Table of Contents

Overview

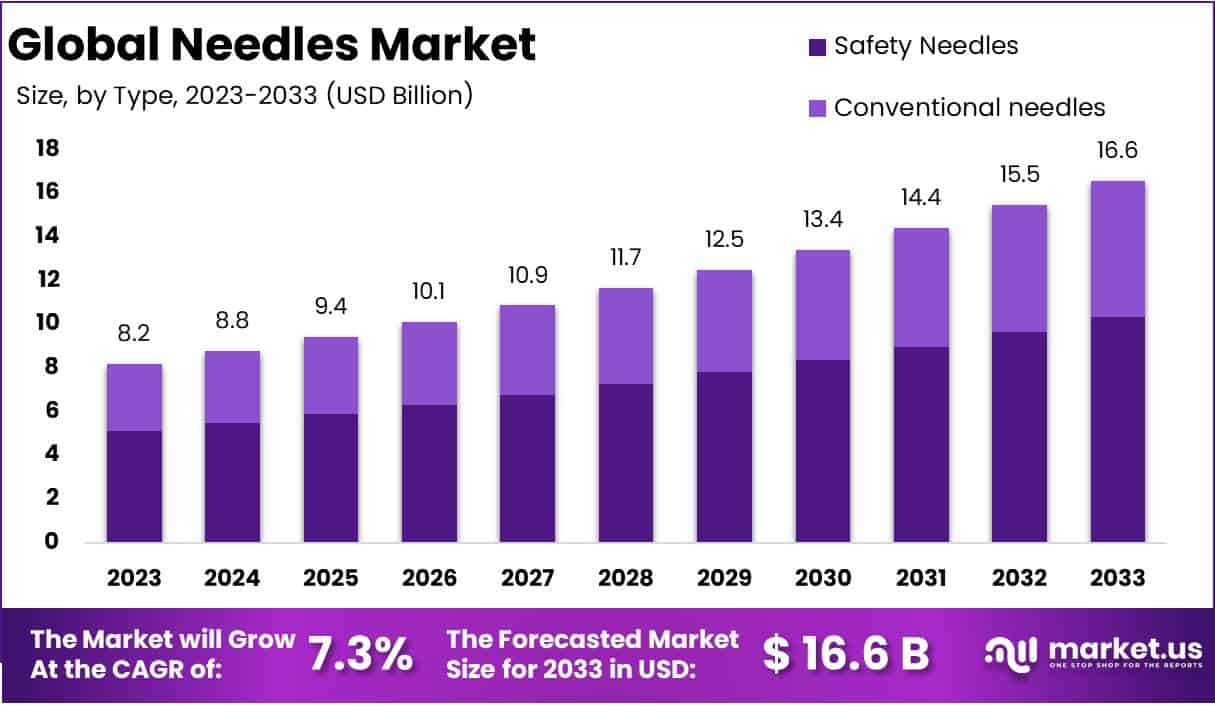

New York, NY – August 22, 2025: The Global Needles Market is projected to grow significantly, reaching around USD 16.6 billion by 2033, up from USD 8.2 billion in 2023, at a CAGR of 7.3% between 2024 and 2033. Needles are widely used for administering medications, drawing blood samples, and supporting vaccination programs. The market expansion is closely tied to the rising elderly population, increasing vaccination demand, and the growing prevalence of chronic diseases. Furthermore, the expansion of hospitals and clinics in developing nations supports the wider adoption of injectable therapies and contributes to steady market growth worldwide.

A major driver of the market is the rising prevalence of cancer and other chronic diseases. Cancer incidence rates continue to increase globally, requiring more frequent use of injectable treatments. Similarly, cardiovascular diseases, diabetes, and infectious conditions contribute to the rising demand for needles. Beyond human healthcare, the growing prevalence of pet diseases also creates additional demand within the veterinary segment. The combination of these factors ensures a consistent market need for needles across multiple healthcare domains, making chronic and acute disease treatment one of the strongest drivers of market expansion.

Technological advancements in needle design are another growth factor. Innovations focus on reducing injection-related pain and anxiety, which are common barriers to treatment adherence. For example, dental injections are strongly associated with discomfort, and research efforts aim to create designs that minimize stress for patients. The development of advanced, patient-friendly needles not only enhances user experience but also supports higher adoption rates. Alongside this, increasing awareness about blood donation is fueling demand for needles and syringes. Voluntary donations help meet blood supply shortages, driving usage across hospitals and blood banks.

Government support and investments in healthcare infrastructure further strengthen the market outlook. Both public and private players are channeling funds into modernizing medical facilities, improving accessibility to advanced treatments, and developing new medical devices. Higher spending on healthcare, particularly in emerging economies, creates lucrative opportunities for manufacturers. Additionally, rising disposable incomes and the introduction of innovative products in hospitals and clinics support broader adoption of advanced injection technologies. These trends enhance the commercial viability of new needle designs and stimulate competition among market players.

The market is also influenced by increasing R&D activities. Companies and healthcare institutions are investing heavily in the development of advanced medical devices, including safer and more efficient needles. Research activities promise high returns, particularly in areas like infectious disease detection and advanced drug delivery systems. Coupled with the increasing pace of drug development, this trend ensures sustained demand for needle technologies. As healthcare facilities adopt cutting-edge devices, the global needles market is set to witness strong, long-term growth, supported by rising demand, innovation, and government-backed healthcare expansion.

Key Takeaways

- The global needle market is projected to hit USD 16.6 billion by 2033, expanding at 7.3% CAGR from USD 8.2 billion in 2023.

- Advances in needle technologies focus on minimizing patient anxiety, with safety needles gaining traction for their infection resistance and reduced operation time benefits.

- Pen needles accounted for more than 62.3% of the market in 2023, largely driven by the increasing global diabetic patient base.

- Hypodermic needles led with a 36% share in 2023, while intravenous needles are expected to experience the fastest growth in coming years.

- Stainless steel needles dominated with 42.3% share in 2023, preferred due to their durability, strength, and potential for reuse in medical procedures.

- Hospitals captured 63.4% of the market in 2023, consistent with WHO guidelines that emphasize safe needle use in healthcare environments.

- Safety needles are projected as the fastest-growing segment ahead, valued for their simplicity, safer design, and lower infection risks compared to conventional options.

- North America led globally with 43.9% market revenue share in 2023, translating into a regional market size worth USD 3.9 billion.

- Rising consumer interest in self-administered medications drives higher demand for self-injectable needle solutions, reducing patient anxiety and increasing treatment convenience.

Regional Analysis

North America holds a dominant position in the global needles market. The region benefits from strong healthcare infrastructure and high investment from key players in advanced medical devices. A well-established distribution network also strengthens its growth. In 2024, North America accounted for more than 43.9% of the revenue share, representing a market value of USD 3.9 billion. The increasing number of research activities further enhances the demand for innovative needle products. This makes North America the leader in terms of revenue and technological adoption.

The Asia-Pacific region is emerging as the fastest-growing market for needles. Factors such as medical tourism, rising healthcare demand, and significant investments in research are driving growth. Patients in this region are increasingly seeking high-quality treatment options. Healthcare providers are expanding their services to meet this demand. Countries like India, China, and South Korea are becoming key contributors to the expansion. This trend is expected to accelerate in the coming years with greater healthcare spending.

There is also a rising demand for blood components in Asia-Pacific and other regions. The increase in surgical procedures and the growing prevalence of chronic and acute diseases are major drivers. Blood disorders, such as anemia and hemophilia, are becoming more common, necessitating frequent diagnostic blood tests. This has created a steady need for medical needles across hospitals and clinics. The market continues to grow as healthcare facilities focus on improving access to diagnostic and therapeutic services. This ensures consistent demand for various needle types.

China is a key contributor to the regional market expansion. The country is experiencing strong growth due to the rising demand for plasma derivatives and therapeutic apheresis. Increasing awareness about advanced treatment methods is also supporting market development. Additionally, the growing number of neoplasm cases is driving the need for advanced needle-based procedures. Healthcare modernization efforts in China further accelerate adoption. With a large population and rising healthcare needs, China is expected to remain a major growth hub in the needles market over the forecast period.

Key Players Analysis

Dickinson and Company

Becton, Dickinson and Company (BD) is a leading producer of needles and syringes within its Medication Delivery Solutions unit. In FY2024, company revenue reached $20.2 billion, supported by strong MDS demand. In Q2 FY2024, the drug-administration unit recorded $2.45 billion in sales. BD increased U.S. syringe manufacturing in March 2024 and installed new needle and syringe lines after investing over $10 million in 2024. In 2025, BD reported U.S. Posiflush output above 750 million units, about a 10% capacity rise, as it continued expansions. These actions are aimed at supply security and steady growth in core injection products.

Johnson & Johnson

Johnson & Johnson participates in the needles market through Ethicon, its wound-closure business supplying surgical suture needles used across many specialties. The company offers more than 200 types of suture needles, enabling selection by tissue, needle geometry, and procedure need. In 2024, Johnson & Johnson MedTech reported $31.9 billion in sales (+4.8% reported). Within MedTech, the Surgery franchise delivered $9.85 billion (–1.9% reported), and General Surgery contributed $5.36 billion (–0.2% reported; +2.0% operational). Growth in General Surgery was attributed to technology penetration and benefits from the differentiated Wound Closure portfolio, alongside increased procedure volumes—indicating sustained demand for sutures and needles across settings. Product quality and vigilance activities were visible in 2024–2025: a Class II recall was initiated for certain PDS II (polydioxanone) sutures (initiated May 10, 2024; posted June 14, 2024), and on December 20, 2024 the company mailed recall notices for selected ETHIBOND EXCEL polyester suture lots (public notice February 4, 2025). Overall, Ethicon’s needle portfolio continued to underpin General Surgery performance in 2024, with ongoing field actions focused on maintaining safety and supply continuity through 2025.

Stryker Corp.

Stryker Corp. operates in the “needles” space primarily through its Interventional Spine portfolio, supplying access and bone-biopsy needles used in vertebral augmentation and vertebroplasty. Its bone-biopsy kits are compatible with 8-, 10-, and 11-gauge needles and enable core sample collection within the vertebral body, supporting diagnosis and cement delivery in compression-fracture care. In 2024, Stryker recorded net sales of $22.6 billion, up 10.2% year over year; within this, MedSurg & Neurotechnology—where Interventional Spine was reclassified in 4Q24—delivered $13.5 billion, up 11.1%, reflecting robust demand for procedure-enabling tools. For 2025, management communicated continued growth expectations, underpinned by healthy end markets. Execution has remained strong: in 2Q25, Stryker’s net sales reached $6.0 billion (+11.1% y/y), while MedSurg & Neurotechnology rose to $3.8 billion (+17.3% y/y). These results, together with the company’s focus on maneuverable needles designed to access the vertebral body and deliver bone cement, indicate sustained utilization in spine procedures and supportive demand for Stryker’s needle solutions through 2024–2025.

Medtronic PLC

Medtronic plc participates in the “needles” space through surgical access and tissue-sampling tools inside its Medical Surgical portfolio. Offerings include pneumoperitoneum/insufflation needles for minimally invasive surgery (Surgineedle™ and Step™/VersaStep™) and aspiration/biopsy needles used in lung and gastrointestinal procedures, such as the superDimension™ aspirating needle and the SharkCore™ fine-needle biopsy (FNB) system for core tissue collection. In fiscal 2025 (year ended April 25, 2025), Medical Surgical sales reached $8.407 billion, essentially flat versus fiscal 2024’s $8.417 billion; Surgical & Endoscopy was also flat year on year. The portfolio covers advanced and general surgical products, endoscopy, interventional lung, and monitoring—areas where needles enable access, diagnosis, and therapy. During early FY2025, management reported low-single-digit organic growth in Endoscopy, while later commentary cited weakness in Stapling offset by strength in Advanced Energy within Surgical & Endoscopy. The company continues to back minimally invasive surgery expansion (“Open-to-MIS”), where these needle products support safer access and better sample quality across GI and lung care pathways.

Conclusion

The global needles market is set for steady growth, supported by rising demand for safe and effective drug delivery, growing chronic disease cases, and strong investments in healthcare infrastructure. Technological advancements, such as patient-friendly and safety-focused needle designs, are improving treatment comfort and adoption worldwide. Expanding hospital networks, higher healthcare spending, and government support in both developed and emerging regions further boost the market outlook. With ongoing research, innovation, and increasing use in human and veterinary healthcare, the needles market is expected to maintain long-term growth, offering manufacturers strong opportunities to expand their product portfolios and strengthen their global presence.

View More:

Pen Needles Market || Hypodermic Needles Market || Acupuncture Needles Market || Medical Injection Needles Market || Aesthetic Needles and Cannulas Market || Endoscopic Ultrasound Needles Market || Biopsy Needle Market || Retractable Needle Safety Syringes Market || Amniocentesis Needle Market || Microneedle Drug Delivery Systems Market || Needle Free Drug Delivery Devices Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)