Table of Contents

Overview

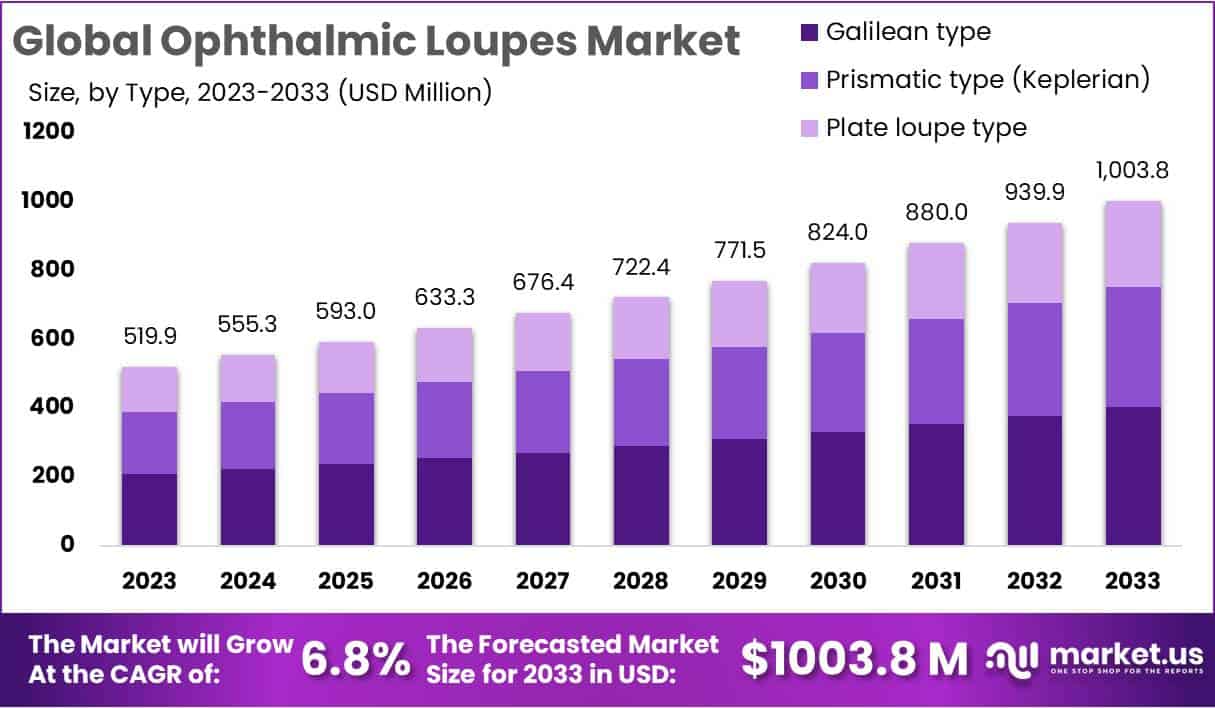

The Ophthalmic Loupes Market is projected to expand significantly, reaching around USD 1,003.8 million by 2033, compared to USD 519.9 million in 2023. This rise represents a Compound Annual Growth Rate (CAGR) of 6.8% from 2024 to 2033. The market’s expansion is largely driven by a growing clinical demand for precise visualization tools in ophthalmic care. Increasing global vision impairment cases are creating strong pressure to scale eye health services. According to the World Health Organization (WHO), at least 2.2 billion people live with vision impairment or blindness, and 1 billion cases remain preventable or unaddressed. This growing backlog is accelerating investments in magnification tools such as loupes to enhance procedural accuracy and efficiency in both clinical and surgical settings.

Cataract remains the leading cause of visual disability and a major contributor to surgical demand. WHO has set a global target to increase the “effective coverage” of cataract surgery by 30% by 2030. However, current baseline data show wide coverage gaps, with median effective surgical coverage remaining around one-third across countries. To achieve the WHO target, significant scaling of cataract programs is required. Consequently, this expansion directly stimulates demand for reliable and ergonomic ophthalmic loupes used during pre-operative evaluations and intra-operative procedures.

Data from major health systems confirm this trend. In England, more than 409,000 cataract surgery admissions were recorded in the year ending 2022, equating to 3,803 procedures per 100,000 people. The National Ophthalmology Database Audit further reports about 608,000 publicly funded cataract operations in England and nearly 16,000 in Wales in the same year. These volumes make cataract surgery the most frequently performed operation within the National Health Service (NHS). As procedural volumes continue to rise, there is a growing need for advanced loupes that offer clarity, durability, and ergonomic comfort to support surgeons during long operating sessions and maintain high-quality visual outcomes.

Demographic, Clinical, and Ergonomic Trends

Population ageing is one of the most significant structural drivers of market growth. According to United Nations (UN) projections, the global population aged 65 years and above will increase from 10% in 2022 to 16% by 2050. Older adults are more prone to cataracts and other eye disorders, leading to a higher demand for eye examinations and surgical interventions. The continuous increase in procedure volumes reinforces the need for precise visualization tools and ergonomically designed loupes that ensure comfort and accuracy for surgeons handling growing caseloads.

Chronic diseases such as diabetes are further accelerating this demand. The World Health Organization (WHO) reports that the global number of diabetes patients rose from 200 million in 1990 to approximately 830 million in 2022. This surge, particularly in low- and middle-income countries, has led to the expansion of diabetic eye disease screening programs. Magnification is essential for detecting subtle retinal changes, enhancing diagnostic accuracy during outpatient consultations. As screening programs expand, ophthalmic loupes are becoming an indispensable part of routine practice for clinicians managing diabetic eye complications.

Ergonomics and workforce well-being are also major influencing factors. Studies by the Centers for Disease Control and Prevention (CDC) and NIOSH reveal that one-third to two-thirds of ophthalmologists experience neck-related musculoskeletal symptoms. NIOSH has recommended the use of equipment such as loupes with appropriate declination angles to reduce strain and prevent injury. Hospitals adopting ergonomic equipment to improve surgeon comfort and retention rates are increasingly investing in advanced loupe designs.

Regional data also validate these patterns. In Australia, the Australian Institute of Health and Welfare recorded 8,008 cataract hospitalisations among Aboriginal and Torres Strait Islander peoples between 2021 and 2023, representing 4,467 per 1,000,000 population. These volumes highlight ongoing service gaps and point to continued growth in ophthalmic service capacity. Similarly, the CDC Vision and Eye Health Surveillance System in the United States reported over 7 million Americans living with vision loss or blindness in 2017. Collectively, these demographic, clinical, and ergonomic trends ensure sustained global demand for efficient, ergonomic, and high-quality ophthalmic loupes over the next decade.

Key Takeaways

- The Ophthalmic Loupes Market is projected to reach USD 1003.8 million by 2033, advancing steadily at a 6.8% CAGR from 2024 to 2033.

- Galilean Type loupes dominated the market with over 40.1% share in 2023, appreciated for their ergonomic design, simplicity, and operational ease.

- The Through-The-Lens (TTL) design accounted for over 60.5% market share in 2023, offering superior usability and a direct, unobstructed line of sight.

- Hospitals led the end-use segment with a 42.1% share in 2023, emphasizing their crucial role in diverse medical and ophthalmic procedures.

- North America captured 31.6% market share, equivalent to USD 164.2 million in 2023, driven by advanced healthcare infrastructure and technological innovation.

- LED illumination is increasingly adopted for enhanced visual quality, while lightweight, wireless, and portable designs improve comfort and procedural efficiency.

- High initial costs and limited awareness among healthcare professionals remain primary challenges to the widespread adoption of Ophthalmic Loupes globally.

- Expanding opportunities exist in emerging markets through strategic collaborations, product customization, and integration with advanced digital and imaging technologies.

Regional Analysis

In 2023, North America dominated the global Ophthalmic Loupes market with a strong share of 31.6% and a market value of USD 164.2 million. The region’s leadership is supported by advanced healthcare infrastructure and a large network of ophthalmic professionals. Continuous innovation and precision in medical practices have driven the demand for optical devices. The presence of top-tier medical institutions and consistent investment in healthcare technology has further strengthened the region’s position in the global Ophthalmic Loupes market.

The aging population across North America has been a key driver for market growth. The rising prevalence of age-related eye disorders and vision impairments has increased the need for high-quality optical tools. Ophthalmic Loupes play an essential role in improving visual accuracy during eye examinations and surgical procedures. The growing awareness of eye health and early diagnosis has further supported demand. Additionally, an expanding base of ophthalmic professionals is contributing to the growing utilization of advanced Loupes in clinical applications.

Technological advancement remains a core factor behind North America’s continued dominance. The integration of innovative features such as augmented reality and adjustable magnification has boosted market competitiveness. Strategic partnerships among key manufacturers, research institutions, and healthcare providers have accelerated product development. Moreover, a well-regulated medical device framework ensures product safety and compliance. This strong regulatory environment has built trust among healthcare professionals and end-users, fostering widespread adoption of Ophthalmic Loupes across hospitals, clinics, and specialized surgical centers.

Segmentation Analysis

In 2023, the Galilean Type segment dominated the ophthalmic loupes market with a strong 40.1% share. This type is preferred for its ergonomic design, simplicity, and user-friendly nature. Its lightweight structure enhances comfort during long procedures, making it ideal for professionals. The Prismatic or Keplerian Type also gained significant traction due to its advanced prism technology, offering higher magnification and a broader field of view. Meanwhile, the Plate Loupe Type attracted users seeking portability, combining compactness with strong optical performance.

The Through-The-Lens (TTL) design led the ophthalmic loupes market in 2023, capturing over 60.5% of the share. Its seamless integration and direct viewing capability made it the top choice for ophthalmic professionals. The ergonomic benefits and precise alignment offered by TTL loupes improved user comfort and accuracy. In contrast, the Flip-Up design maintained a notable market presence but lagged behind TTL in preference. However, its adjustable flexibility continues to appeal to practitioners who value versatility in clinical settings.

The end-use analysis revealed that hospitals held the largest share, exceeding 42.1% in 2023. Their adoption underscores the importance of ophthalmic loupes in enhancing surgical precision and diagnostic efficiency. Ambulatory Surgical Centers also showed significant growth, driven by the demand for advanced visualization tools in outpatient procedures. Additionally, other facilities such as specialty clinics and eye care centers contributed to market expansion. Their increasing adoption demonstrates the widening acceptance and importance of ophthalmic loupes across diverse medical applications and healthcare environments.

Type

- Galilean Type

- Prismatic Type (Keplerian)

- Plate Loupe Type

Design

- Through-The-Lens (TTL)

- Flip Up

End-Use

- Hospitals

- Ambulatory Surgical Centers

- Others

Key Players Analysis

The Ophthalmic Loupes Market is characterized by strong competition among leading manufacturers striving for innovation and quality. SurgiTel has established itself as a prominent player by delivering cutting-edge loupes that enhance surgical precision. Its ergonomic designs cater to ophthalmic professionals seeking both comfort and accuracy. Similarly, SHEERVISION focuses on advanced optical performance, offering high-quality loupes known for clarity and user comfort. The company’s emphasis on visual excellence and ease of use meets the rising demand for precision-driven tools in ophthalmic procedures.

Keeler continues to strengthen its position in the global market through durable and reliable ophthalmic loupes. The brand’s long-standing reputation for performance instills confidence among practitioners, making it a preferred choice for consistency in clinical settings. ZEISS, a global leader in optics, adds technological sophistication to the market. Its precision-engineered loupes integrate advanced optical systems that enhance magnification accuracy. ZEISS’s expertise in visual technology supports its role as a frontrunner in improving the user’s diagnostic and surgical experience.

In addition to these major players, companies such as Rudolf Riester GmbH, NEITZ INSTRUMENTS CO. LTD., and Orascoptic contribute significantly to product diversity and market expansion. Their focus on design efficiency and visual performance drives competitive differentiation. Univet S.r.l. and Ocutech Inc. also emphasize innovation and comfort, addressing the evolving needs of ophthalmologists. Collectively, these companies foster a highly competitive ecosystem that encourages continuous product enhancement and technological improvement.

Overall, the presence of these key players fuels advancements in optical precision and ergonomic design within the Ophthalmic Loupes Market. Their combined efforts support improved user experiences and enhanced procedural accuracy. As competition intensifies, product innovation and differentiation are expected to remain critical growth strategies. The integration of advanced materials, improved magnification systems, and lightweight designs will likely shape the future landscape of the ophthalmic loupes industry, benefiting both manufacturers and end-users.

Market Key Players

- SurgiTel

- SHEERVISION

- Keeler

- ZEISS

- Rudolf Riester GmbH

- NEITZ INSTRUMENTS CO. LTD.

- Orascoptic

- Univet S.r.l.

- Ocutech Inc.

Challenges

1. Ergonomics and Surgeon Discomfort

Surgeons often experience neck and upper-back strain when using heavy or poorly fitted loupes. Low declination angles increase muscle tension and discomfort during long procedures. Studies have shown that loupe use is linked to higher neck loads and musculoskeletal symptoms among surgeons. In ophthalmology, many users report that discomfort and poor ergonomics reduce the frequency of use. Long surgeries amplify these effects, causing fatigue and reduced concentration. Therefore, improving ergonomic design is critical to increasing adoption and minimizing surgeon discomfort in clinical practice.

2. Optical Constraints (Field, Depth, and Working Distance)

Optical performance is another major concern for ophthalmic surgeons. Many users report a narrow field of view and limited depth of field while using loupes. These restrictions often slow surgical procedures and require frequent repositioning. Oculoplastic and other eye subspecialties depend on precise visualization. Any reduction in peripheral vision or working distance can negatively affect accuracy. Such limitations discourage routine use and reduce the perceived value of loupes. Enhanced optical quality and wider visual fields are essential to meet ophthalmic surgery demands and improve workflow efficiency.

3. Fit and Customization Complexity

Achieving a proper fit is often difficult due to variations in interpupillary distance, working distance, and declination angle. Poorly fitted loupes can cause visual fatigue, posture problems, and eye strain. Many residency programs now emphasize ergonomic training to address these issues. However, standard models often fail to accommodate individual differences. This lack of personalization reduces comfort and discourages long-term use. Custom-fitted solutions could enhance usability and minimize health risks. Simplifying the fitting process is key to ensuring both comfort and accuracy during surgery.

4. Workflow and Adoption Barriers

Despite the benefits of magnification, many ophthalmic surgeons rarely use loupes in daily practice. Surveys show that only about one-third of surgeons use them regularly. Ownership does not always lead to consistent use due to discomfort and optical limitations. Some users also find the setup time inconvenient in fast-paced surgical settings. Others rely on microscopes for higher magnification. These workflow challenges reduce adoption across the specialty. To increase regular use, manufacturers must focus on comfort, optical quality, and ease of integration into existing surgical workflows.

5. Infection Control and Reprocessing

Ophthalmic loupes are classified as reusable surgical instruments in the European Union. They must endure repeated cleaning and sterilization cycles under EU MDR regulations. However, maintaining optical coatings, lenses, and hinges during reprocessing is a major challenge. Improper sterilization can degrade materials and shorten product life. Hospitals demand equipment that is both durable and compliant with hygiene standards. Manufacturers face growing pressure to develop sterilization-resistant coatings and robust mechanical parts. Ensuring easy and safe reprocessing will be vital for regulatory compliance and product longevity.

6. Regulatory Considerations

In the United States, ophthalmic and surgical loupes are regulated under FDA product code FSP. They are categorized as manual surgical instruments for general use. Although regulatory requirements are less stringent than for implants, they still involve strict quality systems and labeling standards. Compliance adds cost and time to product development. Manufacturers must also follow documentation and post-market surveillance rules. Understanding and meeting these regulations is essential to ensure market access and maintain trust among healthcare professionals.

Opportunities

1. Ergonomic Innovation (Neck-Saving Designs)

Ergonomic loupes with high-declination angles and prismatic optics reduce strain on the neck and shoulders. These designs improve comfort without affecting task precision. There is strong potential for product lines that focus on “ergonomics-first” features. Lightweight materials such as titanium or carbon composites enhance comfort during long procedures. Balanced frames and adjustable fittings address user pain points like posture and fatigue. Offering personalized fitting options can further strengthen appeal. Such ergonomic innovations make daily use safer and more comfortable for ophthalmologists and surgical teams.

2. Optical Performance Upgrades for Eye Surgery

Ophthalmic professionals need loupes with a wider field of view and deeper focus for short-to-medium working distances. Custom optics designed for oculoplastics, strabismus, and retina work can greatly enhance performance. These specialized optics already show strong adoption among eye surgeons. Premium models targeting these segments can gain fast acceptance. By improving clarity, precision, and visual comfort, such loupes directly address critical surgical demands. The opportunity lies in creating differentiated, task-specific optical systems that elevate the standard of care in ophthalmic surgery.

3. Integrated Illumination and Power Management

Shadow-free, coaxial illumination remains essential in ophthalmic practice. Integrating advanced LED optics and efficient battery systems can significantly improve usability. Longer run times, reduced heat generation, and lightweight power packs enhance comfort during extended procedures. These improvements also simplify workflows in busy operating environments. Offering consistent lighting with minimal maintenance needs helps users maintain focus on precision tasks. Loupes featuring modern illumination and power management systems can establish a clear competitive edge in both performance and convenience.

4. Digital and Training Use-Cases

The rising global volume of eye-care procedures, especially cataract surgeries, is increasing demand for magnification tools. Loupes play an important role in pre-operative, clinic, and teaching settings. Specialized loupe solutions for medical training centers and ambulatory facilities offer strong growth potential. Digital add-ons such as posture feedback and usage tracking can enhance training outcomes. By helping users improve ergonomics and technique, these tools reduce musculoskeletal strain and boost long-term satisfaction. Such innovations align well with modern education and institutional wellness programs.

5. Customization and Service Models

Quick, accurate customization is becoming a key differentiator in ophthalmic loupes. Adjustable parameters such as interpupillary distance, working distance, and angle of declination improve fit and comfort. Clinics value vendors that provide precise fitting support and reduce trial times. Personalized fitting services can also improve long-term user satisfaction. Offering after-sales support and easy adjustment options builds loyalty among clinical users. These service-driven approaches ensure users get the best ergonomic and optical performance, supporting both comfort and productivity in daily operations.

6. Compliance and Quality Positioning

Regulatory compliance strengthens brand credibility in the medical device market. Mapping product design to FDA FSP and EU MDR standards ensures faster hospital approvals. Validated cleaning and sterilization instructions also simplify infection-control procedures. These compliance features support hospitals and surgical centers in procurement decisions. Positioning products as safe, reliable, and compliant encourages trust and premium pricing. Manufacturers that invest in quality documentation and transparent testing can gain an advantage in competitive tenders and institutional partnerships.

Conclusion

The Ophthalmic Loupes Market is expected to grow steadily due to increasing eye care needs and advancements in optical technology. Rising cases of vision impairment and the growing elderly population are driving demand for precise and comfortable visualization tools. Hospitals and clinics are adopting advanced loupes to improve surgical accuracy and reduce strain for ophthalmologists. Continuous innovation in ergonomic design, illumination, and customization is making loupes more efficient and user-friendly. With expanding awareness, strong regulatory support, and increasing investment in healthcare infrastructure, the market is set for long-term growth, creating new opportunities for manufacturers and healthcare providers worldwide.

View More

Ophthalmic Knives Market | Ophthalmic Devices Market | Ophthalmic Drugs Market | Ophthalmic Lasers Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)