Table of Contents

Overview

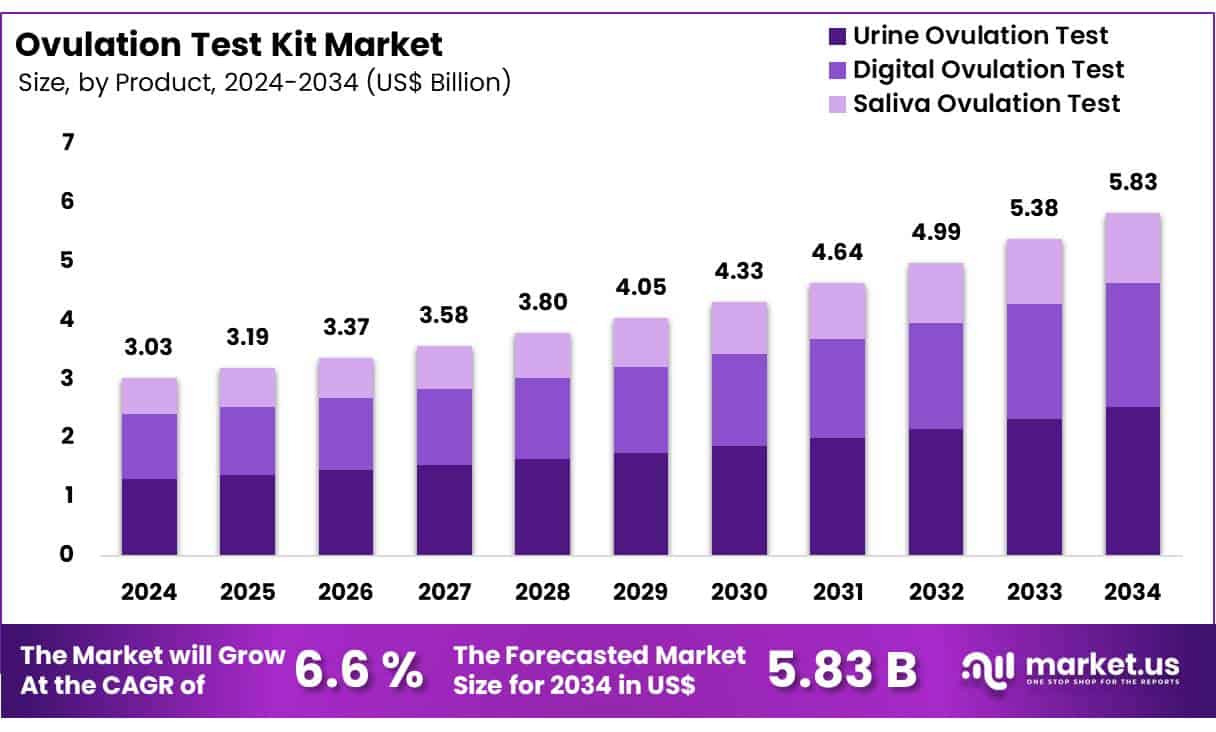

New York, NY – May 22, 2025 – Global Ovulation Testing Kits Market size is expected to be worth around US$ 5.83 Billion by 2034 from US$ 3.04 Billion in 2024, growing at a CAGR of 6.6% during the forecast period from 2024 to 2034.

The global ovulation testing kits market is experiencing consistent growth, attributed to increasing awareness about fertility tracking and the rising preference for home-based diagnostic solutions. Ovulation kits are widely used by women to identify their most fertile days by detecting luteinizing hormone (LH) surges in urine, which precede ovulation.

This surge in demand is primarily driven by delayed pregnancies, rising infertility rates, and growing awareness of reproductive health. The COVID-19 pandemic further accelerated the shift toward at-home health monitoring tools, increasing reliance on non-invasive, easy-to-use testing kits. In addition, the convenience, affordability, and privacy offered by these kits are enhancing their adoption across diverse demographics.

Digital ovulation kits, which offer higher accuracy and ease of interpretation, are gaining popularity over traditional test strips. The integration of smartphone apps with digital testing solutions is also enabling better fertility tracking and health data management.

Pharmacies, online platforms, and retail stores remain key distribution channels, supported by strong marketing campaigns and improved accessibility. North America holds the largest share of the market, while Asia-Pacific is projected to witness the fastest growth due to improving healthcare infrastructure and increasing reproductive health awareness.

Key Takeaways

- In 2024, the Ovulation Test Kit market generated a revenue of US$ 3.04 billion and is projected to reach US$ 5.41 billion by 2033, expanding at a compound annual growth rate (CAGR) of 6.6%.

- By product type, the urine ovulation test segment emerged as the leading contributor, accounting for 43.4% of the total market revenue in 2024, due to its ease of use and widespread availability.

- By end user, the individual/personal use segment dominated the market with a revenue share of 53.8%, driven by increasing consumer awareness and the growing preference for at-home fertility monitoring solutions.

- By distribution channel, the e-commerce segment held the largest share at 41.8%, supported by the convenience of online purchasing, wide product availability, and growing digital health trends.

- Regionally, North America led the global market, securing a dominant share of 37.7%, attributed to advanced healthcare infrastructure, high awareness of reproductive health, and strong demand for self-care diagnostics.

Segmentation Analysis

- By Product Analysis: The ovulation test kit market is segmented into urine, digital, and saliva-based tests. In 2024, the urine ovulation test segment held the largest market share at 43.4%, owing to its reliability in detecting key fertility hormones. Meanwhile, the digital ovulation test segment is anticipated to grow at the fastest CAGR due to innovations such as app connectivity and memory functions. These features enhance cycle tracking accuracy, attracting tech-savvy users and encouraging new market entrants.

- By End-User Analysis: The individual/personal use segment dominated the ovulation test kit market in 2024, driven by increasing consumer preference for private, affordable at-home fertility monitoring. The segment’s growth reflects the rising awareness of reproductive health and improved access through online platforms. Conversely, fertility centers and clinics are expected to witness the fastest growth, propelled by rising infertility cases and increased use of ovulation kits as part of comprehensive fertility assessments and assisted reproductive treatments.

- By Distribution Channel Analysis: In 2024, pharmacies and drugstores held the largest share of the ovulation test kit market at 34.6%, supported by their widespread presence and trusted access points in emerging economies. However, the e-commerce segment is projected to grow at the highest CAGR, as consumers increasingly favor the convenience, discretion, and product variety offered by online platforms. This shift, amplified by post-pandemic digital trends, is expected to reshape distribution strategies and boost global market penetration.

Market Segments

By Product

- Urine Ovulation Test

- Test Strip Type

- Cassette Type

- Midstream Type

- Digital Ovulation Test

- Saliva Ovulation Test

By End User

- Individual/Personal use

- Hospitals/Clinics

- Fertility Centers/ Clinics

- Research Institutes/Medical Colleges

- Others

By Distribution Channel

- Hypermarkets and Supermarkets

- E-Commerce

- Pharmacies and Drugstores

Regional Analysis

In 2024, North America remained the dominant region in the global ovulation test kit market, capturing approximately 37.7% of the total revenue share. This leadership is largely attributed to the rising adoption of technologically advanced kits, featuring capabilities such as Bluetooth connectivity and smart countdown timers, which cater to consumers seeking convenience and real-time fertility tracking.

A significant contributor to this trend is the large working population in the United States, where busy schedules limit the feasibility of frequent clinical visits. As a result, demand for accurate, home-based ovulation solutions has increased notably.

Manufacturers in the region are focusing on launching cost-effective, user-friendly products with enhanced accuracy. In addition, strategic partnerships and collaborations are being pursued to expand regional product portfolios and market reach.

For instance, in 2022, Sugentech, a key player in digital ovulation testing, entered into a strategic partnership with CGETC, Inc., a U.S.-based firm specializing in fulfillment and marketing, to strengthen its U.S. operations. Leading brands such as Clearblue, First Response, and E.P.T. continue to shape the market landscape with product innovation and strong consumer trust.

Emerging Trends

- The integration of digital connectivity is being observed in ovulation testing kits, with many devices now designed to sync with smartphone apps for cycle tracking and personalized insights.

- Point-of-care testing technologies are being developed to deliver faster results and higher sensitivity in home settings, as outlined in recent reviews of ovulation detection methods.

- Wearable biosensor approaches are being investigated for continuous fertility monitoring. In one study, cardiovascular fluctuations were analyzed across 45,811 menstrual cycles from 11,590 participants to infer ovulation timing.

- An overall increase in the use of fertility awareness-based methods has been documented: about 18.5% of sexually experienced women in the U.S. reported ever using symptothermal or mucus-based cycle-tracking methods, which include urine-based ovulation kits.

Use Cases

- Timing conception: Ovulation kits are being used to identify the fertile window, supporting conception efforts. Approximately 18.5% of women have relied on such cycle-tracking methods at least once.

- PCOS management: Women with polycystic ovary syndrome (PCOS) which affects an estimated 6.6% of U.S. women of reproductive age use ovulation kits to monitor irregular cycles and optimize timing for medical interventions.

- Infertility evaluation: Given that 1 in 5 married women aged 15–49 experience infertility after one year of trying, ovulation testing kits are applied in preliminary at-home assessments before clinical consultation.

- Research studies: Ovulation kits continue to provide ground-truth data in clinical and academic research. For example, they were used alongside wearable sensors in a study encompassing 11,590 participants and 45,811 recorded cycles to improve algorithms for non-invasive ovulation detection.

Conclusion

The global ovulation testing kits market is poised for steady expansion, driven by rising fertility awareness, increasing preference for home-based diagnostics, and advancements in digital health technologies. The dominance of urine-based kits and the growing popularity of digital solutions reflect consumer demand for accuracy and convenience.

North America leads the market due to strong healthcare infrastructure and early technology adoption, while Asia-Pacific is expected to grow rapidly. Use cases span from fertility planning to clinical research, highlighting the kits’ relevance across healthcare and personal health monitoring. Continued innovation and digital integration are expected to further accelerate market adoption globally.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)