Table of Contents

Overview

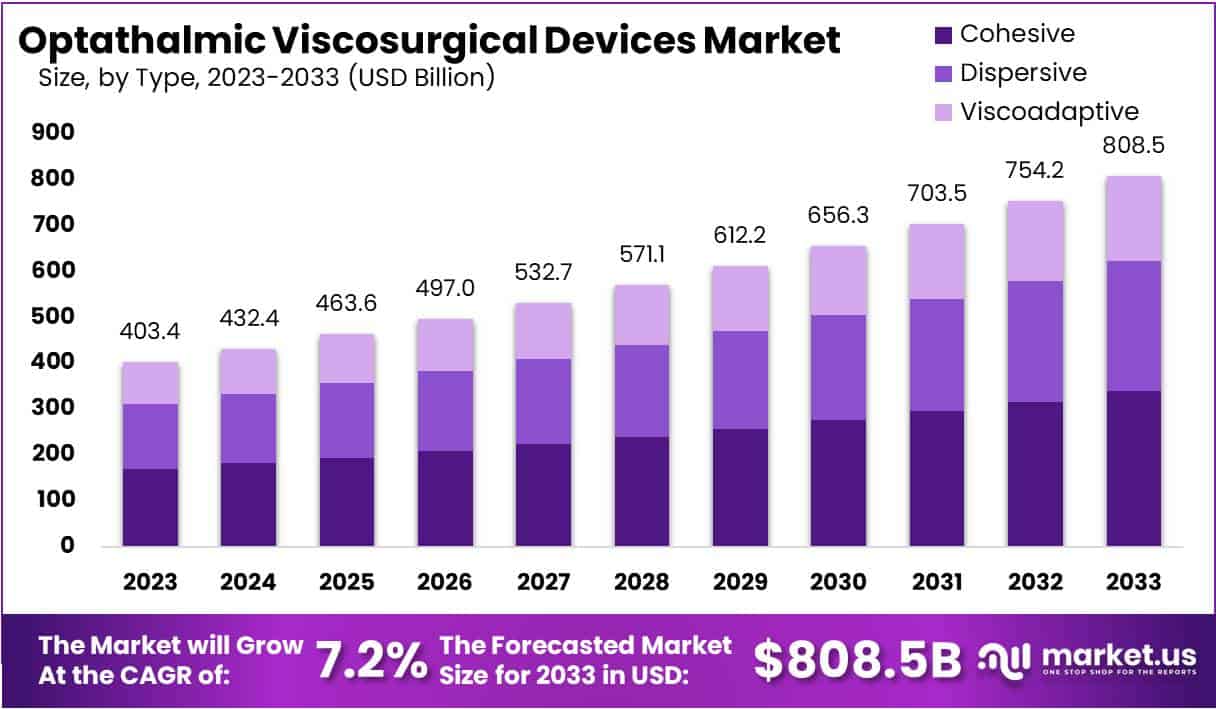

New York, NY – June 24, 2025: The Global Ophthalmic Viscosurgical Devices (OVD) Market is projected to grow from USD 403.4 billion in 2023 to USD 808.5 billion by 2033. This represents a compound annual growth rate (CAGR) of 7.2% from 2024 to 2033. The primary driver behind this growth is the growing elderly population, particularly in low- and middle-income countries. Cataract remains the leading cause of vision impairment among people aged 50 and older. As of 2023, around 94 million individuals over 50 suffer from moderate-to-severe visual impairment due to cataracts. However, only 17% of these patients have access to appropriate surgical treatment, creating strong demand for OVDs used in cataract procedures.

Global public health goals are further boosting the market. In 2021, the World Health Assembly approved a target to increase effective cataract surgery coverage by 30 percentage points by 2030. A 2022 baseline report confirmed the high cost-effectiveness of cataract and refractive surgeries. These goals are increasing the number of cataract surgeries being performed. This directly raises the need for essential surgical tools like OVDs, which are critical to maintaining eye structure during operations and protecting intraocular tissues.

Efforts to improve surgical access in underserved areas are also fueling demand. WHO initiatives are establishing regional tertiary eye care centers in low-resource settings. These centers support cataract treatment programs through surgeon training and outreach services. As surgical infrastructure improves, the volume of cataract surgeries increases. This leads to a higher need for OVDs to ensure safe and efficient procedures. Greater access to quality surgical care supports consistent use of OVDs as standard practice in these settings.

The volume of global cataract surgeries remains high. Over 28 million procedures are performed annually, averaging nearly 75,000 operations each day. More than 90% of these surgeries result in restored useful vision, exceeding the WHO benchmark of 80% achieving 6/18 visual acuity or better. These outcomes are possible due to the regular use of OVDs that help maintain intraocular pressure and surgical precision. Sustained procedure volume and quality outcomes continue to support long-term market growth.

Lastly, rising cases of glaucoma, diabetic retinopathy, and other chronic eye diseases are increasing surgical demand. In many cases, cataract surgery remains the most effective treatment. OVDs play a key role in these complex procedures. Health systems, including the U.S. National Eye Institute, emphasize evidence-based surgical protocols that rely on OVDs for optimal safety and recovery. This growing clinical reliance further contributes to the steady expansion of the global OVD market.

Key Takeaways

- The global OVD market is projected to reach USD 808.5 billion by 2033, growing steadily at a 7.2% CAGR due to surgical advancements and aging demographics.

- Dispersive OVDs led the market in 2023 with a 42% share, appreciated for their broad applicability and superior effectiveness during various ophthalmic surgeries.

- Animal-derived OVDs accounted for over one-third of the market, preferred for their high biocompatibility and favorable outcomes in intraocular procedures.

- Cataract surgery remained the leading application, holding more than 32% market share in 2023, driven by rising incidence among older adults globally.

- The aging population and surge in eye-related disorders significantly drive the demand for OVDs, particularly in cataract management.

- Stringent regulatory requirements for product approvals have slowed market expansion, adding burdensome documentation and extended clinical evaluation periods.

- Continuous innovation in OVD formulations is encouraging greater adoption among ophthalmic surgeons, supporting broader market penetration.

- A growing preference for minimally invasive eye procedures is pushing demand for OVDs tailored to reduce surgical trauma and enhance recovery.

- North America held a dominant position in 2023 with over 37% market share, benefiting from advanced surgical infrastructure and high procedure volume.

- Asia-Pacific is emerging as a high-growth region, supported by rising healthcare investments and increasing public awareness around vision care.

Challenges

- Safety and Clinical Efficacy: One key challenge in the Ophthalmic Viscosurgical Devices sector is the risk of intraocular pressure (IOP) spikes after surgery. This happens when residual cohesive OVDs block the natural outflow of aqueous fluid. The condition can cause temporary IOP elevation. It is especially dangerous for glaucoma patients, where even short-term pressure changes may lead to damage. Additionally, if OVDs are not fully removed, they can cause adverse reactions. These include inflammation, toxic anterior-segment syndrome, or even long-term vision loss. This highlights the need for safe product formulation and complete removal during surgery.

- Training and Technique Sensitivity: Using OVDs effectively requires skilled hands and proper technique. Different types—dispersive versus cohesive—need separate removal strategies. For instance, cohesive agents are easier to remove but may not protect the endothelium well. Dispersive ones protect better but are harder to remove completely. Inexperienced use may lead to complications like endothelial trauma or chamber instability. This raises concerns, particularly in settings where advanced training is not available. Hence, proper surgeon education and clear usage guidelines are crucial for successful outcomes.

- Regulatory Barriers and High Entry Costs: Ophthalmic Viscosurgical Devices are subject to strict safety regulations. Approvals from agencies like the U.S. FDA require extensive clinical trials and long documentation cycles. This process is both time-consuming and expensive. New companies often find it difficult to enter the market due to these high costs. As a result, innovation slows down, especially for small or emerging players. The burden of compliance creates a financial strain, leading to market domination by a few well-established firms.

- Pricing and Cost Pressures: Manufacturers of Ophthalmic Viscosurgical Devices are under growing pressure to keep prices competitive. However, maintaining product quality and innovation adds to their costs. On top of that, global supply chain disruptions can lead to shortages or increased material prices. This creates an imbalance between demand and profitability. Hospitals and surgical centers, particularly in low-income regions, may struggle to afford high-quality products. These pricing issues can limit market expansion and patient access, especially in underserved areas.

Opportunities

- New Product Innovations: There is growing interest in viscoadaptive OVD formulations. These products offer better tissue protection and longer retention time during surgery. For example, ClearVisc includes antioxidants like sorbitol. This additive helps protect sensitive eye tissues from damage during phacoemulsification. Such innovations can reduce the risk of tissue trauma. They also improve patient outcomes and surgeon satisfaction. These advanced formulations are particularly useful in high-risk procedures. Manufacturers focusing on next-generation OVDs can gain a competitive edge. The demand for safer, more effective products is expected to rise with surgical advancements.

- Advanced Surgical Techniques: Modern eye surgeries require highly specialized tools. The “soft-shell” technique, for instance, uses two types of OVDs for better tissue handling. Some products are dyed blue to enhance visibility during complex steps. Others include lidocaine, which helps with pain control. These advanced methods are being widely adopted in cataract and vitreoretinal surgeries. Surgeons prefer tools that provide both safety and precision. OVDs designed for specific surgical styles are becoming more popular. Companies developing such targeted products have a clear opportunity to meet rising clinical needs.

- Rising Clinical Specialization and Partnerships: Eye care is becoming more specialized across many regions. Advanced clinics and eye hospitals are investing in premium OVD systems to improve patient outcomes. These facilities use high-quality tools to offer better care and attract more patients. Strategic partnerships are also playing a key role. For example, Carl Zeiss Meditec has partnered with D.O.R.C., and Centre for Sight has tied up with Laxmi Eye Hospital. These collaborations help companies expand their reach and strengthen their market presence. Such alliances can accelerate innovation and build brand trust among healthcare providers.

- Tech Convergence with Robotics and AI: Technology is changing the way eye surgeries are performed. Robotic-assisted microsurgery is now being used to enhance surgical precision. Artificial intelligence (AI) is also being integrated into surgical systems. When OVDs are used with these advanced platforms, the result is fewer complications and better outcomes. Surgeons can perform more delicate tasks with greater accuracy. This convergence of OVDs, robotics, and AI represents a major growth area. Companies that align their products with these technologies will be well-positioned for future market success.

Conclusion

In conclusion, the global ophthalmic viscosurgical devices market is set for steady growth, supported by rising surgical demand and advancements in eye care. The growing number of cataract procedures, along with improved access to eye surgeries, is increasing the need for safe and effective OVDs. Despite challenges like regulatory hurdles and pricing pressures, the market benefits from strong clinical reliance and ongoing innovation. Advanced techniques, tech integration, and new product developments are creating fresh opportunities. As healthcare systems continue to expand surgical capacity and improve outcomes, OVDs will remain a critical part of standard ophthalmic care. The market outlook remains positive, especially with increasing focus on quality and precision in eye surgery.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)