Table of Contents

Overview

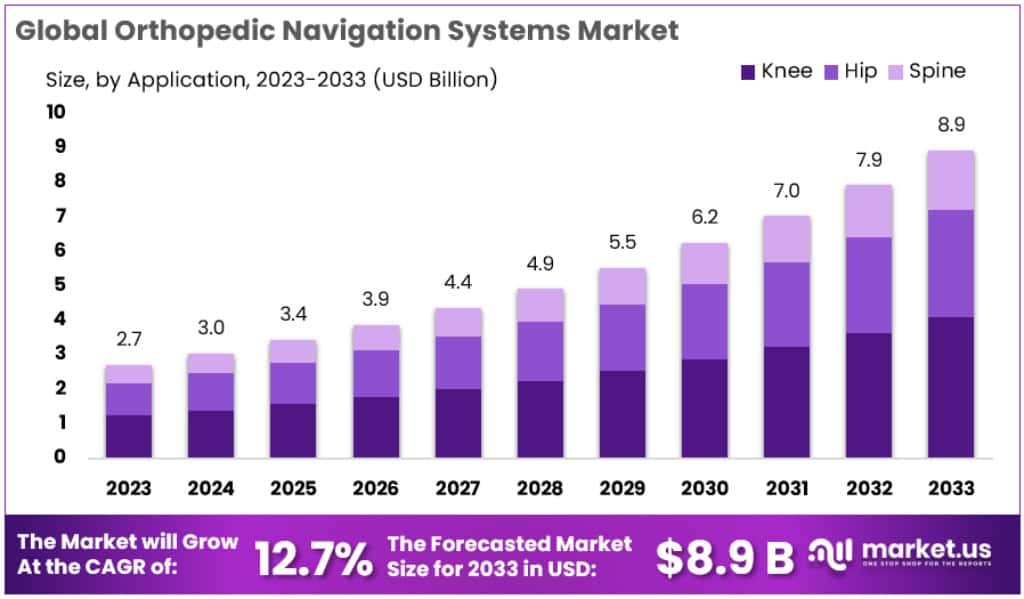

The Global Orthopedic Navigation Systems Market is projected to reach USD 8.9 billion by 2033, rising from USD 2.7 billion in 2023, at a CAGR of 12.7%. Orthopedic navigation systems are computer-assisted surgical tools that guide implant positioning and bone preparation. Their adoption is expanding due to a growing surgical patient base, rising accuracy requirements, and supportive regulatory frameworks. The U.S. FDA classifies these under “computer-assisted surgical systems,” with multiple approvals through the 510(k) pathway. Such regulatory clarity has reduced adoption barriers by defining safety and intended use standards.

Population ageing is a significant driver. The World Health Organization (WHO) projects that people aged 60 years and above will rise from 1 billion in 2019 to 2.1 billion by 2050. Joint diseases and degenerative conditions increase with age, creating a higher need for hip and knee replacement surgeries. Orthopedic navigation systems are positioned to support precision and consistency in such procedures, offering clinical and long-term benefits.

The growing burden of osteoarthritis further strengthens demand. According to WHO, about 528 million people were living with osteoarthritis in 2019, reflecting a 113% increase since 1990. The knee remains the most affected joint, driving procedure volumes for replacements where navigation adds significant value. This rising disease prevalence translates into strong and consistent demand for advanced surgical technologies.

Surgical volumes in developed countries highlight sustained growth potential. OECD data indicate averages of 172 hip replacements and 119 knee replacements per 100,000 population, with several nations exceeding these levels. Such high baseline volumes support consistent expansion of installed systems. Hospitals and healthcare providers are focusing on upgrading operating theatres with enabling technologies that improve reproducibility, accuracy, and long-term outcomes.

Adoption Factors and Clinical Evidence

Government-led quality measurement programmes are reinforcing the adoption of navigation systems. OECD findings show that hip replacements significantly improve patient-reported quality of life, raising the importance of precision in implant alignment. In the UK, the National Health Service (NHS) runs PROMs programmes for joint replacements, reporting tens of thousands of cases each year. These initiatives highlight outcome measurement, encouraging hospitals to standardise alignment and performance through computer-assisted navigation systems.

Clinical evidence further validates technology benefits. Randomised trials and prospective studies indexed by the U.S. National Institutes of Health reveal that computer-assisted total knee arthroplasty improves radiographic alignment and corrects deformity more effectively than conventional methods. Although early functional outcomes may appear similar, alignment accuracy supports long-term implant survival and reduced revision rates. This alignment advantage is a strong motivator for surgeons and purchasers focused on reproducibility and durability.

In the United States, the CDC reports that around 58.5 million adults live with arthritis, and over 25 million face activity limitations due to the condition. The prevalence of arthritis rises with age, signaling ongoing demand for orthopedic procedures. These conditions put continuous pressure on healthcare systems and increase the relevance of technologies that support surgical efficiency without compromising precision.

Health technology assessment bodies have also reviewed enabling solutions. For example, NICE in the UK acknowledges the role of navigation in joint replacement pathways. While not yet the universal standard of care, the inclusion of navigation in formal assessments shows system-level recognition of its value. Moreover, post-pandemic recovery of elective surgery has revived hip and knee replacement volumes. The NHS has reported efforts to reduce surgical backlogs, and navigation systems are increasingly considered part of theatre modernisation strategies.

In conclusion, market growth is being shaped by population ageing, rising osteoarthritis burden, sustained procedure volumes, regulatory clarity, and clinical validation of improved alignment outcomes. These drivers collectively ensure steady adoption of orthopedic navigation systems, positioning them as essential tools for accuracy, consistency, and improved surgical results.

Key Takeaways

- The Orthopedic Navigation Systems Market is projected to expand from USD 2.7 billion in 2023 to nearly USD 8.9 billion by 2033.

- This expansion corresponds to a Compound Annual Growth Rate (CAGR) of 12.7% throughout the forecast period spanning 2023 to 2033.

- Knee navigation systems dominated in 2023 with over 45.9% share, supported by a rising trend in global knee replacement surgical procedures.

- Hospitals emerged as the leading end-users in 2023, capturing more than 56.2% market share due to their extensive medical infrastructure and resources.

- North America led the market with a 45.1% share in 2023, driven by advanced healthcare systems and strong patient awareness levels.

- Asia Pacific is anticipated to grow fastest with a CAGR of 13.7%, propelled by unmet clinical demands and proactive government healthcare initiatives.

- The top five players—Stryker, Zimmer Biomet, Smith & Nephew, Medtronic, and NuVasive—jointly commanded over 60% of the global market share.

Regional Analysis

In 2023, North America accounted for the largest share of the Orthopedic Navigation Systems Market. The region held 45.1% of the market, valued at USD 1.21 billion. This dominance is driven by advanced healthcare infrastructure and strong adoption of innovative technologies. High awareness among surgeons and patients regarding the benefits of navigation systems further strengthens the market position. Rising demand for precision in orthopedic surgeries has accelerated the deployment of these solutions, ensuring sustained leadership in the region.

The growing elderly population has been a major contributor to this expansion. The rising prevalence of musculoskeletal disorders has resulted in increased demand for advanced surgical navigation solutions. Government spending on healthcare services remains substantial, ensuring wider access to modern treatment methods. The presence of favorable reimbursement policies further supports patients and providers in adopting navigation systems. This creates a robust environment for growth and strengthens the market leadership of North America in the global orthopedic navigation segment.

North America is also home to several established medical device manufacturers. These companies actively invest in research and development, bringing innovation and advanced navigation products to the market. Strong competition among these players ensures continuous technological upgrades and better clinical outcomes. The presence of advanced hospitals and specialty clinics creates a fertile ground for product adoption. With strong supply networks and consistent product launches, North American manufacturers significantly influence the growth trajectory of the global orthopedic navigation systems industry.

Collaborations between professional bodies and academic institutions are further shaping the market. Organizations such as the American Board of Orthopedic Surgeries support initiatives that enhance surgeon training and skill development. Educational partnerships promote advanced learning programs that familiarize surgeons with navigation technologies. This enhances surgical precision and improves patient outcomes. Together with supportive government policies, such initiatives foster innovation and strengthen market adoption. These factors collectively reinforce North America’s dominance and ensure continued leadership in the orthopedic navigation systems market.

Segmentation Analysis

In 2023, knee navigation systems led the orthopedic navigation systems market with over 45.9% share. This growth was fueled by the rising number of knee replacement surgeries and advancements in knee navigation technology. Increasing awareness among patients and surgeons about advanced surgical options supported adoption. An aging population also contributed to demand, as knee disorders are more prevalent in older age groups. Manufacturers emphasized minimally invasive and precise techniques, strengthening the appeal of these systems and reinforcing their dominant position among orthopedic surgeons worldwide.

Hip navigation systems also demonstrated notable growth in 2023. The segment’s expansion was attributed to advancements that improved surgical accuracy and efficiency in hip replacement procedures. Rising cases of osteoarthritis and hip dysplasia fueled adoption. These systems gained popularity due to their ability to reduce complications and lower revision surgery rates. As surgeons prioritize improved outcomes and efficiency, hip navigation technologies are increasingly integrated into clinical practice, making them a valuable tool in modern orthopedic procedures and contributing to steady market expansion.

Spine navigation systems recorded significant momentum in the orthopedic navigation market. Growth was supported by the rising prevalence of spinal disorders and the need for precision in complex spinal surgeries. These systems enhance implant placement accuracy through real-time visualization, reducing surgical risks and complications. Ongoing technological innovations and a strong focus on patient safety are expected to further drive adoption. With increasing demand for precision-driven outcomes, spine navigation systems are likely to achieve wider acceptance, establishing themselves as an important segment in orthopedic navigation solutions.

Key Players Analysis

The orthopedic navigation systems market is dominated by a few global players, with the top five firms collectively accounting for more than 60% of the total market. Stryker leads this segment with a commanding 25% share, supported by its wide product portfolio spanning joint replacement, spine, and trauma surgeries. The company’s systems are highly valued for their precision, ease of use, and clinical reliability. Strong presence in developed countries and increasing penetration into emerging markets further strengthen Stryker’s position as the global leader.

Zimmer Biomet follows closely, securing approximately 20% of the global market share. The company has built a reputation for high-quality navigation systems, known for effectiveness and reliability in orthopedic procedures. A notable differentiator is its leadership in robotic-assisted surgery, where its platforms are driving innovation and adoption in hospitals worldwide. With robotic technologies becoming more integral to orthopedic care, Zimmer Biomet is strategically positioned to expand its market influence further and reinforce its standing as a key competitor to Stryker.

Smith & Nephew holds the third-largest share, accounting for nearly 15% of the market. The company’s solutions are particularly focused on joint replacement procedures and are recognized for advanced design and user-friendly features. Its NAVIO robotic-assisted platform demonstrates Smith & Nephew’s commitment to innovation and expanding applications in surgical navigation. While its global market share trails the two leaders, the company continues to strengthen its competitive position through new product development, technological upgrades, and expansion into emerging economies where demand for orthopedic navigation systems is steadily rising.

Market Key Players

- B. Braun Melsungen AG

- Zimmer Biomet

- Stryker Corporation

- Amplitude Surgical

- Medtronic Plc

- Kinamed Inc.

- Smith & Nephew Plc

- Medical Device Business Services, Inc.

- Globus Medical

- Other Key Players

FAQ

1. What are orthopaedic navigation systems?

Orthopaedic navigation systems are advanced computer-assisted tools designed to guide surgeons during complex orthopaedic procedures. They use digital imaging and tracking technologies to provide a clear, three-dimensional view of the patient’s anatomy in real time. These systems help in planning and executing surgeries like joint replacements and spine procedures with higher accuracy. By reducing manual guesswork, they improve alignment and precision. Their role is to enhance surgical outcomes, reduce complications, and support minimally invasive surgical practices in modern healthcare.

2. How do these systems work?

These systems function by combining imaging techniques such as CT scans, MRI, or fluoroscopy with real-time tracking devices. The data is processed into a 3D model that displays the patient’s anatomy. During surgery, optical or electromagnetic trackers monitor instrument movements with accuracy. Surgeons can see precise feedback on a display, ensuring correct alignment of implants or cuts. This technology reduces human error, provides visual guidance, and increases confidence in complex procedures. It transforms surgical planning into safer, data-driven execution.

3. What are the main applications of orthopaedic navigation systems?

Orthopaedic navigation systems are used across multiple procedures that demand accuracy. Their primary applications include total knee arthroplasty, total hip arthroplasty, spine surgeries, and complex trauma reconstructions. They help align implants with precision, improve joint stability, and extend implant longevity. In spinal surgeries, navigation reduces risks of nerve damage and misalignment. In trauma cases, it supports reconstruction with accurate placement of screws and plates. Their ability to improve functional outcomes has led to increasing adoption in hospitals and surgical centers.

4. What are the benefits of using orthopaedic navigation systems?

The benefits of these systems lie in their ability to enhance surgical precision and patient safety. They provide accurate implant positioning, leading to fewer complications and better functional results. By guiding surgeons with real-time visualization, they reduce reliance on manual estimation. Studies show that patients experience improved mobility and lower revision surgery rates. Additionally, the technology enables minimally invasive approaches, resulting in faster recovery and less blood loss. Overall, orthopaedic navigation systems represent a reliable advancement in orthopaedic surgery.

5. What are the limitations of orthopaedic navigation systems?

Despite their benefits, these systems face several challenges that limit widespread adoption. The primary barrier is the high cost of installation and maintenance, which restricts use in smaller hospitals. There is also a learning curve, as surgeons must undergo training to use them effectively. Initial surgeries may take longer as teams adapt to new workflows. System accuracy depends on imaging quality, which can affect outcomes. Additionally, integration with existing surgical practices requires adjustments. These factors slow broader global adoption.

6. What technologies are commonly used in navigation systems?

Navigation systems employ advanced tracking and visualization technologies. Optical tracking systems use infrared cameras and markers to monitor instrument positions. Electromagnetic tracking eliminates line-of-sight issues by using magnetic fields for guidance. Robotics-integrated navigation combines real-time imaging with robotic arms for enhanced stability and accuracy. Artificial intelligence is being applied to improve surgical planning, predict outcomes, and refine techniques. Together, these technologies provide surgeons with reliable tools for precision and safety. Their development is shaping the future of orthopaedic surgeries worldwide.

7. How are orthopaedic navigation systems different from robotic surgery systems?

Orthopaedic navigation systems guide surgeons with real-time imaging and tracking but do not perform physical tasks. They act as a supportive tool, enhancing visualization and decision-making during surgery. Robotic systems, in contrast, can perform specific surgical movements under surgeon supervision, often integrating navigation software for guidance. Navigation improves accuracy, while robotics adds automation and stability. Both technologies aim to improve patient outcomes but differ in function. Many modern solutions now combine robotics and navigation to maximize precision and efficiency.

8. What is the current size of the orthopaedic navigation systems market?

Global Orthopedic Navigation Systems Market size is expected to be worth around USD 8.9 Billion by 2033, from USD 2.7 Billion in 2023, growing at a CAGR of 12.7% during the forecast period from 2023 to 2033. Growth is being fueled by rising surgical volumes, technological advancements, and demand for minimally invasive procedures. The increasing prevalence of musculoskeletal disorders is also boosting adoption. Hospitals in developed regions are leading usage, while emerging markets are gradually adopting the systems. With continuous innovation and healthcare infrastructure investments, the market has become a crucial segment of the medical technology industry worldwide, attracting investors and manufacturers.

9. What is the expected growth rate of the market?

The orthopaedic navigation systems market is projected to grow steadily at a compound annual growth rate (CAGR) of 12.7% in the coming years. Factors such as rising ageing populations, higher surgical volumes, and demand for advanced treatment methods are driving expansion. Technology integration with robotics and artificial intelligence is expected to further accelerate growth. Regional disparities remain, with North America and Europe leading adoption. However, Asia-Pacific is anticipated to record the fastest growth, supported by expanding healthcare systems and increasing medical tourism.

10. What factors are driving market growth?

The market is being driven by multiple demand-side and supply-side factors. Growing cases of osteoarthritis, osteoporosis, and spinal disorders are increasing surgical requirements. Patient preference for minimally invasive surgeries is creating demand for precision-based technologies. Innovations in artificial intelligence, robotics integration, and smart imaging are pushing adoption further. In addition, increasing awareness of surgical accuracy and improved patient safety supports global demand. Healthcare spending, particularly in developed regions, ensures availability of advanced systems. Collectively, these factors create strong growth opportunities for manufacturers and providers.

11. What challenges are restraining market growth?

Despite promising growth, several challenges are limiting wider adoption of orthopaedic navigation systems. High initial costs remain a major concern, especially in developing regions with limited budgets. Reimbursement barriers in some healthcare systems reduce patient affordability. The complexity of system use requires extensive surgeon training, which slows integration into practice. Smaller hospitals and surgical centers often face financial and operational hurdles. Technical issues, such as imaging dependency, also impact effectiveness. These factors collectively create obstacles that manufacturers must address for broader market penetration.

12. Which regions dominate the orthopaedic navigation systems market?

North America dominates the market due to advanced healthcare infrastructure, strong reimbursement systems, and high adoption of medical technologies. The United States is the largest contributor, supported by a high number of orthopaedic surgeries each year. Europe follows, with Germany, the UK, and France showing strong demand driven by ageing populations and supportive healthcare policies. Asia-Pacific is emerging as the fastest-growing region, driven by medical tourism, rising disposable incomes, and infrastructure expansion. Countries like China and India are leading growth opportunities.

13. Who are the key players in the market?

The orthopaedic navigation systems market is highly competitive, with several global players dominating supply. Key companies include Stryker Corporation, Medtronic plc, Zimmer Biomet, Brainlab AG, Smith & Nephew, and Johnson & Johnson through its DePuy Synthes division. These firms invest heavily in research and development to advance technologies such as robotics integration and artificial intelligence-based planning. Strategic partnerships, acquisitions, and geographic expansion are common approaches to strengthen market presence. Their focus remains on improving product portfolios and addressing surgeon and hospital requirements worldwide.

14. What future trends will shape the market?

Future growth will be shaped by integration of robotics with navigation systems, offering enhanced accuracy and stability. Artificial intelligence is expected to play a major role in predictive analytics and surgical planning, improving efficiency. Cloud-based data sharing will enable remote consultations and tele-surgery support. Outpatient and ambulatory surgical centers are also likely to adopt these systems, driven by demand for cost-efficient solutions. The focus on personalized treatment, coupled with faster recovery rates, will influence adoption. These innovations are reshaping market dynamics globally.

Conclusion

The orthopedic navigation systems market is moving toward strong and steady growth, driven by rising surgical needs, an ageing population, and increasing cases of joint and spine disorders. Hospitals are focusing on upgrading surgical theatres with advanced tools that improve accuracy, safety, and long-term results. Clinical studies have confirmed the value of navigation in ensuring precise implant placement and reducing revision surgeries. Regulatory clarity, wider adoption in developed markets, and faster uptake in emerging regions are further supporting expansion. With continued innovation, integration of robotics, and government support for modern healthcare, orthopedic navigation systems are positioned to become an essential part of advanced surgical practices worldwide.

View More

Orthopedic Implants Market || Pediatric Orthopedic Implant Market || Wrist Replacement Orthopedic Devices Market || Orthopedic Devices Market || Orthopedic Bone Cement Market || Orthopedic Contract Manufacturing Market || Orthopedic Drugs Market || Orthopedic Biomaterials Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)