Table of Contents

Overview

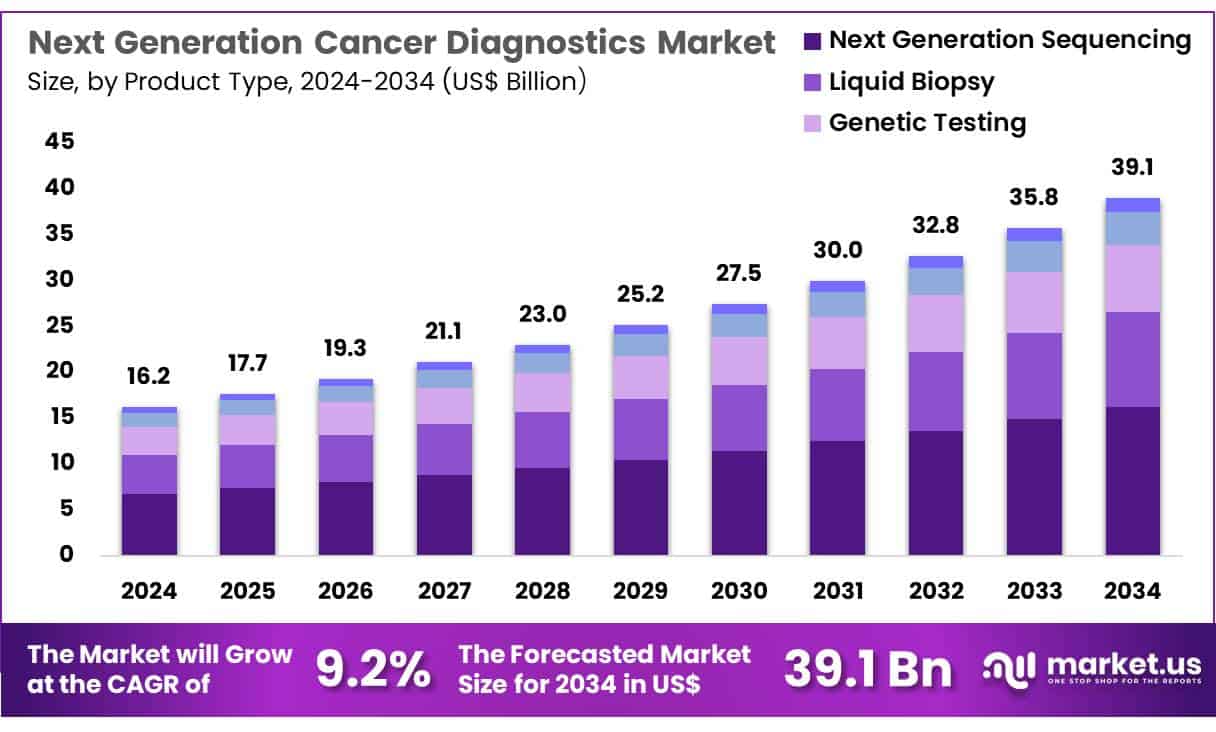

New York, NY – June 04, 2025 – Global Next generation cancer diagnostics Market size is expected to be worth around US$ 39.1 billion by 2034 from US$ 16.2 billion in 2024, growing at a CAGR of 9.2% during the forecast period 2025 to 2034

In 2024, the field of oncology witnessed major advancements with the rapid development of next-generation cancer diagnostics (NGCD). These cutting-edge technologies enable early and accurate detection of cancer by analyzing genetic, molecular, and cellular changes in patient samples often before clinical symptoms appear. NGCD includes tools such as liquid biopsy, next-generation sequencing (NGS), digital pathology, and multiplex biomarkers, offering a transformative shift from traditional methods to more precise, non-invasive approaches.

One of the key breakthroughs involves liquid biopsies, which analyze circulating tumor DNA (ctDNA) from blood samples. This allows for real-time cancer monitoring, recurrence tracking, and therapy response assessment, reducing the need for invasive procedures. Furthermore, the integration of artificial intelligence (AI) and machine learning has significantly improved diagnostic accuracy and data interpretation, enabling faster clinical decision-making.

The rise in cancer incidence worldwide, along with the growing demand for personalized treatment, has accelerated the adoption of NGCD. Government-backed initiatives and global research collaborations are driving innovation, improving patient outcomes while reducing healthcare costs. In the United States, the National Cancer Institute (NCI) continues to fund projects that enhance biomarker discovery and digital diagnostics infrastructure. With strong momentum in both clinical and commercial adoption, next-generation cancer diagnostics are set to redefine cancer care by delivering timely, targeted, and patient-centric solutions across the globe.

Key Takeaways

- In 2023, the market for next-generation cancer diagnostics recorded a revenue of US$ 16.2 billion and is projected to reach US$ 39.1 billion by 2033, growing at a CAGR of 9.2%.

- Based on product type, the market is segmented into liquid biopsy, genetic testing, next-generation sequencing, immunoassays, and radiomics. Among these, next-generation sequencing accounted for the largest share at 41.6% in 2023.

- By application, the market covers breast cancer, colorectal cancer, lung cancer, prostate cancer, and leukemia. Breast cancer diagnostics represented a significant portion, holding an 37.8% market share.

- In terms of end users, the market is categorized into hospitals, research institutions, laboratories, and diagnostic centers. Hospitals emerged as the leading segment, contributing 48.5% of total revenue.

- Regionally, North America dominated the global market in 2023, capturing a share of 39.8%.

Segmentation Analysis

- Product Type Analysis: In 2023, next-generation sequencing (NGS) dominated the product segment with a 41.6% market share, driven by its precision in identifying genetic mutations. NGS allows for comprehensive genomic profiling of tumors, supporting early diagnosis and personalized treatment. Its integration with non-invasive liquid biopsy techniques enhances clinical adoption. As the focus on precision medicine increases, NGS is expected to witness significant growth, offering targeted treatment strategies that improve patient outcomes in cancer diagnostics.

- Application Analysis: Breast cancer accounted for 37.8% of the application segment in 2023, owing to improved diagnostic methods and rising cases worldwide. The adoption of genetic testing and NGS to detect BRCA1 and BRCA2 mutations has bolstered early detection efforts. Technological advances in liquid biopsy and non-invasive tools have further improved diagnostic accuracy. This, combined with the push for precision oncology, supports the growing reliance on next-generation diagnostics for personalized breast cancer management.

- End-User Analysis: Hospitals led the end-user segment with a 48.5% market share in 2023, driven by the demand for advanced diagnostic capabilities. With increasing adoption of NGS, liquid biopsy, and genetic testing, hospitals are central to delivering early, accurate cancer diagnoses. The shift toward precision medicine has spurred investment in specialized diagnostic infrastructure within hospitals, enabling tailored treatment plans and better outcomes. As cancer care becomes more personalized, hospitals are expected to remain the primary users of next-generation cancer diagnostics.

Market Segments

Product Type

- Liquid Biopsy

- Genetic Testing

- Next Generation Sequencing

- Immunoassays

- Radiomics

Application

- Breast Cancer

- Colorectal Cancer

- Lung Cancer

- Prostate Cancer

- Leukemia

End-user

- Hospitals

- Research Institutions

- Laboratories

- Diagnostic Centers

Regional Analysis

North America led the next-generation cancer diagnostics market in 2023, accounting for a 39.8% revenue share. This dominance is attributed to technological advancements, FDA approvals such as Novartis’ Pluvicto for prostate cancer, and a strong focus on precision medicine. The widespread use of liquid biopsy, genomic profiling, and AI-driven diagnostic tools has enabled early cancer detection and personalized treatment.

Strong investments in oncology research, coupled with collaborations between diagnostic firms and research institutions, have accelerated innovation and commercialization. Additionally, expanding healthcare infrastructure, favorable reimbursement policies, and increased awareness among patients and clinicians continue to drive market growth.

Meanwhile, Asia Pacific is projected to register the highest CAGR during the forecast period. The rise in cancer prevalence, combined with increased healthcare investments, is boosting demand for advanced diagnostics. The launch of Australia’s preventive DNA screening program exemplifies the region’s progress in personalized medicine.

Growing access to healthcare in India, China, and Japan, along with supportive government initiatives, is expected to foster rapid market expansion. Collaborations with global diagnostic firms, rising awareness, and advancements in sequencing and bioinformatics are set to improve accessibility and affordability of cutting-edge diagnostics in Asia Pacific.

Emerging Trends

- Integration of Artificial Intelligence (AI): AI-driven methods are being increasingly applied in cancer diagnostics to enhance accuracy and speed. Machine learning algorithms are used to analyze complex datasets such as imaging scans and genomic profiles to detect subtle signals of early-stage tumors. This trend is supported by initiatives from the National Cancer Institute, which highlight AI’s role in improving diagnostic precision and enabling real-time analysis of pathology slides.

- Liquid Biopsy and Circulating Tumor DNA (ctDNA): Diagnostic approaches based on liquid biopsy particularly the analysis of ctDNA fragments in blood are gaining prominence. These non-invasive tests can detect tumor-derived DNA months before changes are visible on imaging, allowing for earlier intervention. Recent NCI publications have noted that ctDNA assays are being optimized to identify minimal residual disease and monitor treatment response across various solid tumors.

- Fragmentomics for Early Detection: Fragmentomics leverages machine learning to analyze the size and end motifs of cell-free DNA fragments in plasma. In preliminary NCI-funded studies, a fragmentomics-based blood test accurately detected early-stage liver cancer in hundreds of participants, demonstrating sensitivities above conventional screening methods. This approach is being investigated for other cancer types, with the goal of broadening early detection capabilities.

- Nanotechnology-Enabled Biosensors: Nanotechnology is being employed to develop ultrasensitive biosensors capable of detecting biomarkers at extremely low concentrations. Nanowires and nanoparticle platforms are under study to improve the sensitivity of protein- and nucleic acid-based assays. The NCI has identified nanotechnology as a key enabler for next-gen diagnostics, enabling earlier detection through high-precision biosensors and point-of-care devices.

- Multi-Cancer Detection Panels: Efforts are underway to create assays that screen for multiple cancer types simultaneously by measuring panels of biomarkers in a single blood sample. The Cancer Screening Research Network (CSRN) plans to launch a Vanguard Study in late 2024 to evaluate multi-cancer detection tests that quantify tumor-derived DNA fragments. These tests aim to identify several cancers at once, potentially raising overall detection rates and reducing missed diagnoses.

Use Cases

- Monitoring Minimal Residual Disease (MRD): Tumor-informed ctDNA assays are being used to detect minimal residual disease in patients after curative-intent therapy. Personalized panels created by sequencing each patient’s tumor to identify somatic mutations are used to track those mutations in plasma. In solid tumors such as colorectal, lung, breast, and bladder cancer, these assays can identify recurrence risk weeks to months before imaging would show disease. This information guides decisions on adjuvant therapy, with studies demonstrating that ctDNA-based MRD tests can detect relapse up to six months earlier than conventional methods.

- Early-Stage Liver Cancer Detection via Fragmentomics: In a preliminary study funded by NCI, a fragmentomics-based blood test was applied to over 300 participants including both healthy controls and patients with early-stage liver cancer. Machine learning models classified fragment patterns with over 85% accuracy for distinguishing cancer from non-cancer samples. This use case highlights how fragmentomics may enable detection of liver cancer at stages I and II, when treatments are most effective.

- Multi-Cancer Screening Trials: The CSRN’s Vanguard Study on multi-cancer detection is designed to enroll approximately 2,000 individuals across several sites in late 2024. Participants will undergo blood tests that measure panels of ctDNA biomarkers. Early data suggest that such tests could detect five to ten different cancer types with sensitivities ranging from 60% to 80% for later-stage tumors and 40% to 50% for early-stage tumors. If successful, this approach could expand to population-level screening and potentially identify cancers before symptoms develop.

Conclusion

Next-generation cancer diagnostics are transforming the global oncology landscape by enabling earlier, more precise, and less invasive cancer detection. Driven by technological advancements in genomic profiling, liquid biopsy, and AI integration, these diagnostics support personalized treatment strategies that improve patient outcomes.

Strong market growth is evident, with North America leading and Asia Pacific emerging rapidly due to healthcare innovation and rising awareness. Backed by initiatives from trusted bodies like the NCI, emerging technologies such as fragmentomics and nanobiosensors are expanding diagnostic capabilities. As adoption increases, next-generation diagnostics are poised to become the cornerstone of future cancer care worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)