Table of Contents

Overview

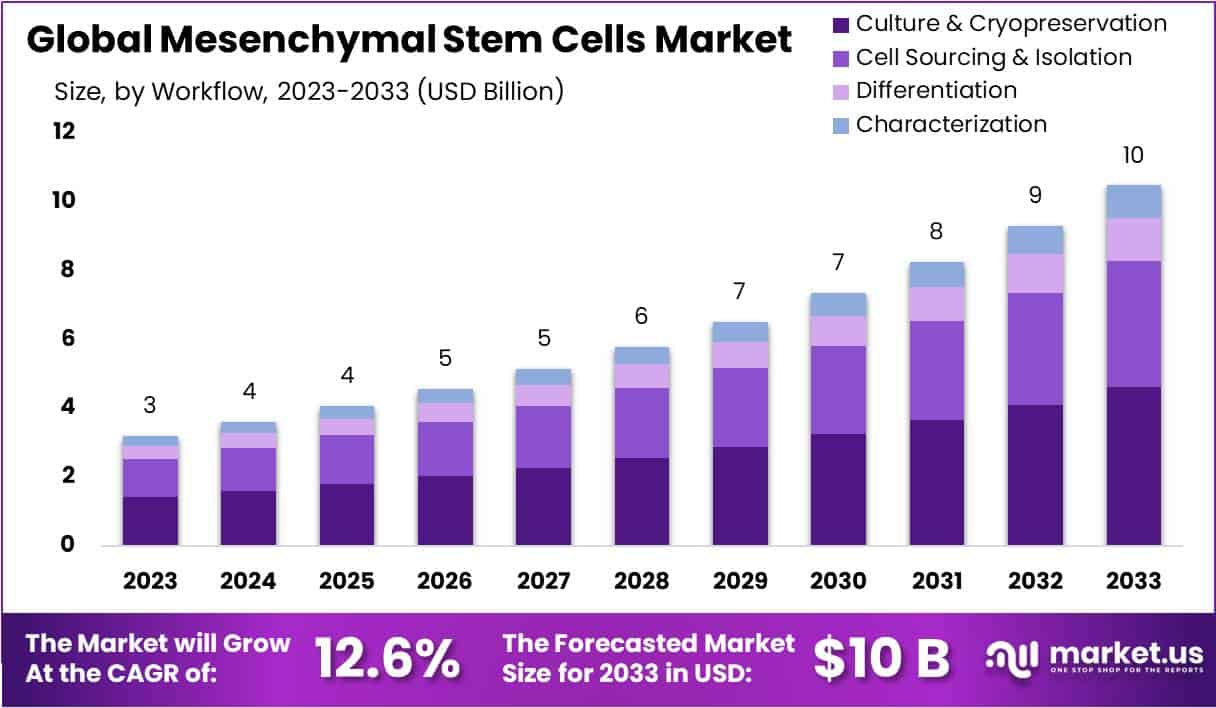

The Mesenchymal Stem Cells (MSC) market is projected to grow significantly over the next decade. Market size is anticipated to expand from USD 3 billion in 2023 to approximately USD 10 billion by 2033. This trajectory represents a compound annual growth rate (CAGR) of 12.6% during 2024–2033. Growth is driven by rising clinical demand, ageing populations, and clearer regulatory pathways. Together, these forces create a strong foundation for the adoption of MSC-based therapies across multiple disease areas.

Demand remains high due to the global burden of musculoskeletal and degenerative conditions. According to the World Health Organization (WHO), musculoskeletal disorders affect about 1.71 billion people worldwide and remain the leading cause of disability. Osteoarthritis alone impacted around 528 million people in 2019. These figures highlight the scale of the patient population in need of effective treatment. MSC therapies are being developed to address unmet needs in joint, spine, cardiovascular, and immune conditions, ensuring a consistent demand pull.

Demographic shifts further reinforce market growth. The United Nations projects a sharp increase in the global 65+ population in the coming decades. Older adults face higher risks of degenerative and inflammatory diseases, directly correlating with MSC-targeted applications. This trend supports continued research investment and clinical development. As the ageing population rises, healthcare systems and industry stakeholders are prioritizing regenerative solutions that preserve mobility, manage pain, and delay the need for invasive surgery.

Clinical research is also accelerating market expansion. ClinicalTrials.gov currently lists over 1,700 MSC-related studies worldwide. These cover diverse indications such as orthopedics, neurology, cardiology, pulmonology, and immune disorders. The scale of these investigations ensures continuous data generation on safety, efficacy, and process optimization. Results from such trials, alongside new partnerships and translational research, enhance confidence in MSC programs. This steady pipeline sustains near-term momentum while laying the foundation for long-term adoption.

Regulatory Support and Market Enablers

Regulatory progress provides significant support to the MSC sector. In the United States, the Food and Drug Administration (FDA) offers the Regenerative Medicine Advanced Therapy (RMAT) designation. This framework accelerates clinical development for qualifying products and enables greater interaction with regulators. Data from the FDA highlight an increase in RMAT requests and approvals, showing sustained developer interest. In Europe, the European Medicines Agency (EMA) regulates cell-based products under the Advanced Therapy Medicinal Products (ATMP) classification, further streamlining market pathways.

Manufacturing guidelines also strengthen market readiness. The World Health Organization’s good manufacturing practice (GMP) standards for biological products are widely referenced by regulators and manufacturers. Adherence to GMP ensures consistent sourcing, testing, and quality control of living-cell therapies. Similarly, FDA guidance clarifies expectations for comparability in cellular therapy manufacturing. Together, these frameworks reduce technical risks, support scale-up, and give investors confidence in the transition from clinical to commercial production.

The persistent burden of musculoskeletal and degenerative disease ensures long-term commercial viability for MSC therapies. WHO data and UN population projections confirm that rising prevalence will continue to pressure healthcare systems. MSC approaches are positioned as viable solutions to preserve function, reduce chronic pain, and postpone costly surgical interventions. This makes them strategically attractive to healthcare providers and payers seeking durable outcomes.

Looking ahead, the sector’s outlook remains cautiously optimistic. Market growth will be driven by ageing demographics, a robust clinical pipeline, supportive regulations, and harmonized manufacturing practices. Success, however, depends on evidence generation in well-controlled trials and real-world studies. Demonstrating safety, efficacy, and cost-effectiveness will be critical. If developers align with international regulatory standards and deliver measurable patient benefits, the MSC market is expected to achieve sustainable expansion through 2033.

Key Takeaways

- The Mesenchymal Stem Cells market is projected to reach USD 10 billion by 2033, expanding at a strong 12.6% CAGR.

- Market expansion is being driven by intensified MSC research, dynamic stem cell advancements, and rising adoption of cell-based therapies worldwide.

- Mesenchymal Stem Cells are gaining therapeutic importance in regenerative medicine, with applications in orthopedic, cardiovascular, autoimmune disorders, and wound healing treatments.

- The Culture and Cryopreservation segment holds a 44.1% market share, ensuring MSC viability and functionality during their entire life cycle.

- Bone marrow remains the leading MSC isolation source, holding 25.1% share, valued for its rich MSC content and clinical accessibility.

- Cardiovascular disease indication dominates the market with 23.2% share, highlighting MSC’s critical role in treating heart-related medical conditions.

- Disease modeling applications account for 23.2% share, enabling controlled laboratory settings for advancing understanding of numerous medical disorders.

- Growing clinical trials and increasing regulatory approvals are fostering market confidence, accelerating widespread adoption of MSC-based therapeutic interventions.

- Market growth is constrained by high treatment costs and limited reimbursement, restricting access for a broader global patient population.

- North America leads with 45.2% market share (USD 1.44 billion), benefiting from advanced research facilities, strong healthcare systems, and early adoption.

- Innovative trends include the rise of MSC-derived exosome therapies, AI integration in research, and regenerative medicine advancements reshaping future treatment landscapes.

Regional Analysis

In 2023, North America established itself as the dominant region in the Mesenchymal Stem Cells Market. The region accounted for more than 45.2% of the global share, reflecting a strong market value of USD 1.44 billion. This leadership highlights the advanced state of the regional market and underlines its importance to the global growth trajectory. The performance is a result of structural strengths and strategic initiatives that continue to shape North America as a leading hub for regenerative medicine research.

The region’s dominance can be attributed to several key factors. Advanced research facilities, coupled with well-established healthcare infrastructure, provide a solid foundation for market expansion. In addition, a proactive approach toward adopting innovative medical technologies has created an environment conducive to stem cell research and commercialization. The presence of thriving pharmaceutical and biotechnology industries further contributes to demand. These strengths collectively ensure North America’s sustained leadership in the Mesenchymal Stem Cells Market, reinforcing its global influence.

The United States plays a crucial role in North America’s strong market position. It hosts a vibrant biopharmaceutical sector and continues to make significant investments in regenerative medicine. Moreover, collaborations between research institutions, industry leaders, and government bodies drive innovation and application. Initiatives supporting clinical research and funding programs also accelerate progress. These activities have not only strengthened the domestic market but have also set benchmarks for global advancements. As a result, the United States remains central to North America’s success in the stem cell landscape.

North America’s commitment to innovation is further supported by a favorable regulatory environment. Policies encouraging scientific progress and market adoption have allowed the region to lead global developments in mesenchymal stem cells. The ability to integrate regulatory flexibility with strong research capabilities positions the region as a global influencer. Moving forward, the reaction of other regions to this dynamic landscape will be critical. Whether North America retains its dominant share will depend on how effectively emerging markets strengthen their infrastructure and investment strategies.

Segmentation Analysis

In 2023, the Culture & Cryopreservation segment held a commanding share of over 44.1% in the mesenchymal stem cells market. This segment plays a crucial role in ensuring the preservation and expansion of cells, maintaining their viability during experimentation and therapy. Growing demand for advanced cryopreservation technologies has propelled this segment forward. The rising emphasis on safeguarding stem cell integrity across clinical and research settings further strengthens its market position. Its dominance highlights its indispensable role in the overall mesenchymal stem cell workflow.

Bone marrow remained the leading source of isolation in 2023, owing to its accessibility and reliability. Cord blood also gained traction due to its ease of collection and high-quality mesenchymal stem cells. Peripheral blood contributed steadily because of its practicality and simple extraction process. Niche sources like fallopian tube and fetal liver demonstrated potential by offering unique properties for therapeutic use. Additionally, adipose tissue showed strong adoption, thanks to its abundance and high yield. Collectively, these sources shape the foundation of stem cell isolation.

Indication analysis showed cardiovascular diseases at the forefront, accounting for 23.2% of the market in 2023. Mesenchymal stem cells demonstrated remarkable potential in supporting cardiac health. Bone and cartilage repair emerged strongly, reflecting increasing demand in musculoskeletal applications. The inflammatory and immunological disease segment grew, underscoring the versatility of stem cells in immune-related disorders. Liver diseases highlighted their therapeutic promise, while oncology applications showed growing adoption. Cancer treatment represents an emerging opportunity for stem cell use, making it a notable area of exploration within regenerative medicine.

Application analysis revealed disease modeling as the top segment with a 23.2% share in 2023. It facilitates controlled simulation of diseases, enabling better understanding of medical conditions. Drug development and discovery also expanded significantly, driven by the critical role of stem cells in novel therapies. Stem cell banking demonstrated considerable growth, aligned with rising demand for preservation in regenerative medicine. Tissue engineering gained traction, supporting efforts to construct functional tissues. Toxicology studies also grew, highlighting their value in safety evaluations. These applications collectively reinforce the expanding utility of mesenchymal stem cells.

Key Players Analysis

Thermo Fisher Scientific Inc holds a leading position in the mesenchymal stem cells (MSC) market. The company is known for innovative technologies and solutions that support advanced MSC research. Its strong product portfolio and global reach make it a key contributor to scientific progress in stem cell applications. With continuous investments in research and development, Thermo Fisher has strengthened its role in enabling breakthroughs across life sciences. Its efforts are vital in expanding the use of MSCs in diagnostics, therapeutics, and biotechnology.

Cell Applications Inc and Axol Biosciences Ltd are significant players advancing MSC research and tools. Cell Applications specializes in providing cell biology solutions, offering high-quality resources that support cellular function studies. Its products are essential for laboratories engaged in MSC development. Axol Biosciences, on the other hand, focuses on human cell-based models and stem cell biology. Its expertise in developing high-quality products strengthens the reliability of MSC research. Together, these companies enhance innovation and provide strong support for regenerative medicine.

Cytori Therapeutics Inc represents the therapeutic side of the MSC market. The company develops novel approaches for regenerative medicine, leveraging MSCs for advanced therapeutic applications. Cytori’s strategies focus on the potential of MSCs in treating various conditions, particularly in tissue repair and regeneration. Its presence highlights the transition of MSCs from research to clinical use. Alongside other players, Cytori demonstrates how research and commercial focus collectively strengthen the market. Together, these organizations drive competition, foster collaboration, and expand the global MSC ecosystem.

Opportunities

1. Immunomodulation Across High-Burden Indications

MSCs regulate immune cells such as T cells, B cells, dendritic cells, and macrophages. This makes them useful in immune-mediated disorders including graft-versus-host disease (GVHD), Crohn’s perianal fistulas, and acute respiratory distress syndrome (ARDS). FDA approval of MSC therapy in GVHD validates the class and reduces risk for similar indications. This approval creates confidence for further clinical use. The mechanism of action is broad, and the potential to target multiple conditions is strong. MSCs are seen as flexible tools for modulating immunity, positioning them well in the evolving cell therapy market.

2. Allogeneic, “Off-the-Shelf” Products

MSCs are typically low in immunogenicity, which allows use in allogeneic formats. These can be banked, cryopreserved, and delivered as ready-to-use therapies. This approach enables rapid treatment compared to autologous products, where delays are common. Health authorities have also created clear categories for human cell and tissue products (HCT/Ps). These guidelines help companies plan development and ensure regulatory alignment. Comparability and safety requirements are better understood today. With scalable manufacturing, allogeneic MSCs support broader access and faster adoption. They combine convenience, cost efficiency, and clinical potential, making them attractive for both developers and healthcare systems.

3. Secretome and Extracellular Vesicles (EVs)

MSCs release bioactive molecules and extracellular vesicles (EVs), also known as exosomes. These EVs provide the therapeutic benefits of MSCs without requiring whole-cell infusion. They are easier to standardize, store, and deliver. Studies published in 2024 highlight their potential in tissue regeneration and theranostics, which combine therapy with diagnostics. EVs may offer improved safety, simpler logistics, and predictable dosing. This innovation expands the MSC pipeline into new forms of therapy. Researchers and companies are investing heavily in EVs, viewing them as a natural extension of MSC-based solutions. This opportunity could redefine cell-free regenerative medicine.

4. Combination Products and Biomaterials

MSC effectiveness can be enhanced when combined with biomaterials such as scaffolds, hydrogels, or 3D constructs. These support better engraftment at the target site and address the issue of pulmonary trapping after intravenous dosing. Orthopedic and wound healing fields are exploring these methods with growing interest. Research highlights how biomaterials improve delivery and retention of therapeutic cells. Combination products can create longer-lasting results and reduce treatment variability. Manufacturing refinements are being published, offering guidance for developers. These approaches move beyond cell infusion, offering advanced solutions for complex tissue repair. The synergy of cells and materials is a key growth driver.

5. Growing Regulatory Toolkits

The regulatory environment for cell and gene therapies has become clearer. Programs such as expedited approval pathways and guidance on minimal manipulation and homologous use are available. These frameworks set standards for manufacturing, clinical evidence, and device use with MSCs. Companies that align with these criteria may benefit from shorter development timelines. Regulators now offer more predictable expectations, reducing uncertainty. As MSC products evolve, compliance strategies are easier to define. This progress supports faster innovation and broader clinical application. With strong regulatory pathways, MSCs are positioned to expand into mainstream therapeutic markets more efficiently.

Challenges

1. Biological heterogeneity and nomenclature

Mesenchymal stem cells (MSCs) are highly diverse. They differ by tissue source, donor, and processing method. Even the term “stem” versus “stromal” is still debated. The International Society for Cell and Gene Therapy (ISCT) has issued position statements, including the 2006 “minimal criteria.” However, these efforts have not removed variability. Researchers still find it difficult to compare results across studies and manufacturing lots. This lack of consistency slows progress and creates challenges in clinical translation. Greater agreement on definitions and classification is needed to reduce confusion and strengthen scientific comparisons.

2. Potency assays and critical quality attributes

Potency assays for MSCs are still developing. Robust tests that link potency to mechanisms of action are limited. Universal critical quality attributes (CQAs) have not yet been established. This limits comparability between manufacturing lots. It also reduces regulatory confidence. Clinical effects are believed to rely mostly on paracrine activity, which adds complexity. Recent expert reviews have stressed the need for standardized “hallmarks” of pharmacology. Clearer assays would improve both scientific reliability and regulatory approval. Standardization in potency testing is essential to prove consistency and enable broader therapeutic use.

3. Manufacturing scale-up and consistency

Scaling up MSC production presents serious challenges. Donor variability, cell culture conditions, passage number, and cryopreservation affect cell quality. These factors can reduce cell viability and alter function. Ensuring consistency across batches while expanding production is difficult. Regulatory bodies demand proof that manufacturing changes do not alter clinical performance. This adds time and cost to development. Without stable processes, clinical outcomes may vary widely. Reliable manufacturing systems are critical to reduce risks. Establishing strong comparability data is also necessary to gain regulatory approval and build trust in large-scale production.

4. Delivery, dosing, and biodistribution

Optimizing MSC delivery remains unresolved. Intravenous infusion often causes pulmonary “first-pass” trapping. This limits the number of cells reaching target tissues. Local administration may improve delivery but can be invasive and inconsistent. Researchers continue to study the best route, dose, and schedule. Trial results remain mixed across different diseases and patient groups. The lack of reliable biodistribution data adds complexity. Success depends on identifying safe, effective, and repeatable delivery strategies. Without this, therapeutic outcomes remain unpredictable. Improving administration methods is a major step toward clinical success for MSC therapies.

5. Mixed late-stage clinical readouts and payer scrutiny

Late-stage clinical trials for MSCs have shown mixed results. Some confirmatory studies have failed. For example, the EU withdrawal of darvadstrocel followed negative trial outcomes. These results highlight the need for durable and reproducible efficacy. Health technology assessment (HTA) bodies and payers will demand strong evidence. They expect robust endpoints, longer follow-ups, and real-world data. Cost justification will depend on consistent clinical performance. Without these, payer acceptance will remain limited. Demonstrating clear, long-term benefit is critical for market access and sustainable adoption of MSC-based therapies worldwide.

6. Regulatory classification and manipulation rules

Regulatory rules create further challenges. MSC projects face strict review under “minimal manipulation” and “homologous use” definitions. If cells fall outside these categories, they are treated as advanced biologics. This triggers stricter regulations, longer timelines, and higher costs. Developers must carefully evaluate whether their processes qualify as minimal manipulation. Homology between tissue source and therapeutic use is also closely examined. Falling outside these definitions can significantly delay development. Regulatory classification is therefore a critical factor in planning. Careful alignment with legal frameworks is essential to avoid costly setbacks.

Conclusion

The mesenchymal stem cells market is set for strong and steady growth, supported by ageing populations, high disease burdens, and clearer regulatory support. Rising demand for advanced regenerative solutions is encouraging research, clinical trials, and investment in this field. Progress in manufacturing, cryopreservation, and regulatory alignment is creating a more reliable pathway for clinical adoption. While challenges such as costs, delivery methods, and standardization remain, ongoing innovation in exosome therapies, biomaterials, and off-the-shelf products is opening new opportunities. With evidence of safety, efficacy, and cost-effectiveness, MSC therapies are expected to strengthen their role in global healthcare and achieve sustainable long-term growth.

View More

Cancer Stem Cells Market || Induced Pluripotent Stem Cells Production Market || Induced Pluripotent Stem Cells Market || Cell Counting Market || Autologous Cell Therapy Market || Cell Culture Market || Cell Harvesting System Market || Cell Culture Media Market || Stem Cell Banking Market || Cell And Gene Therapy Manufacturing Market || Cell and Gene Therapy CDMO Market

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)