks can build trust. Buyers will view them as safer partners, especially compared with vendors offering only basic protections. Following federal best practices and exceeding minimum standards signals long-term reliability. In a market where trust is fragile, security can be more than compliance—it can become a core differentiator.

5. Inclusive, plain-language design

Patient engagement is not effective if users cannot understand or access the tools. Inclusive design is therefore essential. PES platforms that use simple language, multiple language options, and culturally relevant content can reach more people. Low-literacy content helps those who struggle with complex medical terms. Assisted onboarding features, such as guided tutorials, can further support older adults or underserved populations. These improvements increase adoption rates and engagement metrics. When patients feel included and supported, they are more likely to actively participate in managing their health. This approach turns accessibility into a measurable advantage for vendors.

6. Consolidated patient front doors

Many patients still face the challenge of multiple logins and fragmented portals. Consolidated patient front doors solve this by creating one access point. Using FHIR APIs, vendors can aggregate information from multiple providers and systems. This gives patients a single hub to manage all aspects of their care. Aligning with TEFCA also ensures compliance with federal interoperability rules. For providers, these unified platforms reduce confusion and support continuity of care. For patients, they simplify the process of accessing records, scheduling, and communication. Vendors offering such architectures can deliver both convenience and compliance in one solution.

7. Proactive engagement from patient-generated data

The rise of wearables, mobile apps, and home health devices is generating valuable patient data. PES platforms can ingest this information in structured formats. Rule-based triage systems can flag out-of-range readings, allowing providers to intervene early. This reduces avoidable emergency visits and supports better outcomes. Importantly, when billing rules are followed, these services can also generate revenue under value-based contracts. Proactive engagement helps providers achieve performance goals while improving patient safety. Vendors that offer seamless integration of patient-generated data into clinical workflows can position themselves as strategic partners in value-driven healthcare delivery.

8. Transparency and open notes

Federal rules now mandate faster release of test results and clinical notes to patients. This shift creates both challenges and opportunities. Tools that simply comply with regulations meet the minimum standard. However, PES vendors can go further. By guiding patients on how to interpret results and what steps to take next, they transform compliance into engagement. Educating patients builds confidence and improves satisfaction. Transparent communication also strengthens trust between patients and providers. Vendors that design user-friendly open notes features will help organizations achieve better outcomes while meeting regulatory requirements. Transparency becomes a driver of loyalty.

Conclusion

The Patient Engagement Solutions market is set for strong and lasting growth as healthcare continues its digital shift. Increasing cases of chronic illness, an aging global population, and wider internet access are making these solutions essential for care beyond hospitals. Government rules and rising use of electronic medical records have built a solid base for adoption, while new habits such as telehealth and mobile apps are reshaping patient behavior. At the same time, providers face workforce shortages and rising costs, which drive demand for scalable engagement tools. With technology advances and supportive policies, patient engagement platforms are becoming central to improving outcomes and building sustainable healthcare systems.

View More

Patient Portal Market || AI In Remote Patient Monitoring Market || Digital Patient Monitoring Devices Market || Patient Registry Software Market || Patient Positioning Systems Market || Interactive Patient Care Systems Market || Outpatient Care Market || Remote Patient Monitoring Software and Services Market || Patient Data Hub Solutions Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)