Table of Contents

Overview

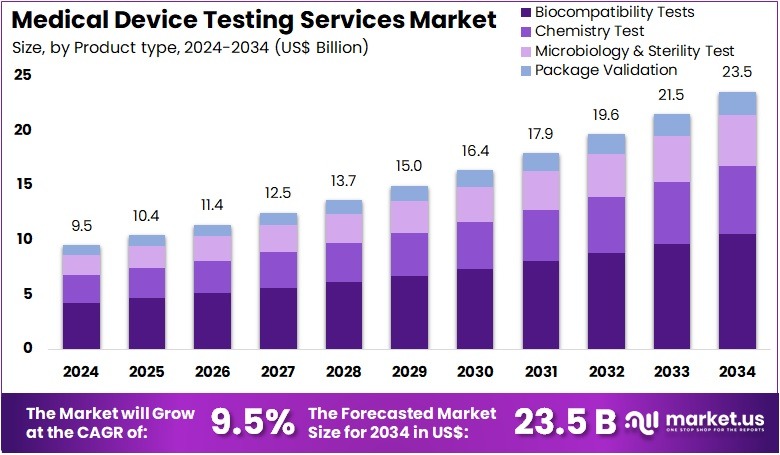

New York, NY – July 29, 2025 – The Medical Device Testing Services Market Size is expected to be worth around US$ 23.5 billion by 2034 from US$ 9.5 billion in 2024, growing at a CAGR of 9.5% during the forecast period 2025 to 2034.

In 2024, the global medical device testing services market is experiencing notable expansion, driven by stringent regulatory standards, growing device complexity, and increased demand for safety and performance validation. As medical devices play an essential role in patient care, ensuring their efficacy, biocompatibility, and compliance with global standards has become paramount.

Testing services include biocompatibility, sterility, electrical safety, performance evaluation, and regulatory consulting. With the increasing adoption of wearable and implantable devices, demand for both preclinical and post-market testing has intensified. Outsourced testing providers are increasingly supporting manufacturers in meeting ISO 13485, FDA, MDR (EU Medical Device Regulation), and other international compliance requirements.

Technological advancements such as AI-driven diagnostics and connected medical systems are also boosting the need for cybersecurity assessments, usability testing, and electromagnetic compatibility evaluations.

North America currently leads the market due to the presence of established testing laboratories and a highly regulated environment, while the Asia Pacific region is projected to witness the fastest growth owing to rapid medical device manufacturing expansion and rising exports.

The industry is further supported by government initiatives to enhance patient safety, improve device reliability, and streamline product approval processes. As innovation in healthcare technology accelerates, the medical device testing services market is expected to remain a critical enabler of product development and global market access.

Key Takeaways

- In 2024, the global medical device testing services market generated a revenue of US$ 9.5 billion and is projected to reach US$ 23.5 billion by 2034, expanding at a CAGR of 9.5% during the forecast period.

- Based on product type, the market is segmented into biocompatibility tests, chemistry tests, microbiology & sterility tests, and package validation. Among these, biocompatibility tests dominated in 2023, accounting for the largest share of 44.7%.

- By application, the market is categorized into preclinical and clinical*testing. The clinical segment emerged as the leading contributor, holding a significant share of 61.5% in 2023.

- Regionally, North America held the largest market share, contributing 41.2% of the global revenue in 2023, driven by stringent regulatory frameworks and the presence of advanced testing infrastructure.

Segmentation Analysis

- Product Type Analysis (Biocompatibility Tests): The biocompatibility tests segment accounted for 44.7% of the market, driven by growing regulatory mandates to ensure device safety and prevent adverse biological reactions. The increasing use of implantable and wearable medical devices is accelerating demand for these evaluations. Advancements in materials science and testing methods have enhanced precision and reduced turnaround times. Regulatory authorities such as the FDA and ISO continue to enforce stringent biocompatibility guidelines, supporting the segment’s long-term growth trajectory.

- Application Analysis (Clinical Testing): The clinical application segment held a dominant 61.5% share, attributed to the rising need for human-based validation of medical devices. Growing concerns about patient safety and device efficacy have made clinical trials essential prior to market entry. Improvements in trial design and digital technologies enable faster and more accurate data collection. Additionally, increasing innovation in fields like orthopedics and cardiology, coupled with stricter regulatory demands for clinical evidence, is fueling steady growth in this segment.

Market Segments

By Product Type

- Biocompatibility Tests

- Orthopedic Device’s Biocompatibility Tests

- Ophthalmic Implantation Device’s Biocompatibility Tests

- Neurosurgical Implantation Devices Biocompatibility Tests

- General Surgery Implantation Devices Biocompatibility Tests

- Dermal Filler’s Biocompatibility Tests

- Dental Implant Devices’ Biocompatibility Tests

- Cardiovascular Device’s Biocompatibility Tests

- Others

- Chemistry Test

- Toxicological Risk Assessment and consulting

- Chemical characterization (E&L)

- Analytical method development and validation

- Microbiology & Sterility Test

- Sterility Test & Validation

- Pyrogen & Endotoxin Testing

- Bioburden Determination

- Antimicrobial Testing

- Others

- Package Validation

By Application

- Preclinical

- Large animal research

- Microbiology & Sterility Test

- Chemistry Test

- Biocompatibility Tests

- Small animal research

- Microbiology & Sterility Test

- Chemistry Test

- Biocompatibility Tests

- Large animal research

- Clinical

Regional Analysis

North America Leads the Medical Device Testing Services Market

North America accounted for the largest market share of 41.2%, driven by stringent regulatory frameworks enforced by the FDA and the increasing complexity of medical devices. The FDA’s focus on thorough pre-market approvals and safety validation continues to fuel demand for comprehensive testing services. The high volume of device manufacturing in the U.S. necessitates robust testing infrastructure. As of April 2024, clinicaltrials.gov reported a substantial number of active medical device trials, highlighting the region’s ongoing innovation and development.

Asia Pacific to Witness Fastest Growth Rate

The Asia Pacific region is projected to register the highest CAGR during the forecast period, supported by a rapidly growing medical device manufacturing industry, particularly in China and India. The adoption of more rigorous quality standards and evolving regulatory frameworks is driving increased reliance on testing services. Notably, in March 2024, Stryker launched a new testing facility in India to strengthen its R&D efforts reflecting rising investment in quality assurance. In addition, the region’s diverse patient population and growing healthcare infrastructure contribute to a favorable environment for accelerated market expansion.

Emerging Trends

Stricter Regulatory Oversight of Laboratory-Developed Tests (LDTs)

The U.S. FDA has redefined many laboratory-developed diagnostic tests as medical devices. These must now be registered, report adverse events, and within a phased four-year timeline undergo FDA review for accuracy and safety, with high-risk tests prioritized.

Expansion of AI-Enabled Device Testing

The FDA has introduced a public listing for AI-enabled medical devices. It expects that such devices meet rigorous review processes tailored to safety, effectiveness, traceability, and transparency in machine-learning components.

Cybersecurity Validation Requirements

Under EU’s Medical Device Regulation (MDR) and IVDR, new rules mandate explicit cybersecurity risk management. Testing must account for security risks, resilience, and compliance with standards such as ISO14971 and IEC60601-1-2.

Digital Twin Simulation for Large-Scale Testing

Innovative research (e.g. MeDeT) demonstrates the use of high-fidelity digital twins for system integration testing. Fidelity rates above 96% and scalability to 1,000 device simulations allow cost-effective validation of evolving devices.

Integration of Point-of-Care and Multiplexed Device Testing

Testing for point-of-care devices (e.g. handheld blood-glucose, rapid diagnostics) and multiplexed assays (xPOCT) is increasing. These require validation under real-world conditions and often simultaneous analyte detection from a single sample.

Use Cases

Pre-market Clinical and Biocompatibility Testing

Manufacturers of implantable devices (e.g. orthopedic or cardiovascular implants) conduct chemical, mechanical, sterility, and biocompatibility tests. Biocompatibility comprised roughly USD4.8billion of the global testing services revenue in 2024 nearly 50% of the market.

Purpose: to prove safety in contact with tissue, durability under use, and compliance with IEC60601 and ISO14971 risk standards.

Software Validation & Human Factors (Usability Testing)

Software-driven devices (SaMD) must undergo validation as per IEC62304 and risk analysis via ISO14971. FDA requires human factors testing to show that intended users can operate the device without error in real-use conditions.

Numeric example: nearly all Class II and III devices (representing a majority of submissions) must include formal human-factors validation.

Cybersecurity and Electromagnetic Compliance Testing

Devices with Wi-Fi, Bluetooth, or network connectivity are tested for susceptibility to electromagnetic interference and cyber threats. Compliance with IEC60601-1-2 and risk-based EMI management is mandatory in EU and U.S. regulatory regimes.

Use Case: Connected infusion pumps, pacemakers, or wireless monitors must show immunity and resilience under defined interference scenarios.

Point-of-Care and Multiplexed Assay Verification

Testing labs validate point-of-care tests such as rapid COVID-19 assays, multi-marker cancer tests, or nutritional status panels (e.g. iron, vitamin D, B12), often yielding results within minutes.

Scale: Multiplexed point-of-care testing (xPOCT) enables simultaneous measurement of multiple analytes. Its adoption is rising in clinics and home-use settings, especially in resource-limited regions.

Digital Twin-Based Integration Testing

Testing of device ecosystems (e.g. IoT medical systems) is supported via digital twins. The MeDeT method demonstrated generating digital replicas with >96% fidelity, adaptable across device versions in approximately 1 minute, and scaled to 1,000 concurrent simulations.

Conclusion

The global medical device testing services market is poised for sustained growth, driven by stringent regulatory requirements, rising device complexity, and the proliferation of connected and implantable technologies. The dominance of biocompatibility and clinical testing underscores the critical focus on safety and human efficacy.

North America remains the largest market due to advanced regulatory infrastructure, while Asia Pacific is emerging rapidly with growing manufacturing capabilities. Technological advancements, including AI-enabled diagnostics, cybersecurity protocols, and digital twin simulations, are reshaping testing methodologies. As innovation accelerates, robust testing services will remain essential for global compliance, patient safety, and successful device commercialization.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)