Table of Contents

Overview

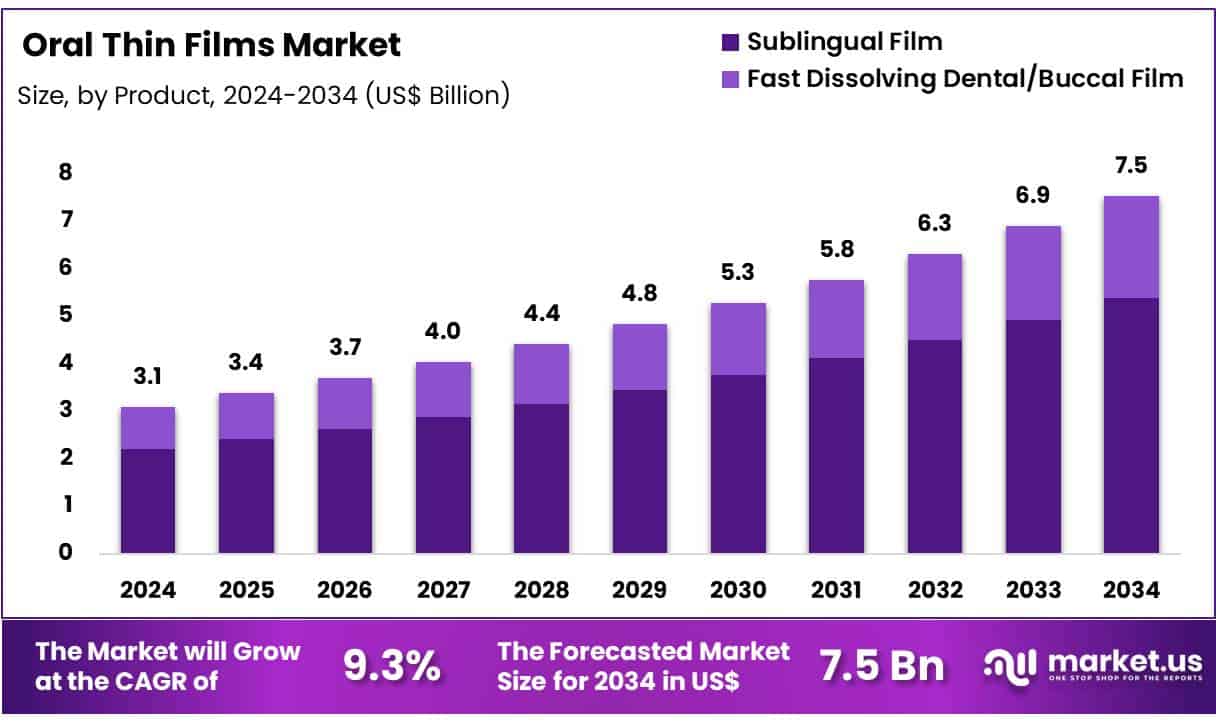

New York, NY – June 16, 2025 – Global Oral Thin Films Market size is expected to be worth around US$ 7.5 Billion by 2034 from US$ 3.1 Billion in 2024, growing at a CAGR of 9.3% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 35.5% share with a revenue of US$ 1.0 Billion.

The global oral thin films (OTFs) market is witnessing growing attention due to increasing interest in non-invasive and patient-friendly drug delivery methods. These thin, dissolvable strips are designed for rapid absorption through the oral mucosa, providing a convenient alternative to tablets, capsules, and injections.

The adoption of oral thin films is expanding across multiple therapeutic categories, including pain relief, allergy treatment, and neurological disorders. Their ease of administration, particularly for pediatric, geriatric, and dysphagic patients, continues to drive clinical preference. Oral thin films offer quick onset of action and eliminate the need for water, which further supports their use in outpatient and emergency settings.

Recent innovations in polymer science and formulation techniques have improved the stability, taste-masking, and drug-loading capacity of these films. As a result, pharmaceutical developers are increasingly exploring this format for both prescription drugs and nutraceutical applications.

North America continues to lead the market due to the presence of advanced drug development infrastructure and supportive regulatory frameworks. At the same time, Asia-Pacific is emerging as a high-growth region, supported by increased healthcare access and expanding pharmaceutical manufacturing. The market outlook remains optimistic as manufacturers explore oral thin films for new drug categories, including vaccines and hormonal therapies, enhancing their clinical and commercial potential.

Key Takeaways

- The global oral thin films market was valued at USD 3.1 billion in 2024 and is projected to reach USD 7.5 billion by 2034, growing at a CAGR of 9.3%.

- In 2024, the sublingual film segment dominated the global market, accounting for 70.3% of the total revenue share.

- The schizophrenia segment emerged as the leading application area, contributing 29.4% to the total market revenue in 2024.

- Hospital pharmacies held the largest share among distribution channels, capturing 41.3% of the global revenue.

- North America continued to lead the global market in 2024, with a revenue share exceeding 35.5%.

Segmentation Analysis

- Product Analysis: In 2024, the sublingual film segment led the global oral thin films market with a 70.3% share. These films enable rapid drug absorption under the tongue, allowing faster onset of action than conventional oral dosage forms. They are ideal for conditions requiring immediate relief, such as pain, seizures, and nausea. Their ease of use, non-invasive nature, and enhanced bioavailability have driven adoption, particularly among patients seeking discreet and portable treatment options.

- Disease Indication Analysis: The schizophrenia segment captured a 29.4% share of the global oral thin films market in 2024. Oral thin films are well-suited for schizophrenia patients due to their ease of use and ability to deliver antipsychotic drugs quickly. These films support better patient compliance by avoiding swallowing difficulties and enabling discreet administration. With rising global mental health concerns and approximately 21 million people affected by schizophrenia, demand for efficient and fast-acting therapies continues to grow.

- Distribution Channel Analysis: Hospital pharmacies accounted for 41.3% of the oral thin films market share in 2024. These settings favor oral thin films due to their quick action, ease of administration, and improved patient outcomes in acute care. They are frequently used for patients with swallowing difficulties, especially in emergency or post-operative conditions. Hospitals benefit from customizable dosage and enhanced patient adherence, reinforcing the preference for these films in clinical environments focused on precision and comfort.

Market Segments

Product

- Sublingual Film

- Fast Dissolving Dental/Buccal Film

Disease Indication

- Schizophrenia

- Migraine

- Opioid Dependence

- Nausea and Vomiting

- Others

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

Regional Analysis

North America held the largest share in the global oral thin films market, supported by well-established healthcare infrastructure and strong awareness of advanced drug delivery technologies. The region’s large population affected by chronic and neurological conditions contributes to sustained demand for patient-friendly treatment formats such as oral thin films. Pharmaceutical companies and research institutions across North America are actively advancing the development and commercialization of these films for therapeutic areas including mental health, pain, and neurological disorders.

A favorable regulatory landscape also supports market growth, with the U.S. Food and Drug Administration (FDA) having approved multiple oral thin film products in recent years. These approvals encourage innovation and facilitate faster product launches. The growing incidence of disorders such as schizophrenia, Parkinson’s disease, and other long-term conditions increases the need for effective, easy-to-administer therapies in the region.

Moreover, the shift toward personalized medicine and a rising preference for non-invasive delivery methods among patients have further accelerated the adoption of oral thin films. This aligns with healthcare providers’ goals to improve treatment adherence and patient outcomes, reinforcing North America’s leading position in the global market.

Emerging Trends

- Additive Manufacturing for Personalized Dosing: Recent studies demonstrate the use of 3D-printing techniques such as fused deposition modeling and LCD photopolymerization to fabricate orodispersible films with precise dose control, patient-specific geometries, and multilayer release profiles. For example, researchers have successfully printed mucoadhesive bilayer films that combine a backing layer for directional release with an adhesive layer for prolonged mucosal contact.

- Mucoadhesive and Multilayer Formulations: Formulation scientists are increasingly incorporating polymers like hydroxypropyl methylcellulose (HPMC) and polyethylene glycol derivatives to enhance film strength, adhesion, and controlled drug release. Liquid-crystal-display 3D-printed films achieved over 80% drug release within 30 minutes while maintaining strong adhesion to buccal mucosa.

- Solvent-Free and Eco-Friendly Manufacturing: Novel solvent-free approaches including hot-melt extrusion and melt casting—are being adopted to eliminate organic solvents, reduce environmental impact, and simplify quality control. Investigations using additive manufacturing and hot-melt extrusion have produced amorphous oral thin films with uniform drug dispersion and improved stability.

- Vaccine and Biologic Delivery Platforms: Building on nanopatch concepts, biomedical engineers at Johns Hopkins have explored repurposing breath-freshener thin-film technology to deliver rotavirus vaccine strips, offering a heat-stable, needle-free option suited for infants in low-resource settings.

- Evolving Regulatory and Quality Guidelines: The FDA’s recent emphasis on content uniformity testing for thin films (per 21 CFR § 460.600) and industry recommendations for laser-scanning confocal microscopy to monitor API distribution reflect a trend toward stricter quality assurance standards.

Use Cases

- Acute Migraine Treatment

- Product Example: Rizafilm (rizatriptan orally disintegrating film), approved by the FDA on April 17, 2023, for adults and pediatric patients (≥ 40 kg) with migraine with or without aura.

- Clinical Need: Migraine affects an estimated 14–15% of the global population, accounting for nearly 4.9% of worldwide disability-adjusted life years.

- Chemotherapy-Induced Nausea and Vomiting (CINV)

- Product Example: Zuplenz (ondansetron oral thin film), first approved July 7, 2010, to prevent moderate to severe CINV without the need for water.

- Incidence: Within five days of chemotherapy, approximately 42% of patients experience nausea and 20.8% experience vomiting without optimal antiemetic control.

- Epilepsy Management

- Product Example: SYMPAZAN™ (clobazam oral film), FDA-approved in 2011 for adjunctive treatment of seizures in Lennox-Gastaut syndrome.

- Disease Burden: Epilepsy affects around 50 million people worldwide, with 70% of cases potentially controlled by appropriate antiseizure therapy.

Conclusion

The global oral thin films (OTFs) market is poised for sustained growth, supported by rising demand for patient-friendly drug delivery, advancements in formulation technologies, and expanding therapeutic applications. Sublingual films dominate due to rapid onset and high bioavailability, particularly for neurological and psychiatric conditions like schizophrenia.

North America remains the leading region, bolstered by regulatory approvals and robust R&D infrastructure. Emerging trends such as 3D-printed films, solvent-free production, and vaccine delivery innovations are reshaping the landscape. As regulatory standards evolve and use cases expand, OTFs are expected to become integral to future pharmaceutical and personalized medicine strategies.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)