Table of Contents

Overview

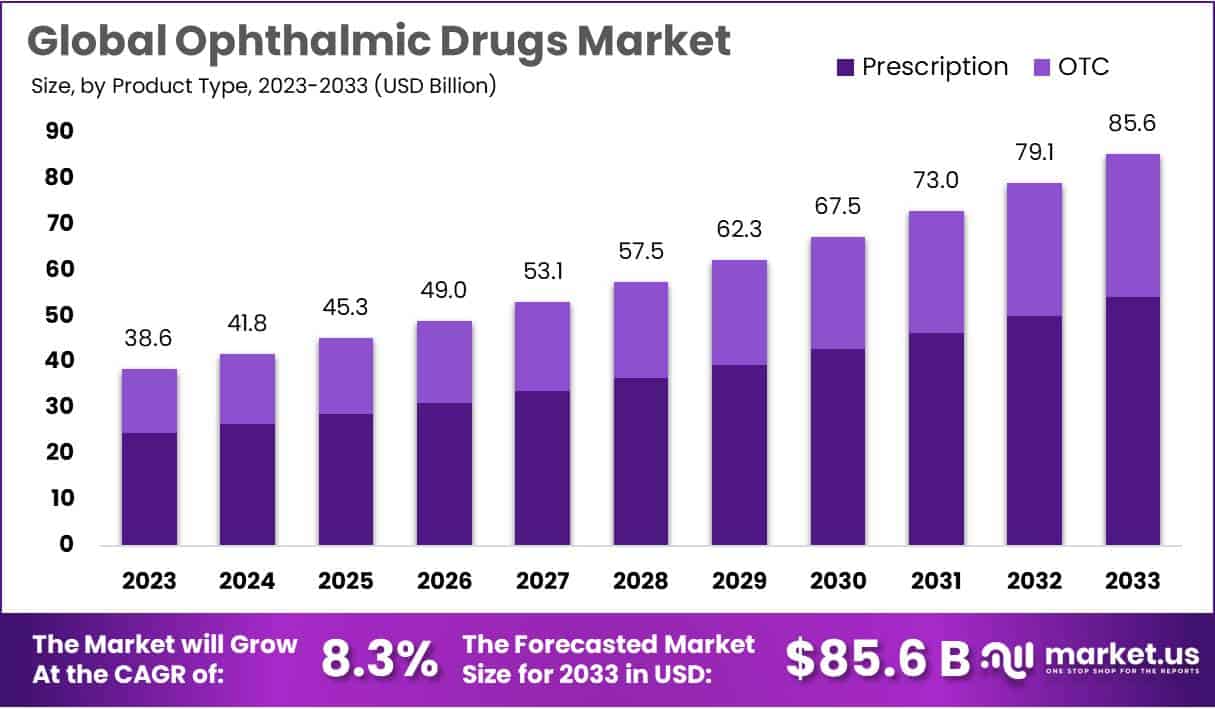

New York, NY – Oct 09, 2025 – The Global Ophthalmic Drugs Market size is expected to be worth around USD 85.6 Billion by 2033, from USD 41.8 Billion in 2024, growing at a CAGR of 8.3% during the forecast period from 2025 to 2033.

The global ophthalmic drugs market is experiencing significant growth, driven by the increasing prevalence of eye-related disorders and the rising geriatric population. The market is projected to expand at a steady rate, supported by advancements in drug delivery systems and the growing demand for minimally invasive treatments.

Ophthalmic drugs, which include anti-inflammatory, anti-infective, anti-glaucoma, and anti-allergy formulations, are being increasingly adopted for the management of glaucoma, dry eye, retinal disorders, and infections. The demand is further strengthened by the surge in cases of age-related macular degeneration and diabetic retinopathy, conditions strongly correlated with lifestyle changes and aging demographics.

Pharmaceutical companies are investing heavily in research and development to introduce novel therapeutics with improved efficacy and safety profiles. Innovative drug delivery mechanisms such as sustained-release implants, gels, and nano-formulations are reshaping treatment outcomes and enhancing patient compliance. Additionally, regulatory approvals of biologics and biosimilars are creating new avenues for growth in the ophthalmic segment.

North America currently dominates the market due to advanced healthcare infrastructure and high awareness levels, while Asia-Pacific is anticipated to register the fastest growth owing to large patient pools and rising healthcare expenditure.

The outlook for the ophthalmic drugs market remains positive, with strong opportunities for innovation and strategic collaborations. The sector is positioned for robust expansion as healthcare providers and manufacturers address the increasing global burden of eye disorders.

Key Takeaways

- Market Projection: The ophthalmic drugs market is projected to reach USD 85.6 billion by 2033, expanding at a CAGR of 8.3% between 2024 and 2033.

- Product Type Leadership: Prescription drugs accounted for 63.5% of the market in 2023, supported by the growing prevalence of age-related macular degeneration (AMD) and diabetic retinopathy.

- Drug Class Leadership: Anti-glaucoma drugs held a 31.9% share in 2023, reflecting the increasing incidence of glaucoma cases worldwide.

- Dosage Form Leadership: Eye drops represented the largest segment with a 41.8% market share in 2023, attributed to over-the-counter (OTC) availability, improved patient compliance, and frequent new product launches.

- Route of Administration: Topical administration remained dominant with 57% of the market in 2023, favored for its ease of self-administration, non-invasiveness, and high patient adherence.

- Distribution Channel: Hospital pharmacies led the market with a 60.4% share in 2023, owing to the rising prevalence of chronic eye disorders, while online pharmacies are expected to register the fastest growth during the forecast period.

- Regional Outlook: North America captured 44% of the global market in 2023, driven by the increasing burden of eye diseases, ongoing technological advancements, and a growing elderly population.

Regional Analysis

In 2023, North America accounted for over 44% of the global ophthalmic drugs market, representing a market value of USD 16.9 billion. The region’s growth is being driven by the rising prevalence of eye-related disorders, advancements in ophthalmology technologies, and the expanding elderly population. Further contributing to market expansion are robust R&D investments, the strong presence of leading market players, and an increasing number of new product launches and regulatory approvals for ophthalmic drugs and devices.

The Asia-Pacific region, on the other hand, is expected to register the fastest growth over the forecast period. The demand for ophthalmic medications in the region is projected to rise due to the growing incidence of ocular diseases and increasing awareness among patients regarding therapeutic efficacy. Moreover, regional pharmaceutical companies are actively engaging in strategic initiatives to develop and commercialize innovative treatment solutions, further stimulating market growth across Asia-Pacific.

Frequently Asked Questions on Ophthalmic Drugs

- What are ophthalmic drugs?

Ophthalmic drugs are specialized medications formulated to treat various eye disorders such as glaucoma, dry eye, infections, and macular degeneration. They are administered through eye drops, ointments, injections, or implants to deliver targeted therapeutic effects. - What conditions are treated with ophthalmic drugs?

These drugs are widely used to manage conditions including glaucoma, conjunctivitis, age-related macular degeneration, dry eye syndrome, diabetic retinopathy, and ocular infections. By targeting specific pathways, ophthalmic drugs help preserve vision and improve patient quality of life. - What are the major types of ophthalmic drugs?

The major categories include anti-glaucoma agents, anti-inflammatory drugs, anti-infectives, anti-allergy medications, and biologics. Each class of ophthalmic drugs addresses distinct therapeutic needs, supporting effective disease management across a wide spectrum of ophthalmic conditions. - How are ophthalmic drugs administered?

Ophthalmic drugs are administered topically, orally, or via intraocular injections and implants. Topical administration, especially through eye drops, is the most common due to convenience, high patient compliance, and the ability to directly target the eye. - Which product type dominates the ophthalmic drugs market?

In 2023, prescription drugs held the largest share at 63.5%, primarily due to the high prevalence of chronic eye conditions such as age-related macular degeneration and diabetic retinopathy, which require continuous medical intervention and advanced therapeutic solutions. - What drug class leads the market share?

Anti-glaucoma drugs dominated the segment in 2023 with a 31.9% share, reflecting the rising global incidence of glaucoma. Early detection programs and improved therapeutic solutions are also contributing to the growth of this drug class. - Which dosage form is most widely used?

Eye drops accounted for 41.8% of the market in 2023, due to over-the-counter availability, better patient compliance, and frequent product launches. They remain the preferred dosage form for managing both chronic and acute ophthalmic conditions. - Which region holds the largest share of the ophthalmic drugs market?

North America led the global market in 2023, capturing 44% share with a value of USD 16.9 billion, supported by technological innovations, high awareness, and the presence of leading pharmaceutical players in the region.

Conclusion

The global ophthalmic drugs market is poised for sustained growth, driven by the rising prevalence of eye disorders, an expanding elderly population, and continuous innovations in drug delivery systems. With anti-glaucoma and prescription drugs leading market share, and eye drops remaining the most widely used dosage form, the industry reflects strong therapeutic adoption.

North America currently dominates due to advanced infrastructure and awareness, while Asia-Pacific is expected to witness the fastest growth. Increasing R&D investments, regulatory approvals, and strategic collaborations are expected to further strengthen the market outlook, positioning the sector for robust expansion through 2033.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)