Table of Contents

Overview

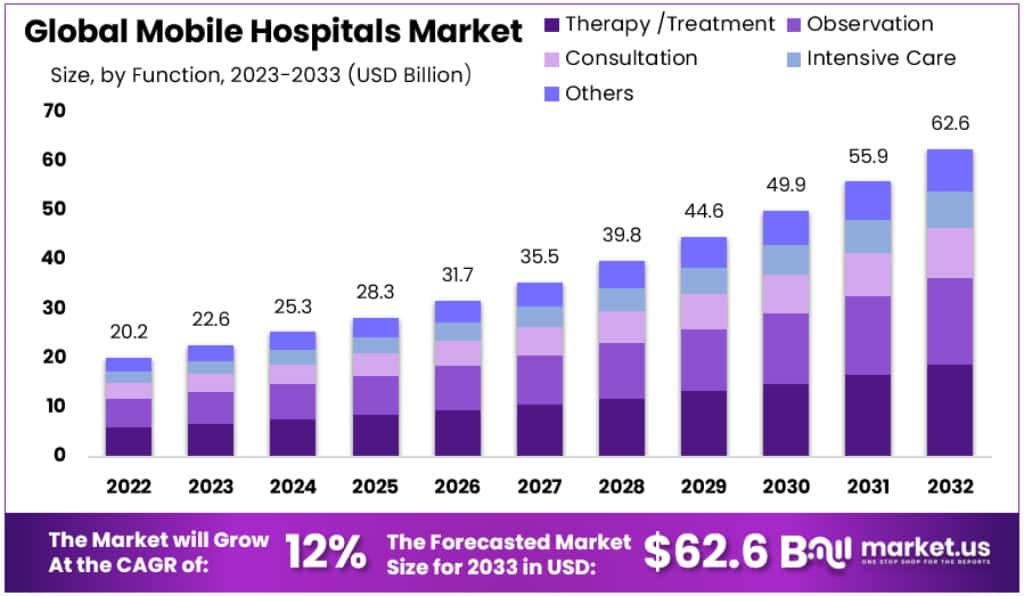

The Global Mobile Hospitals Market is projected to reach USD 62.6 billion by 2033, growing from USD 22.6 billion in 2023 at a CAGR of 12%. Growth is being driven by the increasing frequency and intensity of global health emergencies. According to the World Health Organization (WHO), 42 graded emergencies were active as of January 2025, prompting a US$1.5 billion Health Emergency Appeal. These events highlight the persistent strain on fixed healthcare systems and accelerate the demand for deployable and mobile medical units that can operate in conflict, outbreak, and disaster conditions.

The rising number of attacks on health facilities has intensified the shift toward mobile healthcare. WHO reported over 1,000 annual attacks on health infrastructure in recent years, with 1,065 incidents recorded in 2025 alone. Such disruptions make mobile hospitals a practical alternative for delivering care safely in crisis regions. These platforms ensure continuity of essential services and are increasingly integrated into humanitarian and emergency response frameworks, offering scalable and protected delivery of medical care closer to affected populations.

Government initiatives have moved beyond pilot projects to sustained implementation. India’s National Health Mission (NHM) reported 610 districts equipped with Mobile Medical Units under rural programs and 981 units under the urban NUHM track as of mid-2024. These figures indicate established funding and policy support for mobile healthcare. Similarly, the U.S. Health Resources and Services Administration (HRSA) recognizes mobile care locations as part of routine health center operations, signaling institutional normalization and lowering barriers for private and public investment in mobile platforms.

Mobile diagnostics and preventive outreach programs are also expanding. England’s National Health Service (NHS) achieved a 7.4% improvement in early-stage lung cancer diagnosis in 2023–24 through mobile CT scanning trucks, demonstrating their efficiency in early detection. Global immunization efforts by WHO and UNICEF also rely on mobile units to reach 14.3 million “zero-dose” infants, especially in hard-to-reach regions. These mobile deployments improve access, reduce inequality in service delivery, and strengthen population health outcomes.

Long-term market growth is supported by demographic trends and digital integration. By 2030, one in six people globally will be aged 60 or older, and noncommunicable diseases (NCDs) will account for about 75% of deaths worldwide. Mobile clinics offering chronic care and telehealth-enabled services are bridging accessibility gaps. OECD data confirm sustained post-pandemic teleconsultation use, with 30.1% of U.S. adults using telemedicine in 2022. This hybrid care model enhances service capacity and positions mobile hospitals as a core component of future healthcare systems.

Key Takeaways

- The Global Mobile Hospitals Market is projected to reach nearly USD 62.6 Billion by 2033, increasing from USD 22.6 Billion in 2023.

- Between 2023 and 2033, the market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of approximately 12%.

- In 2023, the Accident & Emergency Care Facility segment accounted for the largest share, representing more than 27.5% of the total market.

- Therapy and Treatment services emerged as the leading service category in 2023, contributing over 29.8% to the overall market revenue.

- North America dominated the global landscape in 2023, securing a 39.8% share, equivalent to a market value of USD 8.3 Billion.

- The Asia Pacific region is expected to demonstrate substantial growth, supported by rising healthcare investments and mobile hospital adoption in India and China.

Regional Analysis

North America continues to dominate the global mobile hospitals market, accounting for an estimated 39.8% share valued at USD 8.3 billion in 2023. The region’s leadership is supported by its robust healthcare infrastructure and a strong focus on technology integration. High investments in advanced medical imaging equipment, such as PET-CT scanners in mobile units, have improved diagnostic precision. These developments have enhanced patient outcomes and contributed to the overall efficiency of mobile healthcare delivery in the region.

The rapid adoption of innovative technologies is transforming North America’s mobile hospital landscape. The integration of digital health tools and portable diagnostic systems has accelerated market expansion. Increasing demand for flexible healthcare access, particularly in rural and disaster-prone areas, is further strengthening regional growth. The presence of leading manufacturers and favorable government initiatives have also ensured a consistent rise in mobile hospital deployments across the United States and Canada.

In contrast, the Asia Pacific region is projected to register the fastest growth during the forecast period. The region’s expansion is driven by rising healthcare expenditure, strategic partnerships, and new product launches. Countries such as China and India are leading this growth due to large populations, rapid urbanization, and increasing healthcare needs in underserved areas. The emphasis on affordable, mobile healthcare services has made mobile hospitals an effective solution to bridge access gaps and improve healthcare delivery.

Additionally, favorable government policies and the expansion of healthcare infrastructure are boosting the Asia Pacific market. Strategic collaborations, mergers, and distribution agreements by key players are enhancing market reach and operational efficiency. Mobile hospitals are being increasingly deployed in remote and rural regions to provide essential medical services. This growing emphasis on accessibility and affordability positions Asia Pacific as a vital contributor to the global mobile hospitals market in the coming years.

Segmentation Analysis

In 2023, the Accident and Emergency Care Facility segment led the mobile hospitals market, holding more than a 27.5% share. This dominance was driven by the rising demand for rapid and accessible healthcare in remote and disaster-affected areas. These facilities deliver immediate medical support and are essential for emergency response operations. Their capability to function efficiently in regions with limited infrastructure highlights their critical role in bridging healthcare accessibility gaps and improving patient outcomes in urgent care situations.

The General Surgery Facility segment also held a substantial share of the market. These mobile units provide essential surgical services in underserved regions, where permanent hospital infrastructure may be unavailable or overburdened. Their flexibility and mobility allow for critical interventions during emergencies or high-demand periods. The ability of such facilities to deliver surgical care in field conditions underscores their growing importance in improving surgical outreach and ensuring continuity of care in challenging environments.

Diagnostics and Imaging Facilities represent another significant portion of the market. These mobile units deliver advanced diagnostic services, including X-ray, ultrasound, and imaging solutions, ensuring early and accurate detection of medical conditions. Their expansion is driven by the global need for improved access to diagnostic capabilities in rural and remote regions. The increasing integration of modern imaging technologies in these units enhances healthcare efficiency and diagnostic precision, making them indispensable for preventive and emergency healthcare systems.

Specialized Surgery, Dental, and Ophthalmic Facilities form niche but vital market segments. Specialized units cater to complex surgical requirements, such as orthopedic or cardiac procedures, where localized expertise is limited. Meanwhile, mobile dental and ophthalmic facilities address essential oral and vision care needs in underserved areas. Additional units dedicated to maternity, pediatric, or mental health care further demonstrate the adaptability of the mobile hospitals market. These segments collectively reflect a strategic effort to deliver comprehensive healthcare beyond traditional hospital settings.

Key Players Analysis

The global mobile hospitals market is characterized by the presence of leading players offering integrated healthcare mobility solutions. Companies such as Alvo Medical, Aspen Medical, and CGS Premier dominate through advanced modular and mobile hospital technologies. Their focus on emergency response, remote healthcare access, and rapid deployment capabilities enhances their market share. These firms leverage strong logistics networks, government contracts, and international partnerships to address the growing demand for accessible healthcare services across disaster-prone and rural regions.

In addition, Saba Palaye and Vanguard Healthcare Solutions have established significant footprints in emerging and developed markets. Their mobile medical units are widely adopted for field hospitals and temporary healthcare setups. Vetter GmbH holds a strong position in Europe, supported by engineering expertise and compliance with regional healthcare regulations. These companies continuously invest in technological innovation, improving the efficiency and durability of mobile healthcare structures, thereby strengthening their competitive positioning and global brand visibility.

Innovative entrants like U-PROJECT have introduced modular healthcare units that combine flexibility and functionality. Their designs cater to both civilian and military healthcare needs, ensuring adaptability in diverse operational conditions. Similarly, EMS Healthcare Ltd. focuses on patient-centered mobile clinic solutions, often utilized in community outreach programs. Their emphasis on cost-effective deployment and quick installation has allowed them to capture market segments in regions requiring short-term healthcare infrastructure expansion.

Regional and niche participants such as La Clinica Health Centers, Coastal Community Health Services, and Lamboo Mobile Medical play crucial roles in extending healthcare access to underserved populations. These organizations specialize in region-specific solutions, often emphasizing preventive care and local health awareness programs. Their localized strategies, coupled with partnerships with government and non-profit entities, enhance healthcare outreach. Collectively, these players contribute to a competitive and evolving market ecosystem that prioritizes innovation, accessibility, and patient well-being.

Conclusion

The global mobile hospitals market is positioned for strong and sustained growth, supported by rising healthcare needs and technological advancements. Increasing global health emergencies and attacks on medical infrastructure have accelerated the adoption of mobile healthcare solutions. These units provide flexible, safe, and efficient care delivery in conflict, rural, and disaster-affected regions. Growing government support, digital integration, and aging populations are further strengthening market demand. The continued use of telemedicine and mobile diagnostics underscores the shift toward accessible and preventive healthcare models. As mobile hospitals become an essential extension of healthcare infrastructure, they are expected to play a central role in improving global health resilience and equity.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)