Table of Contents

Overview

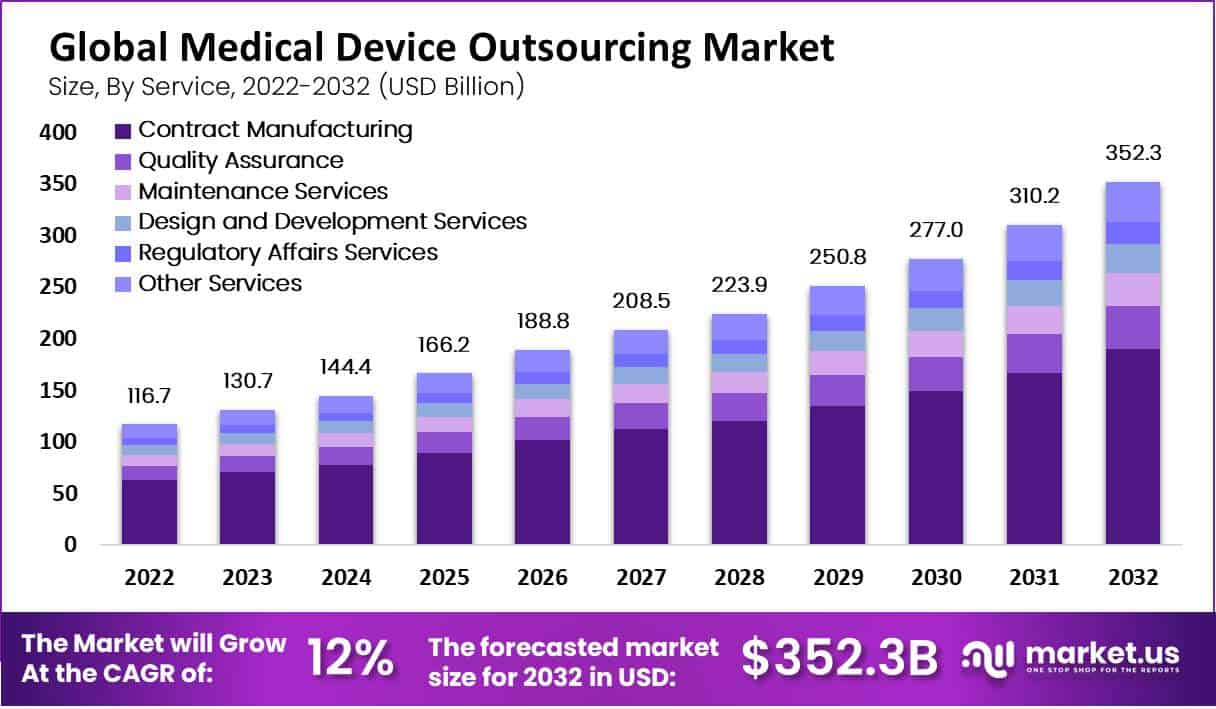

New York, NY – Aug 21, 2025 – Global Medical Device Outsourcing Market size is expected to be worth around USD 352.3 Billion by 2032 from USD 130.7 Billion in 2023, growing at a CAGR of 12.0% during the forecast period from 2023 to 2032.

The global Medical Device Outsourcing market is experiencing robust expansion, driven by the increasing need for cost optimization, regulatory compliance, and rapid product development. Outsourcing has emerged as a strategic approach adopted by OEMs (Original Equipment Manufacturers) to enhance operational efficiency and focus on core competencies.

The market is being propelled by growing complexities in device design, stringent regulatory frameworks, and the rising demand for technologically advanced and high-quality medical devices. Contract manufacturers, especially those with regulatory expertise and strong quality management systems, are gaining traction as preferred partners.

Segments such as Class II and Class III devices are witnessing heightened outsourcing activity due to their intricate design and regulatory requirements. Key services include device design, prototyping, component manufacturing, assembly, packaging, and regulatory consulting.

North America continues to lead the global market, attributed to the presence of major OEMs and established regulatory standards. However, Asia-Pacific is projected to record the fastest growth, driven by lower production costs, expanding healthcare infrastructure, and skilled labor availability.

Strategic collaborations, mergers, and investments in innovation by outsourcing firms are further shaping the competitive landscape. The growth of this market reflects a shift toward integrated service models and value-based partnerships, making outsourcing a cornerstone strategy for long-term competitiveness in the medical device industry.

Key Takeaways

- Market Size: The Medical Device Outsourcing Market was valued at USD 130.7 billion in 2023 and is projected to reach approximately USD 352.3 billion by 2033, registering a CAGR of 12.0% during the forecast period (2023–2032).

- Service Segment: Contract manufacturing is the leading service category, accounting for 53.8% of total revenue.

- Device Class Segment: Class II medical devices, considered moderate to high risk, dominate the market with a 64.8% share.

- Application Segment: Cardiology holds the largest application share, supported by the increasing prevalence of cardiovascular diseases.

- Regional Insights: The Asia Pacific region leads with a 40.6% revenue share, followed by North America, which shows substantial growth opportunities.

- Key Players: Prominent companies in this market include IQVIA Inc., SGS SA, Eurofins Scientific, Intertek Group plc, WuXiAppTec, Charles River Laboratories, PAREXEL International Corporation, Pace Analytical Services Inc., Sterigenics U.S. LLC, Freyr Solutions, among others.

Company Analysis

- IQVIA Inc.: IQVIA announced in April 2024 the acquisition of Clinipace, a global clinical research organization. This strategic move is expected to augment IQVIA’s footprint in clinical trial services catering to medical device firms, particularly enhancing regulatory consulting and clinical development capabilities to better support device clients in outsourcing clinical functions.

- SGS SA: In mid-2024 and early 2025, SGS relaunched its M&A strategy, executing multiple bolt-on acquisitions, and in July 2024 notably agreed to acquire Gossamer a cybersecurity testing provider for connected devices. This supports SGS’s expansion in digital trust and medical device testing, aligning with regulatory trends in connected medical device safety.

- Eurofins Scientific: In September 2024, Eurofins completed the acquisition of Infinity Laboratories, thereby expanding its microbiology, chemistry, sterilisation, and packaging testing services across the United States. This acquisition broadens Eurofins’ laboratory footprint and strengthens its medical device testing capabilities for packaging and sterilisation compliance.

- Intertek Group plc: Although no recent medical device-specific acquisitions have been identified, Intertek continues to offer a comprehensive suite of scientific testing services including for cardiovascular implants, stents, diagnostics, and other devices—supporting its role in the medical device outsourcing market.

- WuXi AppTec: WuXi AppTec divested its U.S. medical device testing facilities in Minnesota and Georgia, with the sale completed on February 28, 2025, to NAMSA. This divestiture reflects strategic realignment and has implications for outsourcing capacity dynamics in the U.S. testing market.

- Charles River Laboratories: Charles River finalized the acquisition of MPI Research, valued at approximately USD 800 million. This purchase enhances Charles River’s preclinical testing capabilities, reinforcing its position as a CRO serving medical device developers with outsourced laboratory services.

- PAREXEL International Corporation: In February 2017, PAREXEL entered into a definitive agreement to acquire The Medical Affairs Company (TMAC), thereby strengthening its outsourced medical affairs and commercialization services across pharmaceutical, biotechnology, and medical device sectors expanding its reach into regulatory and advisory capabilities.

- Pace Analytical Services Inc.: In September 2024, Pace Life Sciences acquired Catalent’s Analytical Services Laboratory in Research Triangle Park. This expanded Pace’s small-molecule and analytical capacity, indirectly bolstering its outsourced testing services that serve the medical device industry’s analytical and manufacturing support needs.

Conclusion

The medical device outsourcing market is poised for sustained growth, driven by rising demand for cost-effective manufacturing, regulatory compliance, and rapid innovation. Dominated by contract manufacturing and Class II devices, the market reflects strong demand across cardiology and surgical applications.

Asia-Pacific leads in regional growth, while North America remains a key contributor. Strategic acquisitions and investments by major players such as IQVIA, Eurofins, and SGS are reshaping the competitive landscape. With increasing regulatory complexity and emphasis on quality, outsourcing is expected to remain a core strategy, enabling OEMs to accelerate time-to-market while maintaining operational efficiency and global competitiveness.

Discuss your needs with our analyst

Please share your requirements with more details so our analyst can check if they can solve your problem(s)