Table of Contents

Overview

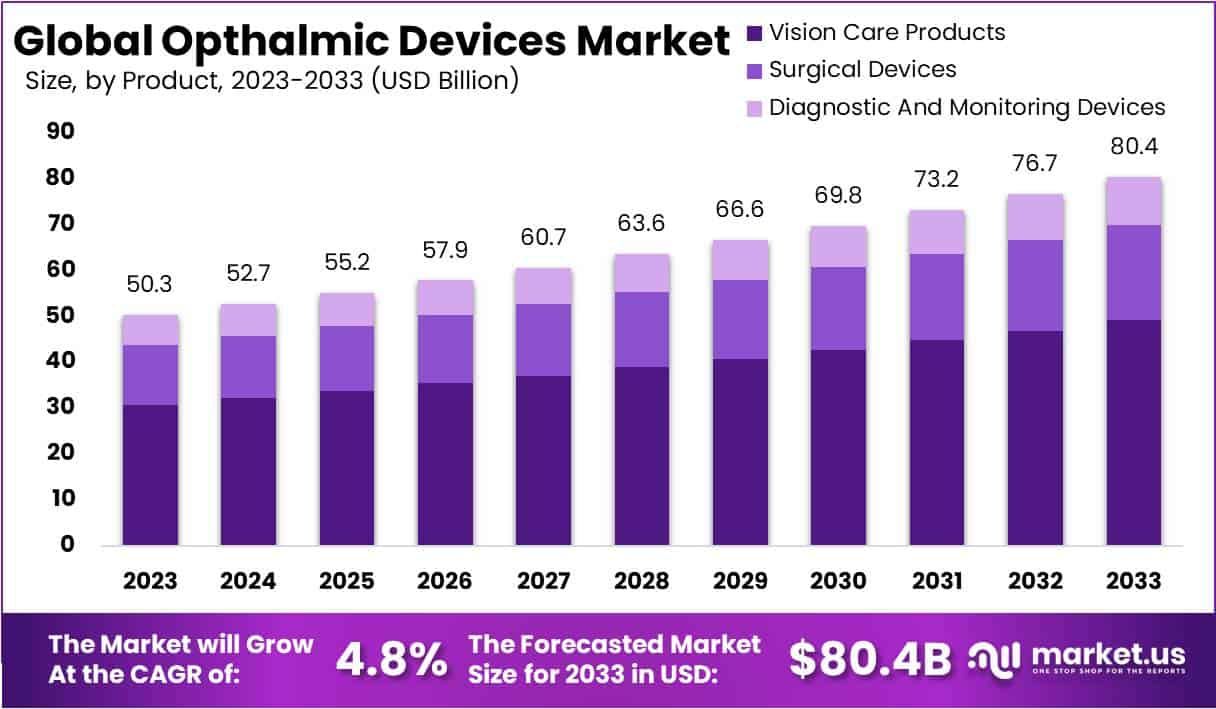

The Global Ophthalmic Devices Market is projected to reach USD 80.4 billion by 2033, rising from USD 50.3 billion in 2023. This growth reflects a compound annual growth rate (CAGR) of 4.8% during 2023–2032. Expansion is strongly supported by the increasing burden of eye disorders, demographic shifts, and continuous technological innovation. With visual impairment affecting more than 2.2 billion people worldwide, demand for effective diagnostic, surgical, and corrective devices is intensifying at a consistent pace.

Aging demographics are a major contributor to this demand. Elderly populations are at high risk for conditions such as cataracts, glaucoma, and age-related macular degeneration. This has fueled steady adoption of surgical instruments, intraocular lenses, and advanced diagnostic imaging systems. With global life expectancy rising, the demand for ophthalmic interventions will continue to expand across developed and developing economies alike.

Technological advancement has also been a strong catalyst for growth. Minimally invasive surgical instruments, Optical Coherence Tomography (OCT), and robotic-assisted surgery have transformed treatment approaches. Smart lenses and intraocular implants with enhanced functionalities are gaining traction. These innovations improve precision, shorten recovery times, and boost overall treatment efficiency. The emphasis on better patient outcomes has encouraged hospitals and specialty clinics to accelerate the adoption of modern ophthalmic solutions.

Growing awareness of eye health further strengthens this outlook. Public health campaigns and improved access to care have increased routine screenings and early diagnosis of conditions like glaucoma and diabetic retinopathy. Early detection significantly reduces the risk of permanent impairment. Consequently, diagnostic ophthalmic devices are experiencing wider usage, particularly in urban regions where eye health awareness is stronger. This trend is expected to continue as more governments invest in preventive healthcare strategies.

Market Expansion Opportunities

Healthcare infrastructure development in emerging markets is a key enabler of ophthalmic device adoption. Governments in Asia-Pacific, Latin America, and the Middle East are expanding hospitals and specialty clinics. Increased investments in eye care centers, coupled with international partnerships, have improved accessibility to advanced ophthalmic treatments. This infrastructure expansion provides global manufacturers with new opportunities to penetrate high-growth markets and strengthen their revenue base.

Demand for corrective lenses and refractive surgeries is also on the rise. The prevalence of myopia and hyperopia is increasing due to digital screen exposure and lifestyle changes. Younger populations, in particular, are driving demand for contact lenses and surgical equipment. Higher disposable incomes and a preference for advanced corrective solutions support this growth trend. The corrective lens segment is therefore expected to remain a stable contributor to overall market expansion.

Supportive reimbursement policies in developed regions are another positive factor. Coverage for cataract surgeries and glaucoma treatments has improved patient access to advanced devices. Reimbursement frameworks reduce out-of-pocket costs, enabling broader acceptance of innovative surgical and diagnostic technologies. This financial support creates a favorable environment for manufacturers to introduce advanced solutions and improve adoption rates in mature markets.

Finally, rising investment in research and development is enhancing competitiveness. Companies are introducing cost-effective and patient-friendly devices through innovation and strategic partnerships. Collaborations with research institutes and universities have strengthened product pipelines and accelerated new product approvals. This focus on innovation not only boosts market penetration but also ensures long-term sustainability in a rapidly evolving ophthalmic devices sector.

Key Takeaways

- The ophthalmic devices market is projected to reach USD 80.4 billion by 2033, expanding steadily at a 4.8% CAGR from 2023’s USD 50.3 billion.

- Market growth is primarily supported by the aging global population, favorable government initiatives, and pandemic-driven awareness, which increased demand for advanced ophthalmic solutions worldwide.

- Limited healthcare spending in emerging economies, high device costs, and restricted accessibility continue to act as significant restraints on broader market expansion.

- Rising numbers of clinics, increasing patient awareness, and growing ambulatory centers are creating substantial growth opportunities within the global ophthalmic devices industry.

- Market trends are shaped by technological innovation, with advanced tools and micro-invasive glaucoma implants significantly fueling demand for next-generation ophthalmic devices.

- Vision care products dominated with 61.2% market share in 2023, largely driven by persistent global demand for corrective eyeglasses and contact lenses.

- The cataract treatment segment held the largest application share of 48.9% in 2023, with projections indicating robust future expansion in surgical demand.

- Hospitals and specialized eye clinics represented 80.2% of market share in 2023, strengthened by advanced technology adoption and an increasing number of clinical establishments.

- Core product categories—Vision Care, Surgical Devices, and Diagnostics & Monitoring tools—remain critical to addressing diverse ophthalmic requirements across global healthcare systems.

- North America led with a 46.2% share (USD 23.2 billion in 2023), while Asia-Pacific emerged as a key growth hub.

Regional Analysis

In 2023, North America secured a dominant position in the ophthalmology devices market, holding over 46.2% share with a market value of USD 23.2 billion. The high prevalence of diabetic retinopathy, vision loss, and blindness has been the key factor behind this dominance. The region benefits from advanced healthcare infrastructure and strong adoption of innovative medical technologies. These factors, combined with the rising demand for improved eye care solutions, have strengthened the role of North America as the market leader.

The sector in North America is primarily driven by an aging population and an increasing prevalence of chronic eye conditions. Poor lifestyle habits and high stress levels are further contributing to cases of diabetic retinopathy and related disorders. Additionally, favorable reimbursement models are being adopted for ophthalmologic therapies. Alongside this, strict regulatory measures have been implemented to ensure patient safety and treatment efficacy. Together, these factors are creating a stable foundation for sustained demand in ophthalmic devices.

The Asia-Pacific region is forecasted to experience significant growth during the projection period. This expansion is attributed to increased outsourcing activities by global leaders such as Alcon, Inc. The rising awareness about modern corrective eye procedures is also supporting demand, especially in emerging economies like China and India. Furthermore, improving healthcare facilities and expanding access to ophthalmology treatments are strengthening the regional market outlook. These conditions are expected to position Asia-Pacific as one of the fastest-growing markets for ophthalmology devices in the coming years.

Segmentation Analysis

In 2023, the Vision Care Products segment held the largest market share of 61.2%. This category includes eyeglasses, contact lenses, and related products for vision correction and improvement. A large population depends on these products, which strengthens demand. Rising cases of eye disorders, higher awareness of eye health, and rapid technological advances are expected to support further growth. Vision care is therefore anticipated to maintain its dominance in the ophthalmic devices market over the forecast period.

The Cataract application segment led the market in 2023, capturing 48.9% of the share. This growth is linked to the widespread use of ophthalmic tools in cataract surgeries, which remain one of the most common procedures globally. Over the forecast period, this trend is expected to continue with significant expansion. Meanwhile, refractor disorders are projected to grow fastest. This is supported by strong adoption of phoropters and retinoscopes, as companies innovate diagnostic and treatment solutions for rising patient needs.

Hospitals and eye clinics dominated the end-user segment in 2023 with over 80.2% share. This dominance results from the cost-effective and high-quality care these facilities deliver, coupled with rising adoption of advanced ophthalmic technologies. Consolidation through mergers and acquisitions has further boosted demand for new device installations. Additionally, many clinics are expanding into diagnostic services, increasing ophthalmic device usage. Significant growth is also projected in academic and research laboratories, supported by funding and investment in ophthalmic care research during the forecast period.

Key Players Analysis

Essilor and Alcon together account for over 30% of revenue in the global ophthalmic device market. Their dominance reflects the fragmented nature of the industry. This market structure gives both companies a major advantage in terms of size and share. They serve a wide base of hospitals, clinics, and eye care professionals. Their leadership position is further supported by diversified product portfolios. These include corrective, surgical, diagnostic, and therapeutic instruments, ensuring relevance across multiple segments of ophthalmic care.

Both Essilor and Alcon provide a broad range of ophthalmic devices to address varying medical needs. Their portfolios include diagnostic instruments, therapeutic solutions, surgical systems, and corrective tools. This product depth helps them meet the rising demand for precision and patient-focused care. Beyond hardware, they provide professional training and educational services. This strategic move strengthens customer loyalty and creates long-term relationships. By integrating products with learning support, these companies offer complete solutions that stand out in a competitive market.

The competitive strength of Essilor and Alcon is reinforced by continued investment in technology. Innovation is central to their strategies, ensuring advancement in vision correction and surgical performance. Smart diagnostic tools and advanced surgical platforms are at the core of their offerings. Both companies emphasize R&D to remain at the forefront of ophthalmic device innovation. This forward-looking approach not only improves clinical outcomes but also enhances user experience for eye care specialists. Their commitment to innovation secures sustained market leadership.

Market Key Players

- Alcon Vision LLC

- Essilor International S.A

- Johnson & Johnson Vision Care

- Carl Zeiss Meditec AG

- Bausch & Lomb Incorporated

- Essilor International S.A

- Ziemer Ophthalmic System Ltd

- Nidek Co. Ltd

- TOPCON Corporation

- Haag-Streit Group

- Hoya Corporation

- OPHTEC BV

- ClearLab

- Other key Players.

FAQ

1. What are ophthalmic devices?

Ophthalmic devices are medical tools used to diagnose, monitor, and treat eye conditions. These devices include instruments for vision testing, imaging systems, surgical equipment, and corrective products like contact lenses. They play an important role in eye care by helping doctors detect diseases early, perform precise surgeries, and improve vision quality. The use of such devices is essential in addressing common eye problems, restoring sight, and preventing blindness. They support both clinical and surgical practices worldwide.

2. What are the main categories of ophthalmic devices?

Ophthalmic devices fall into three main categories. Diagnostic and monitoring devices include tonometers, optical coherence tomography, and fundus cameras, which help in detecting and tracking eye diseases. Surgical devices include phacoemulsification systems, vitrectomy devices, and advanced laser systems, which improve surgical outcomes. Vision care products such as eyeglasses, contact lenses, and intraocular lenses are widely used to correct refractive errors. Each category serves a specific purpose in eye health. Together, they ensure better diagnosis, treatment, and vision correction for patients.

3. What eye conditions are treated using ophthalmic devices?

Ophthalmic devices are used to treat a wide range of eye conditions. They play an important role in managing cataracts, glaucoma, and refractive errors such as myopia, hyperopia, and astigmatism. Devices are also used to address diabetic retinopathy, macular degeneration, and dry eye syndrome. These conditions affect millions of people worldwide and often worsen with age. Using advanced devices, ophthalmologists can detect problems earlier, offer better treatment, and improve patient outcomes. This ensures clearer vision, reduces complications, and helps prevent vision loss.

4. How have technological advancements influenced ophthalmic devices?

Technological advancements have transformed ophthalmic devices. Modern tools use digital imaging, femtosecond lasers, and artificial intelligence for improved diagnosis and treatment. These innovations allow faster, more accurate detection of eye disorders and safer surgical procedures. For example, AI-supported imaging helps detect glaucoma and diabetic retinopathy at early stages. New intraocular lenses with advanced materials also improve vision correction after cataract surgery. Overall, technology has made eye care more precise, effective, and accessible, creating better outcomes for patients and doctors worldwide.

5. Are ophthalmic devices regulated?

Yes, ophthalmic devices are carefully regulated to ensure safety and effectiveness. In the United States, the Food and Drug Administration (FDA) evaluates these devices before approval. In Europe, devices must meet CE Marking standards to enter the market. Similar regulations exist across Asia and other regions. Manufacturers must conduct clinical trials, provide safety data, and meet strict quality standards. These rules help protect patients from risks and ensure that devices perform as expected. Regulation also encourages trust among doctors and patients.

6. What is the size of the global ophthalmic devices market?

The Global Ophthalmic Devices Market size is expected to be worth around USD 80.4 Billion by 2033 from USD 50.3 Billion in 2023, growing at a CAGR of 4.8% during the forecast period from 2023 to 2032. Growth is driven by rising cases of eye diseases and increasing use of advanced technologies. The market expansion is also supported by greater access to healthcare in developing regions. Overall, the demand for both diagnostic and surgical devices is growing, ensuring sustained opportunities.

7. What factors are driving market growth?

Several factors drive the growth of the ophthalmic devices market. Aging populations worldwide are leading to higher cases of cataracts, glaucoma, and macular degeneration. Demand for minimally invasive surgical techniques and vision correction products is increasing. Technological advances, including AI-based imaging and laser-assisted surgeries, are boosting adoption. Emerging economies are investing in healthcare infrastructure, creating opportunities for manufacturers. Rising awareness about eye health also supports growth. These factors together are ensuring a steady rise in demand for ophthalmic devices across regions.

8. Which regions dominate the ophthalmic devices market?

North America dominates the global ophthalmic devices market due to advanced healthcare infrastructure and early adoption of premium technologies. Europe holds a strong share, supported by government initiatives for eye care and growing awareness. Asia-Pacific is the fastest-growing region because of a large patient base, rising healthcare spending, and increasing access to ophthalmology services. Latin America and the Middle East also show potential due to expanding healthcare systems. Regional growth patterns are shaped by demographics, technology access, and regulatory support.

9. Who are the key players in the ophthalmic devices market?

The ophthalmic devices market is highly competitive with several global leaders. Key companies include Alcon Vision LLC, Essilor International S.A, Johnson & Johnson Vision Care, Carl Zeiss Meditec AG, Bausch & Lomb Incorporated, Essilor International S.A, Ziemer Ophthalmic System Ltd, Nidek Co. Ltd, TOPCON Corporation, Haag-Streit Group, Hoya Corporation, OPHTEC BV, ClearLab, and Other key Players. These companies focus on innovation, product launches, and strategic partnerships to maintain their market positions. They also invest heavily in research and development to introduce advanced technologies. Their presence spans across diagnostic tools, surgical equipment, and vision correction products. Together, they shape industry trends and drive growth in the ophthalmic devices sector.

10. What are the current trends in the ophthalmic devices market?

The ophthalmic devices market is witnessing several important trends. Artificial intelligence and machine learning are being integrated into diagnostic imaging, improving disease detection. Premium intraocular lenses are gaining popularity due to better vision outcomes. Tele-ophthalmology is expanding access to remote eye care services. Refractive surgeries such as LASIK and SMILE are seeing growing demand. Wearable monitoring devices for eye health are also emerging. These trends reflect the shift toward technology-driven, patient-centered solutions that improve accessibility, outcomes, and overall quality of eye care.

11. What challenges are faced by the market?

The ophthalmic devices market faces a few challenges despite its growth. High costs of advanced surgical and diagnostic equipment limit access, especially in low-income regions. Strict regulatory requirements make new product approvals lengthy and expensive. There is also a shortage of trained ophthalmologists in many developing countries. Unequal access to advanced technologies continues to widen gaps in care between regions. These challenges may slow adoption rates, but increasing awareness and government initiatives are expected to reduce barriers and support long-term growth.

Conclusion

The global ophthalmic devices market is set for steady growth, supported by rising cases of eye disorders, an aging population, and rapid advancements in technology. The demand for corrective lenses, surgical instruments, and diagnostic systems is increasing as awareness of eye health spreads and healthcare access improves. While high device costs and limited resources in some regions remain challenges, opportunities are expanding in emerging markets with improving infrastructure. Leading companies are strengthening their positions through innovation, partnerships, and advanced product offerings. Overall, the ophthalmic devices sector is expected to maintain long-term growth, driven by technology adoption, supportive policies, and increasing global focus on preventive eye care.

View More

Ophthalmic Knives Market || Ophthalmic Drugs Market || Ophthalmic Loupes Market || Ophthalmic Lasers Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)