Table of Contents

Overview

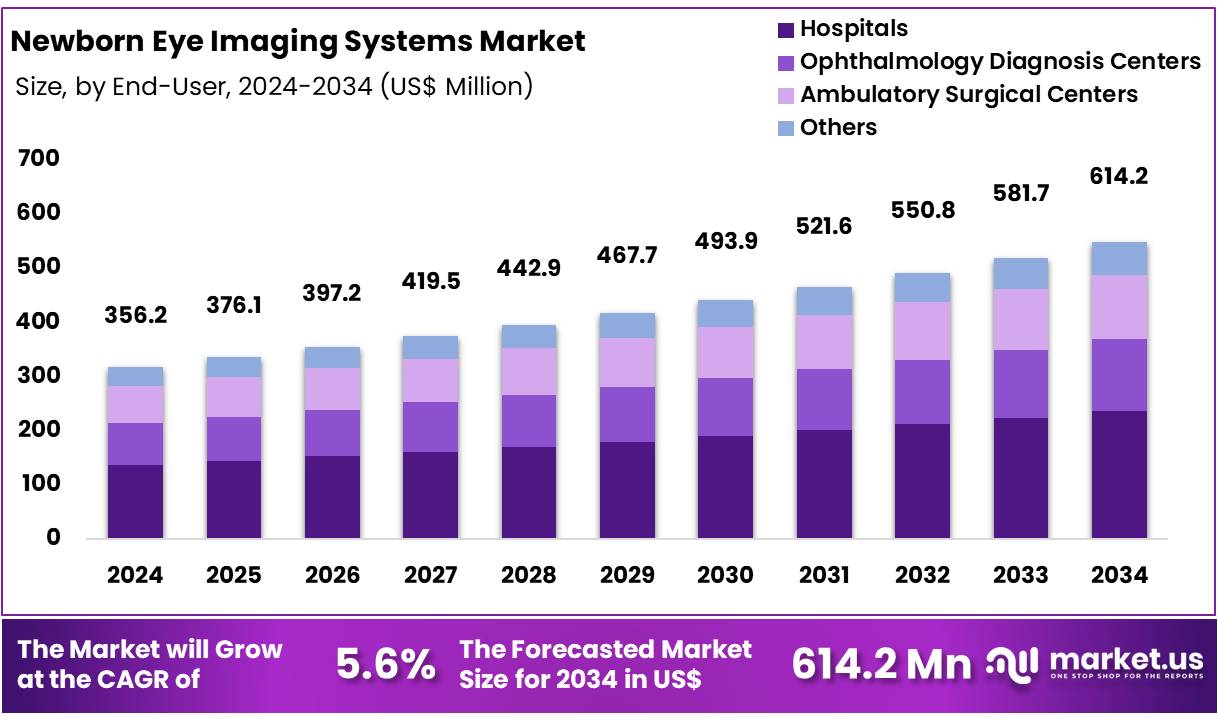

New York, NY – Nov 28, 2025 – Global Newborn Eye Imaging Systems Market size is expected to be worth around US$ 614.2 Million by 2034 from US$ 356.2 Million in 2024, growing at a CAGR of 5.6% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 41.7% share with a revenue of US$ 148.5 Million.

The global adoption of Newborn Eye Imaging Systems has been increasing as healthcare providers prioritize early detection of ocular disorders in infants. The introduction of these systems has enabled hospitals and neonatal care units to identify retinal abnormalities at a significantly earlier stage, supporting timely intervention and improved clinical outcomes. The prevalence of conditions such as retinopathy of prematurity has been increasing in many regions, and the demand for advanced screening technologies has been reinforced as a result.

Newborn Eye Imaging Systems are designed to capture high-resolution retinal images using non-invasive and infant-safe techniques. Their integration into routine neonatal screening programs has been facilitated by technological advancements, including enhanced digital imaging, automated analysis software, and portable device configurations. These innovations have improved diagnostic accuracy and enabled clinical personnel to streamline workflows in busy care environments.

Market growth has also been supported by expanding government initiatives focused on pediatric health and the rising emphasis on early-stage ophthalmic assessment. Strategic partnerships among medical device manufacturers, hospitals, and research institutes have accelerated product development activities, resulting in the availability of more efficient and user-friendly imaging platforms.

The demand for cost-effective and reliable neonatal screening solutions continues to strengthen, and Newborn Eye Imaging Systems are expected to play an essential role in the modernization of neonatal care infrastructure. Increased awareness among healthcare professionals and parents is further contributing to market expansion. The technology is positioned to support preventive healthcare strategies and reinforce global efforts aimed at reducing infant vision impairment.

Key Takeaways

- Market Size: The Global Newborn Eye Imaging Systems Market is projected to reach US$ 614.2 million by 2034, increasing from US$ 356.2 million in 2024.

- Market Growth: The market is anticipated to expand at a CAGR of 5.6% during 2025–2034.

- Disease Type Analysis: The Retinopathy of Prematurity (ROP) segment held the largest share, accounting for 36.5% of the market.

- Device Type Analysis: The Basic Device category dominated the market, representing 56.3% of total share.

- End-Use Analysis: Hospitals remained the leading end-use segment, contributing 38.5% of global revenue.

- Regional Analysis: North America led the market, capturing 41.7% of total global share.

Regional Analysis

In 2024, North America represented 41.7% of the Global Newborn Eye Imaging Systems Market, reaffirming its position as the leading regional contributor. This leadership is supported by the region’s advanced neonatal healthcare systems, strong awareness of early eye screening, and extensive utilization of technologically advanced imaging solutions.

The region benefits from highly specialized neonatal care units and established screening guidelines for conditions such as retinopathy of prematurity (ROP). Well-structured reimbursement policies further facilitate the adoption of newborn eye imaging technologies across healthcare facilities. Continuous investments in teleophthalmology and AI-enabled diagnostic platforms have improved the efficiency, accuracy, and reach of screening programs, including those in underserved regions.

In addition, active collaboration among hospitals, research bodies, and public health agencies enhances the overall capacity to deliver comprehensive newborn eye care. These coordinated efforts support early diagnosis and contribute to improved long-term visual outcomes for infants across North America.

Emerging Trends

- Integration of Artificial Intelligence (AI): AI-enabled algorithms are increasingly being incorporated into newborn eye imaging systems to support automated detection of retinal abnormalities. These tools reduce diagnostic variability, provide real-time assessments, and strengthen early identification of conditions such as retinopathy of prematurity in neonatal care settings.

- Portable and Handheld Devices: The introduction of compact, handheld imaging solutions is enabling point-of-care eye screening in hospitals and remote locations. These devices offer non-invasive, user-friendly imaging capabilities, improving accessibility and reducing infrastructure-related challenges in neonatal eye-care services.

- Telemedicine-Enabled Imaging: Remote data transfer and cloud-based imaging platforms are being adopted to facilitate teleophthalmology consultations. Retinal images captured in distant facilities can be reviewed by specialists, improving access to expert diagnosis and supporting timely interventions for newborns in underserved regions.

- Non-Mydriatic Imaging Advancements: Progress in non-mydriatic imaging technologies allows retinal examinations without pupil dilation, reducing discomfort for infants. These advancements streamline the imaging process, support rapid screenings, and enhance the feasibility of large-scale neonatal eye-care initiatives.

- Integration with Electronic Health Records (EHRs): Newborn eye imaging systems are being linked with electronic health record platforms to ensure streamlined documentation and coordinated care. This integration improves long-term tracking of ocular health and supports more effective communication between pediatric and ophthalmic care teams.

Use Cases

- Screening for Retinopathy of Prematurity (ROP): These imaging systems are extensively used to detect early signs of ROP in premature infants. High-resolution retinal imaging supports timely diagnosis and intervention, reducing the likelihood of permanent vision impairment associated with this condition.

- Diagnosis of Congenital Eye Disorders: Imaging technologies help identify congenital abnormalities such as cataracts, glaucoma, and retinal dystrophies. Early diagnosis ensures prompt clinical management, preventing avoidable vision loss and supporting healthier developmental outcomes for newborns.

- Monitoring Neurological Development: Newborn eye imaging is used to evaluate retinal and optic nerve health, serving as a non-invasive indicator of neurological development. These assessments provide early insights into potential neurodevelopmental issues and guide targeted therapeutic strategies.

- Public Health Screening Programs: Healthcare systems are adopting newborn eye imaging solutions for community-level screening programs. These initiatives support early detection of eye disorders, reduce childhood blindness rates, and enhance access to advanced diagnostics in resource-limited settings.

- Longitudinal Visual Health Tracking: The systems enable continuous monitoring of ocular health from infancy onward. Stored retinal images serve as reference points for tracking disease progression and treatment effectiveness, supporting personalized care and contributing to predictive insights in pediatric ophthalmology.

Frequently Asked Questions on Newborn Eye Imaging Systems

- Why are these systems important in neonatal care?

These systems are essential in neonatal care because they facilitate early identification of conditions such as retinopathy of prematurity. Early diagnosis improves treatment decisions, reduces the risk of vision impairment, and strengthens preventive eye-care practices in vulnerable newborn populations. - How do Newborn Eye Imaging Systems work?

The devices use digital imaging technologies to capture detailed retinal images without causing discomfort. Advanced optics, illumination systems, and software tools allow clinicians to assess retinal health quickly, supporting accurate diagnoses within neonatal intensive care environments. - Are these imaging systems safe for infants?

The systems are designed to meet strict safety standards, using low-intensity illumination and non-invasive techniques. Their operation ensures minimal stress to infants, enabling accurate retinal imaging while maintaining high levels of comfort and safety. - Which conditions can be detected using these systems?

The systems can identify retinopathy of prematurity, congenital cataracts, retinal hemorrhages, and other structural abnormalities. Early detection of these conditions improves clinical outcomes by enabling appropriate intervention during critical stages of neonatal development. - Which region leads the global market?

North America leads the global market due to advanced neonatal healthcare infrastructure, established screening protocols, and strong reimbursement support. High awareness of early eye assessment and adoption of innovative imaging technologies further reinforce regional leadership. - Which segment dominates by disease type?

The Retinopathy of Prematurity segment dominates due to its rising prevalence among premature infants. Healthcare systems prioritize early screening for this condition, increasing demand for high-precision imaging systems that enable timely diagnosis and targeted treatment strategies. - Which end-use sector contributes most to market revenue?

Hospitals contribute the highest share because they manage large volumes of neonatal screenings and possess specialized care units. Their significant investment capacity and adherence to established screening protocols support broader adoption of newborn eye imaging technologies.

Conclusion

The Newborn Eye Imaging Systems Market is experiencing steady expansion as early detection of ocular disorders becomes a priority in neonatal healthcare. Technological advancements, increasing awareness, and supportive government initiatives are strengthening global adoption. North America continues to lead due to advanced infrastructure and established screening practices.

Innovations such as AI integration, handheld devices, telemedicine platforms, and non-mydriatic imaging are enhancing diagnostic accuracy and accessibility. Growing use cases across ROP screening, congenital disorder diagnosis, neurological assessment, and public health programs reinforce the importance of these systems. Overall, the market is positioned for sustained growth, supporting improved visual outcomes for newborns worldwide.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)