Table of Contents

Overview

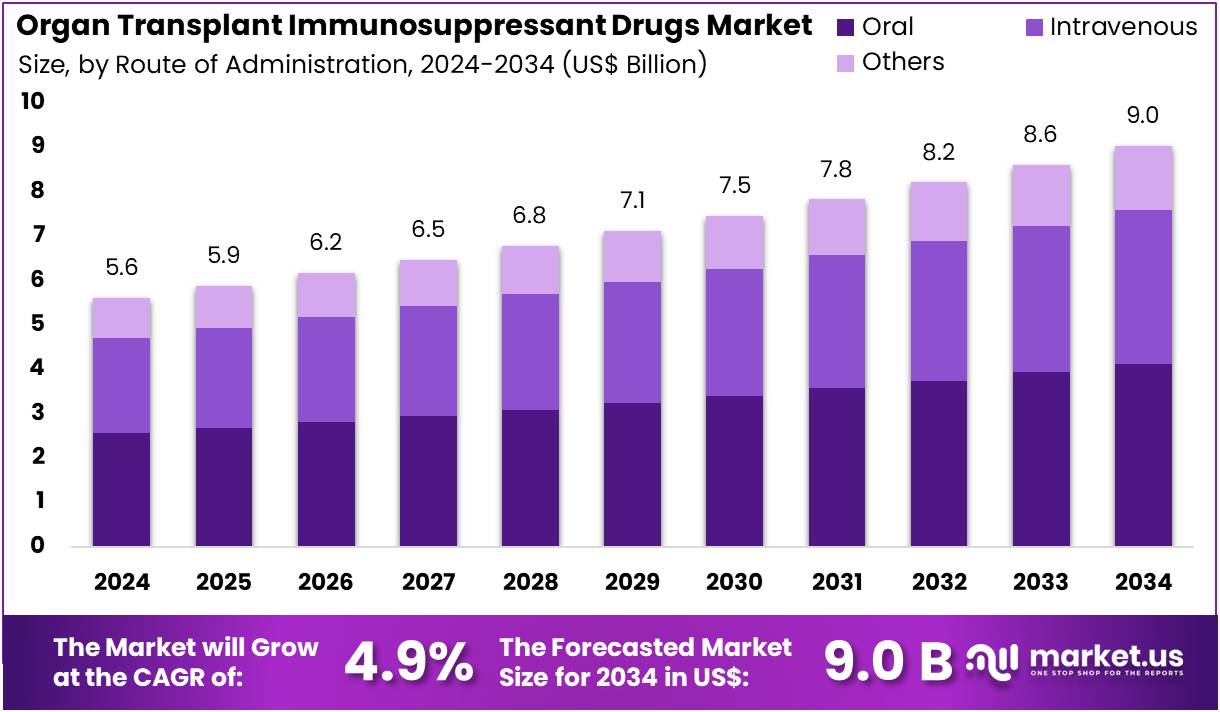

New York, NY – July 30, 2025 – The Organ Transplant Immunosuppressant Drugs Market Size is expected to be worth around US$ 9.0 Billion by 2034 from US$ 5.6 billion in 2024, growing at a CAGR of 4.9% during the forecast period 2025 to 2034.

The global organ transplant immunosuppressant drugs market is witnessing steady expansion, driven by the increasing number of organ transplant procedures and advancements in immunosuppressive therapies. Immunosuppressant drugs play a critical role in preventing organ rejection by suppressing the recipient’s immune response post-transplantation.

The rising prevalence of chronic diseases such as kidney failure, liver cirrhosis, and heart failure has led to a significant increase in organ transplants worldwide. According to data from global health authorities, over 150,000 solid organ transplants were performed globally in 2023. This surge in transplants has directly contributed to the growing demand for immunosuppressive medications.

Key drug classes in the market include calcineurin inhibitors, corticosteroids, mTOR inhibitors, and antiproliferative agents. Among these, tacrolimus and cyclosporine remain the most widely prescribed drugs due to their efficacy and established safety profiles. The development of newer formulations with improved bioavailability and fewer side effects is further enhancing patient outcomes.

North America dominates the global market, supported by a high transplant rate, favorable reimbursement policies, and robust healthcare infrastructure. Meanwhile, Asia Pacific is expected to exhibit the fastest growth, driven by improving healthcare access and increasing transplant capabilities. With rising transplant needs and continuous innovations, the organ transplant immunosuppressant drugs market is projected to grow steadily in the coming years.

Key Takeaways

- In 2024, the global organ transplant immunosuppressant drugs market generated revenue of approximately US$ 5.6 billion. The market is projected to grow at a compound annual growth rate (CAGR) of 4.9%, reaching an estimated value of US$ 9.0 billion by 2034.

- Based on drug class, the market is categorized into calcineurin inhibitors, antiproliferative agents, mTOR inhibitors, corticosteroids, monoclonal antibodies, and others. Among these, calcineurin inhibitors accounted for the largest share in 2023, capturing 34.2% of the total market, owing to their widespread use and proven clinical efficacy.

- By organ type, the market is segmented into kidney, liver, heart, lung, pancreas, and others. Kidney transplants constituted the largest segment, holding a 37.5% share, driven by the high global incidence of end-stage renal disease.

- In terms of route of administration, the market is divided into oral, intravenous, and others. Oral formulations dominated the segment, accounting for 45.6% of the total market revenue, supported by ease of use and patient adherence.

- Considering the distribution channel, hospital pharmacies, retail pharmacies, and online pharmacies are included. Hospital pharmacies emerged as the leading channel, capturing 52.3% of the revenue share due to their critical role in transplant medication dispensing.

- Regionally, North America led the market in 2023, representing a 41.6% share, supported by a high transplant rate and robust healthcare infrastructure.

Segmentation Analysis

- Drug Class Analysis: Calcineurin inhibitors held a 34.2% market share in 2023 due to their critical role in preventing organ rejection, especially in kidney and liver transplants. Drugs like tacrolimus and cyclosporine are widely prescribed for their efficacy in immune suppression. Market growth is supported by the increasing number of transplant procedures and innovations in drug formulations that enhance effectiveness while minimizing adverse effects. The segment is further strengthened by the global rise in chronic kidney disease cases requiring long-term immunosuppression.

- Organ Type Analysis: The kidney transplant segment accounted for 37.5% of the market, driven by the rising prevalence of kidney failure associated with diabetes, hypertension, and chronic kidney disease. Kidney transplants are often preferred due to higher success rates and the high costs of long-term dialysis treatments. Demand is expected to grow in both developed and emerging economies. Additionally, ongoing innovations in targeted immunosuppressive therapies for kidney transplants are expected to sustain pharmaceutical interest and investment in this segment.

- Route of Administration Analysis: Oral administration led the market with a 45.6% revenue share, supported by patient preference for non-invasive treatment options. Oral drugs such as tacrolimus and mycophenolate mofetil offer convenience and improved adherence, eliminating the need for hospital-based intravenous dosing. This segment benefits from the shift toward outpatient care and the development of advanced oral formulations with better absorption and fewer side effects. Healthcare systems are also prioritizing adherence strategies, making oral immunosuppressants the dominant delivery route in transplant care.

- Distribution Channel Analysis: Hospital pharmacies dominated the distribution channel segment, capturing 52.3% of revenue due to their central role in dispensing post-transplant medications. Their integration with transplant centers allows for specialized handling of complex immunosuppressive regimens. Growth in this segment is supported by rising transplant volumes and collaborations between hospitals and pharmaceutical companies to streamline access to personalized therapies. As the number of specialized treatments increases, hospital pharmacies are expected to remain the preferred channel for transplant medication management.

Market Segments

By Drug Class

- Calcineurin Inhibitors

- Antiproliferative Agents

- mTOR Inhibitors

- Corticosteroids

- Monoclonal Antibodies

- Others

By Organ Type

- Kidney

- Liver

- Heart

- Lung

- Pancreas

- Others

By Route of Administration

- Oral

- Intravenous

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Regional Analysis

North America Dominates the Organ Transplant Immunosuppressant Drugs Market

North America accounted for the largest revenue share of 41.6% in the global organ transplant immunosuppressant drugs market. This leading position is attributed to the long-term management needs of transplant recipients and supportive healthcare policies. A key development contributing to market growth is the Medicare immunosuppressive drug benefit, which was implemented on January 1, 2023. This policy ensures continued coverage of immunosuppressive therapy for specific kidney transplant patients, even after their standard Medicare ESRD benefits conclude. By February 2024, 104 patients had enrolled, indicating a phased rollout of the program.

The policy significantly reduces financial burdens on patients, previously a major cause of therapy discontinuation and transplant failure. By ensuring uninterrupted access to essential medications, the initiative is expected to enhance graft survival rates and improve long-term patient outcomes. Furthermore, the increasing survival of transplant recipients is generating sustained demand for immunosuppressive drugs. Together, these factors reinforce North America’s strong position in the global market.

Asia Pacific Expected to Record the Fastest Growth Rate

The Asia Pacific region is projected to register the highest compound annual growth rate (CAGR) during the forecast period. This growth is driven by escalating healthcare investments and a rising number of transplant procedures. According to the World Bank, health expenditure in East Asia and the Pacific reached 5.43% of GDP in 2022, signaling robust government commitment to healthcare expansion.

This increased funding is enabling the development of advanced transplant programs, especially across emerging economies. As transplant infrastructure improves, accessibility to life-saving procedures is expected to increase, driving demand for post-transplant immunosuppressive therapies. Moreover, enhanced diagnostics and broader healthcare coverage are likely to identify more candidates for organ transplantation. These developments collectively position Asia Pacific as a high-growth region, offering substantial opportunities for market expansion in the years ahead.

Emerging Trends

Shift toward costimulatory blockade

The use of costimulatory inhibitors such as belatacept is expanding as an alternative to traditional calcineurin inhibitors. Belatacept-based regimens are being studied in more patients, with the goal of reducing long-term kidney toxicity and improving graft survival. Induction therapy with agents targeting T-cell costimulation is now employed in over 90 % of kidney transplants and in more than 50 % of other solid-organ transplants.

Real-world evidence (RWE) driving label expansions

Regulatory approvals are increasingly based on observational studies and registry data. For example, in early 2021 the FDA approved a new use for tacrolimus (Prograf) to prevent rejection in lung transplant recipients based on RWE demonstrating safety and effectiveness in real-world practice. This approach accelerates access to therapies for broader patient groups.

Personalized dosing via therapeutic drug monitoring

Guidance documents have reclassified cyclosporine and tacrolimus assays to improve accuracy in measuring drug levels. These special-control guidances reflect a trend toward tailoring immunosuppressant doses to each patient’s metabolism and risk profile, aiming to balance rejection prevention with minimized toxicity.

Exploration of tolerance-inducing strategies

Research is focusing on protocols that may one day allow reduced lifelong immunosuppression. Trials are evaluating cellular therapies, such as regulatory T-cell infusions, and novel agents designed to promote immune tolerance of the graft without continuous high-dose drugs. Early-phase studies suggest potential for long-term graft acceptance with fewer side effects.

Use Cases

Prevention of rejection in kidney, heart, and liver transplants

Mycophenolate mofetil (MMF; CellCept) is indicated for prophylaxis of organ rejection in adult and pediatric recipients aged 3 months and older following kidney, heart, or liver transplantation. MMF is routinely combined with a calcineurin inhibitor and corticosteroids to maintain graft function.

Standard induction therapy protocols

Induction immunosuppression is administered at the time of transplantation to prevent early acute rejection. Agents such as anti-thymocyte globulin or interleukin-2 receptor antagonists are used in more than 90 % of kidney transplants and in over 50 % of heart, lung, and liver transplants, reducing the need for high maintenance doses later.

Widespread application across transplant volume

In the United States, 46,632 organ transplants were performed in 2023 an 8.7 % increase over 2022. All of these recipients require lifelong immunosuppressive therapy to prevent graft rejection. Of these procedures, 39,679 involved deceased donors and 6,953 involved living donors.

Dose adjustment through therapeutic monitoring

Routine measurement of trough levels for tacrolimus and cyclosporine enables clinicians to adjust dosing precisely. This practice helps maintain drug concentrations within a target range, reducing risks of toxicity (e.g., nephrotoxicity) while ensuring sufficient immunosuppression to protect the graft.

Conclusion

The global organ transplant immunosuppressant drugs market is poised for steady growth, driven by rising transplant volumes, innovations in drug formulations, and supportive healthcare policies. Key segments such as calcineurin inhibitors and kidney transplants dominate due to clinical efficacy and high prevalence of renal failure.

North America leads the market, while Asia Pacific is emerging as a high-growth region due to expanding healthcare access. Advancements in personalized dosing, real-world evidence, and tolerance-inducing therapies are shaping future treatment landscapes. With growing demand and continuous clinical innovation, the market is expected to witness sustained expansion through 2034.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)