Overview

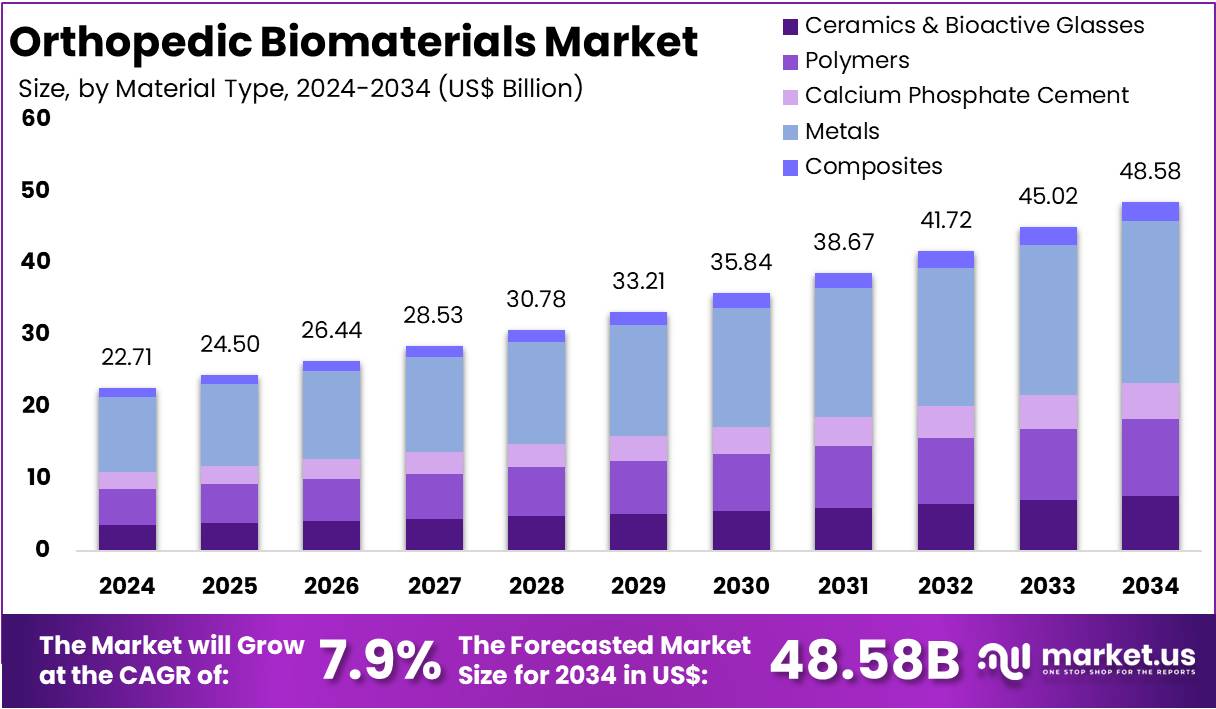

New York, NY – August 19, 2025: The Global Orthopedic Biomaterials Market is projected to reach US$ 48.58 billion by 2034, rising from US$ 22.71 billion in 2024, at a CAGR of 7.9% between 2025 and 2034. North America leads the market with a 37.1% share and a value of US$ 8.43 billion in 2024. Growth is supported by the rising burden of musculoskeletal diseases. The World Health Organization (WHO) reports that 1.71 billion people live with such conditions, making them the leading cause of disability worldwide. Osteoarthritis alone affected 528 million people in 2019, mostly involving knees and hips, creating steady demand for implants, graft substitutes, and cements.

Ageing demographics strongly reinforce market growth. Data from the United Nations and World Bank show that the share of people aged 65+ continues to rise globally. With older populations, conditions like osteoarthritis, osteoporosis, and fragility fractures increase, directly boosting the need for orthopedic materials and implants. WHO estimates show 178 million new fractures occurred in 2019, marking a 33% rise in annual fracture numbers since 1990 due to ageing and population growth. Acute fracture care and long-term recovery both require fixation devices, bone substitutes, and bioresorbable materials.

Osteoporosis further drives the demand. In the United States, surveillance data shows that 12.6% of adults aged 50+ had osteoporosis by 2017–2018, with higher prevalence in women. These patients face increased fracture risks, often needing augmentation cements and bone-strengthening materials. Obesity also contributes to demand. WHO data shows adult obesity rose from 7% in 1990 to 16% in 2022, while adolescent obesity grew from 2% to 8%. Excess body weight accelerates knee osteoarthritis and often leads to earlier joint replacement, raising use of wear-resistant and osteoconductive biomaterials.

Trauma care remains another critical factor. WHO’s road safety report highlights 1.19 million annual deaths from traffic crashes, mainly in low- and middle-income countries. Non-fatal injuries create high demand for fracture fixation devices, plates, screws, and scaffolds made from advanced biomaterials. Surgical procedure volumes also confirm strong market use. According to the OECD, average rates reach 172 hip replacements and 119 knee replacements per 100,000 population, with post-pandemic recovery supporting consistent demand. In England, NHS patient outcomes (2022–2023) show major health gains after hip and knee replacements, reinforcing clinical adoption.

Regulatory and funding frameworks also shape the market. The EU Medical Devices Regulation (MDR) has strengthened safety standards, while FDA guidance supports 3D printing and biocompatibility testing. Public funding further supports innovation, with the NIAMS FY 2024 budget at US$ 685 million for musculoskeletal research. Policies like the U.S. CMS bundled payment model (CJR) also favor durable, infection-resistant biomaterials by linking payments to outcomes. Together, ageing populations, obesity, trauma, regulatory clarity, and research funding ensure sustained growth across trauma, spine, sports medicine, and joint reconstruction.

Key Takeaways

- In 2024, the orthopedic biomaterials market generated revenues of about US$ 22.71 billion, with a growth rate (CAGR) of 7.9% expected.

- Analysts predict the market will almost double, reaching approximately US$ 48.58 billion by 2034, driven by rising orthopedic procedures and innovations.

- System type segmentation shows metals as the clear leader in 2024, accounting for 46.3% share due to strength, durability, and broad medical use.

- Ceramics, bioactive glasses, polymers, calcium phosphate cements, and composites follow metals, each contributing niche applications in orthopedic biomaterial development and clinical use.

- In applications, joint replacement and reconstruction dominated 2024 with a 40.8% share, reflecting increasing demand for hip, knee, and spine procedures.

- Other major application areas include orthopedic implants, orthobiologics, viscosupplementation, and bio-resorbable tissue fixation, all showing significant potential for future market growth.

- Hospitals accounted for the largest end-user segment in 2024 with 55.8% share, highlighting their central role in orthopedic surgeries and biomaterials adoption.

- Specialty clinics, ambulatory surgical centers, and other facilities also contribute steadily, though hospitals remain the primary access point for biomaterial-based treatments.

- North America dominated globally in 2024, capturing 37.1% market share, largely due to advanced healthcare infrastructure and a growing elderly patient population.

Regional Analysis

North America leads the orthopedic biomaterials market with a 37.1% share in 2024. This dominance is driven by advanced healthcare infrastructure, high disposable income, and strong demand for orthopedic treatments. The U.S. and Canada perform a large number of orthopedic surgeries every year. These include joint replacements, spinal surgeries, and fracture fixations. The region’s hospitals and clinics are equipped with advanced technology. This allows orthopedic surgeons to adopt new biomaterials quickly, driving market adoption and ensuring better treatment outcomes.

The aging population in North America is a major growth driver. Older adults often face musculoskeletal problems, which require treatments such as hip and knee replacements. Rising cases of osteoarthritis and osteoporosis further increase the demand for orthopedic biomaterials. The region’s strong insurance coverage supports accessibility to these procedures. Patients can afford advanced treatments, reducing cost barriers. With life expectancy rising, the number of people needing orthopedic care is expected to grow steadily, boosting long-term demand for innovative biomaterials.

Major companies are central to North America’s strong position in this market. Leading manufacturers such as Stryker, Zimmer Biomet, and Johnson & Johnson operate in the region. Their investments in research and development result in advanced biomaterials being introduced regularly. Innovations include more durable metals, biocompatible polymers, and enhanced ceramics. These materials improve patient recovery and implant longevity. The strong presence of global leaders also drives competition. This ensures that hospitals and healthcare providers in North America have access to cutting-edge orthopedic products.

Research and development investments further support North America’s leadership. The region benefits from high healthcare spending and supportive government policies. Universities and research centers collaborate with industry players to develop next-generation biomaterials. Funding for clinical trials helps in bringing safer and more effective products to market. The focus is not only on improving implant durability but also on creating biomaterials that enhance natural bone healing. This strong innovation ecosystem ensures North America remains at the forefront of the orthopedic biomaterials market.

Emerging Trends

- 3D Printing for Custom Implants: 3D printing is transforming orthopedic implants. It allows the creation of patient-specific implants that match individual anatomy. This customization ensures a better fit during surgery. A well-fitted implant reduces the risk of complications, such as misalignment or implant loosening. It also supports faster healing and recovery for patients. Surgeons can design implants based on detailed imaging data. This approach is especially useful for complex bone fractures or deformities. As technology improves, 3D-printed implants are becoming more affordable and widely available. Hospitals and clinics are increasingly adopting this technology to improve surgical outcomes.

- Smart and Responsive Materials: Smart materials are changing the way implants support healing. Some implants now contain iron oxide nanoparticles that react to magnetic fields. This feature can stimulate bone growth and accelerate regeneration. These materials can respond to external signals, actively supporting the healing process. Smart implants reduce recovery time and enhance the overall effectiveness of surgery. They are being studied for applications in spinal repairs, joint replacements, and fracture fixations. Researchers are also exploring ways to make these materials safer and more efficient. This trend shows the potential for implants that do more than just provide structural support—they actively improve patient recovery.

- Bioactive Coatings and Surface Modifications: Bioactive coatings are improving how implants bond with bone tissue. Techniques like plasma treatment or the application of bone matrix proteins enhance implant surfaces. These modifications increase cell adhesion and stimulate bone growth around the implant. Stronger integration reduces the risk of implant failure and complications. Bioactive coatings can also improve long-term durability. They are especially beneficial for patients with osteoporosis or poor bone quality. Surgeons can use these implants in joint replacements, dental implants, and fracture repair. Research continues to focus on developing coatings that are more effective, safe, and compatible with the body.

- Nanotechnology in Biomaterials: Nanotechnology is helping implants mimic natural bone structures. Nanoscaffolds and bioactive glasses support cell growth at the microscopic level. This encourages tissue regeneration and faster healing. Nanomaterials can be designed to release growth factors slowly, aiding bone repair. They also improve the mechanical strength of implants. Researchers are exploring their use in load-bearing bones and complex fractures. Nanotechnology allows implants to interact with cells more naturally. This trend could reduce recovery time and improve patient outcomes. As production methods become more advanced, nanomaterials are likely to become standard in orthopedic treatments.

- Functionally Graded Materials (FGMs): Functionally graded materials gradually change their composition to match natural bone. This gradient design helps distribute stress evenly across the implant. Reducing stress concentrations can prevent fractures and implant failure. FGMs are used in load-bearing implants like hips and knees. They improve long-term performance and durability of orthopedic devices. The design also promotes better bone integration over time. Researchers are developing FGMs using metals, ceramics, and polymers. These implants are especially beneficial for patients with weak or brittle bones. FGMs represent a major step forward in creating implants that act more like natural bone, enhancing both safety and recovery.

Use Cases

- Joint Replacement and Reconstruction: Orthopedic biomaterials play a vital role in joint replacement surgeries. Materials like polyurethanes and PEEK are commonly used for implants. They are strong, durable, and compatible with the human body. These implants help restore mobility in patients suffering from joint damage or arthritis. Patients experience significant pain relief and improved quality of life. The materials are designed to withstand daily wear and tear. They also reduce the risk of inflammation or rejection. Advances in biomaterial technology have led to implants that mimic natural joint movement. This has improved long-term outcomes and reduced complications. The demand for joint replacements continues to grow globally.

- Bone Grafting and Spinal Implants: Bone graft substitutes are essential in spinal surgeries and bone repair. Bioactive glasses and hydroxyapatite composites are commonly used. These materials promote bone growth and support healing in spinal fusions or fractures. They provide structural stability while encouraging natural bone regeneration. Using biomaterials reduces recovery time and improves surgical outcomes. They are also safer than traditional bone grafts, which may involve donor site complications. The materials are designed to integrate with the patient’s own bone tissue. Spinal implants made from these biomaterials are lightweight, strong, and long-lasting. Increasing spinal surgeries globally is driving demand for these innovative materials.

- Bio-Resorbable Tissue Fixation: Bioresorbable biomaterials are used in tissue fixation procedures, such as ligament or tendon repairs. Materials like magnesium alloys gradually break down in the body. This eliminates the need for a second surgery to remove the implant. They provide temporary support while the tissue heals. The materials are biocompatible and reduce inflammation risk. They are particularly useful in pediatric patients or sports-related injuries. Bioresorbable implants promote natural tissue regeneration. Advances in material science have improved their strength and degradation rate. Surgeons can now choose materials tailored to each patient’s needs. This approach reduces recovery time and lowers healthcare costs.

- Trauma and Sports Injury Management: Orthopedic biomaterials are widely used in trauma and sports injury care. Materials such as advanced polymers and metal alloys are applied to fix broken bones, ligaments, and tendons. They provide strong support and stabilize injured areas. Patients can recover faster and return to daily activities sooner. Sports injuries, road accidents, and work-related trauma are major drivers of biomaterial use. Continuous research has improved their durability and biocompatibility. These materials also reduce infection risk and promote faster healing. The market for trauma-related implants is growing due to higher injury rates worldwide. Hospitals increasingly rely on biomaterials to improve patient outcomes.

Conclusion

The orthopedic biomaterials market is set for strong and sustained growth, driven by rising musculoskeletal conditions, ageing populations, and increasing demand for joint and spine procedures. Innovations like 3D-printed implants, smart materials, and bioactive coatings are improving patient outcomes and surgical efficiency. Hospitals remain the primary end-users, while specialty clinics and surgical centers steadily contribute to adoption. North America continues to lead due to advanced healthcare infrastructure, supportive regulations, and active research investments. Overall, the market is evolving with a focus on safer, more durable, and patient-specific biomaterials, ensuring better recovery, longer implant life, and expanding opportunities across trauma, sports medicine, and joint reconstruction applications.

View More

Orthopedic Implants Market || Orthopedic Navigation Systems Market || Pediatric Orthopedic Implant Market || Wrist Replacement Orthopedic Devices Market || Orthopedic Devices Market || Orthopedic Bone Cement Market || Orthopedic Contract Manufacturing Market || Orthopedic Drugs Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)